Paint and Coating Resins Market Size, Specialty Resin Expansion, and Sustainability-Driven Reformulation

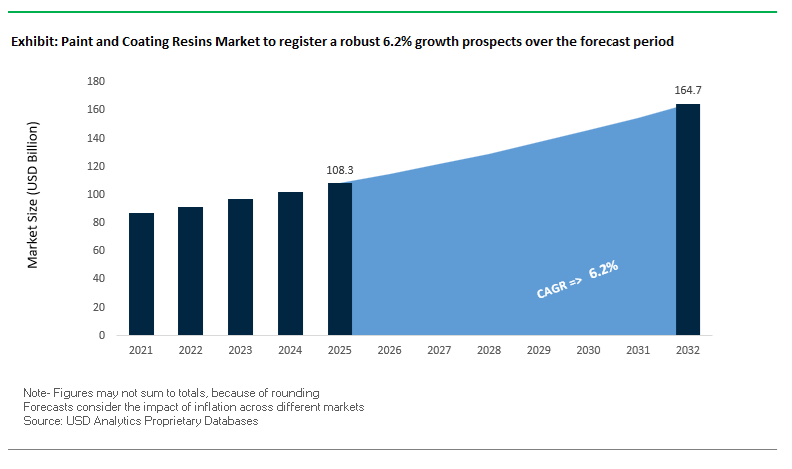

The global Paint and Coating Resins Market reached $108.3 billion in 2025 and is projected to grow at a CAGR of 6.2% through 2032, reaching $165 billion by 2032. This growth reflects the central role of resins as the primary film-forming backbone in coatings, directly influencing adhesion, durability, chemical resistance, and overall coating performance across architectural, automotive, industrial, and specialty applications.

A defining structural trend in this market is the transition toward waterborne, high-solid, UV-curable, and bio-attributed resin systems, driven by tightening environmental regulations and decarbonization targets. Regulatory frameworks across Europe, North America, and Asia are restricting solvent emissions and pushing manufacturers to adopt low-VOC and solvent-free resin technologies. This shift is accelerating innovation in acrylics, polyurethanes, epoxies, alkyds, and hybrid resin chemistries, particularly those compatible with sustainable feedstocks and mass-balance approaches.

Simultaneously, the rapid evolution of end-use industries is increasing demand for high-performance resins. Automotive coatings are moving toward multi-layer, high-gloss, and effect-driven finishes, while industrial applications require enhanced corrosion resistance, mechanical strength, and thermal stability. The rise of electric vehicles, renewable energy infrastructure, and advanced construction materials is further amplifying demand for specialty resins capable of operating under extreme environmental and mechanical conditions.

Another key growth driver is the regionalization of resin production and supply chains, particularly in Asia-Pacific, where local manufacturing capabilities are expanding to meet demand from coatings, packaging, and industrial sectors. Concurrently, the market is witnessing a strategic shift among leading producers toward high-margin specialty resins and integrated solution platforms, moving away from commoditized segments and focusing on innovation-led differentiation.

Recent developments in the Paint and Coating Resins Market highlight a convergence of capacity expansion, raw material volatility, sustainability innovation, and strategic repositioning among key industry players. In February 2026, Covestro confirmed the acquisition of Vencorex’s HDI derivative production sites in Thailand and the United States, significantly strengthening its position in aliphatic isocyanates for polyurethane coatings. This move enhances supply security for high-performance automotive and industrial coatings while reinforcing Covestro’s global manufacturing footprint.

Cost pressures are also emerging as a critical market factor. In April 2026, DIC Corporation implemented global price revisions for epoxy resins, citing rising naphtha costs and geopolitical disruptions in feedstock supply chains. This reflects broader margin compression across thermoset resin segments, prompting manufacturers to optimize pricing strategies and explore alternative raw materials.

Strategic platform integration and digitalization are reshaping product accessibility and formulation workflows. Arkema’s March 2026 launch of its unified “Coating Materials” platform consolidates its resin portfolio, emphasizing bio-attributed and waterborne technologies to support compliance with evolving EU sustainability reporting standards. Similarly, Lubrizol expanded its Carboset® and Hycar® water-based resin lines in November 2025, targeting medical packaging and food-contact applications with a localized production approach in Asia.

Collaborative innovation is accelerating next-generation resin development. The Allnex–Nippon Paint partnership (November 2025) focuses on bio-based sagging control resins and high-performance industrial coatings, particularly for coil and marine applications. In parallel, Allnex’s launch of recycled PET (rPET) powder coating resins (September 2025) represents a significant advancement in circular economy integration, enabling high-performance coatings derived from post-consumer plastic waste.

Portfolio expansion and specialization continue to define competitive strategies. Covestro’s acquisition of Pontacol AG (August 2025) extends its reach into multilayer resin technologies for medical and mobility applications, while Evonik’s strategic pivot toward high-margin specialty resin precursors (March 2025) targets growth in wind energy and EV battery coatings. Meanwhile, BASF’s 2025–2026 automotive color trends initiative is influencing resin innovation toward complex visual effects and enhanced durability, reflecting the increasing intersection of aesthetics and performance in coatings.

Market Trend: High-Tg Acrylic Resins Enabling Durable Zero-VOC Architectural Coatings with Superior Block Resistance

The paint and coating resins industry is advancing rapidly with the adoption of high glass transition temperature acrylic resins designed for zero-VOC architectural coatings. These next-generation acrylic emulsions address a long-standing limitation in low-VOC paints, where soft resin systems resulted in poor block resistance and tacky film formation. High-Tg acrylic binders are now enabling the development of hard, durable coatings without the need for coalescing solvents, aligning with stringent environmental regulations and indoor air quality standards.

Modern high-Tg acrylic resins, with Tg values exceeding 30°C, achieve block resistance ratings of 8 or higher under ASTM D4946 testing at ambient conditions, even in formulations containing less than 5 g/L VOC. This performance matches or exceeds solvent-assisted coatings, making them suitable for high-performance interior applications such as doors, trims, and cabinetry. Enhanced film hardness is another critical advantage. These resins deliver a 20% to 35% increase in König hardness within seven days of application compared to conventional zero-VOC binders, significantly improving scrubbability and resistance to surface damage in flat and eggshell finishes.

To maintain application flexibility in varying climates, high-Tg acrylic systems incorporate multiphase particle morphology, typically featuring hard-core and soft-shell structures. This design enables a minimum film forming temperature below 5°C, ensuring proper film formation even in low-temperature conditions despite the inherently high Tg of the resin. This combination of hardness, durability, and low-temperature applicability is positioning high-Tg acrylic resins as a cornerstone technology in next-generation zero-VOC architectural coatings.

Industrial coating applications are undergoing a significant transformation with the shift toward styrene-free epoxy vinyl ester resins. Increasing regulatory scrutiny from OSHA and REACH on styrene as a hazardous air pollutant is driving the replacement of traditional styrene-based systems with low-VOC alternatives that utilize methacrylates and other reactive diluents.

Styrene-free vinyl ester resins deliver substantial reductions in VOC emissions, typically ranging from 70% to 90% during application and curing processes. This reduction allows these coatings to be used in enclosed or poorly ventilated industrial environments without the need for extensive respiratory protection, improving worker safety and operational flexibility. The low-odor profile of these systems further enhances their suitability for sensitive environments. Compared to styrene-based resins, styrene-free formulations exhibit odor detection thresholds up to 50 times higher, making them ideal for use in food processing facilities, pharmaceutical plants, and occupied commercial retrofit projects.

Mechanical performance remains uncompromised despite the shift in chemistry. Modern styrene-free epoxy vinyl ester resins maintain heat deflection temperatures in the range of 100°C to 120°C, comparable to high-performance bisphenol-A-based systems. This ensures structural integrity in demanding applications such as chemical storage tanks, pipelines, and industrial flooring exposed to high temperatures and aggressive environments. These attributes are driving strong adoption of styrene-free resins in industrial protective coatings where performance, safety, and regulatory compliance are critical.

Market Opportunity: EU BPA-Free Regulation Driving Demand for Advanced Epoxy Alternatives in Food Contact Coatings

The implementation of Regulation (EU) 2024/3190 is creating a major transformation in the paint and coating resins industry, particularly in food contact applications. This regulation mandates the elimination of Bisphenol A from epoxy-based coatings used in packaging and storage systems, with full enforcement beginning on July 20, 2026. The requirement is triggering a large-scale reformulation cycle across metal packaging, tank linings, and food processing equipment coatings.

The industry is rapidly transitioning toward BPA-NI epoxy hybrid systems, where bisphenol content must remain below detection thresholds of 10 parts per billion. Suppliers capable of achieving and validating these ultra-low migration levels are gaining preferred supplier status among global beverage and food packaging manufacturers. This shift is creating a competitive advantage for companies investing in advanced analytical capabilities and compliant resin technologies.

The scale of the transition is significant, with approximately 70% of existing metal packaging coatings in the European market currently relying on BPA-based epoxy resins. This creates a substantial replacement gap, driving demand for alternative chemistries such as polyester, acrylic, and bio-based resins that can meet performance requirements while ensuring regulatory compliance. The convergence of regulatory pressure and supply chain realignment is positioning BPA-free resin technologies as a high-growth segment within the coatings industry.

Market Opportunity: China NDRC Bio-Based Resin Funding Accelerating Development of Sustainable Coating Materials

China’s strategic focus on bio-based materials is creating a major opportunity for resin manufacturers, supported by significant funding initiatives from the National Development and Reform Commission. The integration of bio-based resins into the national industrial roadmap is driving investment in renewable material technologies across the coatings sector.

Under the 2026 to 2030 development plan, manufacturers are incentivized to incorporate resins with at least 30% biogenic carbon content, verified through standardized testing methods. Companies meeting these criteria are eligible for tax rebates of up to 15% on research and development equipment, encouraging rapid scaling of bio-based resin production capabilities. This policy framework is accelerating innovation in renewable chemistries, including cardanol-based and itaconic acid-derived resins.

Performance targets are also clearly defined. Bio-based epoxy and polyurethane resins are expected to match the hydrolysis resistance and durability of petroleum-derived systems over extended service lifetimes, typically exceeding 10 years under accelerated aging conditions. Achieving this parity is critical for adoption in industrial protective coatings, where long-term reliability is essential.

The scale of implementation is already evident, with major domestic manufacturers commissioning large-scale production facilities for bio-based resins as of early 2026. This rapid expansion is positioning China as a global leader in sustainable resin technologies, creating opportunities for both domestic and international suppliers aligned with bio-based innovation and environmental compliance.

Paint and Coatings Resin Market Share and Segmentation Insights

Acrylic Resins Capture 28.3% Share Driven by Low-VOC Regulations and Multi-Sector Demand

The paint and coating resins market by resin type is led by acrylic resins, accounting for 28.3% of the global market share in 2025, primarily due to their central role in waterborne coating technologies. Acrylic emulsions form the backbone of low-VOC architectural paints, widely used in interior and exterior walls, ceilings, and trim, as global regulations increasingly restrict solvent-borne systems. Their dominance is further supported by exceptional versatility across decorative coatings, industrial coatings, automotive refinish, traffic paints, and roof coatings, offering superior weatherability, color retention, and durability. Acrylic resins also enable formulators to achieve high-performance coatings with environmental compliance, making them the preferred choice in both developed and emerging markets. This broad applicability ensures acrylics maintain the largest share in the global coating resins market.

Direct Sales Hold 52.1% Share Driven by Technical Collaboration and Bulk Resin Procurement

In the paint and coating resins market by sales channel, direct sales dominate with a 52.1% market share in 2025, reflecting the critical need for technical collaboration and supply chain reliability among large coating manufacturers. Major players such as BASF, Dow, and Arkema work directly with customers to co-develop custom resin formulations, tailored to specific performance requirements such as scrub resistance, corrosion protection, adhesion, and weatherability. This level of customization is essential for architectural paint producers, industrial coating formulators, and automotive OEMs. Additionally, direct sales enable bulk purchasing agreements, ensuring pricing stability, consistent quality, and priority supply, especially during raw material volatility. By bypassing distributor markups and offering integrated technical support, direct sales channels remain the dominant and most efficient route in the global coating resins market.

Competitive Landscape of the Paint and Coating Resins Market

Allnex Leads Sustainable Resin Innovation with Low-VOC and Non-Isocyanate Technologies

Allnex, owned by PTT Global Chemical, is a global leader in industrial coating resins, particularly in ultra-low VOC and non-isocyanate technologies. In 2026, the company introduced ACURE® AQ, a waterborne 2K system that delivers rapid curing with extended pot life while eliminating risks like reactive blistering. Its CRYLCOAT® OCEAN series incorporates up to 50% recycled polyester (rPET), enabling low-bake curing at 160°C and reducing energy consumption for OEMs. Allnex has also expanded its R&D capabilities in India to develop bio-based alkyds and acrylic polyols for infrastructure applications. With strong leadership in UV-curable resins, its UCECOAT® range supports high-performance coatings for electronics and industrial use.

BASF Drives High-Performance Resin Development with Circular and Automotive Innovations

BASF SE is a dominant force in the paint and coating resins market, leveraging its integrated Verbund system to deliver advanced binder technologies. In 2026, the company enhanced its resin portfolio to support “liquid-metal” color effects through interference-pigment-compatible formulations. Its transition of the Basonal® PLUS range to bio-circular feedstock enables manufacturers to reduce Scope 3 emissions by up to 20%. BASF continues to invest heavily in R&D, focusing on ChemCycling to produce recycled monomers for high-performance resins, including CathoGuard® electrocoat systems for EV applications. With its strong presence in automotive OEM coatings, BASF provides the foundation for nearly 30% of global vehicle production.

Covestro Advances Polyurethane Resin Technologies for Mobility and Smart Applications

Covestro AG is a key innovator in polyurethane and TPU-based coating resins, targeting high-performance and sustainable applications. In 2026, the company introduced antimicrobial INSQIN® coatings integrated with silver technology for automotive interiors, enhancing hygiene in high-contact environments. Its Desmopan® AIR and FLY product lines enable lightweight, recyclable, and flexible resin solutions for footwear, automotive seating, and apparel industries. Covestro is also advancing smart materials through Platilon® films, supporting predictive maintenance and wearable electronics. By focusing on circular economy and advanced polymer engineering, the company strengthens its position in next-generation coating resin technologies.

Arkema Expands Bio-Based Resin Portfolio with High-Performance and Circular Solutions

Arkema is a leading player in the bio-based and high-performance coating resins market, emphasizing non-isocyanate and high-solid resin technologies. In 2026, the company showcased sustainable resins with up to 93% bio-based content, alongside powder coatings containing 40% recycled materials. Its Singapore production facility for Rilsan® Clear polyamides strengthens its leadership in BPA-free transparent resins across Asia. Arkema’s innovations include fast-curing waterborne NISO systems and coatings designed to reduce carbon footprint in infrastructure applications. Its Kynar® PVDF resins remain the industry benchmark for high-weatherability coatings, widely used in architectural and industrial applications.

Evonik Strengthens Resin Performance Through Additive Integration and Green Chemistry

Evonik Industries AG plays a critical role in the paint and coating resins market, focusing on the synergy between additives and resin systems. In 2026, the company expanded its specialty amine production in China to support advanced curing systems that enhance efficiency and reduce VOC emissions. Its TEGO® silicone-epoxy hybrid resins offer extreme heat resistance up to 600°C and superior anti-corrosion performance, making them ideal for energy and marine applications. Evonik is also advancing sustainability by powering its facilities with renewable energy, aligning with RE100 standards. Its integrated approach ensures optimized coating performance, durability, and environmental compliance across industrial applications.

China Paint and Coating Resins Market: High-Performance Scaling and Electronics Integration

China continues to dominate the global paint and coating resins market, rapidly transitioning toward high-performance, specialty resin production for advanced industries such as semiconductors, EVs, and electronics manufacturing. Strategic investments, including Evonik’s expansion of specialty amine curing agent production in Nanjing, are strengthening China’s capabilities in epoxy-based industrial coatings. Additionally, BASF’s advanced Controlled Free Radical Polymerization (CFRP) resin production line is enabling the development of high-gloss coatings tailored for automotive OEM applications.

The implementation of GB 4806.10-2025 standards, which significantly expanded permitted materials for food-contact coatings, has accelerated innovation in plasma-assisted barrier resins. China’s strong push for industrial growth, supported by a 5% annual industrial added value mandate, is driving demand for CVD-compatible resins in electronics manufacturing. Tightening VOC emission regulations are further accelerating the adoption of waterborne binders and HEUR rheology modifiers, reinforcing sustainability goals. With nearly 25% share in global vacuum coating equipment demand, China is also boosting demand for UV-curable oligomers and high-purity coating resins, solidifying its leadership in advanced materials.

United States Paint and Coating Resins Market: PFAS-Free Innovation and Infrastructure-Led Demand

The United States paint and coating resins market is undergoing a major transformation driven by PFAS-free innovations, infrastructure investments, and sustainable resin technologies. Manufacturers are focusing on developing polysiloxane and hyperbranched polymer resins as high-performance alternatives to traditional fluoropolymers in non-stick and anti-fouling applications.

Innovations such as Engineered Polymer Solutions’ 2400 series waterborne acrylic resins are improving durability in industrial wood coatings, while PPG’s DURANEXT UV-curable resin platform is enabling near-instantaneous curing in metal coil applications, reducing energy consumption significantly. The Infrastructure Investment and Jobs Act is driving strong demand for high-solids epoxy and polyurethane resins, particularly for long-term corrosion protection in bridges and highways. Additionally, the rise of bio-based epoxy resins, supported by USDA certification, is expanding applications in aerospace and sporting goods. Nearshoring trends are also strengthening localized production of powder coating resins in the U.S. Sun Belt, supporting automotive and appliance manufacturing.

Germany Paint and Coating Resins Market: Circular Economy Leadership and Bio-Resin Innovation

Germany stands at the forefront of the European paint and coating resins market, driven by its focus on circular economy principles, bio-based chemistry, and Industry 4.0 manufacturing. Innovations such as 50% bio-based UV oligomers derived from sorbitol, showcased at the European Coatings Show 2025, are transforming the production of high-performance coatings for wood and plastics.

German manufacturers are integrating digital tracer technologies directly into resin matrices, enabling automated recycling systems to achieve up to 99.5% sorting accuracy, significantly improving sustainability. The country is also investing heavily in hydrogen infrastructure, where advanced resins are used for coating bipolar plates in fuel cells, ensuring conductivity and corrosion resistance. Regulatory frameworks such as the VerpackG amendments are encouraging the use of water-soluble adhesive resins, simplifying recycling processes. Additionally, the adoption of AI-driven dosing systems is optimizing resin curing kinetics, reducing waste, and improving efficiency, reinforcing Germany’s leadership in sustainable resin technologies.

India Paint and Coating Resins Market: Infrastructure Growth and Smart Housing Innovations

India is emerging as the fastest-growing market for paint and coating resins, driven by rapid urbanization, infrastructure expansion, and government initiatives such as the Pradhan Mantri Awas Yojana and Smart Cities Mission. Investments like Arkema’s polyester resin facility in Navi Mumbai are supporting the rapid growth of the powder coatings segment in India and neighboring regions.

The market is witnessing strong adoption of solar-reflective resins, particularly in cool-roof coatings, which reduce surface temperatures by up to 5°C, improving energy efficiency in urban environments. A steady shift toward waterborne resins, growing at around 6% annually, is being driven by environmental awareness and regulatory pressures. Government incentives under the PLI scheme are boosting domestic production of polyurethane and alkyd resins, reducing reliance on imports. Additionally, the growing demand for antimicrobial coatings with silver-ion and copper-based resins is transforming applications in healthcare and educational infrastructure.

Japan Paint and Coating Resins Market: Advanced Materials and EV Thermal Management

Japan continues to lead the paint and coating resins market through its expertise in advanced material science, active packaging, and energy-efficient coatings. Innovations in thermal-reflective automotive resins are helping reduce cabin temperatures in EVs, improving battery efficiency and driving range.

The country is also pioneering oxygen-scavenging resins for active packaging, enabling extended shelf life without additional preservatives. Developments in photocatalytic resins are enabling coatings that actively decompose pollutants, supporting cleaner urban environments. Japan’s strong focus on ultra-low migration resins ensures compliance with strict safety standards under the Positive List System for food and medical applications. Additionally, advancements in self-healing resin technologies, using micro-encapsulation techniques, are enhancing durability in automotive coatings, while investments in high-purity resins are supporting next-generation 6G optical fiber infrastructure.

Brazil Paint and Coating Resins Market: Bio-Based Polymers and Industrial Coating Expansion

Brazil is leveraging its strong agricultural base to become a leader in bio-based paint and coating resins, particularly those derived from sugarcane ethanol and vegetable oils. The country is a global hub for Green PE resins, widely used in sustainable architectural coatings and packaging applications.

The Brazilian market is experiencing strong growth in industrial coatings, with resin demand rising due to infrastructure investments and logistics expansion. Significant R&D efforts are focused on chemical-resistant epoxy resins for agrochemical containers, ensuring durability under high humidity conditions. The automotive sector is also driving demand for adhesion-promoting resins, particularly for coatings applied to recycled plastic components. Innovations such as carnauba-modified resins are improving scratch resistance in furniture and wood coatings. Additionally, the adoption of high-solids and solvent-free resin technologies is aligning Brazil with global ESG standards, strengthening its position in sustainable coatings.

South Korea Paint and Coating Resins Market: Semiconductor-Grade Materials and Marine Coating Innovation

South Korea’s paint and coating resins market is driven by its dominance in semiconductors, electronics, and advanced materials manufacturing. The country leads in the development of plasma-resistant resins and photo-curable oligomers, essential for advanced semiconductor fabrication processes such as 3D NAND and FinFET technologies.

Technological advancements include low-voltage curing resins (<160V), enabling coating applications on ultra-thin, flexible electronic substrates. South Korea is also a leader in high-barrier retort pouch resins, maintaining structural integrity under extreme sterilization conditions for global food packaging applications. The adoption of bio-based marine coating resins, such as those using Selektope technology, is enabling environmentally friendly anti-fouling solutions. Additionally, the influence of the K-Beauty industry is driving demand for premium soft-touch and pearlescent effect resins for cosmetic packaging. Innovations in thin-film encapsulation (TFE) resins are further supporting the country’s leadership in advanced OLED display technologies.

Paint and Coating Resins Market Report Scope

Paint and Coating Resins Market

Parameter

Details

Market Size (2025)

$108.3 Billion

Market Size (2032)

$165 Billion

Market Growth Rate

6.2%

Segments

By Resin (Acrylic, Epoxy, Polyurethane, Alkyd, Polyester, Vinyl, Fluoropolymer, Amino Resins, Silicones, Natural, Hybrid Resins), By Technology (Water-borne Resins, Solvent-borne Resins, Powder Coating Resins, Radiation-Cured, Solvent-free), By End-Use Industry (Architectural and Decorative, Automotive and Transportation, General Industrial, Industrial Wood and Furniture, Protective and Marine, Packaging, Consumer Electronics, Coil and Extrusion), By Substrate Compatibility (Metals, Wood and Wood-based Panels, Plastics and Polymers, Concrete, Glass, and Masonry, Paper and Flexible Films), By Functional Property (Standard, High-Performance Grade, Specialty), By Price Point (Economy, Mid-Range, Premium), By Sales Channel (Direct Sales, Specialty Chemical Distributors, Contract)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Paint and Coating Resins Market Segmentation

By Resin

Acrylic

Epoxy

Polyurethane

Alkyd

Polyester

Vinyl

Fluoropolymer

Amino Resins

Silicones

Natural

Hybrid Resins

By Technology

Water-borne Resins

Solvent-borne Resins

Powder Coating Resins

Radiation-Cured

Solvent-free

By End-Use Industry

Architectural and Decorative

Automotive and Transportation

General Industrial

Industrial Wood and Furniture

Protective and Marine

Packaging

Consumer Electronics

Coil and Extrusion

By Substrate Compatibility

Metals

Wood and Wood-based Panels

Plastics and Polymers

Concrete, Glass, and Masonry

Paper and Flexible Films

By Functional Property

Standard

High-Performance Grade

Specialty

By Price Point

Economy

Mid-Range

Premium

By Sales Channel

Direct Sales

Specialty Chemical Distributors

Contract

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Paint and Coating Resins Industry

BASF SE

Dow Inc.

Arkema S.A.

allnex GmbH

Covestro AG

Evonik Industries AG

Hexion Inc.

Huntsman Corporation

Mitsui Chemicals, Inc.

Mitsubishi Chemical Group

Sinopec Corporation

DIC Corporation

Wacker Chemie AG

Solvay S.A.

Lubrizol Corporation

*- List not Exhaustive

Table of Contents: Paint and Coating Resins Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Paint and Coating Resins Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Paint and Coating Resins Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers

2.4. Market Restraints and Challenges

2.5. Market Opportunities

2.6. Regulatory and Sustainability Landscape

2.7. Value Chain Analysis

2.8. Pricing Analysis

2.9. Technology Roadmap and Future Outlook

3. Innovations Reshaping the Paint and Coating Resins Market

3.1. Trend: High-Tg Acrylic Resins Enabling Durable Zero-VOC Architectural Coatings with Superior Block Resistance

3.2. Trend: Styrene-Free Epoxy Vinyl Ester Resins Reducing VOC Emissions in Industrial Protective Coatings

3.3. Opportunity: EU BPA-Free Regulation Driving Demand for Advanced Epoxy Alternatives in Food Contact Coatings

3.4. Opportunity: China NDRC Bio-Based Resin Funding Accelerating Development of Sustainable Coating Materials

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Material Innovation

4.3. Sustainability and ESG Strategies

4.4. Market Expansion and Regional Focus

5. Market Share and Segmentation Insights: Paint and Coating Resins Market

5.1. By Resin

5.1.1. Acrylic

5.1.2. Epoxy

5.1.3. Polyurethane

5.1.4. Alkyd

5.1.5. Polyester

5.1.6. Vinyl

5.1.7. Fluoropolymer

5.1.8. Amino Resins

5.1.9. Silicones

5.1.10. Natural

5.1.11. Hybrid Resins

5.2. By Technology

5.2.1. Water-borne Resins

5.2.2. Solvent-borne Resins

5.2.3. Powder Coating Resins

5.2.4. Radiation-Cured

5.2.5. Solvent-free

5.3. By End-Use Industry

5.3.1. Architectural and Decorative

5.3.2. Automotive and Transportation

5.3.3. General Industrial

5.3.4. Industrial Wood and Furniture

5.3.5. Protective and Marine

5.3.6. Packaging

5.3.7. Consumer Electronics

5.3.8. Coil and Extrusion

5.4. By Substrate Compatibility

5.4.1. Metals

5.4.2. Wood and Wood-based Panels

5.4.3. Plastics and Polymers

5.4.4. Concrete, Glass, and Masonry

5.4.5. Paper and Flexible Films

5.5. By Functional Property

5.5.1. Standard

5.5.2. High-Performance Grade

5.5.3. Specialty

5.6. By Price Point

5.6.1. Economy

5.6.2. Mid-Range

5.6.3. Premium

5.7. By Sales Channel

5.7.1. Direct Sales

5.7.2. Specialty Chemical Distributors

5.7.3. Contract

6. Country Analysis and Outlook of Paint and Coating Resins Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. UK

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Middle East

6.19. Africa

7. Paint and Coating Resins Market Size Outlook by Region (2025–2034)

7.1. North America Paint and Coating Resins Market Size Outlook to 2034

7.1.1. By Resin

7.1.2. By Technology

7.1.3. By End-Use Industry

7.1.4. By Substrate Compatibility

7.1.5. By Functional Property

7.1.6. By Price Point

7.1.7. By Sales Channel

7.2. Europe Paint and Coating Resins Market Size Outlook to 2034

7.2.1. By Resin

7.2.2. By Technology

7.2.3. By End-Use Industry

7.2.4. By Substrate Compatibility

7.2.5. By Functional Property

7.2.6. By Price Point

7.2.7. By Sales Channel

7.3. Asia Pacific Paint and Coating Resins Market Size Outlook to 2034

7.3.1. By Resin

7.3.2. By Technology

7.3.3. By End-Use Industry

7.3.4. By Substrate Compatibility

7.3.5. By Functional Property

7.3.6. By Price Point

7.3.7. By Sales Channel

7.4. South America Paint and Coating Resins Market Size Outlook to 2034

7.4.1. By Resin

7.4.2. By Technology

7.4.3. By End-Use Industry

7.4.4. By Substrate Compatibility

7.4.5. By Functional Property

7.4.6. By Price Point

7.4.7. By Sales Channel

7.5. Middle East and Africa Paint and Coating Resins Market Size Outlook to 2034

7.5.1. By Resin

7.5.2. By Technology

7.5.3. By End-Use Industry

7.5.4. By Substrate Compatibility

7.5.5. By Functional Property

7.5.6. By Price Point

7.5.7. By Sales Channel

8. Company Profiles: Leading Players in the Paint and Coating Resins Market

8.1. BASF SE

8.2. Dow Inc.

8.3. Arkema S.A.

8.4. allnex GmbH

8.5. Covestro AG

8.6. Evonik Industries AG

8.7. Hexion Inc.

8.8. Huntsman Corporation

8.9. Mitsui Chemicals, Inc.

8.10. Mitsubishi Chemical Group

8.11. Sinopec Corporation

8.12. DIC Corporation

8.13. Wacker Chemie AG

8.14. Solvay S.A.

8.15. Lubrizol Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Paint and Coating Resins Market Segmentation

By Resin

Acrylic

Epoxy

Polyurethane

Alkyd

Polyester

Vinyl

Fluoropolymer

Amino Resins

Silicones

Natural

Hybrid Resins

By Technology

Water-borne Resins

Solvent-borne Resins

Powder Coating Resins

Radiation-Cured

Solvent-free

By End-Use Industry

Architectural and Decorative

Automotive and Transportation

General Industrial

Industrial Wood and Furniture

Protective and Marine

Packaging

Consumer Electronics

Coil and Extrusion

By Substrate Compatibility

Metals

Wood and Wood-based Panels

Plastics and Polymers

Concrete, Glass, and Masonry

Paper and Flexible Films

By Functional Property

Standard

High-Performance Grade

Specialty

By Price Point

Economy

Mid-Range

Premium

By Sales Channel

Direct Sales

Specialty Chemical Distributors

Contract

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global paint and coating resins market reached $108.3 billion in 2025 and is projected to grow to $165 billion by 2032, expanding at a CAGR of 6.2%. Market growth is being driven by rising demand for waterborne resins, UV-curable technologies, specialty acrylics, polyurethane systems, and sustainable low-VOC resin solutions across architectural, automotive, industrial, packaging, and protective coating applications.

High glass transition temperature (high-Tg) acrylic resins are enabling the development of durable zero-VOC architectural coatings with significantly improved hardness and block resistance. These advanced resin systems achieve ASTM D4946 block resistance ratings of 8 or higher while increasing König hardness by 20% to 35% within seven days compared to conventional low-VOC binders. Their ability to maintain film formation below 5°C through multiphase particle morphology is accelerating adoption in premium interior paints, cabinetry, and trim coatings.

The implementation of EU Regulation 2024/3190 is accelerating the replacement of BPA-based epoxy resins in food-contact coatings and packaging applications. Resin manufacturers are rapidly developing BPA-NI epoxy hybrids, polyester resins, and acrylic alternatives capable of maintaining migration levels below 10 ppb while preserving corrosion resistance and coating durability. This transition is creating major opportunities in beverage can coatings, food packaging, tank linings, and industrial food processing equipment coatings.

Asia-Pacific dominates the market due to rapid industrialization, automotive production, semiconductor expansion, and infrastructure investments in China, India, Japan, and South Korea. Germany and the United States remain innovation leaders in bio-based resins, circular economy technologies, and high-performance automotive coatings. Strong growth opportunities are emerging in EV coatings, marine coatings, active packaging, renewable energy infrastructure, semiconductor-grade coatings, and antimicrobial smart coatings.

Major companies operating in the paint and coating resins industry include BASF SE, Dow Inc., Arkema S.A., allnex GmbH, Covestro AG, Evonik Industries AG, Hexion Inc., and Lubrizol Corporation. These companies are investing heavily in bio-based resin technologies, waterborne coating systems, recycled-content resins, UV-curable chemistries, BPA-free innovations, and specialty high-performance coating materials to strengthen their global market positions.