Packaging Coating Additives Market Size, Growth Trajectory, and Sustainability-Driven Transformation

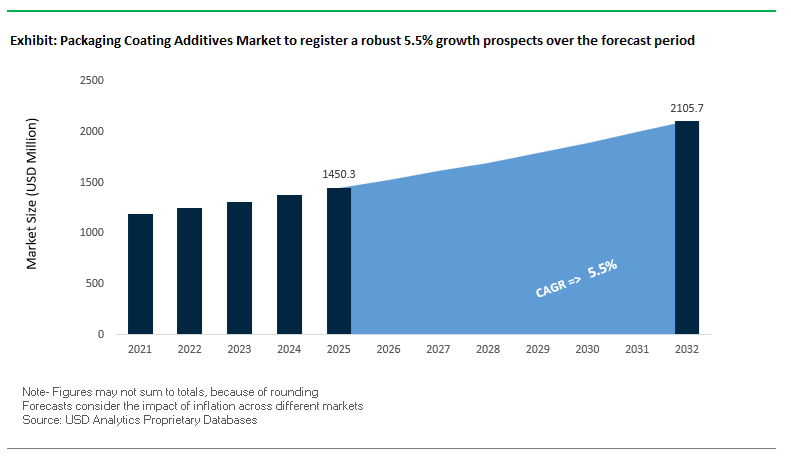

The global Packaging Coating Additives Market reached a valuation of $1,450.3 million in 2025 and is forecast to expand at a CAGR of 5.5% through 2032, ultimately attaining $2,109.7 million by 2032. This growth trajectory reflects a structural shift in the packaging ecosystem, where functional coatings are no longer optional enhancements but critical enablers of performance, compliance, and sustainability.

A key macro driver underpinning this market is the rapid transition toward sustainable, food-safe, and regulatory-compliant packaging systems, particularly across Europe and Asia-Pacific. Regulatory bodies are increasingly restricting the use of fluorinated compounds, VOC-intensive solvents, and fossil-derived additives, compelling manufacturers to adopt bio-based waxes, PFAS-free modifiers, and waterborne-compatible additives. This has elevated the role of coating additives from performance enhancers to compliance-critical components in packaging formulations.

Simultaneously, the rise of high-performance flexible packaging, e-commerce logistics, and premium printed packaging formats is intensifying demand for additives that improve scratch resistance, slip properties, pigment dispersion, and thermal stability. Advanced additives such as dispersants, rheology modifiers, wetting agents, and polyisocyanates are being engineered to deliver multi-functional performance while maintaining recyclability and food-contact compliance.

Another defining trend is the regionalization of additive production, particularly in Asia, where capacity expansions are aligning with strong demand from packaging converters and FMCG manufacturers. The market is also witnessing a strategic pivot among global chemical companies toward high-margin specialty additives, signaling consolidation and portfolio optimization across the value chain.

Recent developments in the Packaging Coating Additives Market indicate a decisive shift toward sustainable chemistry, regulatory compliance, and high-performance material innovation. In February 2026, Clariant secured EU Commission approval for its renewable rice bran wax additives, marking a critical advancement in bio-based alternatives for food-contact packaging. This innovation directly addresses the increasing demand for fossil-free coatings while maintaining stringent safety and performance benchmarks.

In parallel, BASF’s January 2026 launch of Basonat® HI 3100, an advanced aliphatic polyisocyanate, highlights the industry’s focus on enhancing durability and chemical resistance while eliminating hazardous solvents such as PCBTF. This aligns with tightening global VOC regulations and reflects the transition toward environmentally optimized coating systems. BASF further strengthened its market position through its November 2025 commissioning of a high-performance dispersant production line in Nanjing, targeting the rapidly expanding Asian packaging sector.

Portfolio optimization is also evident in Arkema’s December 2025 divestment of impact modifiers and processing aids, expected to conclude in Q1 2026. This move underscores a broader industry trend where leading players are exiting commodity additive segments to focus on specialty, high-value coating technologies. Concurrently, Lubrizol’s PTFE-free Lanco™ surface modifiers, introduced in November 2025, respond directly to the global PFAS-free movement, offering functional performance without fluorinated compounds.

Earlier in 2025, innovation momentum was driven by Evonik’s mass-balanced additives, enabling drop-in sustainability for wetting and defoaming agents, and Syensqo’s fluorosurfactant-free Rhodoline® HBR, designed for improved heat resistance in stacked packaging applications. BASF’s Joncryl® Wax 30 further reinforced the sustainability narrative by enhancing surface durability while preserving substrate recyclability, a critical factor for circular packaging systems.

Market Trend: Non-Fluorinated Slip Additives Transforming PFAS-Free Metal Packaging Coatings

The packaging coating additives industry is undergoing a structural shift as formulators eliminate PFAS-based slip additives in metal packaging coatings to comply with zero-PFAS mandates from global brands and tightening regulatory frameworks. This transition is accelerating across beverage cans, food containers, and industrial packaging, where fluorinated additives historically provided low surface energy, improved slip, and mar resistance.

Major additive suppliers are finalizing the complete phase-out of PFAS-containing chemistries by the end of 2025, forcing coating formulators to validate and commercialize alternative solutions ahead of the 2026 production cycle. This rapid portfolio transition is driving strong demand for silicone-based and wax-based slip additives that can replicate the performance of fluorinated systems without regulatory risk. Silicone-based additives, in particular, are projected to account for approximately 39% of the slip additive market by late 2026 due to their ability to deliver comparable coefficients of friction and surface smoothness.

Compatibility with waterborne coatings is a critical requirement shaping formulation strategies. With waterborne systems now representing nearly 49% of PFAS-free additive applications, formulators are prioritizing additives that maintain stability in high surface tension environments without relying on fluorosurfactants. This has led to increased innovation in surface-modified silicones and hybrid wax dispersions that ensure uniform film formation and consistent performance in aqueous systems. The shift toward PFAS-free additives is not only regulatory-driven but also aligned with sustainability and brand-driven clean packaging initiatives, making non-fluorinated slip technologies a core component of next-generation packaging coatings.

Market Trend: Oxygen Scavenging Additives Enhancing Shelf Life and Food Preservation in Metal Packaging

Active packaging technologies are gaining significant traction within the packaging coating additives market, particularly through the integration of oxygen scavenging additives into internal coating systems. This trend is driven by the need to extend product shelf life, reduce food waste, and minimize reliance on refrigeration and secondary preservation methods.

Modern oxygen scavenging additives, including transition-metal catalyzed polymer systems, are capable of reducing internal headspace oxygen levels to below 0.1%. This substantial reduction slows oxidative degradation processes in packaged foods, extending shelf life by 25% to 40% for high-fat and oxygen-sensitive products. This performance is particularly valuable in canned food applications where long-term stability is essential for distribution and storage.

In addition to shelf-life extension, these additives contribute to improved nutritional retention. Studies indicate that active barrier coatings can achieve approximately 15% higher Vitamin C retention in fruit-based products over a 12-month period compared to conventional passive barrier coatings. This aligns with clean-label trends, as manufacturers can reduce or eliminate the need for chemical preservatives and antioxidants within the food product itself.

The functional mechanism of these additives further enhances product quality. By reacting with oxygen directly within the coating matrix, they prevent the formation and migration of oxidative byproducts that can lead to off-flavors, such as aldehydes in beverages and vegetable products. This integrated approach to oxygen management is positioning active coating additives as a key innovation in advanced packaging systems, supporting both product quality and sustainability objectives.

Market Opportunity: EU Packaging and Packaging Waste Regulation Driving Demand for Recyclability-Compatible Additives

The implementation of the EU Packaging and Packaging Waste Regulation is creating a transformative opportunity for packaging coating additives, particularly in the development of recyclability-compatible and environmentally safe formulations. The regulation introduces mandatory design-for-recycling criteria that fundamentally reshape additive selection and coating formulation strategies.

Starting in August 2026, all packaging must meet harmonized recyclability standards, placing increased emphasis on coatings that do not interfere with material recovery processes. This requirement is driving demand for wash-off and de-inkable additives that allow coatings to be removed efficiently during recycling, enabling higher recovery rates for metal and paper substrates. Additives that minimize contamination and residue during remelting or pulping processes are becoming critical for maintaining high recyclability grades and reducing extended producer responsibility costs.

The regulation also targets hazardous substances, including a significant reduction in PFAS usage in food-contact packaging. This is accelerating the adoption of bio-based and non-toxic additive chemistries that offer a lower environmental impact while maintaining functional performance. As brand owners and packaging manufacturers align with circular economy goals, additive suppliers that can deliver compliant, recyclable, and high-performance solutions are positioned to capture significant market share in the European packaging sector.

Market Opportunity: China GB 4806.10-2025 Standard Driving High-Purity and Low-Migration Additive Demand in Food Packaging

China’s updated regulatory framework for food contact materials is creating a major opportunity for high-purity packaging coating additives. The GB 4806.10-2025 standard, in conjunction with the revised GB 9685 additive list, introduces stricter requirements for migration limits, chemical purity, and safety in coating systems used for food packaging applications.

With mandatory enforcement scheduled for September 2026, all additives used in coatings must comply with updated testing protocols that emphasize low migration and minimal contamination risk. This is driving demand for macromolecular additive technologies with molecular weights exceeding 1,000 Daltons, which are less likely to migrate into food products. These high-molecular-weight systems provide functional performance while meeting stringent safety thresholds.

The regulation also imposes tighter limits on heavy metals and volatile substances, favoring high-purity synthetic additives over conventional materials that may contain trace contaminants. This shift is encouraging manufacturers to adopt cleaner production processes and invest in advanced material purification technologies to meet regulatory requirements.

A notable expansion within the standard is the inclusion of paper-based coating systems, reflecting the growing importance of coated paper packaging in China’s food and beverage sector. This creates a new market segment for hybrid mineral-organic additives designed for paper coatings, particularly in applications such as paper cans and sustainable packaging formats. The combination of regulatory enforcement, market scale, and material innovation is positioning China as a key growth hub for advanced packaging coating additives.

Packaging Coating Additives Market Share and Segmentation Insights

The packaging coating additives market by function is led by oxygen and moisture barrier enhancers, accounting for 22.4% of the global market share in 2025, due to their critical role in extending product shelf life and maintaining food quality. These additives—such as nanoclays, EVOH blends, and specialty waxes—significantly reduce oxygen (O₂) and water vapor (H₂O) transmission rates, preventing spoilage and preserving freshness in flexible food packaging applications. A major growth driver is the shift toward sustainable packaging solutions, where manufacturers are replacing multi-layer laminates with mono-material recyclable films. In such structures, barrier additives become essential to replicate the performance of traditional materials like aluminum foil. As global demand rises for high-performance, recyclable packaging coatings, barrier enhancers remain the most critical functional segment.

Food Contact Grade Holds 58.3% Share Driven by Strict Global Standards and High Packaging Volumes

In the packaging coating additives market by grade, food contact grade additives dominate with a 58.3% market share in 2025, reflecting the massive scale and regulatory complexity of the food and beverage packaging industry. These additives must comply with stringent global standards such as FDA 21 CFR, EU Regulation EC 10/2011, and China GB 9685, ensuring they meet specific migration limits and safety thresholds for direct food contact. The dominance of this segment is further driven by increasing consumer awareness and brand accountability, with manufacturers prioritizing non-toxic, low-odor, and non-migrating additive formulations to avoid contamination risks and product recalls. As packaging innovation accelerates alongside food safety regulations and sustainability goals, food contact grade additives continue to lead the global packaging coatings additives market.

Competitive Landscape of the Packaging Coating Additives Market

Evonik Leads Packaging Additives Innovation with Siloxane Chemistry and PFAS-Free Solutions

Evonik Industries AG continues to dominate the specialty coating additives market, particularly in siloxane-based defoamers and foam-control technologies for packaging applications. In 2026, the company optimized its North American distribution network by partnering with specialized distributors, enhancing technical support for its Custom Solutions segment. Its TEGO® Foamex 8420, a siloxane-based defoamer, addresses foam stabilization challenges in waterborne overprint varnishes and low-VOC inks, improving process efficiency. Evonik is also a leader in radiation-curable additives, offering advanced wetting agents for non-porous substrates like plastics and metals. With €5.4 billion generated from its Custom Solutions segment, the company is investing heavily in PFAS-free packaging additives.

BASF Expands Bio-Based Additives Portfolio to Support Sustainable Packaging Solutions

BASF SE is a key innovator in the packaging coating additives market, leveraging its backward integration and strong presence in APAC. In 2026, the company expanded its dispersions production capacity in India to meet rising demand in the packaging sector. Its Basonal® PLUS series, introduced at Chinaplas 2026, incorporates bio-circular feedstock to reduce product carbon footprint and support sustainability goals. BASF has also transitioned its Rheovis® range to bio-based Ethyl Acrylate, aligning with global environmental standards. Its HALS and NOR® HALS additives remain industry benchmarks for UV stabilization in plastic packaging, reinforcing its leadership in high-performance and eco-friendly coating additives.

BYK Drives Premium Packaging Additives with Advanced Rheology and Nano Surface Technologies

BYK-Chemie, part of the Altana Group, is a technological leader in rheology modifiers and nano-enabled coating additives, particularly for premium packaging applications. Holding a 35.5% share in the acrylic-based additive segment, the company is focusing on water-based formulations, which account for 40% of global demand. BYK is leveraging high-throughput screening technologies to accelerate the development of VOC-free wetting and dispersing additives that prevent pigment flocculation. Its recent innovations include wax-free slip and rub additives, delivering soft-touch finishes and high scratch resistance for luxury packaging. BYK’s expertise in additive-resin compatibility ensures enhanced adhesion and multi-layer barrier performance.

Arkema Strengthens Bio-Based Additives Leadership with Advanced Polymer and Circular Materials

Arkema is positioning itself as a leader in bio-based packaging coating additives, focusing on high-performance polymers and sustainable material solutions. In 2026, the company introduced Tippox™ 2028, a thermal stabilizer designed to reduce defects and VOC emissions during polymer processing. Its new Singapore facility for Rilsan® Clear polyamides enhances its capacity to deliver BPA-free transparent materials for food packaging. Arkema’s Luperox® organic peroxides continue to lead the market for initiators used in barrier coatings. Additionally, its collaboration with European research institutes aims to scale advanced bio-based circular materials, targeting a 30% increase in recycled content in packaging additives by 2028.

Clariant Focuses on Safety-Driven Additives for Industrial and Electronic Packaging

Clariant AG is a key player in the specialty packaging additives market, focusing on safety, flame retardancy, and antistatic performance. In 2026, the company positioned its Exolit® and Hostastat® product lines as industry benchmarks for halogen-free and environmentally compliant additives. Following the integration of Lucas Meyer Cosmetics, Clariant is expanding into high-end personal care packaging with advanced additive technologies. Its strategic focus on replacing legacy surfactants with APEO-free solutions ensures compliance with stringent environmental regulations. Clariant also excels in antistatic additives for electronic packaging, providing critical ESD protection for semiconductor and next-generation 6G infrastructure applications.

United States Packaging Coating Additives Market: Regulatory-Driven Transformation and PFAS-Free Innovation

The United States packaging coating additives market is evolving as a global benchmark for low-VOC and PFAS-free coating additive innovation, driven by stringent environmental regulations and strong industrial demand. Regulatory frameworks such as California’s Rule 1113, which caps VOC levels at 50 g/L, are accelerating the transition toward waterborne rheology modifiers and eco-friendly coating additives. Additionally, the EPA’s scrutiny on PFAS chemicals has intensified R&D efforts to develop silicone-based dispersions and bio-wax additives that replicate the barrier and slip properties of traditional fluorochemicals in food packaging.

Market dynamics are further supported by large-scale infrastructure investments under the Infrastructure Investment and Jobs Act, creating robust demand for anti-block additives and scuff-resistant coating solutions used in industrial packaging. The rapid growth of e-commerce cold-chain logistics, especially in pharmaceutical delivery, has driven increased adoption of anti-fog agents and antimicrobial coating additives to ensure product clarity and hygiene. Strategic collaborations, such as partnerships between Dow and Procter & Gamble, are advancing dissolution-enabled recycling technologies, enabling easier removal of coatings during recycling. Furthermore, the demand for high-purity acrylic additives in medical blister packaging highlights the country’s focus on high-performance, sterile packaging solutions.

China Packaging Coating Additives Market: Global Manufacturing Powerhouse and Capacity Expansion Hub

China continues to dominate the global packaging coating additives market as the largest production hub, supported by extensive capacity expansion and technological advancements. The establishment of advanced production facilities, such as Wacker Chemie’s specialty silicones complex in Zhangjiagang, is strengthening China’s capability to produce high-performance silicone emulsions and coating additives for packaging applications. Similarly, investments by companies like Evonik and BASF in Nanjing are expanding production of amine-based curing agents and CFRP dispersants, essential for epoxy coatings and high-end packaging solutions.

China’s export strength is evident with a 27.72% year-on-year increase in coating exports, reinforcing its role as a global supplier of cost-effective wetting, leveling, and dispersing agents. The country’s industrial ecosystem, particularly in the Pearl River Delta, is driving demand for rheology modifiers and specialty additives. Additionally, innovation in multifunctional light stabilizers is enhancing UV resistance in plastic packaging films, improving durability in global markets. These developments position China as both a volume leader and an innovation hub in packaging coating additives.

Germany is at the forefront of the European packaging coating additives market, driven by strict regulatory frameworks such as the VerpackG (German Packaging Act) and EU PPWR regulations. The 2025 amendments to VerpackG, requiring PET bottles to include at least 25% recycled content, are boosting demand for compatibilizers and recycling-friendly coating additives. The implementation of the LUCID Registry’s modulated fee system incentivizes manufacturers to adopt design-for-recycling solutions, including water-soluble adhesives and non-migratory coatings.

Technological innovation is centered around optical sorting-enabled additives, allowing packaging materials to be identified and separated with up to 99% accuracy, significantly improving recycling efficiency. Germany is also witnessing a strong shift toward bio-based additives derived from lignin and starch, replacing conventional petroleum-based surfactants. Investments in oxygen barrier additives are enabling mono-material packaging to match the performance of multi-layer systems, supporting sustainability goals. Additionally, the adoption of 100% solids UV-curable additives aligns with EU Green Deal objectives by eliminating VOC emissions entirely, reinforcing Germany’s leadership in sustainable packaging solutions.

India Packaging Coating Additives Market: E-commerce Expansion and Infrastructure-Led Growth

India is emerging as one of the fastest-growing markets for packaging coating additives, driven by rapid urbanization, e-commerce growth, and strong government initiatives under “Make in India.” Investments such as Kansai Nerolac’s INR 150 crore expansion in Maharashtra are enhancing domestic production of high-speed coating additives for packaging applications.

The rise of quick-commerce and last-mile delivery models has created strong demand for moisture-resistant coating additives for corrugated boxes and paper packaging. The market is also witnessing a shift toward waterborne coating additives, particularly in the food and beverage sector, as sustainability becomes a priority. Infrastructure growth in pharmaceuticals is increasing the demand for high-purity slip agents and anti-static additives for cleanroom-compatible packaging. Additionally, local innovation in natural antimicrobial coatings derived from neem and citrus extracts is gaining traction for extending the shelf life of perishable goods. With regions like Delhi/NCR accounting for over 35% of market activity, India continues to strengthen its position as a high-growth hub.

Japan Packaging Coating Additives Market: Smart Packaging and High-Precision Additive Innovation

Japan’s packaging coating additives market is defined by advanced material science and smart packaging technologies, particularly in high-value applications. Strategic collaborations such as the partnership between Sakata INX and INX International are strengthening Japan’s presence in sustainable coating additives across Asia.

The country leads in the development of oxygen-scavenging additives, which extend the shelf life of ready-to-eat food without preservatives by actively removing oxygen from packaging. Innovations in nanocellulose-based additives are providing superior gas barrier properties while maintaining biodegradability. Japan is also advancing ultra-fast UV-LED curing additives, improving energy efficiency and productivity in high-speed coating processes. Regulatory frameworks such as the Positive List System for food-contact materials ensure ultra-low migration, pushing manufacturers toward safer, high-performance additive solutions. These factors reinforce Japan’s leadership in precision and functional packaging coatings.

Brazil Packaging Coating Additives Market: Bio-Based Innovation and Agribusiness Packaging Leadership

Brazil is emerging as a key market for sustainable packaging coating additives, leveraging its strong agricultural base and bio-resource availability. Investments in sugarcane-based polyethylene additives are supporting the development of “Green PE” films used in export-grade food packaging, particularly in the meat industry.

The country is also a global leader in barrier coating additives for agrochemical packaging, ensuring durability and preventing chemical leakage under harsh tropical conditions. Growth in the pulp and paper industry is driving demand for functional coating additives that enable paperboard to replace single-use plastics in retail packaging. Additionally, the use of carnauba wax-based bio-wax dispersions is reducing reliance on imported paraffin waxes. Infrastructure upgrades in port logistics are further increasing demand for UV-stabilized coatings for transport packaging. Regulatory alignment with ESG standards is accelerating the adoption of high-solids and waterborne technologies, reinforcing Brazil’s position in sustainable packaging innovation.

South Korea Packaging Coating Additives Market: Electronics-Driven Demand and High-Performance Additive Innovation

South Korea’s packaging coating additives market is heavily influenced by its leadership in electronics, semiconductors, and high-value exports. There is strong demand for anti-static (ESD) and EMI-shielding additives, essential for protecting sensitive electronic components during transportation.

Technological advancements include the use of AI-driven predictive modeling tools, enabling faster development of barrier coatings and reducing product development cycles by up to 30%. South Korea is also a leader in high-barrier retort pouch coatings, utilizing advanced adhesion promoters that maintain performance under high-temperature sterilization. Government initiatives promoting eco-label certifications are encouraging the adoption of bio-based curing agents and solvent-free additives, aligning with sustainability goals. Additionally, the influence of the K-Beauty industry is driving demand for premium sensory-effect additives, such as soft-touch and pearlescent coatings, enhancing the appeal of cosmetic packaging.

Packaging Coating Additives Market Report Scope

Packaging Coating Additives Market

Parameter

Details

Market Size (2025)

$1450.3 Million

Market Size (2032)

$2109.7 Million

Market Growth Rate

5.5%

Segments

By Function (Slip and Anti-Slip Additives, Anti-Block Additives, Antimicrobial Additives, Anti-Static Additives, Anti-Fog Additives, Antioxidants and UV Stabilizers, Defoamers and Deaerators, Surface Modifiers, Wetting and Dispersing Agents, Oxygen and Moisture Barrier Enhancers), By Product (Waxes, Silicones, Metallic Oxides and Minerals, Polymers and Resins, Surfactants and Fatty Acid Derivatives, Bio-based), By Formulation Technology (Water-borne, Solvent-borne, Powder-based, Radiation-Cured), By End-Use Industry (Food and Beverage Packaging, Healthcare and Pharmaceutical Packaging, Cosmetics and Personal Care Packaging, Industrial and Household Packaging, Consumer Electronics Packaging), By Packaging Format (Flexible Packaging, Rigid Packaging, Secondary and Tertiary Packaging), By Grade (Food Contact Grade, Industrial Grade, Medical Grade), By Sales Channel (Direct Sales, Specialty Chemical Distributors, Contract Manufacturers and Toll Blenders)

Study Period

2019- 2025 and 2026-2032

Units

Revenue (USD)

Qualitative Analysis

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

Companies

BASF SE, Evonik Industries AG, BYK-Chemie GmbH, Dow Inc., Clariant AG, Arkema S.A., The Lubrizol Corporation, Eastman Chemical Company, Henkel AG and Co. KGaA, Nouryon, Elementis plc, Michelman, Inc., Croda International Plc, Solvay S.A., Ashland Inc.

Countries

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

Packaging Coating Additives Market Segmentation

By Function

Slip and Anti-Slip Additives

Anti-Block Additives

Antimicrobial Additives

Anti-Static Additives

Anti-Fog Additives

Antioxidants and UV Stabilizers

Defoamers and Deaerators

Surface Modifiers

Wetting and Dispersing Agents

Oxygen and Moisture Barrier Enhancers

By Product

Waxes

Silicones

Metallic Oxides and Minerals

Polymers and Resins

Surfactants and Fatty Acid Derivatives

Bio-based

By Formulation Technology

Water-borne

Solvent-borne

Powder-based

Radiation-Cured

By End-Use Industry

Food and Beverage Packaging

Healthcare and Pharmaceutical Packaging

Cosmetics and Personal Care Packaging

Industrial and Household Packaging

Consumer Electronics Packaging

By Packaging Format

Flexible Packaging

Rigid Packaging

Secondary and Tertiary Packaging

By Grade

Food Contact Grade

Industrial Grade

Medical Grade

By Sales Channel

Direct Sales

Specialty Chemical Distributors

Contract Manufacturers and Toll Blenders

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Packaging Coating Additives Industry

BASF SE

Evonik Industries AG

BYK-Chemie GmbH

Dow Inc.

Clariant AG

Arkema S.A.

The Lubrizol Corporation

Eastman Chemical Company

Henkel AG & Co. KGaA

Nouryon

Elementis plc

Michelman, Inc.

Croda International Plc

Solvay S.A.

Ashland Inc.

*- List not Exhaustive

Table of Contents: Packaging Coating Additives Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Packaging Coating Additives Market Landscape and Outlook (2025–2034)

2.1. Introduction to the Packaging Coating Additives Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Market Drivers

2.4. Market Restraints and Challenges

2.5. Market Opportunities

2.6. Regulatory and Sustainability Landscape

2.7. Value Chain Analysis

2.8. Pricing Analysis

2.9. Technology Roadmap and Future Outlook

3. Innovations Reshaping the Packaging Coating Additives Market

3.1. Trend: Non-Fluorinated Slip Additives Transforming PFAS-Free Metal Packaging Coatings

3.2. Trend: Oxygen Scavenging Additives Enhancing Shelf Life and Food Preservation in Metal Packaging

3.3. Opportunity: EU Packaging and Packaging Waste Regulation Driving Demand for Recyclability-Compatible Additives

3.4. Opportunity: China GB 4806.10-2025 Standard Driving High-Purity and Low-Migration Additive Demand in Food Packaging

4. Competitive Landscape and Strategic Initiatives

4.1. Mergers and Acquisitions

4.2. RandD and Product Innovation

4.3. Sustainability and ESG Strategies

4.4. Capacity Expansion and Geographic Expansion

5. Market Share and Segmentation Insights: Packaging Coating Additives Market

5.1. By Function

5.1.1. Slip and Anti-Slip Additives

5.1.2. Anti-Block Additives

5.1.3. Antimicrobial Additives

5.1.4. Anti-Static Additives

5.1.5. Anti-Fog Additives

5.1.6. Antioxidants and UV Stabilizers

5.1.7. Defoamers and Deaerators

5.1.8. Surface Modifiers

5.1.9. Wetting and Dispersing Agents

5.1.10. Oxygen and Moisture Barrier Enhancers

5.2. By Product

5.2.1. Waxes

5.2.2. Silicones

5.2.3. Metallic Oxides and Minerals

5.2.4. Polymers and Resins

5.2.5. Surfactants and Fatty Acid Derivatives

5.2.6. Bio-based

5.3. By Formulation Technology

5.3.1. Water-borne

5.3.2. Solvent-borne

5.3.3. Powder-based

5.3.4. Radiation-Cured

5.4. By End-Use Industry

5.4.1. Food and Beverage Packaging

5.4.2. Healthcare and Pharmaceutical Packaging

5.4.3. Cosmetics and Personal Care Packaging

5.4.4. Industrial and Household Packaging

5.4.5. Consumer Electronics Packaging

5.5. By Packaging Format

5.5.1. Flexible Packaging

5.5.2. Rigid Packaging

5.5.3. Secondary and Tertiary Packaging

5.6. By Grade

5.6.1. Food Contact Grade

5.6.2. Industrial Grade

5.6.3. Medical Grade

5.7. By Sales Channel

5.7.1. Direct Sales

5.7.2. Specialty Chemical Distributors

5.7.3. Contract Manufacturers and Toll Blenders

6. Country Analysis and Outlook of Packaging Coating Additives Market

6.1. United States

6.2. Canada

6.3. Mexico

6.4. Germany

6.5. France

6.6. Spain

6.7. Italy

6.8. United Kingdom

6.9. Russia

6.10. China

6.11. India

6.12. Japan

6.13. South Korea

6.14. Australia

6.15. South East Asia

6.16. Brazil

6.17. Argentina

6.18. Saudi Arabia

6.19. UAE

6.20. Middle East and Africa

7. Packaging Coating Additives Market Size Outlook by Region (2025–2034)

7.1. North America Packaging Coating Additives Market Size Outlook to 2034

7.1.1. By Function

7.1.2. By Product

7.1.3. By Formulation Technology

7.1.4. By End-Use Industry

7.1.5. By Packaging Format

7.1.6. By Grade

7.1.7. By Sales Channel

7.2. Europe Packaging Coating Additives Market Size Outlook to 2034

7.2.1. By Function

7.2.2. By Product

7.2.3. By Formulation Technology

7.2.4. By End-Use Industry

7.2.5. By Packaging Format

7.2.6. By Grade

7.2.7. By Sales Channel

7.3. Asia Pacific Packaging Coating Additives Market Size Outlook to 2034

7.3.1. By Function

7.3.2. By Product

7.3.3. By Formulation Technology

7.3.4. By End-Use Industry

7.3.5. By Packaging Format

7.3.6. By Grade

7.3.7. By Sales Channel

7.4. South and Central America Packaging Coating Additives Market Size Outlook to 2034

7.4.1. By Function

7.4.2. By Product

7.4.3. By Formulation Technology

7.4.4. By End-Use Industry

7.4.5. By Packaging Format

7.4.6. By Grade

7.4.7. By Sales Channel

7.5. Middle East and Africa Packaging Coating Additives Market Size Outlook to 2034

7.5.1. By Function

7.5.2. By Product

7.5.3. By Formulation Technology

7.5.4. By End-Use Industry

7.5.5. By Packaging Format

7.5.6. By Grade

7.5.7. By Sales Channel

8. Company Profiles: Leading Players in the Packaging Coating Additives Market

8.1. BASF SE

8.2. Evonik Industries AG

8.3. BYK-Chemie GmbH

8.4. Dow Inc.

8.5. Clariant AG

8.6. Arkema S.A.

8.7. The Lubrizol Corporation

8.8. Eastman Chemical Company

8.9. Henkel AG and Co. KGaA

8.10. Nouryon

8.11. Elementis plc

8.12. Michelman, Inc.

8.13. Croda International Plc

8.14. Solvay S.A.

8.15. Ashland Inc.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures

Packaging Coating Additives Market Segmentation

By Function

Slip and Anti-Slip Additives

Anti-Block Additives

Antimicrobial Additives

Anti-Static Additives

Anti-Fog Additives

Antioxidants and UV Stabilizers

Defoamers and Deaerators

Surface Modifiers

Wetting and Dispersing Agents

Oxygen and Moisture Barrier Enhancers

By Product

Waxes

Silicones

Metallic Oxides and Minerals

Polymers and Resins

Surfactants and Fatty Acid Derivatives

Bio-based

By Formulation Technology

Water-borne

Solvent-borne

Powder-based

Radiation-Cured

By End-Use Industry

Food and Beverage Packaging

Healthcare and Pharmaceutical Packaging

Cosmetics and Personal Care Packaging

Industrial and Household Packaging

Consumer Electronics Packaging

By Packaging Format

Flexible Packaging

Rigid Packaging

Secondary and Tertiary Packaging

By Grade

Food Contact Grade

Industrial Grade

Medical Grade

By Sales Channel

Direct Sales

Specialty Chemical Distributors

Contract Manufacturers and Toll Blenders

Leading Countries in the Industry

North America (United States, Canada, Mexico)

Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

South and Central America (Brazil, Argentina, Rest of SCA)

Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

The global packaging coating additives market was valued at $1,450.3 million in 2025 and is projected to reach $2,109.7 million by 2032, expanding at a CAGR of 5.5%. Market growth is being driven by rising demand for PFAS-free additives, oxygen and moisture barrier enhancers, wetting and dispersing agents, anti-block additives, and waterborne-compatible coating technologies across food, beverage, pharmaceutical, industrial, and consumer packaging applications.

Packaging manufacturers are accelerating the transition toward non-fluorinated slip additives due to tightening PFAS regulations and sustainability commitments from global consumer brands. Silicone-based and wax-based additives are increasingly replacing fluorinated systems because they deliver comparable slip performance, mar resistance, and surface smoothness without regulatory risk. Silicone-based technologies are expected to account for nearly 39% of the slip additive segment by late 2026, particularly in waterborne packaging coating systems requiring high compatibility and low migration performance.

Oxygen scavenging additives are becoming critical components in advanced food packaging systems because they reduce internal oxygen levels below 0.1%, significantly slowing oxidative degradation in packaged foods. These additives can extend shelf life by 25% to 40% for oxygen-sensitive products while improving nutritional retention and minimizing the need for chemical preservatives. Their integration into internal metal and flexible packaging coatings is supporting the growth of active packaging technologies focused on food quality preservation and waste reduction.

Asia-Pacific dominates the market due to rapid expansion of food packaging, e-commerce logistics, and flexible packaging production in China and India, while Europe leads in recyclable packaging regulations and PFAS-free innovation. Strong growth opportunities are emerging in mono-material recyclable packaging, pharmaceutical blister packaging, cold-chain logistics, premium cosmetic packaging, beverage cans, and paper-based sustainable packaging systems requiring advanced functional additives.

Major companies operating in the packaging coating additives industry include BASF SE, Evonik Industries AG, BYK-Chemie GmbH, Dow Inc., Clariant AG, Arkema S.A., The Lubrizol Corporation, and Michelman, Inc.. These companies are investing heavily in PFAS-free additive technologies, oxygen barrier systems, bio-based coating additives, recyclable packaging solutions, waterborne-compatible chemistries, and advanced functional surface modifiers to strengthen their global market positions.