Low VOC Coating Additives Market Size, Waterborne Formulation Demand, and Sustainable Additives Outlook

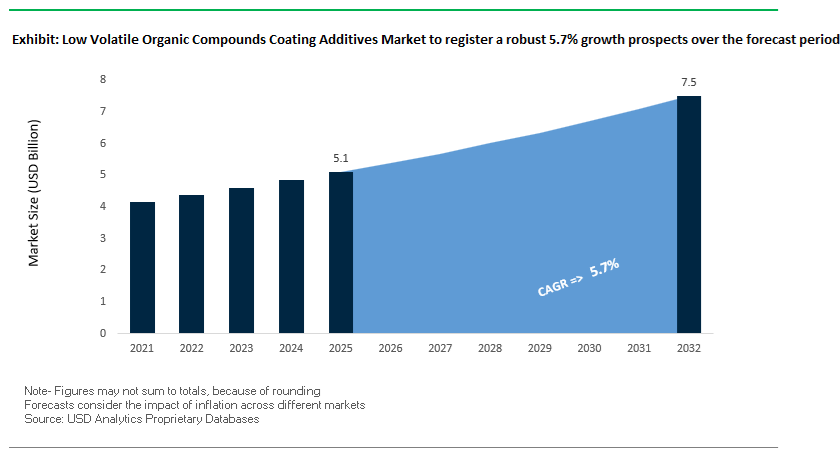

The global low volatile organic compounds (VOC) coating additives market was valued at $5.1 billion in 2025 and is projected to reach $7.5 billion by 2032, growing at a CAGR of 5.7%. This expansion is driven by increasing demand for low-VOC surfactants, dispersants, defoamers, rheology modifiers, and wetting agents used in waterborne coatings, powder coatings, radiation-curable systems, and high-performance industrial coatings. As regulatory frameworks tighten globally, particularly across North America, Europe, and Asia-Pacific, coating formulators are rapidly transitioning toward VOC-free and ultra-low VOC additive systems to meet compliance and sustainability goals.

A key growth driver is the accelerating shift from solvent-borne to waterborne and UV-curable coatings, where advanced additives are essential to maintain performance characteristics such as viscosity control, pigment dispersion, film formation, and durability. Low VOC additives play a critical role in overcoming formulation challenges such as reduced open time, foaming issues, and poor wetting behavior, which are common in eco-friendly coatings. Additionally, rising demand for high-performance coatings in automotive OEM, construction, electronics, and packaging industries is driving the need for customized additive solutions that combine sustainability with enhanced functionality.

The market is also benefiting from increasing adoption of PFAS-free chemistries, bio-based additives, and high-efficiency formulation technologies, aligning with global environmental and health standards. Growth in additive manufacturing, semiconductor coatings, and advanced industrial applications is further expanding demand for precision-engineered coating additives. Regionally, Europe leads in regulatory-driven innovation, while Asia-Pacific is witnessing strong growth due to expanding manufacturing capacity and increasing environmental compliance requirements.

The low VOC coating additives industry is undergoing a significant transformation driven by regulatory pressure, rapid innovation, and strategic restructuring across the value chain. A major development occurred in February 2026, when AkzoNobel and Axalta announced a mega-merger, which is expected to significantly influence global additive specifications. The combined entity’s scale and internal demand for low-VOC surfactants, dispersants, and rheology modifiers are likely to set new benchmarks for formulation standards across the coatings industry.

Operational optimization and supply chain efficiency are becoming critical competitive factors. In May 2026, Evonik streamlined its North American distribution network for coating additives, enhancing delivery speed for its TEGO® and SURFYNOL® low-VOC product lines to key industrial hubs. This move reflects the increasing importance of regional supply chain agility in meeting the growing demand for customized, high-performance additive solutions.

Product innovation continues to focus on improving formulation performance while maintaining ultra-low VOC profiles. In January 2026, Evonik introduced TEGO® Dispers 695, a hyperdispersant designed for radiation-curing and polyurethane ink systems, enabling higher pigment loading without compromising viscosity or environmental compliance. Similarly, Lubrizol’s July 2025 expansion of low-VOC humectants and corrosion inhibitors addresses a key challenge in waterborne coatings by extending open time and improving coating stability.

Sustainability-driven transitions are reshaping additive chemistry. BYK Additives achieved a major milestone in December 2025 by transitioning its entire portfolio to PFAS-free formulations, eliminating environmentally persistent fluorinated compounds. The company further advanced innovation with its High Throughput Screening (HTS) facility, capable of testing 220 additive samples in 24 hours, significantly accelerating the development of VOC-free wetting and dispersing agents. Additionally, its March 2025 launch of BYK-1693 SD, a VOC-free powder defoamer, highlights the shift toward environmentally compliant additives for construction and building materials.

Strategic partnerships and regional manufacturing expansions are also shaping the market. The November 2025 joint venture between Clariant and FUHUA focuses on producing halogen-free flame retardant additives in China, targeting LSHF (Low Smoke Halogen Free) applications in both polymers and coatings. Arkema’s August 2024 expansion of its N3xtDimension® platform further underscores the growing importance of low-VOC UV-curing additives in advanced sectors such as electronics and additive manufacturing.

Innovation is also extending into aesthetic and functional performance enhancements. BASF Coatings’ October 2025 “Driving the Proxy” collection integrates low-VOC additive packages with advanced pigment technologies, enabling multi-color and metallic effects for next-generation automotive OEM coatings without compromising sustainability.

Market Trend: Reactive Coalescent Technologies Enabling Zero-VOC Paint Formulations with Enhanced Film Performance

The low VOC coating additives market is undergoing a significant transformation with the increasing adoption of reactive coalescents, which are replacing traditional volatile coalescing agents such as ester alcohols. These next-generation additives are designed to chemically integrate into the polymer matrix during film formation, effectively eliminating their contribution to volatile organic compound emissions while simultaneously enhancing coating performance characteristics. This shift is critical as architectural paint manufacturers push toward Zero-VOC thresholds below 5 g/L without compromising application properties or durability.

Reactive coalescents are delivering measurable improvements in mechanical and surface performance. Formulations incorporating these additives demonstrate a 25% to 30% increase in final film hardness, significantly improving early block resistance, which has historically been a limitation in low VOC coatings. Additionally, these additives extend open time by up to 45%, allowing for improved workability and wet-edge blending in high-performance waterborne paints, particularly in trim and decorative applications.

From a durability perspective, the cross-linking mechanism of reactive coalescents enhances film integrity, resulting in scrub resistance gains of approximately 15% to 20% in high pigment volume concentration interior emulsions. This directly addresses performance trade-offs typically associated with VOC reduction strategies. Furthermore, reactive coalescents achieve up to a 90% reduction in semi-volatile organic compound emissions, enabling compliance with stringent low-odor requirements in sensitive environments such as healthcare facilities and hospitality spaces. These combined benefits position reactive coalescent technology as a cornerstone innovation in the evolution of zero-emission architectural coatings.

Market Trend: 100% Active Non-VOC Defoamers Optimizing Foam Control in Waterborne Coating Systems

The increasing dominance of waterborne coatings across industrial applications has intensified the need for advanced foam control technologies, driving the adoption of 100% active, non-VOC defoamers. Traditional defoaming systems often rely on solvent carriers or mineral oils, which contribute to VOC and SVOC emissions while introducing potential compatibility issues. In contrast, modern polyether siloxane-based defoamers are engineered to be fully active without volatile carriers, aligning with evolving regulatory and environmental requirements.

These high-performance defoamers exhibit significantly improved efficiency, delivering up to three times greater micro-foam suppression in high-shear processes such as airless spray applications. This enhanced performance ensures smoother film formation and reduces defects associated with entrapped air. In addition, these additives improve surface quality by reducing common coating defects such as craters and fish-eyes by approximately 40%, particularly in high-gloss industrial topcoat formulations where surface uniformity is critical.

Another key advantage lies in dosage optimization. Due to their high active concentration, these defoamers allow manufacturers to reduce additive loading levels by 0.1% to 0.3% by weight. This reduction not only lowers formulation costs but also minimizes risks related to intercoat adhesion failure in multi-layer coating systems. Importantly, their carrier-free composition contributes zero mass to SVOC calculations, making them highly suitable for coatings targeting eco-certifications such as Blue Angel and EU Ecolabel. As regulatory frameworks tighten around emissions and indoor air quality, 100% active non-VOC defoamers are becoming essential components in advanced waterborne coating formulations.

Market Opportunity: China GB 30981.1-2025 Standard Driving Demand for Ultra-Low VOC Additive Technologies

China’s implementation of the GB 30981.1-2025 standard represents a major inflection point for the low VOC coating additives market, establishing stringent limits on harmful substances in architectural coatings and accelerating the transition toward ultra-low VOC formulations. Effective from June 2026, this regulation introduces tighter controls not only on VOC content but also on semi-volatile organic compounds and accessory material emissions, significantly increasing the demand for compliant additive technologies.

The regulatory shift is expected to impact a substantial portion of the market, with approximately 75% of existing architectural coatings in China requiring reformulation to meet updated “Green Label” certification requirements. This creates a large-scale procurement opportunity for advanced additive solutions, including low-emission biocides, surfactants, and coalescents that do not release formaldehyde or alkylphenol ethoxylates. The emphasis on ultra-low VOC performance is driving innovation in additive chemistry, particularly in the development of high-purity, environmentally benign materials.

Transparency requirements within the new standard further amplify this opportunity. Mandatory disclosure of biocide composition, including limits on substances such as arsenic and methylisothiazolinone, is favoring established global suppliers with proven compliance capabilities and robust product documentation. This regulatory environment is accelerating consolidation around high-quality additive providers and reshaping competitive dynamics in the Chinese coatings supply chain. As manufacturers race to meet compliance deadlines, demand for certified low VOC additive packages is expected to surge, positioning China as a key growth driver for advanced coating additive technologies.

Market Opportunity: US GSA P100 Standards Expanding Market for Low VOC Additives in Federal and Commercial Construction

The updated P100 Facilities Standards issued by the U.S. General Services Administration are creating a significant opportunity for low VOC coating additives across federal and commercial construction markets. These standards mandate the use of low-emission materials in approximately 300,000 federal buildings, aligning with broader national objectives to achieve net-zero emissions by 2045 and improve indoor environmental quality for over one million federal employees.

The regulatory framework prioritizes coatings that incorporate certified low VOC additives, particularly those capable of supporting “Healthy Building” certifications and indoor air quality benchmarks. This is driving demand for additives that offer both performance and transparency, including products supported by Health Product Declarations and Environmental Product Declarations. As federal projects increasingly align with LEED v4.1 standards, additive suppliers with verifiable low-toxicity profiles are gaining a competitive advantage.

The scale of federal procurement is also acting as a market catalyst. The GSA’s adoption of low VOC standards is expected to influence private sector construction practices, particularly in commercial real estate and institutional infrastructure. Industry projections indicate a 20% increase in demand for high-performance, low VOC industrial maintenance coatings across the U.S. East Coast through 2026, driven by regulatory alignment and sustainability goals.

Low VOC Coating Additives Market Share and Segmentation Insights

Rheology Modifiers Capture 24% Share as Critical Enablers of Low-VOC Paint Performance

The low volatile organic compounds (VOC) coating additives market by type is led by rheology modifiers, accounting for 24% of the global market share in 2025, driven by their essential role in waterborne coating formulations. Additives such as HEUR (Hydrophobically Modified Ethoxylated Urethanes), HASE (Hydrophobically Modified Alkali Swellable Emulsions), and cellulose ethers are critical for controlling viscosity, sag resistance, leveling, and spatter performance in low-VOC paints. As the industry shifts away from solvent-based systems, these rheology modifiers replicate the application properties of traditional coatings without increasing VOC levels. Additionally, modern associative thickeners enable excellent film build, open time, and brushability while maintaining VOC limits below 50 g/L, aligning with global environmental regulations. This makes rheology modifiers indispensable for formulators developing high-performance, eco-friendly architectural and industrial coatings.

Direct Sales Hold 52% Share Driven by Custom Formulation and OEM-Level Support

In the low VOC coating additives market by sales channel, direct sales dominate with a 52% market share in 2025, reflecting the high level of technical collaboration required between additive suppliers and coating manufacturers. Leading companies such as BYK, Evonik, Dow, and BASF work closely with paint formulators to optimize rheology, dispersion stability, defoaming efficiency, and surface wetting properties for specific resin systems, including acrylics, polyurethanes, and alkyd emulsions. This direct engagement enables the development of custom additive blends and proprietary packages, tailored to achieve the desired balance between VOC compliance, gloss control, durability, and application performance. Furthermore, direct relationships ensure faster innovation cycles and better alignment with evolving regulatory standards, reinforcing this channel as the preferred route for delivering high-performance, low-VOC coating additive solutions.

Competitive Landscape in the Low VOC Coating Additives Market

BASF drives low-PCF additive innovation and digital formulation capabilities

BASF remains a dominant force in the low VOC coating additives market, leveraging its global chemical expertise to deliver low product carbon footprint (PCF) solutions and advanced dispersions. At the American Coatings Show 2026, the company introduced the PureOptions® platform, a next-generation colorant technology designed for low-VOC paints with enhanced scuff resistance. BASF expanded its production capacity in Mangalore, India, adding new lines for Acronal® and Basonal® dispersions to meet rising demand in South Asia. Its hydroxyl functional acrylate dispersion for waterborne 2K direct-to-metal systems enables combined primer and topcoat functionality in a single low-VOC layer. The company is also integrating AI-powered formulation tools to optimize additive-resin interactions and accelerate green coating development cycles.

Evonik strengthens cross-linker innovation for low-VOC high-performance coatings

Evonik Industries is a global leader in specialty amines and cross-linking agents, addressing performance challenges in low-VOC epoxy and polyurethane systems. In April 2026, the company expanded its specialty amine production facility in Nanjing, China, powered entirely by green electricity to support demand in the Asia-Pacific region. Evonik introduced a new generation of reactive amines that meet stringent 2026 emission standards while improving processing efficiency in automotive foams and protective coatings. Its expertise in isophorone chemistry, particularly through VESTANAT® and VESTAMIN® product lines, supports high-performance coatings in wind energy and aerospace sectors. The company also focuses on ultra-low-temperature catalysts that reduce curing energy requirements, enhancing sustainability and operational efficiency.

BYK-Chemie leads additive performance and digital measurement integration

BYK-Chemie, part of the ALTANA Group, is a leading specialist in wetting, dispersion, and surface additives for low-VOC coatings. The company maintains a strong R&D focus, reinvesting 8–10% of its revenue into innovation, while implementing strategic price adjustments in 2026 to offset rising input costs. Its DISPERBYK and BYK-DYNWET product lines are widely recognized as industry standards for stabilizing pigments in waterborne coatings without increasing VOC content or disrupting hydrophilic-lipophilic balance. BYK’s integration of its BYK-Gardner measurement division enables a comprehensive approach to coating appearance, combining instrumentation with additive chemistry. The company is also advancing solutions for coating recycled and bio-based substrates, addressing emerging challenges in sustainable material applications.

Dow delivers scalable rheology solutions for low-VOC coatings across industries

Dow Inc. leverages its global manufacturing scale and integrated supply chain to provide cost-effective additives for low-VOC coatings in architectural, packaging, and infrastructure applications. In Q1 2026, the company reported a 2% volume increase in its Performance Materials & Coatings segment, driven by strong demand for silicones and acrylic monomers. Dow’s ACRYSOL™ rheology modifiers are essential for achieving the viscosity, application feel, and spatter resistance required in low-VOC formulations, matching the performance of traditional solvent-based coatings. Through its “Transform to Outperform” strategy, Dow is streamlining supply chains and enhancing responsiveness to high-growth sectors such as mobility and consumer packaging, ensuring consistent supply and performance reliability.

Arkema advances bio-based and zero-VOC additive technologies for emerging applications

Arkema is at the forefront of bio-based additive innovation, focusing on renewable and zero-VOC technologies for advanced coating systems. At ACS 2026, the company introduced additives with up to 93% bio-based content, targeting wood coatings and furniture applications where indoor air quality is critical. Arkema is expanding its UV/EB radiation-curable additive portfolio, eliminating solvent evaporation and enabling true zero-VOC curing processes. Its solutions are also applied in EV battery insulation and sound-dampening coatings, supporting next-generation mobility platforms. The company’s ecodesign strategy extends to data center applications, providing additives for cool-roof coatings and high-performance sealants that improve thermal management and energy efficiency in server infrastructure.

Clariant focuses on sustainable dispersants and halogen-free additive technologies

Clariant International Ltd. is a key player in sustainable additive chemistry, emphasizing high-performance dispersants and environmentally compliant solutions. In March 2026, the company launched Dispersogen™ PSL 100, a polymeric dispersant capable of stabilizing high-load systems even in complex electrolyte environments. Its Tonnegel™ 50 rheology modifier enhances thixotropic stability in demanding applications such as industrial coatings and agricultural formulations. Clariant is also transitioning its Exolit® flame retardant portfolio to fully halogen-free systems, aligning with broader low-smoke halogen-free trends in electronics and transportation sectors. With strong expertise in non-hazardous and biocompatible additives, the company enables formulators to meet stringent GHS compliance requirements while maintaining high coating performance.

China Low VOC Coating Additives Market: Regulatory Leadership and Semiconductor-Driven Innovation

China has evolved into a global epicenter for low VOC coating additives, combining regulatory rigor with rapid industrial advancement. The introduction of GB 8624—2025 standards and subsequent amendments has significantly reshaped the coatings ecosystem, mandating the adoption of additives that balance low smoke toxicity, flame retardancy, and environmental compliance. The enforcement of the Ecological and Environmental Code (2026), with stringent penalties for non-compliance, is accelerating the shift toward high-performance, low-emission additive formulations.

Technological advancements include the scaling of solvent-free wetting agents, dispersants, and rheology modifiers tailored for high-precision sectors such as semiconductor lithography equipment. The expansion of waterborne coating additive production lines, including BASF’s facility in Nanjing, reflects strong infrastructure investment to meet rising demand. China’s dominance in lithium-ion battery manufacturing is further driving the adoption of low VOC friction-reducing additives, improving production efficiency and coating quality. Additionally, domestic innovation in bio-based ethyl acrylate technologies is supporting the transition toward sustainable, low-carbon additive solutions.

United States Low VOC Coating Additives Market: PFAS-Free Innovation and Bio-Based Chemistry Leadership

The United States is leading the low VOC coating additives market through stringent environmental regulations and strong innovation in bio-based and PFAS-free formulations. The anticipated restrictions under the EPA’s PFAS regulations are driving manufacturers toward silicone-based and bio-polymer surfactants, significantly transforming additive chemistry across industries.

Product innovation is evident in advanced solutions such as siloxane defoamers (e.g., TEGO® Foamex 8051), designed to stabilize waterborne coatings while preventing surface defects. Government funding through the Inflation Reduction Act (IRA) is enabling the development of CO₂-sequestering additives, which actively reduce environmental impact by trapping pollutants within coating films. The adoption of AI-driven formulation platforms is accelerating product development cycles and enhancing performance optimization for near-zero VOC coatings. High-end applications, including aerospace MRO and composite airframe coatings, are driving demand for advanced adhesion promoters and functional additives that meet strict durability and environmental standards.

Germany serves as a European hub for sustainable coating additive innovation, focusing on circular economy principles and strict compliance with evolving EU Ecolabel standards. The development of VOC-free, biocide-free additive architectures, such as those introduced under hubergroup’s ELARA brand, is enabling high-performance waterborne systems with reduced environmental impact.

Technological advancements include the transition to 100% bio-based rheology modifiers, eliminating the need for solvent-heavy thickeners while maintaining high viscosity and performance. Germany’s regulatory environment is pushing manufacturers to minimize the chemical footprint of coatings, driving demand for ultra-low-hazard additive solutions. Key applications include automotive OEM coatings, where low VOC leveling agents are critical for achieving premium finishes in waterborne multi-layer systems. Additionally, investments and consolidation strategies by companies like Evonik are strengthening Germany’s position in the specialty chemicals and coating additives sector. The integration of low VOC additives in hydrogen infrastructure coatings further highlights the country’s focus on future-ready applications.

India Low VOC Coating Additives Market: Local Manufacturing Expansion and Infrastructure-Led Demand

India is witnessing rapid growth in the low VOC coating additives market, driven by infrastructure expansion and increasing localization of production under the “Make in India” initiative. Events such as PAINT INDIA 2026 have showcased next-generation dispersing and wetting agents optimized for high-humidity environments, reflecting the region’s unique climatic requirements.

The influx of foreign direct investment (FDI), including expansion plans by global players like AkzoNobel, is boosting domestic manufacturing capabilities for advanced coating additives. The enforcement of standards such as IS 15489 for plastic emulsion paints is ensuring widespread adoption of low VOC formulations in public infrastructure projects. The development of Multi-Modal Logistics Parks is increasing demand for industrial coatings that incorporate anti-slip and abrasion-resistant additives. Additionally, applications in smart city infrastructure, including waterborne road marking systems, are driving the transition from solvent-based to eco-friendly additive technologies.

UAE Low VOC Coating Additives Market: Smart City Development and Wellness Architecture Driving Adoption

The UAE is emerging as a high-value niche market for low VOC coating additives, driven by ambitious sustainability goals under the “Net Zero by 2050” initiative. Strict regulatory frameworks, including defined VOC limits for interior coatings, are making high-efficiency low VOC additives essential for market entry.

Innovations such as cool-roof additives with high solar reflectance index (SRI) are gaining traction, particularly in large-scale urban developments aimed at reducing heat island effects. The demand for low-odor, antimicrobial additives is strong in hospitality and healthcare sectors, enabling rapid re-occupancy after renovations. Industrial zones such as Jebel Ali and KIZAD are witnessing increased adoption of waterborne coating systems supported by government incentives. Additionally, infrastructure projects are driving demand for low VOC waterproofing additives, ensuring durability and safety in underground and high-moisture environments. Market trends indicate a shift toward transparency, with end-users increasingly demanding verified VOC content data in technical specifications.

Japan Low VOC Coating Additives Market: Functional Surface Innovation and Advanced Material Science

Japan’s low VOC coating additives market is defined by its focus on functionalized surfaces, precision engineering, and advanced material innovation. The country is pioneering visible-light photocatalytic additives, which actively decompose VOCs, effectively transforming coated surfaces into air-purifying systems.

Technological advancements include the development of high-solid, low-viscosity dispersants, enabling coatings with up to 70–80% solids content while maintaining low VOC emissions. These innovations are critical for applications in industrial robotics, electronics, and high-tech infrastructure, where performance and environmental compliance are equally important. Regulatory updates under the Chemical Substances Control Law (CSCL) are pushing manufacturers toward safer, eco-friendly additives, replacing traditional chemical components. Japan is also leading in self-healing additive technologies, which extend the lifecycle of coatings and reduce maintenance costs in public infrastructure and advanced manufacturing environments.

By Type (Rheology Modifiers, Dispersants, Wetting Agents, Defoamers, Biocides, Anti-Corrosion Additives, UV Stabilizers, Specialty Additives), By Formulation Technology (Water-borne, High Solids, Powder-based, Radiation-Cured, Bio-based), By End-Use Industry (Architectural, Automotive and Transportation, Industrial Coatings, Wood and Furniture, Packaging, Electronics and Semiconductors), By Substrate Material (Metals, Plastics and Polymers, Concrete and Masonry, Wood and Composites), By Price Tier (Standard, Premium, Eco-Certified), By Sales Channel (Direct Sales, Specialty Chemical Distributors, Online B2B Platforms)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

2. Low Volatile Organic Compounds Coating Additives Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Low Volatile Organic Compounds Coating Additives Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers

2.4. Market Restraints and Challenges

2.5. Market Opportunities

2.6. Regulatory and Sustainability Landscape

2.7. Value Chain Analysis

2.8. Pricing Analysis

2.9. Technology Roadmap and Future Outlook

3. Innovations Reshaping the Low Volatile Organic Compounds Coating Additives Market

3.1. Trend: Reactive Coalescent Technologies Enabling Zero-VOC Paint Formulations

3.2. Trend: 100% Active Non-VOC Defoamers Optimizing Waterborne Coating Systems

3.3. Opportunity: China GB 30981.1-2025 Standard Driving Ultra-Low VOC Additive Demand

3.4. Opportunity: U.S. GSA P100 Standards Expanding Federal Construction Demand

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Low Volatile Organic Compounds Coating Additives Market

5.1. By Type

5.1.1. Rheology Modifiers

5.1.2. Dispersants

5.1.3. Wetting Agents

5.1.4. Defoamers

5.1.5. Biocides

5.1.6. Anti-Corrosion Additives

5.1.7. UV Stabilizers

5.1.8. Specialty Additives

5.2. By Formulation Technology

5.2.1. Water-borne

5.2.2. High Solids

5.2.3. Powder-based

5.2.4. Radiation-Cured

5.2.5. Bio-based

5.3. By End-Use Industry

5.3.1. Architectural

5.3.2. Automotive and Transportation

5.3.3. Industrial Coatings

5.3.4. Wood and Furniture

5.3.5. Packaging

5.3.6. Electronics and Semiconductors

5.4. By Substrate Material

5.4.1. Metals

5.4.2. Plastics and Polymers

5.4.3. Concrete and Masonry

5.4.4. Wood and Composites

5.5. By Price Tier

5.5.1. Standard

5.5.2. Premium

5.5.3. Eco-Certified

5.6. By Sales Channel

5.6.1. Direct Sales

5.6.2. Specialty Chemical Distributors

5.6.3. Online B2B Platforms

6. Country Analysis and Outlook of Low Volatile Organic Compounds Coating Additives Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Low Volatile Organic Compounds Coating Additives Market Size Outlook by Region (2025–2034)

7.1. North America Low Volatile Organic Compounds Coating Additives Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Formulation Technology

7.1.3. By End-Use Industry

7.1.4. By Substrate Material

7.1.5. By Price Tier

7.1.6. By Sales Channel

7.2. Europe Low Volatile Organic Compounds Coating Additives Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Formulation Technology

7.2.3. By End-Use Industry

7.2.4. By Substrate Material

7.2.5. By Price Tier

7.2.6. By Sales Channel

7.3. Asia Pacific Low Volatile Organic Compounds Coating Additives Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Formulation Technology

7.3.3. By End-Use Industry

7.3.4. By Substrate Material

7.3.5. By Price Tier

7.3.6. By Sales Channel

7.4. South America Low Volatile Organic Compounds Coating Additives Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Formulation Technology

7.4.3. By End-Use Industry

7.4.4. By Substrate Material

7.4.5. By Price Tier

7.4.6. By Sales Channel

7.5. Middle East and Africa Low Volatile Organic Compounds Coating Additives Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Formulation Technology

7.5.3. By End-Use Industry

7.5.4. By Substrate Material

7.5.5. By Price Tier

7.5.6. By Sales Channel

8. Company Profiles: Leading Players in the Low Volatile Organic Compounds Coating Additives Market

8.1. Evonik Industries AG

8.2. BASF SE

8.3. BYK-Chemie GmbH

8.4. Dow Inc.

8.5. Arkema S.A.

8.6. Eastman Chemical Company

8.7. Clariant AG

8.8. The Lubrizol Corporation

8.9. Elementis plc

8.10. Solvay S.A.

8.11. Ashland Inc.

8.12. Allnex GmbH

8.13. Nouryon

8.14. Momentive Performance Materials Inc.

8.15. Munzing Chemie GmbH

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

The global low volatile organic compounds (VOC) coating additives market was valued at $5.1 billion in 2025 and is projected to reach $7.5 billion by 2032, growing at a CAGR of 5.7%. Market growth is being driven by rising demand for low-VOC surfactants, dispersants, rheology modifiers, wetting agents, and VOC-free additive systems used in waterborne, powder-based, and radiation-cured coatings across architectural, automotive, industrial, and electronics sectors.

Reactive coalescents and 100% active non-VOC defoamers are gaining strong adoption because they enable zero-VOC paint formulations while improving film hardness, scrub resistance, foam control, and surface smoothness. These advanced additives help coating manufacturers overcome traditional waterborne formulation challenges such as poor wetting, micro-foam formation, and reduced open time, while ensuring compliance with increasingly strict global indoor air quality and emissions regulations.

The industry is rapidly transitioning toward PFAS-free and bio-based additive technologies as environmental regulations tighten across North America, Europe, and Asia-Pacific. Coating formulators are increasingly adopting sustainable rheology modifiers, silicone-free wetting agents, VOC-free dispersants, and renewable-content additives to reduce environmental impact while maintaining coating durability, gloss control, corrosion resistance, and high-performance application properties.

Architectural coatings, automotive OEM coatings, industrial maintenance coatings, electronics, semiconductor manufacturing, packaging, and advanced construction applications are generating substantial demand for low VOC additive technologies. Europe remains a leader in regulatory-driven sustainable additive innovation, while Asia-Pacific, particularly China and India, is witnessing rapid expansion due to manufacturing growth, VOC reformulation mandates, and rising environmental compliance requirements.

Major companies operating in the low VOC coating additives industry include Evonik Industries AG, BASF SE, BYK-Chemie GmbH, Dow Inc., Arkema S.A., Clariant AG, The Lubrizol Corporation, and Elementis plc. These companies are investing heavily in PFAS-free additive platforms, bio-based chemistries, AI-driven formulation technologies, and high-efficiency waterborne coating additives to strengthen their global market positions.