Decarbonized Silicone Chemistry and High-Performance Applications Driving Mid-Range Growth

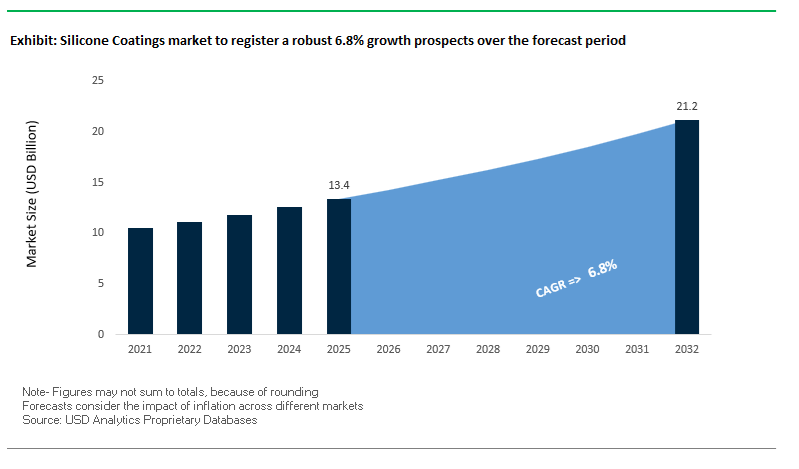

The global Silicone Coatings Market is advancing steadily, supported by rising demand for high-temperature resistance, weatherproofing, and long-term durability across construction, automotive, electronics, and industrial sectors. The market was valued at $13.4 billion in 2025 and is projected to reach $21.2 billion by 2032, expanding at a CAGR of 6.8% during 2025–2032. This growth reflects the increasing reliance on silicone-based technologies for applications requiring extreme environmental stability, UV resistance, and moisture protection, particularly in infrastructure and advanced manufacturing environments.

A primary structural driver is the shift toward low-carbon and sustainable silicone production, aligning with global decarbonization targets. Silicone coatings, traditionally energy-intensive to produce, are now being re-engineered using reduced-carbon feedstocks and circular material systems, significantly lowering lifecycle emissions. This transition is particularly relevant in construction and automotive sectors, where ESG compliance and carbon reporting are becoming mandatory procurement criteria.

Another key growth catalyst is the increasing integration of silicone coatings in next-generation applications, including EV batteries, electronics, and renewable energy systems. Silicone materials provide thermal insulation, electrical resistance, and chemical stability, making them essential for protecting sensitive components in high-performance environments. Additionally, the construction sector continues to drive demand for silicone-based façade coatings and sealants, particularly in regions exposed to extreme weather conditions.

The market is also witnessing a shift toward hybrid coating systems, where silicone is combined with silicate or polymer chemistries to enhance performance characteristics such as breathability, adhesion, and durability. These hybrid systems are expanding the application scope of silicone coatings, particularly in architectural and infrastructure projects requiring both aesthetic performance and long-term protection.

Market Analysis: Portfolio Restructuring, Circular Silicone Innovation, and EV Battery Applications Reshaping Competitive Landscape

The silicone coatings market is undergoing significant transformation driven by portfolio restructuring, supply chain optimization, and innovation in sustainable and high-performance materials. In March 2026, Elkem announced the divestment of the majority of its silicone division to Bluestar, marking a strategic shift toward becoming a focused metals and materials company. This transaction transfers global silicone assets while retaining select strategic operations, signaling consolidation and realignment within the silicone value chain.

Sustainability-led innovation is emerging as a key competitive differentiator. Dow’s May 2025 launch of Decarbia™ low-carbon silicones represents a major step toward carbon-neutral silicone coatings, utilizing decarbonized silicon metal feedstocks and verified carbon compensation. Similarly, Elkem’s September 2025 breakthrough in silicone circularity enables the recycling of high-consistency rubber into high-quality raw materials, supporting the development of circular silicone coatings with reduced environmental impact.

Product innovation is increasingly focused on advanced functional performance and hybrid systems. Wacker Chemie’s March 2026 introduction of SILRES® BS 6922 enhances water repellency and durability in silicate-silicone hybrid coatings, addressing the need for weather-resistant and breathable construction materials. Meanwhile, Jotun’s June 2025 launch of silicone-hybrid coatings for EV batteries highlights the critical role of silicone in providing thermal insulation and electrical protection, reducing risks such as thermal runaway in electric vehicles.

Supply chain and distribution optimization are also shaping market dynamics. Evonik’s February 2026 restructuring of its North American distribution network consolidates silicone additive supply through specialized partners, improving technical support and customer responsiveness in coatings and inks applications. Additionally, Momentive’s March 2025 joint venture with Hungpai strengthens silane production capacity in Asia, ensuring a stable supply of critical precursors for high-performance silicone coatings.

In the personal care and specialty coatings segment, Momentive’s January 2026 launch of Harmonie NatuDerma, a fully bio-based emollient, reflects the growing demand for bio-derived and biodegradable silicone alternatives, particularly in regulated consumer applications.

Strategic integration and consolidation are further influencing innovation pipelines. KCC Corporation’s ongoing integration of Momentive’s silicone business is driving new R&D initiatives in architectural coatings, particularly targeting high-growth markets in Asia and the Middle East. At the same time, hybrid repair technologies such as Dalton Enterprises’ QuickPatch H2O (November 2024) demonstrate the increasing convergence of silicone and silicate chemistries to enable rapid, durable repair solutions compatible with advanced coating systems.

Market Trend: EU REACH 2026 Restrictions on Cyclic Siloxanes Forcing Structural Reformulation of Silicone Coatings

The European Union’s amendment to Annex XVII under REACH, effective June 6, 2026, is introducing a fundamental shift in silicone chemistry by restricting cyclic siloxanes D4, D5, and D6 to concentrations below 0.1% by weight in industrial and consumer formulations. These cyclic compounds, widely used as intermediates and carriers in silicone coatings, are classified as persistent, bioaccumulative, and toxic, prompting regulatory intervention aimed at achieving a 90% reduction in environmental emissions by the 2026–2027 period. This regulatory tightening is creating a pronounced reformulation challenge for manufacturers, as legacy silicone systems often rely on these low-molecular-weight species for processability and performance tuning. The transition toward “linear-only” silicone polymer architectures is accelerating, requiring significant investment in R&D to maintain coating properties such as flow, leveling, and adhesion without the volatility benefits of cyclic siloxanes. In parallel, supply chain disruptions are emerging as non-compliant inventory must be phased out of the EU market within strict deadlines, increasing raw material costs and elongating product qualification cycles. This shift is also catalyzing innovation in low-volatile and solvent-free silicone coatings, positioning compliance-driven product development as a central competitive differentiator in the global silicone coatings market.

Market Trend: Global Food Contact Regulations Elevate Migration Standards and Drive Adoption of Platinum-Cured Silicone Systems

The regulatory landscape for silicone coatings in food-contact applications has tightened significantly across 2025 and 2026, driven by heightened scrutiny of chemical migration and consumer safety. Following the U.S. FDA’s removal of PFAS-based grease-proofing agents, silicone coatings have emerged as a key alternative but are now subject to stricter evaluation of extractable and migratable substances. The implementation of Mercosur Resolution No. 34/2025, effective January 2026, has harmonized food-contact material standards across South America, aligning closely with the European Union’s stringent specific migration limits. Under current compliance frameworks, silicone coatings used in cookware, baking molds, and food packaging must demonstrate that total volatile organic matter migration does not exceed 0.5% by weight. This requirement is accelerating the transition from peroxide-cured silicone systems, which can leave residual byproducts, to platinum-cured systems that offer higher purity and reduced extractables. Manufacturers are increasingly optimizing crosslink density and curing kinetics to meet these migration thresholds without compromising mechanical flexibility or thermal resistance. As global regulatory convergence intensifies, silicone coatings designed for food-contact applications are evolving toward ultra-clean, low-migration chemistries, reinforcing safety as a primary innovation axis.

Market Opportunity: Fouling-Release Silicone Coatings Enabling Biocide-Free Marine Efficiency and IMO Compliance

The maritime coatings segment is witnessing a strategic pivot toward silicone-based fouling-release coatings as the International Maritime Organization advances its 2025/2026 biofouling management guidelines toward enforceable standards. Traditional copper-based antifouling systems are facing increasing regulatory and environmental pressure due to their biocidal impact on marine ecosystems. In response, silicone fouling-release coatings, which operate through ultra-smooth, low-surface-energy interfaces rather than toxic leaching, are gaining rapid adoption. Advanced hydrogel-based silicone systems now deliver measurable operational benefits, including up to 20% improvement in fuel efficiency due to reduced hydrodynamic drag associated with surface roughness levels near 1 micrometer. These coatings also maintain vessel performance over extended service intervals, demonstrating speed loss below 1% across a 60-month dry-docking cycle. This is a critical parameter for ship operators targeting compliance with the IMO’s Carbon Intensity Indicator requirements. Additionally, the friction-reduction properties of silicone coatings can lower total vessel emissions by as much as 35%, offering a capital-efficient decarbonization pathway without requiring hardware retrofits. As regulatory and economic pressures converge, fouling-release silicone coatings are emerging as a high-value solution in sustainable marine coatings.

Market Opportunity: High-Temperature Silicone Coatings Expanding in Automotive Exhaust and Industrial Stack Applications

The intrinsic thermal stability of silicone coatings, driven by the high bond energy of the Si-O-Si backbone, is creating strong growth opportunities in high-temperature industrial and automotive environments. Advanced silicone-ceramic hybrid coatings developed for 2026 applications are capable of withstanding continuous operating temperatures up to 650°C and intermittent exposure up to 800°C without degradation phenomena such as chalking, cracking, or delamination that are common in conventional organic coatings. This performance is particularly critical in modern internal combustion engines operating at higher thermal efficiencies and in industrial exhaust systems where extreme heat and corrosive conditions coexist. Beyond thermal resistance, these coatings maintain protective barrier properties even after repeated thermal cycling, with validated performance exceeding 1,000 hours in salt spray testing following pre-exposure to elevated temperatures. This ensures long-term corrosion protection for components such as exhaust manifolds and chimneys exposed to moisture, salts, and chemical pollutants. In industrial stack applications, the adoption of high-solids silicone coatings has been shown to extend maintenance intervals from approximately three years to more than seven years, significantly reducing lifecycle costs and operational downtime. As industries prioritize durability and cost efficiency under increasingly harsh operating conditions, high-temperature silicone coatings are becoming a critical material solution across multiple sectors.

Silicone Coatings Market Share and Segmentation Insights: 100% Silicone Dominance and Waterproofing Applications Driving Demand

By Composition Type: 100% Silicone Coatings Lead with Superior Weatherability and Long-Term Performance

The 100% silicone coatings segment dominated the silicone coatings market with a 42.8% share in 2025, driven by its unmatched weather resistance, flexibility, and long-term durability in harsh environments. Based on polydimethylsiloxane (PDMS) chemistry, these coatings offer exceptional UV stability, elasticity, and moisture vapor permeability, making them the preferred solution for roof coatings, building facades, bridge expansion joints, and infrastructure protection. A key advantage is their ability to maintain gloss, color stability, and mechanical integrity for over 15–20 years, significantly outperforming conventional acrylic and polyurethane coatings, especially in extreme climates such as deserts, tropical regions, and high-altitude zones. Additionally, their resistance to cracking, chalking, and environmental degradation reduces maintenance costs and extends asset lifespan. This combination of high-performance protective coatings, durability, and environmental resilience solidifies the leadership of 100% silicone coatings in the global market.

By Functionality: Waterproofing and Moisture Protection Segment Leads with Building Envelope Applications

The waterproofing and moisture protection segment accounted for the largest 37.4% share of the silicone coatings market in 2025, reflecting strong demand across roofing systems and building envelope applications. Silicone coatings are widely used as fluid-applied waterproof membranes for low-slope roof restoration, balconies, podium decks, and below-grade foundation protection, where preventing water ingress is critical. A major differentiator is their breathable barrier capability, allowing trapped moisture within substrates to escape while blocking liquid water penetration, which helps prevent blistering, cracking, and delamination—common issues with epoxy and polyurethane systems. This makes silicone coatings particularly effective in humid environments and aging structures. With increasing focus on energy-efficient buildings, leak prevention, and long-lasting waterproof coatings, silicone-based solutions continue to gain traction, reinforcing their dominance in the waterproofing segment of the global silicone coatings market.

Competitive Landscape of the Silicone Coatings Market

Wacker Leads Market with Operational Efficiency and Specialty Silicone Focus

Wacker Chemie AG is a key leader in the silicone coatings market, leveraging its PACE cost-efficiency program to maintain profitability amid volatile market conditions. In Q1 2026, the company reported sales of €1.41 billion with a 12.3% EBITDA margin. Wacker is focusing heavily on specialty silicone products, particularly for construction and semiconductor applications, with 82% of its revenue generated outside Germany. Its global footprint and cost optimization strategies position it strongly in high-growth regions such as the Americas and Asia-Pacific.

Dow Drives Sustainability Leadership with Carbon-Neutral Silicone Technologies

Dow Inc. is the sustainability frontrunner in the silicone coatings market, pioneering carbon-neutral silicone production. Its DOWSIL™ 213S and 214S dispersions enhance slip and mar resistance in waterborne coatings, while maintaining low usage levels. Dow’s innovations include thermal management gels for EV battery packs, supporting next-generation electric vehicle manufacturing. Its commitment to reducing carbon emissions by up to 85% in silicon production reinforces its leadership in sustainable silicone solutions.

Shin-Etsu Leads High-Performance Segment with Advanced Automotive and Semiconductor Silicones

Shin-Etsu Chemical Co., Ltd. is a dominant player in the silicone coatings market, particularly in high-performance applications. The company has expanded production capacity for automotive-grade silicones, targeting EV thermal interface and insulation systems. Its innovations include advanced adhesives and sealants for autonomous vehicle sensors, offering superior vibration damping and moisture protection. Shin-Etsu also maintains a leading position in semiconductor-related silicones, supporting the rapid growth of AI and electronics industries.

Elkem Restructures Portfolio to Focus on High-Value Silicone Coating Applications

Elkem Silicones (Elkem ASA) is undergoing strategic restructuring to strengthen its position in specialized silicone markets. Its BLUESIL™ TCS 7544 textile coating achieves Euroclass A1/A2 fire safety compliance, targeting architectural and fire protection applications. The company’s divestment strategy aims to streamline operations and focus on high-margin segments. Its sustainability credentials, including strong environmental ratings, further enhance its competitive position.

Momentive Expands Specialty Silicone Coatings with High-Temperature and Electronics Applications

Momentive Performance Materials is a key innovator in the silicone coatings market, focusing on high-temperature and high-performance applications. The company is investing in silicone elastomers for EV drivetrains and aerospace systems, offering durability under extreme conditions. Its leadership in electronics conformal coatings, particularly solvent-free and UV-cured systems, positions it strongly in the rapidly growing electronics segment. Momentive’s focus on circular economy solutions further strengthens its market position.

Evonik Strengthens Market Position with Additives and Radiation-Curing Silicone Technologies

Evonik Industries AG plays a critical enabling role in the silicone coatings market, supplying advanced additives and specialty chemicals. Its TEGO® Rad silicone acrylates enhance wetting, slip, and surface performance in radiation-cured coatings. The company’s expansion in Nanjing, powered by green electricity, supports growing demand in Asia-Pacific markets. Evonik’s focus on sustainability and advanced materials reinforces its role as a key supplier in next-generation silicone coating technologies.

Germany Leading Sustainable Silicone Coatings Innovation with Green Chemistry and Energy-Efficient Construction

Germany continues to dominate the silicone coatings market, driven by its leadership in low-VOC, solvent-free silicone technologies and strong emphasis on sustainable construction. The commercialization of bio-based silicone resins derived from plant-based methanol marks a significant breakthrough in reducing dependence on fossil fuel feedstocks, aligning with global decarbonization goals.

Regulatory frameworks such as the updated AgBB evaluation scheme (2025) are enforcing stricter emission limits, accelerating the transition toward eco-friendly silicone coatings in architectural applications. Government-backed infrastructure investments under energy-efficient refurbishment programs are driving demand for silicone liquid-applied membranes to mitigate thermal bridging in building envelopes. Product innovations such as self-cooling silicone roof coatings with infrared-reflective pigments are addressing urban heat island challenges, while R&D expansion in high-performance textile coatings and dielectric conformal coatings is strengthening Germany’s position as a global innovation hub.

China Scaling High-Purity Silicone Coatings for EV Batteries and Infrastructure Protection

China is rapidly advancing in the global silicone coatings market, transitioning toward high-value, specialty applications in e-mobility and infrastructure. Government initiatives such as the New Material Industry Standard Strengthening Plan (2025–2026) are boosting domestic production of high-purity silicone polymers, reducing reliance on imports and strengthening supply chain resilience.

Technological innovation is evident in the development of thermally conductive silicone coatings for EV battery systems, enhancing safety and performance in cell-to-pack architectures. Regulatory updates, including new standards for food-contact silicone coatings, are further driving product quality improvements. Infrastructure projects such as the Hong Kong-Zhuhai-Macao Bridge are utilizing silicone-based anti-corrosion coatings for durability in marine environments. Expansion of manufacturing capacity, including advanced clean-room facilities for electronic-grade coatings, and the widespread use of silicone release coatings in packaging and logistics, highlight China’s growing dominance in both industrial and consumer applications.

United States Driving Aerospace and Renewable Energy Applications in Silicone Coatings

The United States is a key innovation hub in the silicone coatings industry, with strong growth in aerospace, infrastructure, and renewable energy sectors. Technological advancements such as UV-curable silicone coatings are significantly reducing processing times while maintaining high thermal stability, making them ideal for aerospace components.

Infrastructure investments are driving the adoption of silicone-alkyd hybrid coatings for bridges and steel structures, offering superior durability and UV resistance. In the renewable energy sector, anti-icing silicone coatings for wind turbine blades are improving operational efficiency in cold climates. Regulatory policies, including updates to emission standards, are accelerating the transition toward water-based silicone formulations. Additionally, the growing demand for 100% silicone roof coating systems in commercial retrofits and investments in high-purity silicone production for semiconductors are reinforcing the United States’ leadership in high-performance coating technologies.

Japan Advancing Nano-Silica Reinforced Silicone Coatings for Electronics and Automotive Innovation

Japan is a global leader in advanced silicone coatings, particularly through the integration of nanotechnology in high-precision applications. Innovations such as nano-silica reinforced silicone coatings are delivering exceptional scratch resistance, making them ideal for foldable displays and automotive touch interfaces.

The automotive sector is adopting lightweight silicone-based coatings for airbags, improving performance and efficiency. Government initiatives under the Green Growth Strategy are supporting the development of silicone-based hydrogen barrier coatings for fuel-cell vehicles. Infrastructure applications include silicone water-repellent coatings for seismic retrofitting, enhancing structural durability. Expansion in production capacity for medical-grade silicones and the increasing use of dielectric conformal coatings for 5G and 6G technologies further highlight Japan’s role as a leader in high-tech silicone coating applications.

India Emerging as a High-Growth Market for Silicone Coatings in Infrastructure and Smart Cities

India is witnessing a significant rise in the silicone coatings market, driven by urbanization and infrastructure development initiatives. Government programs such as the Smart Cities Mission are promoting the adoption of silicone-based architectural coatings for heritage conservation and modern construction, ensuring durability and breathability.

Infrastructure expansion is driving demand for silicone-modified coatings in highways and metro projects, particularly in regions with heavy rainfall and humidity. Investments in domestic production, including new manufacturing facilities and siloxane production initiatives, are strengthening supply chain capabilities. Product innovations such as cost-effective silicone waterproofing solutions for affordable housing are addressing key challenges such as wall seepage and mold growth. Additionally, the growing use of silicone structural glazing systems in commercial real estate is enhancing building performance and aesthetics across major urban centers.

Saudi Arabia Driving Extreme-Environment Silicone Coatings Demand Under Vision 2030

Saudi Arabia is emerging as a high-growth market in the silicone coatings sector, driven by large-scale infrastructure projects and extreme climatic conditions. Mega developments such as NEOM are utilizing heat-resistant silicone coatings capable of withstanding surface temperatures exceeding 70°C, ensuring durability in harsh desert environments.

The country is investing heavily in domestic silicone production capacity, including the development of large-scale siloxane manufacturing facilities. The energy sector remains a key application area, with widespread use of high-heat silicone coatings to prevent corrosion under insulation in pipelines and refineries. Product innovations such as sand-repellent silicone coatings for solar panels are improving energy efficiency in renewable projects. Regulatory frameworks promoting high-performance materials are further accelerating adoption, while applications in airport infrastructure and steel protection highlight the growing importance of silicone coatings in long-term asset preservation.

Silicone Coatings Market Report Scope

Silicone Coatings market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.4 Billion

|

|

Market Size (2032)

|

$21.2 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Composition Type (100% Silicone, Silicone Polymers, Silicone Water Repellents, Silicone Additives), By Technology (Solvent-less, Solvent-based, Water-borne, Radiation-Cured, Powder-based), By Substrate (Metal, Concrete and Masonry, Plastics and Composites, Glass and Ceramics, Paper and Film, Textiles and Fabric), By End-User Industry (Building and Construction, Automotive and Transportation, Electronics, Consumer Goods, Industrial, Marine, Paper and Packaging, Medical and Healthcare), By Functionality (Waterproofing and Moisture Protection, Thermal Insulation and Heat Resistance, UV and Weather Resistance, Anti-Corrosion, Release and Non-Stick Properties)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Wacker Chemie AG, Momentive Performance Materials Inc., Shin-Etsu Chemical Co., Ltd., Evonik Industries AG, Elkem ASA, Akzo Nobel N.V., PPG Industries, Inc., KCC Corporation, The Sherwin-Williams Company, Hempel A/S, Jotun Group, Sika AG, CHT Germany GmbH, Siltech Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicone Coatings Market Segmentation

By Composition Type

- 100% Silicone

- Silicone Polymers

- Silicone Water Repellents

- Silicone Additives

By Technology

- Solvent-less

- Solvent-based

- Water-borne

- Radiation-Cured

- Powder-based

By Substrate

- Metal

- Concrete and Masonry

- Plastics and Composites

- Glass and Ceramics

- Paper and Film

- Textiles and Fabric

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Electronics

- Consumer Goods

- Industrial

- Marine

- Paper and Packaging

- Medical and Healthcare

By Functionality

- Waterproofing and Moisture Protection

- Thermal Insulation and Heat Resistance

- UV and Weather Resistance

- Anti-Corrosion

- Release and Non-Stick Properties

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Silicone Coatings Industry

- Dow Inc.

- Wacker Chemie AG

- Momentive Performance Materials Inc.

- Shin-Etsu Chemical Co., Ltd.

- Evonik Industries AG

- Elkem ASA

- Akzo Nobel N.V.

- PPG Industries, Inc.

- KCC Corporation

- The Sherwin-Williams Company

- Hempel A/S

- Jotun Group

- Sika AG

- CHT Germany GmbH

- Siltech Corporation

*- List not Exhaustive