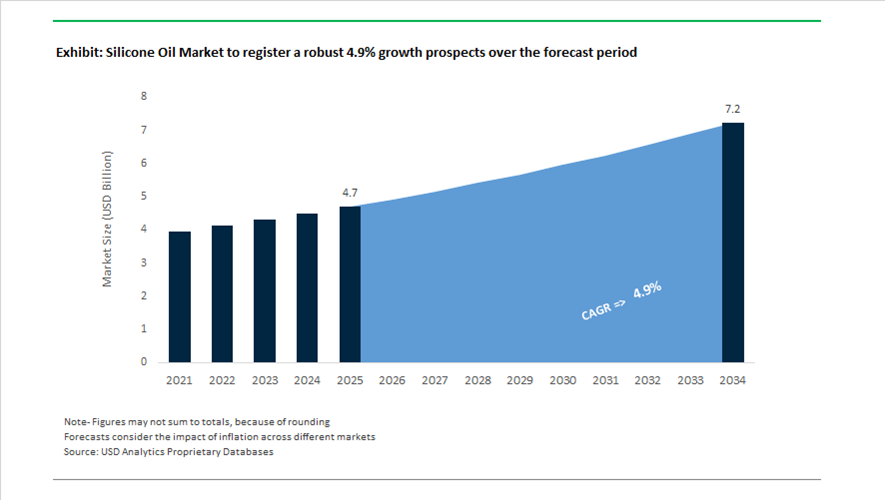

Silicone Oil Market Valuation 2025–2034: $4.7 Billion to $7.2 Billion at 4.9% CAGR Led by High-Purity Electronics and Sustainable Formulations

The global silicone oil market is valued at $4.7 billion in 2025 and is projected to reach $7.2 billion by 2034, registering a CAGR of 4.9%. Market expansion is supported by growing demand for polydimethylsiloxane (PDMS) oils, dielectric silicone fluids, high-temperature lubricants, cosmetic-grade silicone oils, and thermal management fluids across semiconductor fabrication, EV battery systems, medical devices, personal care, and industrial coatings. Silicone oils offer superior thermal stability, electrical insulation, oxidative resistance, low surface tension, and moisture repellency, making them essential in advanced electronics cooling, precision lubrication, and high-performance cosmetic formulations. The transition toward higher-margin medical and electronics grades, coupled with tightening environmental regulations on cyclic silicones, is reshaping product portfolios and pricing strategies across the value chain.

In 2024, KCC Corporation completed the full acquisition of Momentive Performance Materials and subsequently merged its Korean silicone operations with Momentive in January 2025. This consolidation integrates global R&D capabilities for advanced silicone oils used in thermal management systems, specialty lubricants, and automotive electronics encapsulation. In November 2025, DuPont finalized the spinoff of its electronics division into Qnity Electronics, which now manages high-purity silicone oils and dielectric fluids designed for semiconductor manufacturing and high-density chip cooling applications. In September 2025, Wacker Chemie showcased its α3 silane-silicone technology, focusing on functional silicone fluids with enhanced moisture-curing efficiency and improved storage stability for industrial adhesives and coatings.

Pricing discipline and sustainability-focused innovation defined 2025 activity. Effective April 20, 2025, Dow implemented a global 5%–10% price increase across its silicone oils and fluids portfolio, citing an 18% rise in silicon metal costs and a strategic repositioning toward premium medical and electronics segments. In May 2025, Dow introduced its Decarbia™ reduced-carbon platform, featuring low-carbon silicone fluids verified by third-party Environmental Product Declarations. In November 2025, Dow launched DOWSIL™ CB-2251 at in-cosmetics Asia, targeting high-performance hair conditioning with improved deposition efficiency and clean-label compliance.

Structural realignment intensified in 2026. In February 2026, Elkem ASA signed a definitive agreement to divest the majority of its Silicones division to Bluestar, consolidating silicone oil and fluid assets under Bluestar’s specialty chemicals portfolio while Elkem transitions into a metals-focused entity. The same month, Elkem’s MIRASIL™ N-DML 15 received a SEAL Environmental Initiative Award for replacing volatile cyclic silicones such as D4 and D5 in personal care formulations with long-chain alternatives aligned with EU regulatory direction. REC Silicon confirmed in early 2026 that its Butte, Montana facility is concentrating on monosilane gas and oil production for silicon-anode battery technologies following the 2024 shutdown of polysilicon lines. Shin-Etsu Chemical is on schedule to complete its ¥2.1 billion Zhejiang facility in February 2026, dedicated to high-functional silicone oils and emulsions serving China’s electronics and automotive markets. These strategic expansions, regulatory adaptations, and pricing recalibrations underscore how high-purity electronics demand, EV battery materials, and sustainable silicone chemistry are shaping the silicone oil market trajectory through 2034.

Key Trends and High-Value Opportunities Shaping the Global Silicone Oil Market

Brand-Led Sustainability Mandates Reshaping Textile Silicone Oil Consumption

The silicone oil market is experiencing a material shift in textile applications as global apparel brands impose aggressive sustainability and water-reduction mandates across their supplier networks. Traditional paraffin waxes and fatty softeners are being systematically replaced by amino-functional and polyether-modified silicone oils that deliver superior softness, elasticity, and wrinkle recovery at significantly lower add-on levels. These next-generation silicone emulsions achieve comparable or better hand-feel performance at nearly 30% lower application rates, directly reducing biochemical and chemical oxygen demand loads in textile effluent streams. This transition is no longer discretionary. It is increasingly embedded in brand audit protocols linked to wastewater discharge compliance and supplier scorecards.

Capacity expansion decisions reflect this structural demand shift. In May 2024, Shin-Etsu Chemical announced an $85 million investment in a new silicone production facility in Zhejiang, China, scheduled for completion in early 2026. The site is strategically located to serve the world’s largest garment manufacturing ecosystem, where demand for modified silicone textile finishing agents continues to accelerate. By late 2025, polyether- and amino-functional silicone oils accounted for nearly 49% of the silicone textile chemical segment, driven by performance apparel requirements for moisture management, fabric breathability, and elastic recovery. This marks a decisive shift away from commodity softeners toward engineered silicone oils with sustainability-linked performance advantages.

High-Voltage Grid Modernization Accelerating Adoption of Silicone Dielectric Oils

Beyond textiles, power infrastructure modernization is emerging as a second major growth driver for the silicone oil market. National smart grid programs are accelerating the replacement of mineral oil-filled transformers with silicone-based dielectric fluids, particularly in urban and high-risk environments. Silicone oils are increasingly specified due to their Class K3 less-flammable rating, with fire points exceeding 370 degrees Celsius, a critical safety parameter for substations located in densely populated areas.

In the United States, grid expansion initiatives supported by the U.S. Department of Energy, including the $10.5 billion Grid Resilience and Innovation Partnerships program, are catalyzing deployment of high-capacity transformers capable of managing variable renewable energy loads. Silicone dielectric oils are preferred in these systems because they maintain dielectric breakdown voltages above 50 kilovolts while exhibiting stable viscosity from minus 60 to plus 250 degrees Celsius. Environmental compliance further reinforces adoption. In mid-2023, distributors such as Antala expanded advanced silicone transformer oil portfolios to meet increasingly stringent fire safety and environmental regulations across Europe and North America. Non-toxic and non-corrosive profiles reduce the long-term environmental liability associated with transformer leaks, aligning silicone oils with utility ESG frameworks.

Ultra-Pure Silicone Lubricants for Next-Generation Biologic Drug Delivery

Regulatory evolution in pharmaceutical packaging is opening a high-margin opportunity for medical-grade silicone oils. The enforcement of USP <382> from December 2025 has fundamentally raised qualification thresholds for elastomeric components used in drug delivery systems. Device manufacturers are now required to demonstrate functional suitability and biocompatibility, driving demand for USP Class VI silicone oils that ensure consistent plunger motion in pre-filled syringes and auto-injectors.

This regulatory upgrade is particularly impactful for high-viscosity biologics, including GLP-1 therapies and biosimilars, where precise break-loose and glide force control is essential for accurate dosing. Leading suppliers such as Dow and Wacker are commanding premium pricing for ultra-pure silicone oils, typically ranging between $5,000 and $8,000 per ton in mid-2025. Beyond injectables, these oils are critical for diaphragms, seals, and moving components in artificial heart pumps and dialysis systems, where the absence of extractables and leachables is a non-negotiable safety requirement.

Functionalized Silicone Oils Enabling Advanced CMP Slurry Formulations

The transition toward wide-bandgap semiconductors such as silicon carbide and gallium nitride is creating a specialized opportunity for silicone oils in chemical mechanical planarization processes. These materials are significantly harder than traditional silicon, exposing the limitations of conventional slurry chemistries. Silicone oils are increasingly deployed as rheology modifiers and dispersants to stabilize abrasive nanoparticles, including ceria and alumina, within CMP slurries used on 300 millimeter wafers for EV power electronics and AI data center components.

In 2024, the global CMP slurry market expanded by more than 10%, supported by advanced node and power device fabrication. By late 2025, over 70% of global fabs had transitioned to advanced CMP processes, with silicone-enhanced formulations gaining traction due to measurable performance benefits. Industry evaluations indicate that silicone-modified slurries can reduce surface roughness by up to 35% on ultra-hard substrates while contributing to a 15% reduction in defectivity rates. For leading foundries in Taiwan and South Korea, these improvements directly translate into higher yield stability and lower rework costs, positioning functionalized silicone oils as yield-critical process enablers rather than auxiliary additives.

Silicone Oil Market Share and Segmentation Insights

Dimethyl Silicone Oils Dominate the Silicone Oil Market Due to Versatility Across Industrial and Consumer Applications

Dimethyl silicone oils accounted for 58.60% of the silicone oil market in 2025, making them the most widely used silicone oil category across industrial and consumer applications. Based on polydimethylsiloxane (PDMS) chemistry, these oils provide exceptional thermal stability, low surface tension, chemical inertness, and oxidation resistance, enabling use in applications such as release agents, lubricants, defoamers, hydraulic fluids, and personal care formulations. Their availability across a broad viscosity spectrum allows manufacturers to tailor formulations for different functional requirements. A key 2025 development is the increasing adoption of viscosity grade optimization, where dimethyl silicone oils are supplied in narrow, application-specific viscosity ranges to enhance performance in foam control, mold release, and damping systems.

Industrial & Textiles Sector Drives Silicone Oil Consumption Across Manufacturing Processes

Industrial and textiles represent the largest end-use segment in the silicone oil market, accounting for 28.40% of total consumption in 2025 due to the widespread use of silicone oils across manufacturing operations. These oils function as mold release agents for plastics and rubber processing, specialty lubricants for high-temperature equipment, defoamers in chemical processing, and textile finishing agents for softness and water repellency. The scale of global industrial production continues to drive consistent silicone oil demand. A major 2025 industry trend is the rising demand for high-performance specialty lubricants, where silicone oils provide superior thermal stability, oxidation resistance, and wide operating temperature ranges, making them suitable for extreme environments where conventional petroleum-based lubricants are less effective.

Silicone Oil Market Competitive Landscape

The 2026 silicone oil market is driven by EV thermal management, semiconductor-grade purity, and regulatory-driven shifts toward low-cyclic, VOC-compliant siloxanes. Leading players are investing in localized production, circular silicone oils, and dielectric immersion cooling fluids to capture high-growth opportunities in AI data centers and sustainable personal care.

Wacker drives low-cyclic PDMS innovation and cost efficiency through Project PACE restructuring

Wacker Chemie AG is reinforcing its leadership in specialty silicone oils through Project PACE, targeting €200 million savings in 2026 and €300 million annually by 2027. Its €2.73 billion Silicones division is pivoting toward high-margin functional silicone oils for cosmetics and textiles. The company is expanding linear PDMS oils with ultra-low cyclic content below 0.1%, aligning with ECHA regulations and clean beauty demand. Forecasted EBITDA of €550 million to €700 million reflects recovery driven by specialty fluids. Workforce realignment of 1,500 roles supports capital reallocation toward semiconductor-grade silanes and Asian production hubs. This strategy positions Wacker as a leader in compliant, high-purity silicone oil solutions.

Shin-Etsu scales ultra-high-purity silicone oils with $1.2 billion global expansion strategy

Shin-Etsu Chemical is executing a large-scale capacity expansion exceeding $1.2 billion to dominate high-purity silicone oil markets. Investments across Japan, Thailand, Hungary, and the U.S. strengthen its "local-for-local" manufacturing footprint. The company introduced advanced silicone oil dispersants that eliminate instability and color streaking in anhydrous cosmetic formulations, addressing premium beauty trends. Its vertically integrated silicone-to-wafer ecosystem ensures consistent quality for semiconductor and dielectric fluid applications. With projected revenue of ¥2.4 trillion and strong dividend payouts, Shin-Etsu maintains robust financial backing. This positions it as a critical supplier of eco-friendly and electronics-grade silicone oils.

Dow accelerates electronics-grade silicone oil capacity with AI cooling and high-margin medical fluids

Dow Inc. is repositioning toward high-performance silicone oils through its Transform to Outperform initiative, targeting $2 billion EBITDA growth. A $500 million expansion at its Zhangjiagang facility will increase electronics-grade silicone oil capacity by 40%, supporting semiconductor and EV demand. Dow maintains a 45% gross margin in medical and electronics-grade silicones, significantly above the industry average, driven by FDA-approved formulations. Pricing increases of 5% to 10% offset rising silicon metal costs and decarbonization investments. Its Cooling Science Studio in Shanghai advances immersion cooling fluids for AI-driven data centers. This integrated strategy secures Dow’s leadership in high-margin, next-generation silicone oil applications.

Elkem advances bio-based silicone oils and low-cyclic formulations amid strategic silicones divestment

Elkem Silicones is undergoing a strategic transformation in 2026, divesting its silicones division to Bluestar while strengthening its upstream silicon materials focus. The company introduced PURESIL™ ORG bio-based silicone oils derived from sunflower carriers, aligning with sustainability mandates in personal care. It also launched low-cyclic silicone formulations with less than 0.1% D4, D5, and D6 content to meet REACH compliance requirements. Despite market softness, Elkem reported NOK 31 billion operating income and achieved 23% EBITDA growth in its silicones segment. Its innovations support circular silicone chemistry and regulatory readiness. This positions Elkem as a key innovator in sustainable silicone oil solutions.

Momentive targets EV and SiC semiconductor growth with thermally conductive silicone oil systems

Momentive Performance Materials is focusing on high-reliability silicone oil technologies for EV power electronics and semiconductor applications. The integration of Sibelco’s spherical alumina and silica business enhances its capability to develop highly filled, thermally conductive silicone oils. Its R&D efforts in Silicon Carbide processing support the expansion of high-efficiency power modules in EVs. Momentive’s thermal interface materials enable up to 15% weight reduction in battery systems compared to traditional mechanical solutions. The company is also advancing ultra-low-volatility silicone oils for ADAS sensors, preventing fogging and ensuring reliability in autonomous vehicles. This positions Momentive as a specialist in advanced thermal and electronic silicone fluid systems.

Japan: Precision Thermal Management and Sustainable Reformulation

Japan continues to anchor the global silicone oil industry through precision engineering, electronics-grade purity, and early adoption of sustainability-led manufacturing. In January 2025, Wacker Chemie AG inaugurated a new Tsukuba facility dedicated to silicone-based Thermal Interface Materials, where advanced silicone oils function as heat-dissipating gap fillers for power electronics and traction batteries. This investment aligns directly with Japan’s leadership in EV power modules and high-density electronics. On the pricing front, Shin-Etsu Chemical implemented a global price revision exceeding 10% from July 2024, reflecting structural increases in raw material, logistics, and energy costs. Rather than dampening demand, this move has reinforced the market’s shift toward high-value, application-specific silicone oils with defensible margins.

Sustainability and functional differentiation are increasingly intertwined. In March 2025, Shin-Etsu transitioned part of its Rayong operations to biomass-based cogeneration, reducing the carbon intensity of regional silicone oil output and setting a precedent for low-emission Asian supply chains. Product development remains highly specialized, including ultra-low volatility phenyl-silicone oils for extreme ultraviolet lithography, where even trace outgassing can compromise semiconductor yields. In parallel, Japanese formulators debuted biodegradable soft-focus silicone oils as microplastic alternatives in premium cosmetics, while scaling dielectric silicone fluids for immersion cooling in 800V EV architectures. These developments position Japan as a global reference point for high-purity, low-volatility, and sustainability-aligned silicone oil systems.

South Korea: Semiconductor-Driven Purity and EV Thermal Demand

South Korea’s silicone oil market is expanding rapidly on the back of semiconductor and battery dominance. With semiconductor exports reaching USD 173.4 billion in 2025, demand for 7N and 8N-purity silicone oils used in chip fabrication and High Bandwidth Memory packaging has intensified. Early 2025 saw Wacker Chemie AG expand its Jincheon site, adding capacity tailored to high-performance silicone oils and sealants for domestic electronics and automotive customers. The shift toward advanced memory architectures has further accelerated uptake of ultra-low metal silicone oils, essential for preventing ionic contamination in dense electronic encapsulation environments.

Corporate consolidation has strengthened regional supply depth. KCC Corporation completed the full integration of Momentive Performance Materials in late 2024, creating one of the most comprehensive functional silicone oil portfolios in Asia-Pacific. Investment momentum is now concentrated on dielectric silicone fluids for EV battery leaders such as LG Energy Solution and SK On, where immersion cooling and thermal stability are mission-critical. South Korea’s market is therefore characterized by purity-driven specifications, electronics-led scale, and vertically integrated chemical platforms.

China: Regulation-Led Reformulation and Infrastructure-Led Volume

China remains the largest volume market for silicone oils, but regulatory tightening is reshaping product mix and supplier behavior. The issuance of GB 4806.16-2025 by the National Health Commission introduced stringent limits on volatile substances in food-contact silicone materials, with enforcement beginning in September 2026. This has compelled silicone oil producers to upgrade analytical capabilities and reformulate products to comply with stricter migration thresholds. Parallel implementation of GB 4806.15-2024 for food-contact adhesives in early 2025 further increased compliance complexity, requiring detailed Specific Migration Limit disclosures for aromatic amines.

Infrastructure and environmental policy continue to underpin demand. As part of a USD 142 billion infrastructure initiative, China is expanding the use of silicone oil-based water repellents and anti-corrosive coatings across major rail and airport projects in cities such as Chengdu and Xi’an. Capacity additions also remain significant. In March 2025, Wacker Chemie AG completed a downstream expansion at Zhangjiagang focused on specialty silicone oil emulsions for personal care and textiles. Meanwhile, revisions to the Environmental Protection Tax Law introduced pilot VOC taxes, accelerating the transition toward water-borne silicone oil systems. The 14th Five-Year Plan has additionally driven large-scale adoption of silicone defoamers in municipal wastewater treatment, reinforcing China’s role as both a regulatory bellwether and a volume engine.

United States: Decarbonization, Transparency, and High-End Applications

The United States silicone oil market is increasingly defined by decarbonization strategies, ESG transparency, and advanced electronics. In May 2025, Dow introduced its Decarbia™ portfolio, positioning low-carbon silicone oils and elastomer blends produced through decarbonized silicon metal feedstocks. These products are supported by third-party Environmental Product Declarations and verified carbon compensation, aligning with procurement requirements of large industrial and consumer brands. Investment momentum remains strong, highlighted by Shin-Etsu Silicones of America surpassing USD 577 million in cumulative investment at its Akron facility over a four-year cycle.

Product innovation is extending into bio-based personal care and semiconductor infrastructure. The launch of DEXCARE™ CD-2 Polymer, a bio-fermented polymer designed to enhance silicone oil deposition in biodegradable formulations, reflects growing regulatory and consumer pressure to reduce petrochemical content. At the industrial level, CHIPS Act funding has accelerated deployment of on-site ultra-high purity silicone oil delivery systems for new domestic logic-node fabs, embedding silicone oils deeper into the U.S. semiconductor value chain. The U.S. market is thus transitioning from commodity volumes toward premium, documented, and sustainability-aligned silicone oil solutions.

Germany and the European Union: Compliance-Led Innovation and Circularity

Germany anchors the European silicone oil landscape through regulatory leadership and system-level innovation. The launch of Smart Effects by Evonik Industries in January 2025 merged silica and silanes capabilities to develop integrated silica-silane-oil systems for green tires and electronics. Regulatory pressure is intensifying, with EU REACH updates effective June 2026 prohibiting silicone products containing more than 0.1% of D4, D5, or D6 siloxanes in several cosmetic and industrial uses. This has accelerated reformulation and driven demand for compliant, low-cyclic silicone oils.

Circular economy initiatives are becoming commercially relevant. At K-Fair 2025, German producers showcased TEGO® Antifoam KS 53, a food-contact-compliant silicone oil defoamer that improves the stability of mechanical plastics recycling. Beyond traditional markets, Evonik is pioneering Direct Air Capture technologies using amino-silicone-oil-treated silica carriers, extending silicone oil applications into carbon management. Germany’s market is therefore shaped by regulatory foresight, circular material flows, and cross-sector innovation.

Comparative Snapshot: Silicone Oil Industry by Country

Silicone Oil Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Differentiation

|

|

Japan

|

EV power electronics, semiconductors

|

Ultra-low volatility oils, biomass-powered production

|

|

South Korea

|

Memory semiconductors, EV batteries

|

7N–8N purity oils, integrated silicone portfolios

|

|

China

|

Infrastructure, personal care, wastewater

|

Regulatory-driven reformulation, large-scale emulsions

|

|

United States

|

Semiconductors, personal care, ESG

|

Low-carbon oils, EPD-backed transparency

|

|

Germany / EU

|

Green tires, recycling, compliance

|

REACH-aligned oils, circular and DAC applications

|

Silicone Oil Market Report Scope

Silicone Oil Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.7 Billion

|

|

Market Size (2034)

|

$7.2 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Product Type (Dimethyl Silicone Oils, Phenyl Methyl Silicone Oils, Methyl Hydrogen Silicone Oils, Functional Silicone Oils, Silicone Oil Emulsions), By Viscosity Range (Low Viscosity, Medium Viscosity, High Viscosity, Ultra-High Viscosity), By End-Use Industry (Automotive, Electronics, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Industrial & Textiles, Construction, Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co. Ltd., Momentive Performance Materials Inc., Evonik Industries AG, Elkem ASA, Hoshine Silicon Industry Co. Ltd., Zhejiang Xanan Chemical Industrial Group, KCC Corporation, Siltech Corporation, Gelest Inc., Innospec Inc., CHT Group, Elkay Chemicals Pvt. Ltd., Hubei BlueSky New Material Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicone Oil Market Segmentation

By Product Type

- Dimethyl Silicone Oils

- Phenyl Methyl Silicone Oils

- Methyl Hydrogen Silicone Oils

- Functional Silicone Oils

- Silicone Oil Emulsions

By Viscosity Range

- Low Viscosity

- Medium Viscosity

- High Viscosity

- Ultra-High Viscosity

By End-Use Industry

- Automotive

- Electronics

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Industrial & Textiles

- Construction

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicone Oil Industry

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co. Ltd.

- Momentive Performance Materials Inc.

- Evonik Industries AG

- Elkem ASA

- Hoshine Silicon Industry Co. Ltd.

- Zhejiang Xinan Chemical Industrial Group

- KCC Corporation

- Siltech Corporation

- Gelest Inc.

- Innospec Inc.

- CHT Group

- Elkay Chemicals Pvt. Ltd.

- Hubei BlueSky New Material Inc.

*- List not Exhaustive