Mold Release Coatings Market Size, PFAS-Free Technologies, and High-Performance Molding Applications Outlook

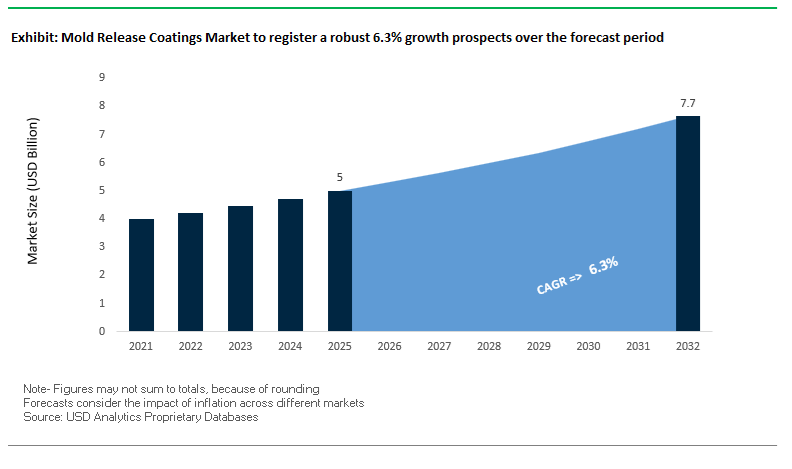

The global mold release coatings market was valued at $5 billion in 2025 and is projected to reach $7.7 billion by 2032, expanding at a CAGR of 6.3%. Market growth is driven by increasing demand for mold release agents, semi-permanent release coatings, water-based release systems, silicone-based release coatings, and PFAS-free mold release solutions across automotive, aerospace, rubber, plastics, composites, and food packaging industries. These coatings are critical in ensuring clean part release, improved surface finish, reduced cycle times, and extended mold life, making them essential for high-volume manufacturing environments.

A key growth driver is the rapid expansion of composite manufacturing and lightweight materials, particularly in electric vehicles (EVs), aerospace structures, and wind energy components, where precision molding is required. Mold release coatings play a vital role in enabling complex geometries, defect-free surfaces, and efficient demolding processes. Additionally, increasing regulatory pressure to eliminate hazardous chemicals such as PFAS and high-VOC solvents is accelerating the adoption of environmentally friendly, water-based, and bio-based release agents.

The market is also benefiting from advancements in nanotechnology, silicone chemistry, and biomimetic surface engineering, which enhance lubricity, durability, and thermal stability. Demand is rising for food-grade and medical-grade release coatings, where compliance with strict safety standards is essential. Regionally, Asia-Pacific dominates due to strong manufacturing activity, while Europe leads in sustainability-driven innovation and regulatory compliance.

The mold release coatings industry is undergoing significant transformation driven by sustainability mandates, advanced material innovation, and expanding applications in high-performance manufacturing sectors. In March 2026, Henkel reported strong growth in its Adhesive Technologies segment and confirmed a strategic focus on low-emission mold release solutions targeting EV and aerospace composite markets, reflecting the increasing importance of environmentally compliant coatings in advanced manufacturing.

Sustainability is a central theme shaping product development. Chem-Trend achieved a major milestone in September 2025 by surpassing its PFAS elimination goals, transitioning its global portfolio to PFAS-free chemistries ahead of regulatory deadlines. This shift is complemented by Münch Chemie’s December 2025 launch of MK-69/11 and MK-77, which are PFAS-free and silicone-free release agents designed for rubber processing, offering both semi-permanent performance and high-efficiency production.

Water-based technologies are gaining rapid traction as manufacturers seek to reduce VOC emissions and improve workplace safety. Chem-Trend’s August 2025 introduction of water-based release systems for composite manufacturing enhances tool life and process efficiency, particularly in the production of wind turbine blades and aerospace components. Similarly, Stoner Molding’s April 2025 launch of the B445 denesting agent provides a food-safe, water-based solution for high-speed packaging lines, ensuring clean release and reduced static in thermoforming processes.

Product innovation is also focused on improving process efficiency and material performance. Chem-Trend’s March 2025 SL-10187 release agent for high-pressure aluminum casting enhances heat exchange and biostability, enabling shorter cycle times and improved surface finishes in automotive components. Additionally, Kao Corporation’s May 2024 launch of LUNAFLOW RA, based on cellulose nanofiber (CNF) technology, introduces a biomimetic, solvent-free release system inspired by natural surfaces, representing a breakthrough in sustainable release coating design.

Strategic R&D and operational focus are expanding into specialized applications. Wacker Chemie’s March 2026 strategy emphasizes silicone-based release agents for medical and food-grade molding, addressing the growing need for high-purity and compliant coating solutions. Meanwhile, Chem-Trend’s Next-Gen Tire Molding Solutions, launched in February 2024, are optimized for complex EV tire designs, improving release efficiency and tread precision.

Leadership and strategic direction are also influencing market dynamics. Chem-Trend’s March 2024 leadership transition marked the beginning of a renewed focus on digital integration and advanced product development, strengthening its position in thermoplastics and industrial molding applications.

The mold release coatings industry is undergoing a structural transition in aerospace composites, with manufacturers rapidly shifting from solvent-borne, sacrificial release agents to water-based semi-permanent systems. This transition is driven by stringent environmental regulations, the need for improved workplace safety, and the increasing demand for defect-free composite surfaces suitable for secondary bonding and high-performance coatings.

Water-based semi-permanent formulations deliver substantial reductions in volatile organic compound emissions, achieving 80% to 95% lower VOC output compared to traditional solvent-based wipe-on systems. This improvement directly enhances air quality within confined composite layup environments, addressing occupational health concerns while supporting compliance with evolving environmental standards. Beyond emissions, these coatings are engineered to maintain extremely low surface energy, typically below 20 mN/m, enabling precise resin flow control during molding processes. This ensures high-quality surface finishes with minimal defects and eliminates contamination transfer, removing the need for post-demolding cleaning or sanding in approximately 92% of aerospace components.

Operational efficiency gains are also significant. Unlike single-use sacrificial coatings, semi-permanent systems provide multiple release cycles per application, typically ranging from 5 to 15 releases depending on resin chemistry and mold geometry. This reduces tool preparation time by approximately 40%, improving throughput and lowering labor costs. As aerospace manufacturers continue to scale composite production for next-generation aircraft platforms, water-based semi-permanent mold release coatings are emerging as a critical enabler of efficiency, quality, and regulatory compliance.

The wind energy sector is driving demand for high-durability mold release coatings as turbine blade dimensions exceed 100 meters and production cycles become increasingly time-sensitive. Manufacturers are adopting fluoropolymer-based systems, including PTFE and PFA formulations, to address the challenges associated with large-scale composite demolding and to minimize costly mold downtime.

These advanced coatings offer significantly extended release cycles, supporting between 50 and 100 or more demolding operations before requiring reapplication. This represents a tenfold increase compared to conventional wax-based systems, substantially improving mold utilization and production efficiency. Given the scale and cost of wind turbine blade molds, this extended lifecycle directly translates into reduced downtime and lower operational costs.

Friction reduction is another critical performance parameter. Fluoropolymer-based coatings achieve static coefficients of friction below 0.05, enabling smooth and damage-free release of large composite structures, including blades weighing over 25 metric tons. This low-friction interface is essential for maintaining structural integrity and minimizing defects during demolding.

Thermal stability further enhances the suitability of these coatings for modern manufacturing processes. Fluoropolymer systems maintain performance at continuous operating temperatures between 150°C and 200°C, supporting accelerated cure cycles that reduce overall production time by approximately 15%. As wind energy deployment expands globally, the demand for high-performance mold release coatings that enable faster, more reliable manufacturing is expected to increase significantly.

Market Opportunity: EPA NESHAP Amendments Driving Adoption of Low-HAP and Low-VOC Mold Release Technologies

The regulatory landscape in the United States is creating substantial opportunities for advanced mold release coatings, particularly following the 2026 amendments to the National Emission Standards for Hazardous Air Pollutants. These regulations target emissions from chemical manufacturing and composite processing, placing increased pressure on manufacturers to reduce VOC and hazardous air pollutant output.

The updated standards aim to eliminate over 1,500 tons of VOC emissions annually, compelling composite manufacturers to phase out solvent-based release agents containing aromatic hydrocarbons such as toluene and xylene. This regulatory shift is accelerating the adoption of waterborne and high-solids mold release systems that meet low-emission criteria while maintaining performance.

In addition to emission limits, the introduction of mandatory electronic reporting through systems such as the Compliance and Emissions Data Reporting Interface is increasing transparency and compliance complexity. This is driving demand for pre-certified mold release products that simplify reporting requirements and reduce administrative burdens. Suppliers offering validated low-HAP solutions with documented performance data are gaining a competitive advantage, as manufacturers seek to streamline compliance processes while maintaining production efficiency.

These regulatory changes are reinforcing the transition toward environmentally compliant mold release technologies, creating sustained growth opportunities for suppliers aligned with low-emission and high-performance product development.

Market Opportunity: China’s Blue-Sky Action Plan Driving Mandatory Transition to Ultra-Low VOC Mold Release Systems

China’s environmental policy framework is creating a large-scale transformation in the mold release coatings market, particularly under the final phase of the Blue Sky Action Plan. This initiative targets high-emission industrial processes and mandates the elimination of solvent-based chemicals in key manufacturing regions, including the Greater Bay Area and the Yangtze River Delta.

Beginning in 2027, the use of high-VOC solvent-based mold release agents will be effectively prohibited in these regions, requiring manufacturers in automotive, electronics, and composite industries to transition to waterborne or high-solids alternatives. This regulatory enforcement is creating immediate demand for compliant mold release technologies that can deliver equivalent or superior performance without reliance on volatile solvents.

The introduction of Green Product certification under GB/T 35609-2025 further reinforces this shift. Only products meeting ultra-low VOC thresholds, typically below 10% solvent content, qualify for certification, which is increasingly required for participation in government-backed industrial and infrastructure projects. This creates a strong incentive for manufacturers to adopt certified low-emission solutions and for suppliers to develop formulations aligned with regulatory standards.

The scale of China’s manufacturing base amplifies the impact of these policies, positioning the country as a major growth driver for advanced mold release coatings. Companies capable of delivering high-performance, environmentally compliant systems are expected to benefit from sustained demand as regulatory enforcement intensifies across key industrial sectors.

Mold Release Coatings Market Share and Segmentation Insights

Semi-Permanent Coatings Capture 52% Share Driven by Multi-Release Performance and Clean Part Finishes

The mold release coatings market by type is led by semi-permanent mold release coatings, accounting for 52% of the global market share in 2025, due to their superior efficiency in high-volume composite manufacturing. These advanced coatings provide 10–50 release cycles per application, significantly reducing downtime, labor costs, and reapplication frequency in industries such as automotive, aerospace, and wind energy blade production. Unlike traditional sacrificial agents, semi-permanent coatings chemically bond to mold surfaces (steel, aluminum, composite) and do not transfer onto molded parts, eliminating the need for secondary cleaning and surface preparation. This results in improved production throughput and consistent part quality. As demand rises for high-performance mold release agents and cost-efficient composite processing, semi-permanent coatings continue to dominate the global market.

Direct Sales Hold 55% Share Due to Complex Formulation Requirements and On-Site Technical Support

In the mold release coatings market by sales channel, direct sales dominate with a 55% market share in 2025, reflecting the highly technical and application-specific nature of these coatings. Mold release formulations must be precisely tailored to mold materials (steel, aluminum, composites), resin chemistries (epoxy, polyester, polyurethane), and processing temperatures, making direct supplier engagement essential for optimal performance. Manufacturers rely heavily on technical consultation and on-site support to fine-tune parameters such as application frequency, curing cycles, and film thickness, ensuring minimal defects and reduced scrap rates. This close collaboration enhances production efficiency and consistency, particularly in complex molding operations. As industries increasingly demand customized mold release solutions and process optimization, direct sales channels remain the preferred route in the global mold release coatings market.

Competitive Landscape in the Mold Release Coatings Market

Chem-Trend leads PFAS-free and carrier-free mold release innovation for sustainable manufacturing

Chem-Trend, part of the Freudenberg Group, is the global leader in mold release coatings, driving the transition toward environmentally compliant technologies. By 2026, the company achieved a 100% PFAS-free portfolio for composite and rubber molding applications, surpassing its sustainability targets. Its Carrier-Free™ technology eliminates vapor emissions and waste streams, making it particularly effective for die-casting and rotational molding processes. Chem-Trend dominates the semi-permanent release segment with coatings that chemically bond to mold surfaces, enabling multiple release cycles per application and reducing maintenance downtime. Supported by Freudenberg’s global logistics network, the company delivers integrated “Total Process Solutions,” combining cleaning, sealing, and release systems for optimized manufacturing performance.

Henkel expands mold release ecosystem with VOC-free coatings and strategic acquisitions

Henkel AG & Co. KGaA is strengthening its position in mold release coatings through its Adhesive Technologies division and ecosystem-based approach. In 2026, the company agreed to acquire the Stahl Group for €2.1 billion, expanding its capabilities in specialty coatings for automotive, fashion, and flexible materials. Its Loctite Stycast UV 7998 coating offers a solvent-free, UL 94 V-0 rated solution that functions as both a protective and release coating for electronic components, reducing CO₂ emissions by up to 40%. Henkel is transitioning toward 100% VOC-free and water-based solutions, aligning with its “Purposeful Growth” strategy. Its expertise in hybrid coatings enables applications across electronics, packaging, and industrial manufacturing sectors.

Wacker advances silicone-based release coatings with precision measurement and medical-grade solutions

Wacker Chemie AG is a leader in silicone-based mold release coatings, particularly for medical, label, and tape applications. Its DEHESIVE® platform is widely recognized as the global standard for silicone release coatings on paper and film substrates, offering consistent performance in high-speed production environments. In 2026, Wacker introduced an XRF-based measurement method to accurately quantify extractable silicone, enhancing process control and cost efficiency. The company also developed gamma-sterilizable silicone PSA technology, addressing the shift away from ethylene oxide sterilization in medical applications. Wacker’s focus on solvent-free RTV-2 silicone systems supports sustainability while maintaining high performance in demanding industrial and healthcare environments.

Daikin drives precision mold release coatings with eco-compliant fluoropolymer technologies

Daikin Industries is a key player in fluoropolymer-based mold release coatings, focusing on high-precision applications such as semiconductors and optics. The company is advancing nanolayer coating technologies that deliver ultra-thin release films at sub-micron levels, ensuring high accuracy in precision molding processes. Daikin is also developing water-based fluoropolymer dispersions that match the performance of traditional solvent-based systems while meeting 2026 global safety standards. Its strategic collaborations with automotive OEMs support the development of specialized release coatings for EV battery enclosures and lightweight composite materials. With strong presence in Japan and Southeast Asia, Daikin continues to expand its footprint in advanced manufacturing sectors.

Münch Chemie strengthens composite molding solutions with waterborne release systems

Münch Chemie-Methyl GmbH is a specialized provider of mold release coatings for aerospace and wind energy applications, focusing on polyurethane and composite molding processes. Its waterborne, solvent-free release agents are optimized for closed-mold techniques such as RTM and VARTM, offering low buildup and high thermal resistance under exothermic conditions. The company is expanding its technical service centers in Southeast Asia and Eastern Europe to support emerging aerospace manufacturing hubs. Münch’s integrated system solutions combine mold cleaners, sealers, and semi-permanent coatings to deliver consistent surface finish and improved post-processing adhesion, making it a preferred partner for high-performance composite applications.

Marbocote advances zero-transfer mold release coatings for high-end composite applications

Marbocote Ltd. is a niche innovator in mold release coatings, specializing in composite applications for high-performance industries such as Formula 1 and luxury marine manufacturing. The company’s zero-transfer technology ensures no residue remains on molded parts, eliminating the need for secondary cleaning or sanding before bonding or painting. Its advanced release systems enable Class A surface finishes directly from the mold, reducing production steps and costs. Marbocote is also expanding its presence in the renewable energy sector, particularly for wind turbine blade manufacturing. By transitioning to low-odor and low-VOC formulations, the company aligns with European Green Deal requirements while maintaining high-performance release characteristics.

United States Mold Release Coatings Market: PFAS-Free Innovation and Aerospace Composite Manufacturing Leadership

The United States leads the mold release coatings market, driven by rapid innovation in PFAS-free, water-based semi-permanent release systems and strong demand from aerospace composites and EV lightweighting applications. The introduction of fluorine-free mold release coatings is enabling performance parity with legacy solvent-based systems, particularly for epoxy and phenolic resin molding. Advanced developments such as “smart-transfer” coatings are reducing pre-release defects in complex aerospace components, improving yield and surface quality.

Stringent environmental regulations from the EPA, limiting VOC emissions to below 250 g/L, are accelerating the shift toward water-dilutable mold release coatings, resulting in significant industry transformation. Infrastructure investments in nano-ceramic release coating R&D labs are supporting high-pressure die casting (HPDC) for EV battery housings. Additionally, the integration of robotic spray systems in aerospace manufacturing facilities is ensuring micron-level coating uniformity, essential for stealth and aerodynamic performance. The U.S. also dominates applications such as large-scale wind blade manufacturing, where high-slip coatings enable efficient release of ultra-large composite structures.

Germany stands as a European leader in sustainable mold release coatings, focusing on bio-based formulations, silicone-free technologies, and circular manufacturing processes. Innovations such as plant-derived rheology modifiers are replacing petroleum-based waxes, significantly reducing environmental impact while maintaining high performance.

The adoption of cross-linking silicone-free (CSF) mold release coatings is eliminating surface residues, allowing for immediate post-molding processes such as painting and bonding without additional cleaning steps. Strong alignment with the EU Green Deal is driving mandatory tracking of the carbon footprint per release cycle, reinforcing sustainability across the value chain. Industrial expansion by companies like Freudenberg Group is supporting the production of advanced waterborne coatings for polyurethane applications in furniture and footwear. Germany’s leadership in precision automotive interior molding, particularly for soft-touch components, highlights its focus on high-quality, defect-free surface finishes.

China Mold Release Coatings Market: High-Volume Manufacturing and Smart Coating Integration

China dominates the mold release coatings market in volume, supported by large-scale manufacturing and rapid adoption of smart, high-solid, and waterborne release technologies. Government initiatives such as the “Blue Sky Defense War” are penalizing solvent-heavy operations, resulting in a surge in demand for low-VOC, water-based release coatings across industrial sectors.

Technological advancements include the development of encapsulated pigment technologies, enabling in-mold coating (IMC) processes where color and release agents are applied simultaneously, improving efficiency and reducing processing steps. China’s expansion into semiconductor packaging and electronic manufacturing is driving demand for precision release coatings that prevent electrostatic discharge during part removal. Investments in domestic production of PTFE-alternative chemistries are strengthening supply chain independence, while innovations in high-heat-resistant coatings are supporting magnesium alloy die casting applications.

Japan Mold Release Coatings Market: Nano-Structured Coatings and Zero-Defect Manufacturing

Japan’s mold release coatings market is defined by precision engineering, nanotechnology innovation, and zero-defect manufacturing standards. The development of nano-structured “lotus-effect” coatings is enabling release performance based on surface topography rather than chemical interaction, offering extended lifecycle and minimal maintenance.

Technological leadership includes visible-light cured mold release coatings, enabling ultra-fast curing times for high-speed injection molding processes. These coatings are widely used in medical device manufacturing, where USP Class VI-certified materials ensure zero contamination. Japan is also integrating self-diagnostic sensors within mold cavities, enabling real-time monitoring of coating performance and wear. Investments by companies such as Daikin and Shin-Etsu in advanced aqueous emulsions are further enhancing performance stability across multiple application cycles.

India Mold Release Coatings Market: Infrastructure Growth and Cost-Effective Solutions Driving Adoption

India is emerging as a high-growth market for mold release coatings, driven by expanding infrastructure projects and increased domestic manufacturing under the “Make in India” initiative. The National Infrastructure Pipeline is boosting demand for reactive release coatings used in precast concrete segments for railways and bridges.

The market is witnessing a transition from traditional waste-oil-based release agents to soap-film forming coatings, improving surface finish and durability of infrastructure components. Growth in the automotive and tire sectors is also driving demand for water-based mold release coatings, enhancing efficiency and reducing defects such as tire browning. Government incentives under the PLI scheme are supporting the white goods sector, increasing demand for high-gloss mold release coatings. Additionally, the development of low-cost aqueous concentrates tailored for MSMEs is expanding market accessibility and adoption across small-scale industries.

South Korea Mold Release Coatings Market: Energy Storage and Electronics Innovation Driving Advanced Coatings

South Korea is emerging as a key hub for high-performance mold release coatings, leveraging its dominance in EV battery manufacturing, electronics, and advanced materials engineering. The development of high-dielectric mold release coatings is enabling their application in EV battery separator production, ensuring no conductive residue transfer during high-speed processes.

Innovations such as ultra-thin film (UTF) release coatings, with thicknesses below 0.5 microns, are supporting the production of flexible OLED displays and foldable devices, highlighting South Korea’s leadership in advanced electronics manufacturing. Government initiatives such as the K-Battery Strategy are promoting the development of solvent-free and solid-film release coatings, enhancing sustainability and performance. Expansion of R&D facilities, including KCC Corporation’s Surface Engineering Excellence Center, is driving innovation in high-slip silicone hybrid coatings. Additionally, the adoption of bio-renewable release agents in food-grade packaging applications is aligning with evolving safety standards and sustainability goals.

Mold Release Coatings Market Report Scope

Mold Release Coatings Market

Parameter

Details

Market Size (2025)

$5 Billion

Market Size (2032)

$7.7 Billion

Market Growth Rate

6.3%

Segments

By Product (Water-borne Coatings, Solvent-borne Coatings, Solvent-free, Other Emerging Technologies), By Type (Semi-Permanent, Sacrificial, Internal Release Agents), By Chemistry (Silicone-based, Non-Silicone, Wax and Stearate-based, Natural, Metallic and Mineral), By Substrate Material (Steel and Metallic Molds, Plastic and Polymer Molds, Rubber and Elastomer Molds, Composite Molds, Stone, Concrete and Asphalt Forms), By Application Method (Spray-on, Wipe-on, Brush-on, Dip Coating), By End-Use Industry (Automotive and Transportation, Building and Construction, Aerospace and Defense, Plastics and Rubber Processing, Electronics and Semiconductors, Healthcare and Medical, Food Processing), By Functional Property (High-Temperature Stability, Chemical Resistance, Low Surface Tension, Anti-Corrosion, Rapid-Drying), By Sales Channel (Direct Sales, Specialty Industrial Chemical Distributors, Retail)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Mold Release Coatings Market Segmentation

By Product

Water-borne Coatings

Solvent-borne Coatings

Solvent-free

Other Emerging Technologies

By Type

Semi-Permanent

Sacrificial

Internal Release Agents

By Chemistry

Silicone-based

Non-Silicone

Wax and Stearate-based

Natural

Metallic and Mineral

By Substrate Material

Steel and Metallic Molds

Plastic and Polymer Molds

Rubber and Elastomer Molds

Composite Molds

Stone, Concrete and Asphalt Forms

By Application Method

Spray-on

Wipe-on

Brush-on

Dip Coating

By End-Use Industry

Automotive and Transportation

Building and Construction

Aerospace and Defense

Plastics and Rubber Processing

Electronics and Semiconductors

Healthcare and Medical

Food Processing

By Functional Property

High-Temperature Stability

Chemical Resistance

Low Surface Tension

Anti-Corrosion

Rapid-Drying

By Sales Channel

Direct Sales

Specialty Industrial Chemical Distributors

Retail

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Mold Release Coatings Industry

Henkel AG & Co. KGaA

Chem-Trend L.P.

Dow Inc.

Daikin Industries, Ltd.

Wacker Chemie AG

Shin-Etsu Chemical Co., Ltd.

Evonik Industries AG

LANXESS AG

Michelman, Inc.

Marbocote Ltd.

Miller-Stephenson, Inc.

McGee Industries, Inc.

Parker-Hannifin Corporation

TAG Chemicals GmbH

Chukyo Yushi Co., Ltd.

*- List not Exhaustive

Table of Contents: Mold Release Coatings Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Mold Release Coatings Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Mold Release Coatings Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers

2.4. Market Restraints and Challenges

2.5. Market Opportunities

2.6. Regulatory and Sustainability Landscape

2.7. Value Chain Analysis

2.8. Pricing Analysis

2.9. Technology Roadmap and Future Outlook

3. Innovations Reshaping the Mold Release Coatings Market

3.1. Trend: Water-Based Semi-Permanent Mold Release Coatings Reshaping Aerospace Composite Manufacturing

3.2. Trend: Fluoropolymer-Based Mold Release Coatings Enhancing Throughput in Wind Turbine Blade Manufacturing

3.3. Opportunity: EPA NESHAP Amendments Driving Adoption of Low-HAP and Low-VOC Mold Release Technologies

3.4. Opportunity: China’s Blue-Sky Action Plan Driving Mandatory Transition to Ultra-Low VOC Mold Release Systems

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Product Innovation

4.3. Sustainability and ESG Strategies

4.4. Capacity Expansion and Geographic Expansion

5. Market Share and Segmentation Insights: Mold Release Coatings Market

5.1. By Product

5.1.1. Water-borne Coatings

5.1.2. Solvent-borne Coatings

5.1.3. Solvent-free

5.1.4. Other Emerging Technologies

5.2. By Type

5.2.1. Semi-Permanent

5.2.2. Sacrificial

5.2.3. Internal Release Agents

5.3. By Chemistry

5.3.1. Silicone-based

5.3.2. Non-Silicone

5.3.3. Wax and Stearate-based

5.3.4. Natural

5.3.5. Metallic and Mineral

5.4. By Substrate Material

5.4.1. Steel and Metallic Molds

5.4.2. Plastic and Polymer Molds

5.4.3. Rubber and Elastomer Molds

5.4.4. Composite Molds

5.4.5. Stone, Concrete and Asphalt Forms

5.5. By Application Method

5.5.1. Spray-on

5.5.2. Wipe-on

5.5.3. Brush-on

5.5.4. Dip Coating

5.6. By End-Use Industry

5.6.1. Automotive and Transportation

5.6.2. Building and Construction

5.6.3. Aerospace and Defense

5.6.4. Plastics and Rubber Processing

5.6.5. Electronics and Semiconductors

5.6.6. Healthcare and Medical

5.6.7. Food Processing

5.7. By Functional Property

5.7.1. High-Temperature Stability

5.7.2. Chemical Resistance

5.7.3. Low Surface Tension

5.7.4. Anti-Corrosion

5.7.5. Rapid-Drying

5.8. By Sales Channel

5.8.1. Direct Sales

5.8.2. Specialty Industrial Chemical Distributors

5.8.3. Retail

6. Country Analysis and Outlook of Mold Release Coatings Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Saudi Arabia

6.19. UAE

6.20. Middle East and Africa

7. Mold Release Coatings Market Size Outlook by Region (2025–2034)

7.1. North America Mold Release Coatings Market Size Outlook to 2034

7.1.1. By Product

7.1.2. By Type

7.1.3. By Chemistry

7.1.4. By Substrate Material

7.1.5. By Application Method

7.1.6. By End-Use Industry

7.1.7. By Functional Property

7.1.8. By Sales Channel

7.2. Europe Mold Release Coatings Market Size Outlook to 2034

7.2.1. By Product

7.2.2. By Type

7.2.3. By Chemistry

7.2.4. By Substrate Material

7.2.5. By Application Method

7.2.6. By End-Use Industry

7.2.7. By Functional Property

7.2.8. By Sales Channel

7.3. Asia Pacific Mold Release Coatings Market Size Outlook to 2034

7.3.1. By Product

7.3.2. By Type

7.3.3. By Chemistry

7.3.4. By Substrate Material

7.3.5. By Application Method

7.3.6. By End-Use Industry

7.3.7. By Functional Property

7.3.8. By Sales Channel

7.4. South and Central America Mold Release Coatings Market Size Outlook to 2034

7.4.1. By Product

7.4.2. By Type

7.4.3. By Chemistry

7.4.4. By Substrate Material

7.4.5. By Application Method

7.4.6. By End-Use Industry

7.4.7. By Functional Property

7.4.8. By Sales Channel

7.5. Middle East and Africa Mold Release Coatings Market Size Outlook to 2034

7.5.1. By Product

7.5.2. By Type

7.5.3. By Chemistry

7.5.4. By Substrate Material

7.5.5. By Application Method

7.5.6. By End-Use Industry

7.5.7. By Functional Property

7.5.8. By Sales Channel

8. Company Profiles: Leading Players in the Mold Release Coatings Market

8.1. Henkel AG and Co. KGaA

8.2. Chem-Trend L.P.

8.3. Dow Inc.

8.4. Daikin Industries, Ltd.

8.5. Wacker Chemie AG

8.6. Shin-Etsu Chemical Co., Ltd.

8.7. Evonik Industries AG

8.8. LANXESS AG

8.9. Michelman, Inc.

8.10. Marbocote Ltd.

8.11. Miller-Stephenson, Inc.

8.12. McGee Industries, Inc.

8.13. Parker-Hannifin Corporation

8.14. TAG Chemicals GmbH

8.15. Chukyo Yushi Co., Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Mold Release Coatings Market Segmentation

By Product

Water-borne Coatings

Solvent-borne Coatings

Solvent-free

Other Emerging Technologies

By Type

Semi-Permanent

Sacrificial

Internal Release Agents

By Chemistry

Silicone-based

Non-Silicone

Wax and Stearate-based

Natural

Metallic and Mineral

By Substrate Material

Steel and Metallic Molds

Plastic and Polymer Molds

Rubber and Elastomer Molds

Composite Molds

Stone, Concrete and Asphalt Forms

By Application Method

Spray-on

Wipe-on

Brush-on

Dip Coating

By End-Use Industry

Automotive and Transportation

Building and Construction

Aerospace and Defense

Plastics and Rubber Processing

Electronics and Semiconductors

Healthcare and Medical

Food Processing

By Functional Property

High-Temperature Stability

Chemical Resistance

Low Surface Tension

Anti-Corrosion

Rapid-Drying

By Sales Channel

Direct Sales

Specialty Industrial Chemical Distributors

Retail

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global mold release coatings market was valued at $5 billion in 2025 and is projected to reach $7.7 billion by 2032, expanding at a CAGR of 6.3%. Market growth is being driven by increasing demand for semi-permanent mold release coatings, water-based release systems, silicone-based technologies, and PFAS-free mold release solutions across automotive, aerospace, composites, rubber, plastics, food packaging, and wind energy manufacturing industries.

Water-based semi-permanent mold release coatings are replacing solvent-borne sacrificial systems because they reduce VOC emissions by 80% to 95% while enabling multiple release cycles per application. These coatings improve resin flow control, eliminate contamination transfer, and reduce post-demolding cleaning requirements in approximately 92% of aerospace composite parts. Their ability to lower tool preparation time by nearly 40% is making them critical for high-throughput aerospace composite production environments.

Regulatory pressure from EPA NESHAP amendments, REACH compliance, and China’s Blue Sky Action Plan is accelerating the transition away from PFAS-containing and high-VOC mold release agents. Manufacturers are increasingly adopting PFAS-free, silicone-free, waterborne, and bio-based release systems that reduce hazardous emissions while maintaining thermal stability, lubricity, and release efficiency. These environmentally compliant technologies are becoming standard across automotive die casting, tire manufacturing, composites, and food-grade molding applications.

Asia-Pacific dominates the market due to large-scale manufacturing activity in China, India, Japan, and South Korea, while Europe leads in sustainability-focused innovation and low-emission coating technologies. Strong growth opportunities are emerging in EV lightweight composites, wind turbine blade manufacturing, aerospace structures, semiconductor packaging, medical device molding, tire production, and high-pressure die casting applications requiring precision release performance and defect-free surfaces.

Major companies operating in the mold release coatings industry include Henkel AG & Co. KGaA, Chem-Trend L.P., Dow Inc., Daikin Industries, Ltd., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Evonik Industries AG, and Michelman, Inc.. These companies are investing heavily in PFAS-free chemistries, semi-permanent release technologies, waterborne formulations, fluoropolymer alternatives, composite manufacturing solutions, and precision mold release systems to strengthen their global market positions.