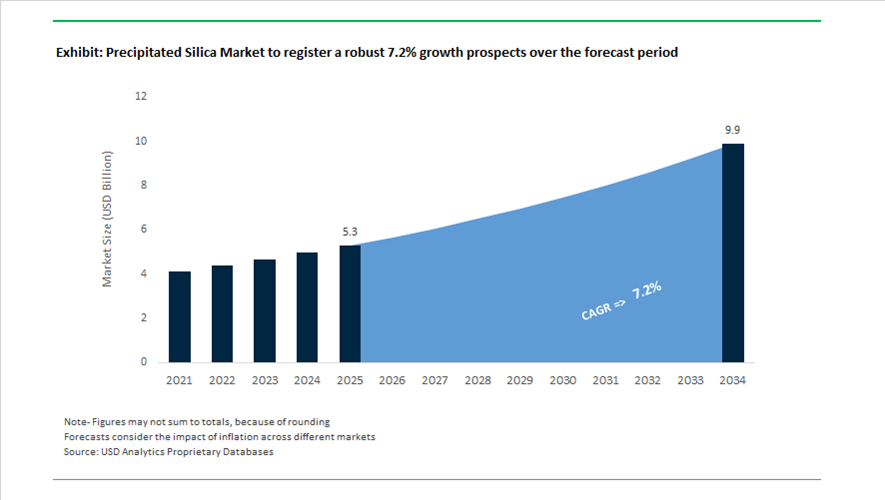

Precipitated Silica Market Valued at $5.3 Billion in 2025, Projected to Reach $9.9 Billion by 2034 at 7.2% CAGR

The global precipitated silica market is valued at $5.3 billion in 2025 and is forecast to reach $9.9 billion by 2034, expanding at a strong CAGR of 7.2%. Growth is being driven by accelerating demand for highly dispersible silica (HDS), green tire silica, circular silica grades, bio-based silica from rice husk ash, and EV tire reinforcement materials. The tire industry remains the largest consumer, particularly for low rolling resistance compounds required in electric vehicles and fuel-efficient SUVs. Additional demand is emerging from personal care, food additives, and specialty rubber applications where purity, surface area control, and dispersibility are critical performance parameters.

Strategic portfolio realignments began in early 2024 when Evonik and Vland Biotech dissolved their joint venture, allowing Evonik to intensify focus on its Smart Materials division, including its global precipitated silica operations. In late 2024, Solvay launched circular silica production at its Livorno, Italy site using rice husk ash as a renewable silicate feedstock, reducing carbon emissions by up to 50% compared to conventional processes. During 2024 and into 2025, Evonik introduced ULTRASIL® 7800 GR, a highly dispersible silica engineered for large SUV and EV tires. The grade addresses higher load-bearing stress associated with EV battery weight while preserving rolling resistance performance. In October 2024, Evonik broke ground on a major expansion of its Charleston, South Carolina facility, designed to increase site capacity by 50% to meet rising North American demand for sustainable tire silica.

Capacity expansion and circularity strategies intensified in 2025. In January 2025, Solvay announced a significant expansion at its Gunsan, South Korea plant dedicated to HDS production for the Asia-Pacific tire and personal care sectors. In late 2024, Solvay began replacing its legacy Zeosil® range with circular “drop-in” alternatives, allowing tire manufacturers to incorporate sustainable silica without modifying existing rubber formulations. In 2025, Solvay further advanced its circular roadmap by confirming that its Qingdao, China and Gunsan, South Korea plants would transition to ISCC+ certified waste sand feedstock beginning in 2026. This initiative enables over half of its regional HDS output to qualify as circular silica.

Industry consolidation reshaped competitive dynamics entering 2026. In February 2026, PPG Industries finalized the $310 million sale of its silica products business to Qemetica S.A., formerly CIECH Group. The transaction strengthens Qemetica’s manufacturing footprint in North America while allowing PPG to concentrate on its core coatings portfolio. Following the 2024 groundbreaking, Evonik confirmed that its expanded Charleston production line is scheduled to begin full operations in early 2026, reinforcing the site’s position as a central hub for green tire silica production in the United States.

The precipitated silica market is increasingly defined by highly dispersible silica for EV and SUV tires, bio-based rice husk ash silica, ISCC+ certified circular feedstocks, drop-in sustainable Zeosil® replacements, 50% capacity expansions in North America, and Asia-Pacific HDS scale-up investments. Tire electrification, decarbonization targets, and supply chain localization are driving sustained demand for advanced precipitated silica grades across global automotive and industrial rubber markets.

Strategic Trends and Growth Opportunities in the Precipitated Silica Market

Strategic Pivot to High-Purity Silica for Silicon-Dominant Battery Anodes

The rapid shift toward higher energy-density lithium-ion batteries is fundamentally redefining the role of precipitated silica within the battery materials value chain. As EV manufacturers push silicon-dominant anodes to overcome the theoretical capacity ceiling of graphite, precipitated silica has emerged as a critical stabilizing agent. Its function extends beyond passive filler use, acting as a thermal, mechanical, and interfacial stabilizer that mitigates silicon’s volumetric expansion during lithiation and delithiation cycles. This capability directly improves cycle life, coulombic efficiency, and safety, making high-purity silica a strategic input rather than a commodity additive.

Capacity investments underscore this transition. In March 2024, Evonik Industries announced a 50% expansion of its precipitated silica capacity at its Charleston, South Carolina facility, explicitly targeting North America’s rapidly scaling battery ecosystem. The expansion supports growing demand for Siridion® Black, a silica-based anode additive engineered to improve oxidation resistance and structural integrity in next-generation lithium-ion cells. This move reflects a broader industry pattern where silica producers are ringfencing dedicated production lines for battery-grade material with tightly controlled particle morphology and impurity profiles.

Performance validation is reinforcing this demand shift. In May 2025, collaborative development disclosures from BASF and Group14 Technologies highlighted silicon anode systems stabilized with advanced binders and silica-modified carbons. Reported test data showed batteries retaining roughly 80% of capacity after 1,000 cycles at room temperature, while delivering close to four times the capacity of conventional graphite-based cells. Importantly, stable performance was also demonstrated at elevated temperatures around 45°C, underscoring silica’s role in managing thermal and mechanical stress in real-world EV operating conditions.

Vertical Integration and Bio-Circular Sourcing in Green Tire Manufacturing

Parallel to battery-driven demand, the tire industry is reshaping the precipitated silica market through aggressive sustainability mandates. Global tire manufacturers have publicly committed to achieving 30% to 50% sustainable material content by 2030, forcing silica suppliers to rethink raw material sourcing and production pathways. The industry is moving away from conventional sand-derived sodium silicate toward agricultural waste streams such as rice husk ash, enabling substantial reductions in Scope 3 emissions.

A defining milestone occurred in October 2025 when Solvay inaugurated Europe’s first industrial-scale bio-circular Highly Dispersible Silica unit at its Livorno site in Italy. The facility utilizes sodium silicate derived from rice husk ash, delivering an estimated 35% reduction in CO₂ emissions per ton of silica produced. Strategic downstream partners, including Continental Tires, have already incorporated this bio-circular HDS into long-term circularity roadmaps aimed at achieving 100% sustainable materials by 2050.

Decarbonization efforts are extending beyond feedstock substitution. To support the fuel-efficiency targets of the roughly 1.5 billion tires produced globally each year, silica manufacturers are investing in electric furnaces and low-emission precipitation technologies. Solvay’s announced transition of its Qingdao and Gunsan plants toward circular production by 2026 illustrates how vertical integration, energy efficiency, and sustainable sourcing are converging to redefine competitive advantage in the green tire silica segment.

High-Performance Carriers for Food and Pharmaceutical Excipients

Outside automotive and energy storage, the pharmaceutical and nutraceutical sectors are emerging as structurally attractive growth avenues for precipitated silica producers. These industries require carriers with consistent porosity, ultra-low metallic impurities, and compliance with global pharmacopeia standards such as USP-NF and Ph. Eur. As formulation complexity increases, silica’s role has expanded from basic anti-caking to active performance enabler in drug delivery and nutritional systems.

In December 2025, PPG Industries achieved REDCert² sustainable raw material certification at two of its European silica facilities. This certification enables the supply of FLO-GARD™ precipitated silica with verifiable sustainability credentials into food, feed, and supplement applications. In these markets, silica’s high oil-absorption capacity is critical for stabilizing essential oils, flavors, and fat-soluble vitamins in powdered formats, while meeting increasingly stringent sustainability disclosure requirements.

From a formulation perspective, controlled porosity and particle size distribution are enabling silica to function as a viscosity modifier and release-control agent in liquid and solid dosage forms. Pharmaceutical manufacturers are leveraging these properties to achieve precise dissolution and release profiles in advanced tableting and suspension systems, where impurity thresholds below 10 ppm are often mandatory. This combination of regulatory complexity and performance sensitivity supports premium pricing and long-term supplier relationships.

Functional Surface-Modified Silica for Advanced Coatings and Adhesives

A second high-value opportunity lies in surface-modified precipitated silica for advanced coatings and adhesive systems. Aerospace, automotive, marine, and renewable energy applications increasingly require additives that deliver rheological control, scratch resistance, and fatigue durability without compromising transparency or low-VOC compliance.

Research disseminated during 2024 and 2025 has highlighted nanosilica-toughened epoxy systems as a strategic growth niche. Surface-functionalized silica nanoparticles have been shown to significantly improve fatigue resistance and crack propagation behavior in fiber-reinforced composites used in satellites, space vehicles, and high-load wind turbine blades. These performance gains position precipitated silica as a structural reinforcement rather than a simple rheology aid.

Commercial traction is already visible. In April 2024, Evonik Industries launched new TEGO® Foamex and silica-based additives tailored for architectural and industrial coatings. These surface-modified silicas enable low-VOC formulations to maintain mechanical durability, matting efficiency, and sag resistance, aligning with the EU’s 2025 sustainability requirements for architectural, marine, and protective coatings.

Precipitated Silica Market Share and Segmentation Insights

Rubber Grade Precipitated Silica Leads Reinforcement Materials for High-Performance Tire Manufacturing

Rubber grade precipitated silica accounted for 58.60% of the Precipitated Silica Market by grade in 2025, supported by its critical role as a reinforcing filler in modern tire compounds. Silica reinforcement technology has become standard in green tire manufacturing where silica silane systems reduce rolling resistance, improve wet traction, and enhance tire durability compared with conventional carbon black formulations. The global scale of tire manufacturing and replacement tire demand continues to drive strong consumption of high dispersibility silica grades. In 2025, tightening global fuel efficiency standards have strengthened demand for silica reinforced tire compounds, encouraging tire manufacturers to adopt advanced silica grades that deliver improved fuel economy performance while maintaining tire safety and longevity.

Automotive and Tire Manufacturing Sector Drives Precipitated Silica Demand

Automotive and tire applications represented 52.80% of the Precipitated Silica Market by application in 2025, reflecting the large volume of silica used in passenger vehicle, commercial vehicle, and specialty tire production. Each tire contains several kilograms of precipitated silica in tread formulations designed to balance traction, rolling resistance, and wear performance. The scale of the global vehicle fleet and steady replacement tire demand continue to support long term consumption of silica reinforcing fillers. In 2025, electric vehicle tire development has increased demand for specialized silica grades, as EV tires require enhanced durability, improved rolling efficiency, and resistance to higher torque loads generated by electric drivetrains.

Precipitated Silica Market Competitive Landscape

The global precipitated silica market in 2026 is defined by circular raw materials, Highly Dispersible Silica (HDS) innovation, and asset consolidation into mega-scale production hubs. Leading players are prioritizing low-carbon silica, EV tire performance, and localized supply chains to comply with ESPR regulations and sustainability mandates.

Evonik Strengthens Market Leadership Through Smart Effects Integration and Capacity Expansion

Evonik is reinforcing its leadership in the precipitated silica market through its “Smart Effects” strategy, integrating silica and silanes to deliver high-performance solutions for green tires and EV applications. The company is optimizing its global asset network by closing smaller facilities in Waterford and Havre de Grace, consolidating production into cost-efficient mega-hubs. Its Charleston expansion will increase ULTRASIL® silica capacity by 50%, directly addressing North America’s demand for fuel-efficient tire materials. Financially, Evonik reported €14.1 billion in sales and €1.9 billion EBITDA in 2025, reflecting strong specialty chemicals performance. The company is also advancing circular silica technologies using sustainable raw materials to reduce carbon footprint. This strategic alignment with SBTi and green mobility trends positions Evonik as a dominant innovator in high-dispersibility silica.

Solvay Leads Bio-Circular Silica Revolution with Rice Husk Ash and Waste Sand Integration

Solvay is emerging as the global benchmark in bio-circular precipitated silica, transitioning its production base toward renewable and recycled feedstocks. Its Livorno facility, inaugurated in 2026, is Europe’s first to produce HDS from rice husk ash, reducing CO2 emissions by 35% per ton. In Asia, Solvay is converting its Qingdao and Gunsan plants to ISCC+ certified waste sand, enabling over 50% circular production capacity. The company’s Zeosil® portfolio allows tire manufacturers to achieve up to 15% renewable content without reformulation. Strategic collaboration with Hankook Tire strengthens its position in sustainable tire supply chains. Solvay’s circular silica leadership directly supports the global push toward 40% sustainable materials in tire manufacturing by 2030.

PPG Advances High-Reinforcement Silica for EV Tires and Battery Separators

PPG Industries is leveraging its specialty materials expertise to deliver high-performance precipitated silica solutions for automotive and energy storage applications. Its Agilon® technology integrates silica and silane, reducing mixing stages and improving EV tire rolling resistance by up to 20%. The company is expanding its footprint in Asia-Pacific, targeting high-growth markets in battery separators and specialty rubber. PPG’s silica solutions offer high porosity and mechanical strength, critical for lithium-ion battery safety and thermal stability. Beyond tires, it provides advanced matting agents and anti-corrosive coatings with superior dispersibility. This diversified application portfolio positions PPG as a key enabler of energy-efficient mobility and advanced materials engineering.

Tata Chemicals Expands Capacity with Backward Integration for Cost-Efficient Silica Production

Tata Chemicals is scaling its precipitated silica production to capitalize on India’s automotive and industrial growth under the “Make in India” initiative. Its $93 million investment in the Cuddalore facility enhances capacity for high-quality silica used in tires and footwear. The company benefits from backward integration into soda ash and sodium silicate, ensuring cost competitiveness and supply stability. Its TAVERSIL® portfolio supports both conventional and highly dispersible silica applications in domestic and export markets. Tata is also exploring green soda ash production to reduce carbon intensity and meet global sustainability benchmarks. This integrated, cost-efficient model strengthens its position as a key supplier in emerging markets.

Madhu Silica Expands Specialty Portfolio with Focus on FMCG, Pharma, and Rubber Applications

Madhu Silica is a leading Indian manufacturer with a diversified portfolio of over 50 precipitated silica grades across multiple industries. The company reported revenues of ₹1,820 crore (~$215 million) in 2025, supported by strong export demand and a workforce exceeding 2,100 employees. Its silica products are widely used in oral care, food additives, and rubber reinforcement, making it a key supplier to global FMCG companies. Its Bhavnagar R&D center is driving innovation in dust-free micro-pearl silica to enhance processing efficiency. The company is also expanding into agrochemicals and pharmaceuticals, offering high-absorbency carriers for controlled-release applications. This diversification strategy enhances its resilience and global competitiveness.

W.R. Grace Focuses on High-Purity Specialty Silica for Pharma and Advanced Industrial Applications

W.R. Grace is strategically shifting toward high-value synthetic silica solutions, prioritizing precision-engineered materials over commodity volumes. Its PERKASIL® range delivers superior abrasion resistance for technical rubber applications such as footwear and transmission belts. Grace is leveraging its catalyst expertise to develop advanced silica carriers and adsorbents, including Chlorocel™ for industrial purification processes. The company is also advancing encapsulation technologies for pharmaceuticals and biofuels, aligning with high-growth specialty markets. Its USP-grade silica remains critical for nutraceutical formulations as a glidant and carrier. This focus on high-purity, application-specific silica positions Grace as a niche leader in advanced materials.

United States: Capacity Onshoring, EV Architectures, and Performance-Driven Substitution

The United States precipitated silica market is entering a structural expansion phase driven by onshoring, regulatory pull from mobility standards, and downstream performance requirements. In March 2024, Evonik Industries announced a mid-double-digit million euro investment to expand its Charleston, South Carolina facility, lifting precipitated silica capacity by 50% with commissioning targeted for early 2026. This expansion reflects a deliberate shift to localize supply for tire, food, and industrial customers amid Buy American incentives and supply chain risk mitigation. Market consolidation has reinforced this momentum. In August 2024, Qemetica acquired the global silicas business of PPG Industries for $310 million, representing one of the most significant U.S. silica market entries by a Central European producer.

Product strategy is increasingly aligned with electrification and sustainability. In January 2025, Evonik launched its Smart Effects entity, integrating Silica and Silanes to serve 800V EV architectures and green tire platforms requiring highly dispersible silica for improved rolling resistance and abrasion balance. Regulatory signals are reinforcing demand quality. The FDA updated GRAS documentation in late 2025 for silicon dioxide used as an anti-caking agent, tightening expectations around purity and traceability for powdered drink and nutrition formats. Simultaneously, revised 2025 fuel economy standards from the National Highway Traffic Safety Administration have accelerated tire makers’ shift from carbon black to HDS, delivering average rolling resistance reductions of around 20%. Infrastructure spending is adding another layer of demand, as Buy American provisions effective January 2026 favor silica-enhanced, high-durability coatings and sealants for bridges and highways.

India: Capacity Scale-Up, Bio-Based Feedstocks, and Battery-Linked Applications

India’s precipitated silica industry is scaling rapidly on the back of domestic capacity additions, agricultural waste valorization, and emerging energy storage uses. In November 2025, Tata Chemicals announced an investment of ₹7.75 billion to expand capacity at its Cuddalore site by 50,000 tonnes per annum, representing an 86% increase at the location. This expansion strengthens India’s position as a competitive supplier to rubber, footwear, and consumer goods sectors. Regional hubs are also deepening. Aksharchem India commissioned its expanded Dahej facility in June 2025, bringing cumulative capacity to 18,000 tonnes per annum to serve domestic rubber demand.

Feedstock innovation is emerging as a differentiator. In mid-2025, startups including Brisil partnered with national rubber boards to scale rice husk ash-based silica, converting agricultural waste into a bio-based sodium silicate precursor. Downstream pull is diversifying beyond tires. India’s status as the world’s largest motorcycle market has driven demand for abrasive-grade silica in whitening toothpastes, with 2025 audits noting increased use in high-clarity formulations. Policy is catalyzing new applications. The Production Linked Incentive scheme for Advanced Chemistry Cell battery storage is encouraging adoption of precipitated silica as a separator additive to enhance thermal stability, linking silica demand directly to India’s energy transition agenda.

China: Energy Optimization, Green Tires, and Export Compliance Tightening

China remains the largest production and consumption base for precipitated silica, with policy now focused on energy efficiency, low-carbon inputs, and export-grade compliance. In May 2025, the Ministry of Industry and Information Technology mandated that 60% of silica output in Shandong province transition to automated smart kiln technologies by 2027, targeting lower energy intensity and improved process control. Sustainability is moving upstream. In September 2025, Solvay announced that its Qingdao plant will shift to ISCC+ certified waste sand as a feedstock from 2026, aiming to cut carbon footprint per tonne by 50%.

Demand fundamentals remain robust, particularly in mobility. The China Rubber Industry Association reported that tire production is on track to reach 704 million units annually by the end of 2025, with approximately 75% of new passenger radials incorporating silica-based green tire technology. Export discipline is tightening in parallel. Chinese customs introduced stricter purity audits for food-grade silica exports in late 2025 to align with EU organic production rules under Regulation 2025/973, raising the bar for documentation and batch consistency. China’s market profile is therefore characterized by scale, efficiency mandates, and a gradual move toward higher-value, compliant grades.

South Korea: Circular Feedstocks and Semiconductor-Grade Demand

South Korea’s precipitated silica market is shaped by high-performance applications in tires and semiconductors, supported by circular raw material strategies. Solvay confirmed plans to convert its Gunsan facility to circular raw materials by 2026, specifically to serve the high-dispersibility silica requirements of Korean tire OEMs such as Hankook Tire and Kumho Tire. This transition aligns with OEM pressure for lower embedded emissions without compromising tread performance.

Electronics demand is accelerating in parallel. Korean semiconductor manufacturers increased procurement of low-ion precipitated silica for chemical mechanical planarization slurries during 2025–2026, supporting the national semiconductor super-cluster expansion. These CMP applications require stringent control of particle size distribution and ionic impurities, positioning precipitated silica as a critical consumable in advanced node manufacturing.

Poland: Post-Acquisition Consolidation and Battery-Focused R&D

Poland is emerging as a strategic innovation center within Europe’s precipitated silica landscape following cross-border consolidation. After acquiring PPG’s global silicas business, Qemetica announced in late 2025 the establishment of a centralized R&D hub in Poland. The facility is focused on developing specialty silicas for battery separator applications, leveraging the acquired asset base to move up the value chain.

This R&D-centric positioning signals a shift from commodity supply toward functional materials tailored for energy storage, particularly where silica morphology and surface chemistry influence separator porosity and thermal behavior. Poland’s role is therefore evolving from a production node to a technology development anchor within the European silica ecosystem.

Comparative Overview of Country-Level Dynamics in the Precipitated Silica Industry

Precipitated Silica Market County Level Snapshot

|

Country

|

Primary Strategic Drivers

|

Implications for Precipitated Silica

|

|

United States

|

Capacity onshoring, EV standards, infrastructure spend

|

Higher demand for HDS, food-grade, and industrial coatings

|

|

India

|

Capacity expansion, bio-based feedstocks, batteries

|

Rapid volume growth with diversification beyond tires

|

|

China

|

Smart kilns, green tires, export compliance

|

Energy-efficient scale with higher-grade export focus

|

|

South Korea

|

Circular raw materials, semiconductors

|

Premium demand for HDS and low-ion CMP grades

|

|

Poland

|

Post-M&A consolidation, battery R&D

|

Shift toward specialty and separator-grade silicas

|

Precipitated Silica Market Report Scope

Precipitated Silica Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.3 Billion

|

|

Market Size (2034)

|

$9.9 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Grade (Rubber Grade, Food & Feed Grade, Dental Grade, Industrial & Specialty Grade), By Application (Automotive & Tires, Footwear, Personal Care, Food & Beverages, Agrochemicals, Industrial Consumables)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries AG, Solvay SA, Qemetica SA, Tata Chemicals Limited, Madhu Silica Private Limited, W. R. Grace & Co., Tosoh Silica Corporation, Quechen Silicon Chemical Co. Ltd., Oriental Silicas Corporation, Glassven CA, Brisil Technologies, MLA Group of Industries, Anten Chemical Co. Ltd., PQ Corporation, Fuji Silysia Chemical Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Precipitated Silica Market Segmentation

By Grade

- Rubber Grade

- Food & Feed Grade

- Dental Grade

- Industrial & Specialty Grade

By Application

- Automotive & Tires

- Footwear

- Personal Care

- Food & Beverages

- Agrochemicals

- Industrial Consumables

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Precipitated Silica Industry

- Evonik Industries AG

- Solvay SA

- Qemetica SA

- Tata Chemicals Limited

- Madhu Silica Private Limited

- W. R. Grace & Co.

- Tosoh Silica Corporation

- Quechen Silicon Chemical Co. Ltd.

- Oriental Silicas Corporation

- Glassven CA

- Brisil Technologies

- MLA Group of Industries

- Anten Chemical Co. Ltd.

- PQ Corporation

- Fuji Silysia Chemical Ltd.

*- List not Exhaustive