Paints and Coatings Additives Market Size, PFAS-Free Transition, and Functional Performance Enhancement

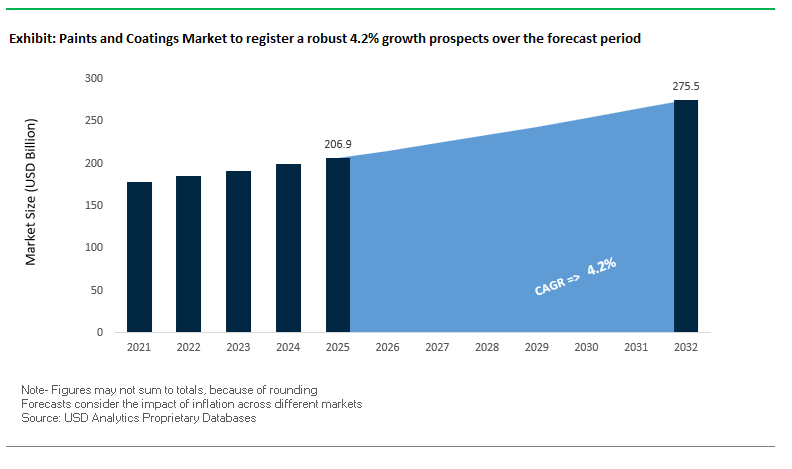

The global Paints and Coatings Additives Market was valued at $14.4 billion in 2025 and is projected to expand at a CAGR of 4.2% through 2032, reaching $19.2 billion by 2032. This growth reflects the indispensable role of additives in modifying rheology, improving dispersion, controlling surface properties, and enhancing durability across architectural, industrial, automotive, and specialty coatings.

A primary structural driver is the rapid transition toward low-VOC, waterborne, and energy-curable coating systems, which require highly engineered additive packages to maintain performance parity with solvent-based formulations. Additives such as defoamers, wetting agents, dispersants, rheology modifiers, and surface modifiers are increasingly designed to deliver multi-functional benefits, including improved flow, leveling, anti-settling, scratch resistance, and long-term stability.

The market is also undergoing a decisive shift toward PFAS-free and environmentally compliant chemistries, driven by regulatory restrictions and corporate sustainability mandates. Fluorinated additives, historically used for slip, leveling, and anti-blocking properties, are being replaced by silicone-based, wax-based, and bio-derived alternatives. This transition is not only regulatory-driven but also a competitive differentiator, as formulators seek future-proof additive solutions aligned with global environmental standards.

In parallel, increasing complexity in coatings—particularly high-solid systems, effect coatings, and advanced pigment technologies—is elevating the importance of precision dispersion and orientation control additives. Additionally, regional manufacturing expansion, particularly in Asia-Pacific, is improving supply chain resilience and enabling localized innovation tailored to evolving regulatory and performance requirements.

Market Analysis: Distribution Optimization, PFAS Elimination Strategies, and Capacity Expansion Driving Market Evolution

Recent developments in the Paints and Coatings Additives Market highlight a strong focus on supply chain optimization, sustainability transformation, and advanced additive innovation. In February 2026, Evonik implemented a major overhaul of its North American distribution network, appointing specialized regional partners to enhance technical service delivery and supply reliability for its portfolio of dispersants, defoamers, and rheology modifiers. This move reflects a broader industry emphasis on customer proximity and application-specific support.

Technological innovation is also shaping next-generation additive performance. Lubrizol’s February 2026 introduction of LED chlorination technology enhances CPVC resin production efficiency, indirectly influencing the development of high-heat and chemically resistant additive systems for industrial coatings. Concurrently, Lubrizol’s APAC-focused “local-for-local” strategy (November 2025) and expansion of Solsperse™ Hyperdispersants production capacity underscore the importance of regional manufacturing and reduced lead times for waterborne and high-solid formulations.

Sustainability-driven portfolio transformation remains a defining trend. Clariant confirmed that its entire additives portfolio is PFAS-free as of 2025, introducing products such as Ceridust 8170 M, a PTFE-free texturing agent for powder coatings. Similarly, BYK is progressing toward the complete phase-out of PFAS-containing additives by the end of 2025, replacing them with silicone-based and bio-based alternatives. These initiatives signal a structural shift toward fluorine-free additive technologies across the coatings value chain.

Strategic portfolio realignment is also evident. Elementis completed the divestment of its talc business, transitioning into a pure-play specialty additives company with a focus on high-margin rheological modifiers. Its expanded NiSAT production in China, including RHEOLATE® HX and CVS series, supports growing demand for VOC- and APEO-free additives aligned with stringent environmental standards.

Finally, evolving aesthetic and functional requirements are influencing additive R&D. BASF’s 2025–2026 “Driving the Proxy” trends emphasize multi-dimensional and liquid-metal surface effects, requiring advanced pigment stabilization and orientation control additives to maintain visual consistency across complex geometries.

Market Trend: Cellulose Nanofiber Rheology Modifiers Enhancing Sag Resistance and Sustainable Architectural Paint Performance

The paints and coatings additives industry are witnessing a material shift toward cellulose nanofiber rheology modifiers in architectural coatings, as formulators seek to replace synthetic thickeners with high-performance bio-based alternatives. CNF additives introduce a fibrillar network structure with a high aspect ratio, delivering superior shear-thinning behavior that is critical for professional-grade application performance, particularly in non-drip and anti-sag coatings.

Formulations incorporating CNF at low loading levels of 0.1% to 0.5% by weight achieve sag resistance in the range of 250 to 300 microns wet film thickness, significantly outperforming traditional hydroxyethyl cellulose systems at comparable concentrations. This enhanced sag resistance allows for thicker, more uniform coating application without runoff, improving coverage efficiency and finish quality in architectural paints.

Application precision is also improved with CNF-based systems. The fibrillar structure reduces roller spatter by approximately 30% compared to conventional associative thickeners, minimizing material loss and improving workplace cleanliness during application. This performance advantage is particularly relevant in professional painting environments where consistency and efficiency are critical.

From a sustainability perspective, cellulose nanofibers are derived from renewable biomass sources and are fully bio-based, offering a clear advantage over petroleum-derived HEUR and HASE thickeners. Despite this shift, CNF additives maintain stable viscosity profiles measured in Krebs Units, ensuring compatibility with existing formulation standards. This combination of performance enhancement and environmental benefit is positioning CNF rheology modifiers as a next-generation solution in architectural coatings.

Market Trend: High Bio-Carbon Wetting and Dispersing Additives Driving Low-Carbon Industrial Coatings Formulations

Industrial coatings are increasingly incorporating bio-based wetting and dispersing additives as manufacturers prioritize lifecycle carbon reduction without compromising pigment dispersion efficiency. These next-generation additives are derived from renewable feedstocks, including agricultural residues and forestry by-products, and are achieving biogenic carbon content levels between 60% and 95% as verified by ASTM D6866 methodologies.

Bio-based dispersants are delivering performance parity with traditional petroleum-derived additives. Polyurethane-modified bio-dispersants are capable of reducing mill-base viscosity by up to 40% when processing difficult pigments such as carbon black, enabling higher pigment loading and improved dispersion stability. This viscosity reduction facilitates smoother processing and enhances coating performance in terms of color development and consistency.

Energy efficiency gains are another key advantage. By improving pigment wetting and dispersion kinetics, these additives reduce grind phase processing time by approximately 15%, lowering the overall energy consumption of paint manufacturing operations. This contributes to both cost savings and reduced carbon footprint in industrial production environments.

The integration of high bio-carbon additives is also supporting sustainability certifications and carbon disclosure requirements across global supply chains. As industrial OEMs and coating manufacturers align with carbon neutrality targets, bio-based wetting and dispersing additives are becoming a critical component of environmentally optimized coating formulations.

Market Opportunity: EPA TSCA and Safer Choice Standards Driving Demand for Low-Dioxane and Non-Ethoxylated Additive Technologies

Regulatory developments in the United States are creating significant opportunities for advanced coating additives, particularly following the EPA’s updated risk assessment for 1,4-dioxane under the Toxic Substances Control Act. Identified as a substance posing unreasonable risk, 1,4-dioxane is commonly present as a byproduct in ethoxylated surfactants, which are widely used in waterborne coating formulations.

The revised Safer Choice Standard effectively mandates that certified additives contain less than 1 part per million of 1,4-dioxane, creating immediate demand for reformulated products. This requirement is driving the adoption of dioxane-stripped ethoxylates as well as alternative non-ethoxylated surfactant technologies that eliminate the risk at the source. As a result, a large portion of legacy wetting agents, estimated at around 70% of the current market, is undergoing reformulation to meet compliance thresholds.

This regulatory pressure is accelerating innovation in green surfactant chemistry, including the development of sugar-based, amino acid-based, and other bio-derived wetting agents. Suppliers capable of delivering compliant, high-performance additives with verified low-contaminant profiles are gaining competitive advantage as manufacturers seek to align with regulatory standards while maintaining product performance.

Market Opportunity: China GB/T 35609-2026 Certification Driving Adoption of Bio-Based Additives in Green Coatings

China’s implementation of GB/T 35609-2026 is creating a structured demand environment for bio-based coating additives, particularly in products targeting the China Green Product certification. This standard introduces mandatory requirements for bio-based carbon content within coatings, extending sustainability criteria to additive-level formulation components.

To achieve Tier 1 environmental certification, coating systems must demonstrate a minimum of 20% bio-based carbon content, requiring additive suppliers to provide verifiable documentation of renewable material content. This requirement is driving the integration of bio-based additives across architectural, automotive, and industrial coating formulations, as manufacturers seek to qualify for government-backed sustainability programs and procurement opportunities.

The certification framework is also acting as a market forcing function, accelerating the localization of advanced bio-based additive production within China. Domestic OEMs, particularly in automotive and electronics sectors, are increasingly mandating compliance with GB/T 35609-2026 for their coating suppliers to meet national carbon neutrality targets.

This regulatory-driven demand is creating significant growth opportunities for additive manufacturers capable of delivering high-performance, bio-based solutions with validated carbon content. As sustainability standards become embedded in procurement and manufacturing practices, bio-based coating additives are expected to play a central role in the evolution of the Chinese coatings market.

Paints and Coating Additives Market Share and Segmentation Insights

Rheology Modifiers Capture 22.8% Share as Essential Performance Additives Across Coating Systems

The paints and coatings additives market by product type is led by rheology modifiers, accounting for 22.8% of global market share in 2025, driven by their critical role in waterborne and low-VOC coating formulations. As the industry rapidly transitions toward environmentally compliant paints, rheology modifiers such as HEUR, HASE, and cellulose ethers are indispensable for controlling viscosity, sag resistance, leveling, and spatter, functions traditionally managed by solvent-based systems. Their versatility ensures widespread use across architectural paints, industrial coatings, automotive finishes, and marine coatings, making them one of the most universally consumed additive categories. With increasing demand for high-performance, eco-friendly coatings, rheology modifiers remain central to achieving optimal application properties, film build, and surface finish, reinforcing their dominance in the global coatings additives market.

Direct Sales Hold 52.8% Share Driven by Custom Formulation Support and Quality Assurance

In the paints and coatings additives market by sales channel, direct sales dominate with a 52.8% market share in 2025, reflecting the importance of technical collaboration and formulation precision. Leading additive manufacturers such as BYK, Evonik, BASF, and Dow work closely with coating producers to develop custom additive packages, optimizing properties like dispersion, defoaming, adhesion, and curing performance for specific resin systems. This direct engagement enables faster troubleshooting, product customization, and innovation in high-performance coatings. Additionally, quality consistency, batch traceability, and regulatory compliance—especially for sensitive additives like biocides, UV stabilizers, and curing catalysts—require controlled supply chains that only direct relationships can ապահով. As coating formulations become more complex and performance-driven, direct sales continue to dominate the global coatings additives distribution landscape.

Competitive Landscape of the Paints and Coatings Additives Market

Evonik Leads Specialty Additives Market with Siloxane Innovation and Sustainable Solutions

Evonik Industries AG continues to dominate the paints and coatings additives market, particularly in siloxane-based defoamers and foam-control technologies. In May 2026, the company streamlined its North American distribution network by partnering with regional specialists to enhance technical support for its Custom Solutions portfolio. Its TEGO® Foamex 8420 defoamer addresses micro-foam stabilization challenges in waterborne overprint varnishes and high-pigment coatings, improving production efficiency. Evonik’s Custom Solutions segment generated €5.4 billion in revenue, reflecting strong demand for specialty coating additives. Additionally, its ACEMATT® bio-based silica matting agents reduce product carbon footprint by up to 20%, reinforcing its leadership in sustainable additives.

BYK Advances Digital Paint Additives Innovation with PFAS-Free and High-Performance Solutions

BYK-Chemie GmbH is a global leader in paint additives, particularly in rheology control and nanotechnology-based surface protection. In 2026, the company implemented significant price increases to sustain high R&D investment amid rising raw material costs. Its AQUACER 492 additive, inspired by lotus-leaf technology, delivers superior slip and rub resistance without fluorinated chemicals, supporting PFAS-free coating solutions. BYK’s BYK-Advance platform uses AI-driven modeling to optimize additive-resin compatibility, reducing development time by 35%. The company’s DISPERBYK series remains the industry benchmark for stabilizing nanoparticles and carbon nanotubes, strengthening its position in high-performance and conductive coatings applications.

BASF Expands Sustainable Additives Portfolio with Circular Economy and Regional Growth Strategies

BASF SE is a key player in the global coatings additives market, leveraging backward integration and sustainable innovation. In 2026, the company expanded its dispersions production capacity in India to support rising demand for Acronal® and Basonal® additive technologies in South Asia. BASF also increased production of HALS and NOR® HALS additives, which are essential for UV protection in high-performance coatings and plastics. Its transition toward bio-attributed acrylates through the ChemCycling process supports circular economy initiatives by converting plastic waste into high-value additives. BASF’s strong presence in paper and packaging additives further reinforces its leadership in sustainable coatings solutions.

Dow Leads Rheology Modifiers Market with Smart Flow Technologies and Waterborne Solutions

Dow Inc. is a leading innovator in the rheology modifiers and surfactant additives market, focusing on advanced flow control technologies. In 2026, the company introduced a new generation of HEUR rheology modifiers designed to enhance spatter resistance and leveling in ultra-low VOC paints. Dow holds a leading share in the rheology modifiers segment, which accounts for 25% of the global additives market, driven by the growing adoption of water-based coatings. Its strategic focus on formulation-on-demand services supports large-scale paint manufacturers in optimizing supply chains. Dow’s expertise in non-ionic surfactant stabilization ensures long-term performance and stability in high-solids coating systems.

Clariant Focuses on Safety and Bio-Based Additives for High-Performance Coating Applications

Clariant AG is a prominent player in the specialty coatings additives market, emphasizing safety, sustainability, and multifunctionality. In 2026, the company achieved EU approval for its renewable rice bran wax additives, supporting the growing demand for food-contact safe and clean-label coatings. Its Tonnegel™ 50 rheology modifier provides stable viscosity across varying conditions, enhancing performance in industrial coatings. Clariant is also advancing PFAS-free processing aids to replace traditional fluoropolymer additives, aligning with stringent environmental regulations. Its Exolit™ flame retardants are widely used in EV battery enclosures and data centers, reinforcing its leadership in safety-critical additive solutions.

China Paints and Coatings Additives Market: Maritime Dominance and Specialty Chemical Scale-Up

China has emerged as the global hub for advanced functional coating additives, transitioning from volume production to high-performance specialty additives. Strategic investments such as Evonik’s expansion of specialty amine curing agents in Nanjing are strengthening capabilities in polyurethane and epoxy systems. BASF’s upcoming CFRP dispersant production line further supports high-end automotive OEM coatings.

China’s dominance in shipbuilding is driving strong demand for biocide-free anti-fouling additives and anti-corrosive agents, aligned with GB 4806.10-2025 standards. The commissioning of Wacker Chemie’s silicone complex in Zhangjiagang is expanding production of high-performance emulsions for industrial and architectural coatings. Additionally, tightening VOC regulations are accelerating the shift toward waterborne rheology modifiers and HEUR thickeners, reinforcing sustainability. With exports rising 27.7% year-on-year, China continues to lead both in scale and global competitiveness.

United States Paints and Coatings Additives Market: PFAS-Free Transition and Energy-Curable Innovation

The United States is a global leader in regulatory-driven innovation, particularly in PFAS-free additive development and energy-efficient coating systems. With EPA reporting requirements coming into force in 2026, manufacturers are scaling silicone-based and bio-wax dispersions to replace fluorochemicals while maintaining performance.

The Infrastructure Investment and Jobs Act (IIJA) is driving demand for anti-block additives and high-solid rheology modifiers in protective coatings for bridges and highways. Technological advancements include PPG’s DURANEXT portfolio, which uses photo-initiator additives for near-instant curing in coil coatings. Growth in pharmaceutical logistics is boosting demand for anti-fog and antimicrobial additives, while AI-driven reflective additives are enhancing building energy efficiency. Strategic consolidation, such as Henkel’s $2.5 billion acquisition of Stahl Holdings, is further strengthening high-value additive capabilities in the U.S.

Germany Paints and Coatings Additives Market: Circular Economy and Bio-Based Additive Leadership

Germany leads Europe’s additives market through its focus on circular economy integration, bio-based chemistry, and VOC-free formulations. Innovations in digital tracer additives are enabling automated recycling systems to identify materials with up to 99% accuracy, significantly improving waste management efficiency.

Investments such as BASF’s €200 million waterborne production expansion in Münster highlight the transition toward aqueous dispersing agents. Germany is also advancing PACVD-compatible additives for hydrogen infrastructure, particularly for coating fuel cell components. The development of 50% bio-based UV oligomers derived from sorbitol underscores the country’s shift toward renewable materials. Regulatory drivers like the VerpackG amendments are promoting water-soluble additives that simplify recycling, reinforcing Germany’s leadership in sustainable coatings.

India Paints and Coatings Additives Market: Decorative Growth and Infrastructure-Led Demand

India is one of the fastest-growing markets for coating additives, driven by rapid urbanization and large-scale housing initiatives such as PMAY-U 2.0. Major consolidation, including JSW Paints’ acquisition of Akzo Nobel India, is centralizing procurement and strengthening domestic supply chains.

The market is witnessing strong innovation in solar-reflective additives, such as Berger Paints’ Weathercoat Anti Dustt Kool range, which reduces indoor temperatures by up to 5°C. Products like Asian Paints’ Apcolite All Proteck are introducing nanotechnology-based additives for self-cleaning and flame-retardant properties. Government incentives under the PLI scheme are boosting domestic production of defoamers and wetting agents. Additionally, the shift toward waterborne additives is accelerating, with projections indicating a 52% market share by 2026, reflecting growing environmental awareness.

Japan Paints and Coatings Additives Market: Smart Functional Additives and Precision Applications

Japan continues to lead in advanced functional additives, particularly in photocatalytic, self-healing, and smart packaging technologies. Innovations such as ARITERAS KPC, a photocatalytic coating, enable the decomposition of organic pollutants, enhancing environmental performance.

The country is also pioneering reflective additives for EV thermal management, improving energy efficiency by reducing cabin heat load. Advances in oxygen-scavenging additives are transforming food packaging by integrating barrier properties directly into coatings. Japan’s strict regulatory frameworks are driving the development of ultra-low migration additives for medical and food-contact applications. Additionally, innovations in UV-LED curing additives are reducing energy consumption in high-speed industrial processes, reinforcing Japan’s leadership in precision coating technologies.

Brazil Paints and Coatings Additives Market: Bio-Based Innovation and Industrial Coatings Growth

Brazil is leveraging its agricultural strength to become a leader in bio-based coating additives, particularly those derived from sugarcane and carnauba wax. The use of carnauba wax dispersions is improving hardness and gloss in coatings while reducing reliance on imported paraffin waxes.

The country’s paint industry reached a record 1.98 billion liters in 2024/2025, driven by infrastructure investments and industrial expansion. Brazil is also a global leader in barrier coating additives for agrochemical packaging, designed to prevent chemical leaching in tropical climates. Growth in the automotive sector is increasing demand for adhesion promoters and cross-linking agents, particularly in São Paulo. Additionally, R&D in UV absorbers and HALS technologies is addressing the challenges of high solar radiation, ensuring durability in outdoor applications.

South Korea Paints and Coatings Additives Market: Semiconductor-Driven Innovation and High-Tech Applications

South Korea’s additives market is shaped by its leadership in electronics, semiconductors, and advanced display technologies. The country is a global leader in anti-static (ESD) and conductive additives, essential for cleanroom environments and electronic packaging.

Technological advancements include PACVD-compatible additives that cure at low voltages (<160V), enabling applications on flexible electronic substrates. South Korea is also pioneering biotechnological marine additives, such as Selektope, for environmentally friendly anti-fouling solutions. The market is benefiting from innovations in high-barrier retort coatings, supporting global food packaging needs. Additionally, demand for premium sensory-effect additives, driven by the K-Beauty industry, is enhancing aesthetic and functional performance in cosmetic packaging. The scaling of thin-film encapsulation (TFE) additives further reinforces South Korea’s position in advanced OLED technologies.

Paints and Coatings Additives Market Report Scope

Paints and Coatings Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$14.4 Billion

|

|

Market Size (2032)

|

$19.2 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Product (Rheology Modifiers, Wetting and Dispersing Agents, Anti-Foaming Agents, Biocides and Preservatives, Surface Modifiers, Leveling and Flow Agents, Adhesion Promoters, UV Stabilizers and Antioxidants, Curing Catalysts and Accelerators, Others), By Product Chemistry (Acrylics, Silicones, Urethanes, Fluoropolymers, Waxes, Metallic Additives, Bio-based), By Formulation Technology (Water-borne, Solvent-borne, Powder-based, Radiation-Cured), By End-Use Application (Architectural, Automotive and Transportation, Industrial, Wood and Furniture, Packaging), By End-User Type (Industrial, Professional, Consumer), By Sales Channel (Direct Sales, Specialty Distributors, Online B2B Marketplaces)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BYK-Chemie GmbH, BASF SE, Evonik Industries AG, Dow Inc., Clariant AG, The Lubrizol Corporation, Arkema S.A., Elementis plc, Eastman Chemical Company, Ashland Inc., Nouryon, Solvay S.A., Croda International Plc, DIC Corporation, Kao Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paints and Coatings Additives Market Segmentation

By Product

- Rheology Modifiers

- Wetting and Dispersing Agents

- Anti-Foaming Agents

- Biocides and Preservatives

- Surface Modifiers

- Leveling and Flow Agents

- Adhesion Promoters

- UV Stabilizers and Antioxidants

- Curing Catalysts and Accelerators

- Others

By Product Chemistry

- Acrylics

- Silicones

- Urethanes

- Fluoropolymers

- Waxes

- Metallic Additives

- Bio-based

By Formulation Technology

- Water-borne

- Solvent-borne

- Powder-based

- Radiation-Cured

By End-Use Application

- Architectural

- Automotive and Transportation

- Industrial

- Wood and Furniture

- Packaging

By End-User Type

- Industrial

- Professional

- Consumer

By Sales Channel

- Direct Sales

- Specialty Distributors

- Online B2B Marketplaces

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Paints and Coatings Additives Industry

- BYK-Chemie GmbH

- BASF SE

- Evonik Industries AG

- Dow Inc.

- Clariant AG

- The Lubrizol Corporation

- Arkema S.A.

- Elementis plc

- Eastman Chemical Company

- Ashland Inc.

- Nouryon

- Solvay S.A.

- Croda International Plc

- DIC Corporation

- Kao Corporation

*- List not Exhaustive