Low Temperature Powder Coatings Market Size, Energy-Efficient Powder Technologies, and Heat-Sensitive Substrate Applications Outlook

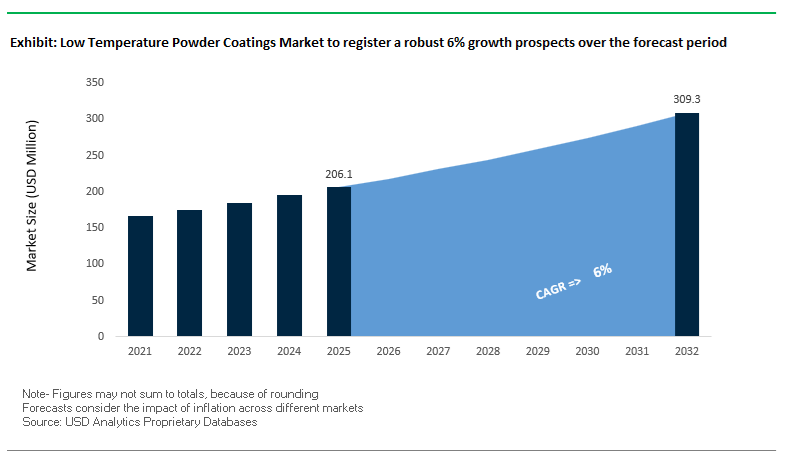

The global low temperature powder coatings market was valued at $206.1 million in 2025 and is projected to reach $309.9 million by 2032, growing at a CAGR of 6%. Market expansion is being driven by rising demand for low-cure powder coatings, energy-efficient powder coating systems, ultra-low bake coatings, and sustainable powder coatings across furniture, automotive, appliances, architecture, and industrial manufacturing sectors. These coatings are engineered to cure at significantly reduced temperatures, enabling manufacturers to lower energy consumption, carbon emissions, and operational costs while expanding compatibility with heat-sensitive substrates.

A key growth driver is the increasing adoption of medium-density fiberboard (MDF), natural wood, plastics, and lightweight composites in modern manufacturing. Traditional powder coatings require curing temperatures of 180°C–200°C, which can damage such substrates. In contrast, low temperature powder coatings can cure at 120°C–150°C, making them suitable for furniture, interior panels, electronics housings, and EV components. Additionally, growing regulatory pressure around decarbonization and green building standards is accelerating the shift toward low-energy coating solutions, particularly in Europe and North America.

The market is also benefiting from advancements in polymer chemistry, additive technologies, and hybrid resin systems, which are improving mechanical durability, weather resistance, and coating adhesion even at reduced curing temperatures. The integration of recycled materials, bio-based resins, and PFAS-free formulations is further strengthening the sustainability profile of these coatings. Regionally, Europe leads in green building adoption and low-energy coating technologies, while Asia-Pacific is witnessing strong growth due to expanding furniture manufacturing and industrial production capacity.

The low temperature powder coatings industry is undergoing rapid transformation driven by technological innovation, sustainability mandates, and strategic consolidation among leading players. A major development occurred in February 2026, when AkzoNobel and Axalta announced a merger of equals, combining their extensive powder coating portfolios. This consolidation is particularly significant for the low-temperature segment, as it integrates AkzoNobel’s Interpon Low-E technology with Axalta’s energy-efficient coating systems, accelerating R&D and global adoption of low-cure powder coatings.

Product innovation continues to push the boundaries of ultra-low curing performance. In January 2026, PPG Industries launched the next generation of ENVIROCRON® HeatSense coatings, capable of curing at temperatures as low as 120°C (250°F), making them highly suitable for high-volume automated coating lines for MDF and natural wood furniture. Similarly, AkzoNobel’s September 2025 launch of Interpon D2525 Low-E coatings offers super-durable architectural performance while curing at 150°C, delivering up to 20% energy savings compared to conventional systems.

Emerging applications in electric mobility and advanced manufacturing are further expanding the market. In November 2025, Jotun introduced a specialized low-cure powder coating for EV battery packs, providing electrical insulation and fire protection without exposing temperature-sensitive battery chemistries to high heat. Additionally, Tiger Drylac’s June 2024 innovation in low-cure powders for 3D-printed components highlights the growing role of these coatings in additive manufacturing, where traditional high-temperature curing would cause deformation.

Sustainability remains a central focus across the value chain. In June 2025, PPG introduced PFAS-free powder coatings containing up to 18% recycled PET, achieving a 30% lower carbon footprint compared to standard formulations. Axalta’s Alesta® BioCore family, launched in July 2024, further advances this trend with bio-based powder coatings that reduce lifecycle CO₂ emissions by up to 25%. Meanwhile, Sika AG’s July 2025 investment in low-bake powder production supports increasing demand for green-certified construction materials.

R&D investments and capacity expansions are also accelerating innovation cycles. Sherwin-Williams, in October 2025, increased R&D spending to reduce curing cycle times by 30%, targeting efficiency improvements in appliance and HVAC manufacturing. AkzoNobel’s €20 million expansion of its Como facility in September 2024 further strengthens production capacity for low-energy architectural powder coatings, supporting growing global demand.

Market Trend: MDF Furniture Manufacturing Transitioning to Low-Cure Powder Coating Systems for Efficiency and Surface Performance

The low temperature powder coatings market is experiencing accelerated adoption in the furniture manufacturing sector, particularly among office furniture and ready-to-assemble (RTA) product segments. Manufacturers are increasingly replacing multi-layer liquid solvent-based coating systems with single-coat low-cure powder coatings optimized for Medium Density Fiberboard (MDF). This transition is driven by the need to achieve high-quality finishes on heat-sensitive substrates without inducing outgassing defects or structural warping associated with traditional high-temperature curing processes above 180°C.

Low-cure powder formulations operating within 120°C to 130°C curing windows are enabling substantial throughput improvements. Production lines utilizing these systems report up to a 40% reduction in total process cycle time due to the elimination of flash-off stages and multi-step drying requirements inherent in liquid coating lines. Material utilization efficiency is also significantly enhanced, with powder coating processes achieving transfer efficiencies between 95% and 98% through effective overspray recovery systems. This contrasts sharply with liquid spray-to-waste systems, which typically operate at 30% to 40% efficiency, resulting in higher material loss and increased operational costs.

Energy consumption is another critical driver of this transition. The integration of infrared-assisted curing technologies with low-temperature powders enables energy savings of up to 25% per unit, supporting corporate sustainability targets and ESG reporting requirements for 2026. In terms of performance, low temperature powder coatings deliver superior surface durability, achieving pencil hardness ratings of 4H to 5H and demonstrating strong resistance to moisture and household chemicals in accordance with SEFA 8 standards. These attributes are positioning powder-on-MDF technologies as a preferred finishing solution in modern furniture production ecosystems.

The automotive coatings segment is undergoing a technical shift toward low-temperature powder clear coatings for aluminum alloy wheels, driven by the need to preserve mechanical integrity while meeting stringent aesthetic and durability standards. Conventional high-temperature curing processes can induce over-aging in aluminum alloys such as A356.0-T6, leading to reduced fatigue strength and compromised impact resistance. Low-cure powder coatings, operating at or below 140°C, mitigate this issue by maintaining the original metallurgical properties of the alloy.

This preservation of mechanical properties is critical for ensuring compliance with automotive safety standards, particularly in high-performance and electric vehicles where wheel integrity directly influences vehicle dynamics. In addition to structural benefits, modern low-temperature powder clear coatings deliver advanced aesthetic performance, achieving high gloss levels exceeding 90 gloss units at 60° and maintaining superior surface uniformity with “orange peel” ratings of 7 to 8 in long-wave measurements. These finishes rival traditional liquid clear coats while offering enhanced durability.

Corrosion resistance is another key performance parameter. In Copper-Accelerated Salt Spray (CASS) testing, low-temperature powder coatings demonstrate zero creep at the scribe after 240 hours, meeting the rigorous durability standards set by global automotive OEMs for exterior components. Furthermore, reducing curing temperatures from conventional 200°C to approximately 150°C results in a 15% to 20% reduction in CO₂ emissions per production line, aligning with net-zero emission targets across Tier 1 automotive suppliers. This combination of mechanical preservation, aesthetic quality, and environmental benefits is driving widespread adoption of low-temperature powder coatings in automotive wheel finishing applications.

Stringent environmental regulations in the United States are creating a strong opportunity landscape for low temperature powder coatings, particularly within the wood furniture manufacturing sector. The Environmental Protection Agency’s enforcement of the National Emission Standards for Hazardous Air Pollutants (NESHAP) under Subpart JJ is compelling manufacturers to transition away from solvent-based coating systems toward zero-emission alternatives.

Low temperature powder coatings provide a direct pathway to compliance, as they contain zero Hazardous Air Pollutants (HAPs). This allows manufacturing facilities to reclassify from “Major Source” to “Area Source” status, significantly reducing regulatory burdens, monitoring requirements, and compliance costs. Additionally, powder coating processes generate negligible Volatile Organic Compounds (VOCs), enabling manufacturers to avoid the installation of capital-intensive emission control systems such as Regenerative Thermal Oxidizers. These systems often require multi-million-dollar investments, making powder coatings an economically attractive alternative.

Waste management benefits further enhance the value proposition. Under the Resource Conservation and Recovery Act (RCRA), powder coating waste is typically classified as non-hazardous, reducing disposal costs by up to 60% compared to hazardous sludge generated from liquid coating operations. This regulatory alignment with environmental compliance, cost reduction, and operational efficiency is expected to drive sustained adoption of low temperature powder coatings across the U.S. wood furniture manufacturing landscape.

China’s regulatory push to reduce industrial emissions is creating substantial growth opportunities for low temperature powder coatings, particularly under the Ministry of Ecology and Environment’s “VOCs Phase 3” Action Plan. This policy targets high-emission industries such as furniture manufacturing and consumer electronics production, mandating a transition to low-VOC or zero-VOC coating technologies across major industrial clusters including the Yangtze River Delta and Pearl River Delta regions.

The regulation imposes strict limits on coating formulations, effectively prohibiting products with VOC content exceeding 420 g/L in key manufacturing zones. This is driving a large-scale shift toward alternative technologies such as UV-curable coatings and low-temperature thermal powder systems. In the consumer electronics sector, the demand for low temperature powder coatings is further amplified by the increasing use of heat-sensitive substrates in device housings. Sub-130°C curing systems are essential to prevent thermal damage to internal electronic components while maintaining high-quality surface finishes.

Government incentives are reinforcing this transition. Manufacturers achieving at least a 10% reduction in VOC emissions through equipment upgrades and process optimization are eligible for tax exemptions and inclusion in “Green Supply Chain” programs. These incentives are accelerating capital investment in powder coating infrastructure, with projections indicating a record number of powder coating booth installations in 2026. This convergence of regulatory enforcement, technological advancement, and financial incentives is positioning China as a key growth hub for low temperature powder coating technologies in the global market.

Low Temperature Powder Coatings Market Share and Segmentation Insights

The low temperature powder coatings market by curing technology is led by thermal cure (low-bake) systems, accounting for 55% of the global market share in 2025, driven by their balance of performance, cost-efficiency, and equipment compatibility. These coatings utilize engineered resin systems such as polyester, epoxy, and polyurethane, enhanced with specialized catalysts and blocked crosslinkers that enable curing at reduced temperatures of 120–150°C, compared to conventional 180–200°C systems. This advancement makes them ideal for heat-sensitive substrates including MDF furniture, plastic components, and assembled electronic enclosures. As the industry standard, low-bake thermal powders are widely adopted across automotive underhood parts, consumer appliances, and industrial components, where durability, adhesion, and finish quality must be maintained without compromising substrate integrity. Their scalability and compatibility with existing curing infrastructure further reinforce their dominance.

Contract Coating Job Shops Hold 52% Share by Enabling Cost-Effective Batch Processing

In the low temperature powder coatings market by sales channel, contract coating job shops lead with a 52% market share in 2025, supported by their ability to deliver cost-effective coating services without requiring in-house capital investment. Powder coating operations demand specialized infrastructure, including electrostatic spray guns, curing ovens, and powder recovery systems, which represent significant upfront costs. Job shops amortize these investments across multiple clients and industries, making them the preferred choice for manufacturers. Additionally, they excel in batch processing for small-to-medium production runs (100–10,000 parts), particularly in sectors such as furniture, lighting fixtures, and electronic housings, where production volumes do not justify dedicated coating lines. Their operational flexibility, combined with technical expertise in low-temperature powder application, positions contract job shops as the dominant channel for delivering high-quality, energy-efficient coating solutions.

Competitive Landscape in the Low Temperature Powder Coatings Market

AkzoNobel drives ultra-low-bake innovation and sustainable powder coating leadership

AkzoNobel continues to lead the low temperature powder coatings market by positioning itself as an efficiency-focused innovator through its Interpon and Resicoat brands. The company is advancing toward a landmark merger with Axalta, targeting approximately $600 million in cost synergies and an EBITDA margin near 20%, strengthening its global coatings leadership. Its collaboration with IPG Photonics in 2026 introduced laser-curing technology, enabling ultra-fast curing cycles and reducing energy consumption by up to 30%. The Interpon Low-E series allows curing at temperatures as low as 150°C, improving line speeds by 20%. Additionally, AkzoNobel achieved a 47% reduction in Scope 1 and 2 emissions by 2025 and is accelerating the adoption of bio-attributed resins to replace fossil-based binders.

PPG expands circular low-temperature powder coatings for automotive and energy applications

PPG Industries is strengthening its position in low temperature powder coatings by integrating circular economy principles with high-performance formulations. In 2026, the company launched ENVIROLUXE™ Plus, a PFAS-free powder coating containing up to 18% recycled plastic (rPET), targeting sustainable industrial applications. Its strategic partnership with PlusCoat in Denmark is enhancing coating efficiency across the EMEA region, supporting industrial scalability. PPG’s coatings are widely used in LPG tanks and EV battery enclosures, delivering corrosion protection with a carbon footprint approximately 30% lower than conventional powders. The company’s expertise in high-edge protection coatings ensures uniform coverage on complex geometries, addressing a critical limitation in traditional powder coating technologies.

Axalta advances bio-based and ultra-low-bake powder coatings for mobility and architecture

Axalta Coating Systems is a key innovator in sustainable powder coatings, with a strong focus on mobility and architectural applications. Its Alesta® BioCore product line has achieved ISCC PLUS certification, utilizing renewable feedstocks such as used cooking oil and sugar beet pulp to reduce CO₂ emissions by approximately 25% per kilogram. Axalta’s investment in digital supply chain optimization earned it a 2026 SAP Innovation Award, highlighting its ability to manage temperature-sensitive products efficiently. The company is actively developing ultra-low-bake powder coatings capable of curing below the traditional 180°C threshold while maintaining long-term durability, including 25-year performance warranties. Its strategic shift toward high-value specialty coatings is designed to protect margins amid global overcapacity in commodity chemicals.

Sherwin-Williams strengthens low-temperature powder coatings for heat-sensitive substrates

The Sherwin-Williams Company dominates the North American segment of low temperature powder coatings, focusing on applications involving heat-sensitive substrates and industrial durability. Its solutions are widely adopted in consumer electronics and furniture manufacturing, particularly for Medium-Density Fiberboard (MDF) and specialty alloys that cannot withstand high curing temperatures. Following record net sales of $23.57 billion in 2025, the company is expanding its Paint Stores Group to provide localized technical support for industrial low-cure applications. Sherwin-Williams has developed advanced catalyst technologies that enable full cross-linking at temperatures as low as 150°C without compromising film integrity. Its FIRETEX® line further integrates passive fire protection with low-temperature application capabilities for offshore and petrochemical environments.

TIGER Coatings drives flexible curing and architectural durability in powder coatings

TIGER Coatings is a specialized high-performance player known for its innovation in architectural powder coatings and flexible curing technologies. Its TIGER Drylac® portfolio includes the Series 138 “Flex Cure” system, which allows real-time adjustment of curing cycles to match production requirements, improving operational efficiency. The company is a market leader in AAMA 2604-compliant super durable powders, with its Series 38/138 systems demonstrating over 30% gloss retention after five years of Florida exposure testing. TIGER is expanding its 3D Metallics and Hyper Durable color portfolios to meet growing demand for aesthetic durability in premium facades and marine applications. Its TIGER Shield system integrates advanced primer and topcoat technologies to deliver superior corrosion resistance in harsh environments.

Germany Low Temperature Powder Coatings Market: Driving Climate-Neutral Finishing with Ultra-Low Bake Technologies

Germany leads the low temperature powder coatings (LTPC) market in Europe, driven by stringent energy efficiency mandates and a strong commitment to climate-neutral industrial finishing. The development of Ultra-Low Bake (ULB) powder coatings, capable of achieving full cross-linking at temperatures as low as 120°C to 130°C, is revolutionizing coating processes for heavy-duty metal castings and thermally sensitive substrates. This innovation is particularly critical for industries aiming to reduce natural gas consumption in curing ovens while maintaining high-performance coating standards.

Government initiatives, including funding from the Federal Ministry for Economic Affairs (BMWK), are accelerating the adoption of infrared (IR) and UV-LED curing technologies, enabling manufacturers to retrofit existing powder coating lines for energy efficiency. Germany’s automotive sector is a major adopter, using LTPC for aluminum alloy wheels and EV battery enclosures, where heat sensitivity and lightweight materials are key considerations. Additionally, the commercialization of bio-based LTPC resins is reducing carbon footprints, aligning with EU sustainability goals. Investments in hybrid smart coating lines with real-time temperature optimization further strengthen Germany’s position as a leader in next-generation coating technologies.

United States Low Temperature Powder Coatings Market: Expanding Powder-on-Non-Metal Applications and Sustainable Innovations

The United States is shaping the low temperature powder coatings market through innovation in heat-sensitive substrate applications and sustainable coating formulations. The integration of dual-cure (thermal and UV) technologies is enabling high-quality powder coating on non-metal materials such as medium-density fibreboard (MDF), particularly in the furniture and architectural sectors.

The market is witnessing strong adoption in defense sustainment programs, where low-cure powders are used to refurbish composite components that cannot tolerate high heat exposure. Leading manufacturers are introducing PFAS-free powder coatings, aligning with evolving EPA regulations and the growing demand for environmentally safe materials. Investments in smart oven technologies with real-time monitoring are reducing energy waste and improving process efficiency across manufacturing hubs in the Midwest. Regulatory enforcement of SCAQMD Rule 1113 continues to push the shift toward zero-VOC powder coatings, making them a preferred alternative to liquid systems.

China Low Temperature Powder Coatings Market: High-Volume Manufacturing and VOC Reduction Initiatives

China dominates the global LTPC market in terms of volume, driven by its focus on industrial modernization, emission reduction, and large-scale manufacturing capacity expansion. Government policies under the “14th Five-Year Plan” are actively promoting the transition from liquid coatings to powder coatings, incentivizing manufacturers to reduce VOC emissions by up to 40%.

Technological advancements in high-efficiency curing catalysts are enabling standard powder coating systems to operate at lower temperatures without compromising chemical resistance or durability. The market is particularly strong in the white goods sector, where low temperature coatings prevent deformation of thin steel panels during curing. Significant investments in robotic powder application systems are ensuring consistent coating quality, which is critical for low-temperature formulations. The expansion of large-scale MDF powder coating lines, such as the facility in Guangdong, highlights China’s growing capability to support high-volume furniture manufacturing with energy-efficient coating technologies.

India Low Temperature Powder Coatings Market: MSME Adoption and Infrastructure Growth Accelerating Demand

India is emerging as one of the fastest-growing markets for low temperature powder coatings, driven by expanding manufacturing activities and strong government support for energy-efficient industrial processes. The “Make in India” initiative has led to the development of numerous industrial estates, where LTPC is being promoted as a cost-effective solution for Micro, Small, and Medium Enterprises (MSMEs) seeking to reduce operational expenses.

The application of LTPC in agriculture and construction equipment (ACE) is gaining traction, as it reduces oven soak time and increases production efficiency. Government subsidies covering up to 25% of the cost of energy-efficient coating equipment are encouraging adoption among domestic manufacturers. Companies like Kansai Nerolac are introducing specialized low-cure powder coatings tailored to India’s climate conditions. Additionally, sectors such as electrical cabinets, switchgear, and EV two-wheelers are witnessing increased use of LTPC for improved durability, corrosion resistance, and lightweight component finishing.

Japan Low Temperature Powder Coatings Market: Precision Coatings and Advanced Functional Materials

Japan’s LTPC market is defined by its focus on precision engineering, advanced materials, and high-performance functional coatings. The development of nanocomposite low temperature powders is enhancing scratch resistance and providing advanced features such as anti-fingerprint surfaces, particularly in premium consumer electronics.

Japanese manufacturers are also pioneering innovations in room-temperature stable powder coatings, addressing storage and handling challenges associated with low-melt-point materials. These coatings are widely used in industrial robotics, where sensitive components require protection without exposure to high heat. The country’s strict regulatory environment under the Chemical Substances Control Law (CSCL) is driving the adoption of bio-renewable curing agents and sustainable coating technologies. Additionally, major automotive manufacturers are integrating low-temperature curing standards across supply chains, further accelerating market adoption.

South Korea Low Temperature Powder Coatings Market: Semiconductor Growth and Energy Storage Applications Driving Innovation

South Korea is leveraging its leadership in semiconductor manufacturing and energy storage systems (ESS) to drive demand for low temperature powder coatings. Investments in the Gyeonggi Province semiconductor cluster are increasing the need for coatings used in cleanroom equipment and furniture, where low-energy curing and zero outgassing are critical requirements.

Technological advancements such as moisture-cure low temperature powder coatings are enabling application on non-conductive substrates like plastics and glass, expanding the scope of LTPC applications. These coatings are also widely used in EV battery manifolds, providing electrical insulation and dielectric strength without compromising component integrity. Regulatory updates under K-REACH are encouraging the elimination of hazardous chemicals like TGIC, promoting safer and more sustainable formulations. Companies such as KCC Corporation are investing in innovation centers focused on rapid-cure technologies for shipbuilding and offshore energy applications, further strengthening South Korea’s position in advanced coatings markets.

Low Temperature Powder Coatings Market Report Scope

Low Temperature Powder Coatings Market

Parameter

Details

Market Size (2025)

$206.1 Million

Market Size (2032)

$309.9 Million

Market Growth Rate

6%

Segments

By Resin (Polyester, Epoxy, Epoxy-Polyester Hybrid, Polyurethane, Acrylic, Specialty Resins), By Substrate (Non-Metal, Metal), By Curing Technology (Thermal Cure, Ultra-Low Bake, Radiation-Cured, Catalytic Infrared), By End-Use Industry (Automotive and Transportation, Furniture, Electronics and Electrical, Appliances, Architectural and Construction, Healthcare and Medical, Industrial Machinery), By Functional Performance (Corrosion Resistance, Chemical and Stain Resistance, UV and Weathering Stability, Anti-Microbial Properties, Aesthetic Finishes), By Sales Channel (Direct Sales, Specialty Industrial Distributors, Contract Coating Job Shops)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

Akzo Nobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Axalta Coating Systems Ltd., Jotun A/S, Tiger Coatings GmbH and Co. KG, Teknos Group, IGP Pulvertechnik AG, Kansai Paint Co., Ltd., Hempel A/S, TCI Powder Coatings, Forrest Technical Coatings, Vitracoat America Inc., Protective Coatings Inc., Berger Paints India Limited

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Low Temperature Powder Coatings Market Segmentation

By Resin

Polyester

Epoxy

Epoxy-Polyester Hybrid

Polyurethane

Acrylic

Specialty Resins

By Substrate

Non-Metal

Metal

By Curing Technology

Thermal Cure

Ultra-Low Bake

Radiation-Cured

Catalytic Infrared

By End-Use Industry

Automotive and Transportation

Furniture

Electronics and Electrical

Appliances

Architectural and Construction

Healthcare and Medical

Industrial Machinery

By Functional Performance

Corrosion Resistance

Chemical and Stain Resistance

UV and Weathering Stability

Anti-Microbial Properties

Aesthetic Finishes

By Sales Channel

Direct Sales

Specialty Industrial Distributors

Contract Coating Job Shops

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Low Temperature Powder Coatings Industry

Akzo Nobel N.V.

PPG Industries, Inc.

The Sherwin-Williams Company

Axalta Coating Systems Ltd.

Jotun A/S

Tiger Coatings GmbH & Co. KG

Teknos Group

IGP Pulvertechnik AG

Kansai Paint Co., Ltd.

Hempel A/S

TCI Powder Coatings

Forrest Technical Coatings

Vitracoat America Inc.

Protective Coatings Inc.

Berger Paints India Limited

*- List not Exhaustive

Table of Contents: Low Temperature Powder Coatings Market

2. Low Temperature Powder Coatings Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Low Temperature Powder Coatings Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers

2.4. Market Restraints and Challenges

2.5. Market Opportunities

2.6. Regulatory and Sustainability Landscape

2.7. Value Chain Analysis

2.8. Pricing Analysis

2.9. Technology Roadmap and Future Outlook

3. Innovations Reshaping the Low Temperature Powder Coatings Market

3.1. Trend: MDF Furniture Manufacturing Transitioning to Low-Cure Powder Coating Systems

3.2. Trend: Low-Temperature Powder Clear Coatings Enhancing Aluminum Wheel Performance

3.3. Opportunity: EPA NESHAP Regulations Accelerating Powder Coating Adoption in Wood Furniture

3.4. Opportunity: China’s VOC Phase 3 Policy Driving Transition to Zero-VOC Powder Coatings

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Low Temperature Powder Coatings Market

5.1. By Resin

5.1.1. Polyester

5.1.2. Epoxy

5.1.3. Epoxy-Polyester Hybrid

5.1.4. Polyurethane

5.1.5. Acrylic

5.1.6. Specialty Resins

5.2. By Substrate

5.2.1. Non-Metal

5.2.2. Metal

5.3. By Curing Technology

5.3.1. Thermal Cure

5.3.2. Ultra-Low Bake

5.3.3. Radiation-Cured

5.3.4. Catalytic Infrared

5.4. By End-Use Industry

5.4.1. Automotive and Transportation

5.4.2. Furniture

5.4.3. Electronics and Electrical

5.4.4. Appliances

5.4.5. Architectural and Construction

5.4.6. Healthcare and Medical

5.4.7. Industrial Machinery

5.5. By Functional Performance

5.5.1. Corrosion Resistance

5.5.2. Chemical and Stain Resistance

5.5.3. UV and Weathering Stability

5.5.4. Anti-Microbial Properties

5.5.5. Aesthetic Finishes

5.6. By Sales Channel

5.6.1. Direct Sales

5.6.2. Specialty Industrial Distributors

5.6.3. Contract Coating Job Shops

6. Country Analysis and Outlook of Low Temperature Powder Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Low Temperature Powder Coatings Market Size Outlook by Region (2025–2034)

7.1. North America Low Temperature Powder Coatings Market Size Outlook to 2034

7.1.1. By Resin

7.1.2. By Substrate

7.1.3. By Curing Technology

7.1.4. By End-Use Industry

7.1.5. By Functional Performance

7.1.6. By Sales Channel

7.2. Europe Low Temperature Powder Coatings Market Size Outlook to 2034

7.2.1. By Resin

7.2.2. By Substrate

7.2.3. By Curing Technology

7.2.4. By End-Use Industry

7.2.5. By Functional Performance

7.2.6. By Sales Channel

7.3. Asia Pacific Low Temperature Powder Coatings Market Size Outlook to 2034

7.3.1. By Resin

7.3.2. By Substrate

7.3.3. By Curing Technology

7.3.4. By End-Use Industry

7.3.5. By Functional Performance

7.3.6. By Sales Channel

7.4. South America Low Temperature Powder Coatings Market Size Outlook to 2034

7.4.1. By Resin

7.4.2. By Substrate

7.4.3. By Curing Technology

7.4.4. By End-Use Industry

7.4.5. By Functional Performance

7.4.6. By Sales Channel

7.5. Middle East and Africa Low Temperature Powder Coatings Market Size Outlook to 2034

7.5.1. By Resin

7.5.2. By Substrate

7.5.3. By Curing Technology

7.5.4. By End-Use Industry

7.5.5. By Functional Performance

7.5.6. By Sales Channel

8. Company Profiles: Leading Players in the Low Temperature Powder Coatings Market

8.1. Akzo Nobel N.V.

8.2. PPG Industries, Inc.

8.3. The Sherwin-Williams Company

8.4. Axalta Coating Systems Ltd.

8.5. Jotun A/S

8.6. Tiger Coatings GmbH and Co. KG

8.7. Teknos Group

8.8. IGP Pulvertechnik AG

8.9. Kansai Paint Co., Ltd.

8.10. Hempel A/S

8.11. TCI Powder Coatings

8.12. Forrest Technical Coatings

8.13. Vitracoat America Inc.

8.14. Protective Coatings Inc.

8.15. Berger Paints India Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Low Temperature Powder Coatings Market Segmentation

By Resin

Polyester

Epoxy

Epoxy-Polyester Hybrid

Polyurethane

Acrylic

Specialty Resins

By Substrate

Non-Metal

Metal

By Curing Technology

Thermal Cure

Ultra-Low Bake

Radiation-Cured

Catalytic Infrared

By End-Use Industry

Automotive and Transportation

Furniture

Electronics and Electrical

Appliances

Architectural and Construction

Healthcare and Medical

Industrial Machinery

By Functional Performance

Corrosion Resistance

Chemical and Stain Resistance

UV and Weathering Stability

Anti-Microbial Properties

Aesthetic Finishes

By Sales Channel

Direct Sales

Specialty Industrial Distributors

Contract Coating Job Shops

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global low temperature powder coatings market was valued at $206.1 million in 2025 and is projected to reach $309.9 million by 2032, growing at a CAGR of 6%. Market growth is being fueled by rising demand for low-cure powder coatings, ultra-low bake technologies, and sustainable coating systems across furniture, automotive, appliances, electronics, and industrial manufacturing sectors focused on energy efficiency and reduced emissions.

Low temperature powder coatings cure at significantly lower temperatures of 120°C to 150°C, enabling coating of medium-density fiberboard (MDF), plastics, lightweight composites, and electronic housings without warping or thermal damage. Manufacturers are increasingly replacing solvent-based liquid coatings with powder-on-MDF systems because they improve transfer efficiency to 95%–98%, reduce process cycle times by up to 40%, and deliver superior durability, chemical resistance, and surface performance.

Stringent VOC and HAP emission regulations in the United States, Europe, and China are accelerating the transition from solvent-based coatings to zero-VOC powder coating systems. Manufacturers are adopting PFAS-free formulations, recycled PET-based coatings, and bio-based resin technologies to meet ESG targets and green building standards. Low temperature powder coatings also help reduce energy consumption and CO₂ emissions by 15% to 30% compared to conventional high-temperature curing systems.

Furniture manufacturing, automotive wheel coatings, EV battery components, appliances, architectural products, and industrial machinery are generating major demand for low temperature powder coatings. Europe leads in sustainable powder coating innovation and low-energy curing technologies, while Asia-Pacific is emerging as the fastest-growing region due to expanding furniture production, industrial manufacturing, and VOC reduction policies in China, India, South Korea, and Japan.

Major companies operating in the low temperature powder coatings industry include Akzo Nobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Axalta Coating Systems Ltd., Jotun A/S, Tiger Coatings GmbH & Co. KG, Teknos Group, and Kansai Paint Co., Ltd.. These companies are investing heavily in ultra-low bake technologies, PFAS-free powder coatings, bio-based resins, recycled-content formulations, and energy-efficient curing systems to strengthen their competitive positions globally.