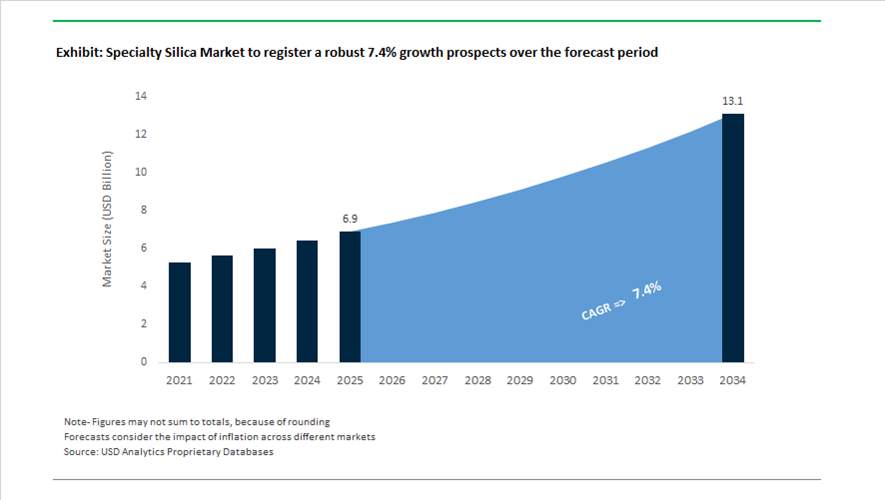

Specialty Silica Market Valuation 2025–2034: $6.9 Billion to $13.1 Billion at 7.4% CAGR Fueled by EV Tire Innovation, Sustainable Feedstocks, and Asset Realignment

The global specialty silica market is valued at $6.9 billion in 2025 and is projected to reach $13.1 billion by 2034, expanding at a CAGR of 7.4%. Growth is anchored in highly dispersible silica (HDS), precipitated silica, fumed silica, and bio-based silica grades used in fuel-efficient tires, EV tire compounds, personal care formulations, food additives, chromatography media, and specialty coatings. Demand for low-rolling-resistance tire silica, green silica from rice husk ash, high-purity silica for pharmaceutical chromatography, and rheology-modifying mineral fillers is accelerating under tightening automotive efficiency standards and sustainability mandates. The market is simultaneously undergoing structural consolidation, capacity optimization, and feedstock diversification to strengthen supply resilience across North America, Europe, and Asia-Pacific.

In February 2024, Evonik expanded its precipitated silica capacity at the Charleston, South Carolina site to address the North American shift toward low-rolling-resistance tire compounds optimized for electric vehicles. In early 2024, Evonik launched ULTRASIL® 4000 GR, engineered for enhanced traction in mud and snow tires, featuring low surface area properties that allow higher filler loading in tread formulations and mechanical rubber goods. In March 2024, W.R. Grace completed the expansion of its fine chemical CDMO facility in South Haven, Michigan, leveraging proprietary specialty silica technologies for chromatography separation and drug delivery systems. In May 2024, Huber Engineered Materials acquired Active Minerals International, integrating complementary kaolin and gel clay mineral technologies into its specialty silica portfolio for coatings and rheology control applications.

Portfolio reshaping intensified in late 2024. In July 2024, PPG validated research demonstrating that its FLO-GARD™ precipitated silica provides up to 40 times the carrying capacity of maltodextrin, positioning specialty silica as a high-performance carrier for liquid-to-powder conversion in food and feed ingredients. In November 2024, PQ completed the expansion of its Pasuruan, Indonesia facility to support Asia-Pacific demand in rubber reinforcement and personal care silica applications. In late 2024, PPG Industries finalized the sale of its precipitated silica business to Qemetica, including manufacturing assets in Lake Charles, Louisiana, and Delfzijl, Netherlands, marking a strategic exit from direct silica production to concentrate on coatings. Throughout 2024, Tata Chemicals commercialized rice husk ash-derived TYSIL™ and TREADSIL™ grades, advancing bio-based specialty silica solutions for sustainable tire manufacturing and reduced carbon intensity.

Operational realignment continued into 2025 and 2026. In January 2025, Evonik announced the closure of its fumed silica plant in Waterford, New York by mid-2025 and its precipitated silica plant in Havre de Grace, Maryland by mid-2026, consolidating production into larger, more competitive hubs to enhance cost efficiency and regional supply resilience. Solvay, following its late-2023 demerger, entered 2024 operating its silica activities under the Essential Co. structure, reinforcing its leadership in highly dispersible silica for fuel-efficient and EV tires. In February 2026, Wacker Chemie AG implemented price increases of up to 25% across silicone and pyrogenic silica products, citing a doubling of platinum catalyst costs and persistent raw material volatility.

Key Trends and Strategic Opportunities in the Specialty Silica Market

High-Purity Fumed Silica as a Safety-Critical Enabler for EV Battery Architectures

The Specialty Silica Market is undergoing a structural demand shift as electric vehicle platforms migrate toward 800V and higher-voltage systems, cell-to-pack architectures, and silicon-rich anode chemistries. In these next-generation battery designs, thermal stability and fire mitigation are no longer secondary performance attributes but core safety requirements. High-purity fumed silica has emerged as a non-discretionary component in thermal interface materials, flame-retardant coatings, and separator technologies, where it functions as a thermal barrier, rheology modifier, and mechanical stabilizer under extreme heat flux.

Strategic product evolution is accelerating in response to these requirements. In February 2024, Evonik highlighted the role of its AEROXIDE fumed metal oxides in enabling ultra-thin ceramic coatings, often at thicknesses below one micrometer, on lithium-ion battery separators. These nanostructured silica layers significantly limit membrane shrinkage at elevated temperatures, reducing the probability of internal short circuits during thermal runaway events and directly supporting longer battery life and enhanced safety margins.

Investment patterns confirm the permanence of this trend. Cabot Corporation’s intensified focus on battery-grade fumed silica following its Kentucky expansion underscores the importance of localized, secure supply for EV manufacturers. Recognition at the China International Import Expo in November 2025 reinforced silica’s role in stabilizing high-nickel cathodes and silicon-containing anodes, where controlled porosity and surface chemistry contribute to improved cycle life, higher energy density, and extended driving range.

Mandatory Transition to Highly Dispersible Silica for Fuel-Efficient and Low-Emission Tires

Regulatory pressure on vehicle efficiency has made the substitution of carbon black with Highly Dispersible Silica unavoidable for tire manufacturers targeting top-tier performance ratings. Frameworks such as the EU Tire Labeling Regulation and U.S. CAFE standards are forcing OEMs to optimize rolling resistance, wet grip, and abrasion resistance simultaneously. Highly dispersible silica has become central to this transition, enabling reductions in rolling resistance of up to 25% while maintaining or improving safety performance.

Manufacturing efficiency is emerging as a parallel driver. Research conducted between 2023 and 2025 demonstrated that co-precipitated silica-silane systems, such as PPG’s AGILON performance silica, can deliver nearly 50% energy savings during tire compounding. By eliminating high-energy mixing steps, these materials reduce production time by approximately one-third while delivering consistent dispersion, improved treadwear, and enhanced wet traction.

Circularity initiatives are further reinforcing silica’s strategic role. The January 2025 collaboration between Solvay and Hankook Tire to develop circular silica from rice husk ash signals a shift away from energy-intensive sodium silicate routes. This bio-based feedstock approach directly addresses Scope 3 emissions for automotive OEMs while preserving the critical balance between efficiency, safety, and durability that defines premium tire performance.

Specialty Silica as a Smart Carrier for Controlled-Release Agrochemical Formulations

The global shift from broad-spectrum pesticides toward precision crop protection is creating a high-value opportunity for engineered porous silica. In modern agrochemical formulations, specialty silica functions as a smart carrier in water-dispersible granules, preventing caking, improving flowability, and enabling controlled release of active ingredients over extended periods.

Adoption is accelerating as resistance management becomes a priority. At the AgroChem Summit 2025 in New Delhi, industry stakeholders emphasized the need for advanced formulations that enhance biological efficacy while reducing overall chemical load. Porous specialty silicas are increasingly qualified as inert carriers that improve leaf adhesion, protect sensitive biopesticides from premature degradation, and enable lower application rates per hectare without compromising yield.

Regulatory alignment is strengthening demand. European initiatives aimed at reducing chemical runoff and operator exposure are driving the adoption of low-dust, high-porosity silica grades in granular formulations. These systems reduce airborne exposure for farmworkers and minimize leaching into soil and water systems, aligning specialty silica with sustainability mandates and long-term food security objectives.

Nano-Silica Integration in Point-of-Need Additive Manufacturing Ecosystems

The rapid expansion of additive manufacturing in aerospace, medical devices, and advanced electronics has opened a premium niche for nano-silica as both a flow aid and nanocomposite reinforcement. In high-resolution 3D manufacturing, silica plays a critical role in stabilizing print rheology, improving layer adhesion, and enhancing final part performance.

Industrial scaling reached a milestone in early 2025 when GBC Advanced Materials expanded ceramic additive manufacturing capabilities using nanoparticle jetting systems. In these platforms, nano-silica serves as the primary ceramic medium, enabling the production of complex geometries with dimensional accuracy and surface finishes unattainable through conventional forming techniques. This capability is particularly valuable for semiconductor tooling and defense components where tolerances are measured in microns.

Material performance data reinforces the opportunity. Research presented in 2025 showed that incorporating silica-based nanocomposites into bio-derived resin systems significantly increases cross-link density during curing. The result is additively manufactured components exhibiting over 36% higher strength and more than 45% improved flexibility compared to standard polymer or concrete-based analogs. As localized, point-of-need manufacturing expands, nano-silica is positioned as a foundational material for next-generation, high-performance additive manufacturing solutions.

Specialty Silica Market Share and Segmentation Insights

Precipitated Silica Dominates the Specialty Silica Market Driven by Green Tire Technology

Precipitated silica accounted for 42.8% of the specialty silica market in 2025, making it the most widely used silica product across industrial applications. Its versatility and cost effectiveness support use in tire reinforcement, coatings rheology modification, food and feed carriers, and personal care formulations. In the tire industry, precipitated silica functions as a reinforcing filler that improves rolling resistance, wet traction, and durability, enabling the development of energy-efficient tire compounds. A major 2025 industry driver is the increasing emphasis on vehicle fuel efficiency standards, which has accelerated adoption of silica-filled tread compounds in passenger vehicle tires. Manufacturers are expanding production of high-dispersibility silica grades designed to improve compound mixing efficiency and optimize tire performance.

Tires and Rubber Applications Drive Global Specialty Silica Demand

Tires and rubber represent the largest application segment in the specialty silica market, accounting for 38.6% of total demand in 2025 due to the extensive use of silica as a reinforcing filler in tire tread formulations. Silica enhances traction performance, rolling resistance, and abrasion resistance, enabling the production of advanced tire designs that improve vehicle safety and fuel efficiency. Each passenger vehicle tire can contain several kilograms of precipitated silica within the tread compound. A significant 2025 industry trend is the growing influence of electric vehicle tire requirements, where heavier vehicles and higher torque output require tires with enhanced durability and energy efficiency. This has driven development of specialized silica grades optimized for EV tire compounds.

Specialty Silica Market Competitive Landscape

The specialty silica market in 2026 is driven by ultra-high purity silica for semiconductors, circular raw materials like rice husk ash, and high-performance fillers for EV batteries and green tires. Industry leaders are optimizing production hubs, advancing CMP-grade silica, and integrating sustainable silica-silane systems for mobility and electronics.

Evonik Expands ULTRASIL® Capacity and Leads Green Tire Silica Integration for EV Performance

Evonik is reinforcing its global leadership in specialty silica through capacity expansion and advanced silica-silane integration. The Charleston plant expansion increases precipitated silica output by 50%, strengthening North American supply for ULTRASIL® sustainable silica. The launch of ULTRASIL® 4000 GR enhances traction performance in winter and all-season tires. Evonik is consolidating operations by closing smaller plants and shifting production to high-efficiency hubs. Its Si 363™ silane integration reduces rolling resistance by up to 35%, improving EV range by approximately 8%. The company remains a benchmark in green tire chemistry and high-performance silica systems.

Cabot Strengthens Circular Silica Portfolio and Regional Footprint Through Strategic Acquisition and Pricing Power

Cabot is advancing its specialty silica business through circular materials innovation and strategic capacity expansion. The acquisition of Mexico Carbon Manufacturing enhances regional manufacturing capabilities in North America. Its EVOLVE® Sustainable Solutions platform enables production of silica using recovered and bio-based feedstocks. In 2026, Cabot implemented price increases of up to 20% to offset energy and supply chain pressures. The company maintains strong ESG positioning with an A- CDP Water Security rating. Cabot’s focus on surface-modified silica and circular reinforcing materials supports high-performance industrial and automotive applications.

Wacker Chemie Enhances Semiconductor-Grade Silica Capacity and Precision Materials for Electronics and Adhesives

Wacker Chemie is focusing on high-purity silica and precision materials for semiconductor and advanced manufacturing applications. The Burghausen site expansion increases capacity for hyperpure polysilicon and silica precursors by over 50%. Under its PACE efficiency program, Wacker is targeting €300 million in savings to reinvest in specialty silica R&D. Its HDK® fumed silica portfolio is critical for CMP slurries, aerospace materials, and medical-grade silicones. The company is developing surface-treated silica for rheology control in non-polar systems used in structural adhesives. Stabilizing demand in electronics and automotive sectors is supporting improved EBITDA margins.

Solvay Advances Highly Dispersible Silica and Oral Care Solutions with Strong ESG and Cost Optimization Strategy

Solvay is strengthening its specialty silica portfolio through cost efficiency and sustainable product innovation. The company achieved €101 million in cost savings in 2025 and is targeting €300 million by 2026 to support reinvestment in high-value silica technologies. Its Highly Dispersible Silica (HDS) solutions are central to green mobility and tire performance applications. Solvay reported a strong 20.7% EBITDA margin and is maintaining disciplined capital allocation. Its Tixosil® range remains a benchmark for oral care silica, offering controlled abrasivity and rheology. ESG leadership, including global living wage implementation, enhances its supplier positioning.

Orion Expands Specialty Hybrid Fillers and ESG Leadership to Capture High-Margin Automotive and Coatings Demand

Orion is positioning itself in the specialty silica market through hybrid filler solutions combining carbon black and silica technologies. The company reported $1.8 billion in revenue in 2025, with EBITDA growth driven by premium product mix in specialty segments. Its EcoVadis Platinum rating supports access to sustainability-driven contracts in the European automotive sector. Orion is prioritizing free cash flow generation through reduced capital expenditure and working capital optimization. Its specialty fillers are gaining traction in polyurethane, coatings, and conductive material applications. Operational improvements have enhanced delivery performance and supply reliability for high-value customers.

United States Specialty Silica Market Shaped by Asset Optimization and High-Value End Uses

The United States specialty silica industry is undergoing a deliberate structural reset focused on asset efficiency, high-margin applications, and regulatory alignment. In 2025–2026, Evonik Industries initiated a strategic repositioning of its North American silica network, announcing the planned closure of its fumed silica plant in Waterford, New York by mid-2025 and precipitated silica operations in Havre de Grace, Maryland by mid-2026. This consolidation strategy is designed to shift production into larger, fully integrated hubs with stronger cost positions and closer proximity to downstream customers. At the same time, Evonik completed a 50% capacity expansion at its Charleston, South Carolina site in late 2024, reinforcing the United States as a core supply base for high-performance precipitated silica used in fuel-efficient green tires.

Portfolio realignment and application-driven innovation continue to redefine competitive dynamics. Wacker Chemie AG has fully integrated its Charleston, Tennessee operation as a silicon hub, leveraging tetrachlorosilane byproducts from polysilicon manufacturing to produce HDK-branded pyrogenic silica. In parallel, PPG exited precipitated silica through a $310 million divestment to QEMETICA, signaling a broader industry shift away from volume-led segments. On the innovation front, W. R. Grace & Co. launched the SYLOID XDP pharmaceutical silica line in 2025, engineered to convert oily APIs into free-flowing powders. New EPA occupational exposure rules effective 2025 are also accelerating demand for low-dust specialty silica in coatings and industrial formulations.

Italy Specialty Silica Market Anchored in Bio-Circular Feedstocks and Tire Industry Alignment

Italy has emerged as a strategic testbed for bio-circular specialty silica production aligned with European decarbonization goals. In September 2025, Solvay inaugurated its first commercial-scale bio-circular Highly Dispersible Silica unit in Livorno. The facility utilizes sodium silicate derived from rice husk ash, replacing conventional sand-based feedstocks and demonstrating a viable pathway for renewable raw material integration into silica manufacturing. This process innovation reportedly delivers up to a 50% reduction in product-level carbon footprint, directly supporting the EU’s 2030 climate objectives.

The Livorno site has been strategically positioned to serve Europe’s premium tire ecosystem, acting as a primary supply node for manufacturers such as Pirelli that are actively increasing sustainable material content in high-performance and ultra-high-performance tires. This tight coupling between specialty silica innovation and downstream tire OEM requirements underscores Italy’s role as a value-driven rather than volume-oriented silica producer within the European landscape.

Japan Specialty Silica Market Driven by Semiconductor Security and Battery Materials

Japan’s specialty silica sector is increasingly defined by its role in safeguarding semiconductor and battery supply chains. In October 2025, Evonik Industries commissioned its Alu5 facility in Yokkaichi, marking the company’s first fumed aluminum oxide production asset in the country. While focused on alumina, the plant directly complements Japan’s electronic-grade silica ecosystem by supplying AEROXIDE grades critical for lithium-ion battery coatings and semiconductor polishing processes.

This investment aligns with the Economic Security Promotion Act, which prioritizes domestic sourcing of high-purity materials for 2 nm and 3 nm chip fabrication lines. Beyond capacity expansion, Japanese producers have implemented ultra-high-purity filtration systems in 2025, enabling colloidal silica production with metallic impurity levels below 10 parts per billion. This focus on purity leadership reinforces Japan’s strategic position in CMP slurries and advanced electronic materials where contamination thresholds are increasingly unforgiving.

China Specialty Silica Market Focused on Self-Sufficiency and Solar Applications

China’s specialty silica industry is evolving under strong policy direction aimed at micro-electronics self-sufficiency and renewable energy scale-up. Through the “Little Giant” industrial framework, domestic producers are incentivized to localize CMP slurry production using internally synthesized colloidal silica, reducing reliance on imported electronic-grade materials. This has accelerated investment in purification, particle-size control, and dispersion technologies tailored for semiconductor fabrication.

Export control dynamics are also reshaping the market. Following tighter scrutiny on dual-use specialty minerals in 2025, Chinese suppliers are recalibrating global trade strategies for high-end optical and electronic silica. Concurrently, China’s leadership in photovoltaic module manufacturing has driven record demand for fumed silica as a rheology and thixotropic additive in solar-grade silicone sealants, positioning the country as the world’s largest demand center for construction and energy-related specialty silica applications.

Germany Specialty Silica Market Defined by Carve-Out Strategies and Energy-Efficient Synthesis

Germany’s specialty silica market is closely linked to broader restructuring within its chemical sector and a strong push toward energy-efficient manufacturing. In late 2025, BASF completed the carve-out of its specialty pigments and resins business, including silica-based additives, into a standalone entity. This separation is intended to unlock targeted investment for high-performance effect pigments and functional fillers without exposure to cyclical upstream operations.

Innovation is increasingly centered on sustainability and process efficiency. Research clusters in Nordrhein-Westfalen achieved industrial-scale production of silica-reinforced bio-polyols in 2025, supporting lightweight automotive interiors and advanced adhesive systems. In collaboration with the Fraunhofer Institute, German producers have also begun piloting microwave-assisted silica synthesis, targeting a 20% reduction in energy intensity compared with conventional precipitation methods.

India Specialty Silica Market Supported by Infrastructure and R&D Clusters

India’s specialty silica demand profile is being shaped by infrastructure expansion and government-backed R&D ecosystems. The expansion of the Science and Technology Clusters initiative from 8 to 25 hubs in 2025 has created shared infrastructure for the development of nano-silica tailored for agricultural yield enhancement, textile finishing, and functional coatings. These clusters are accelerating domestic capability building in application-specific silica grades.

At the same time, large-scale infrastructure investment under the PM Gati Shakti national master plan is driving demand for silica fume and specialty concrete additives. High-durability highways, metro corridors, and logistics parks require performance-enhancing mineral additives, positioning specialty silica as a critical input for India’s long-term construction and urbanization strategy.

Comparative Snapshot: Specialty Silica Industry by Country

Specialty Silica Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Specialty Silica Application

|

Structural Direction

|

|

United States

|

Asset consolidation and green tires

|

Precipitated and pharma-grade silica

|

Hub optimization and regulatory alignment

|

|

Italy

|

Bio-circular production

|

Highly dispersible tire silica

|

Renewable feedstock integration

|

|

Japan

|

Semiconductor and battery security

|

UHP colloidal silica and fumed oxides

|

Purity leadership and localization

|

|

China

|

Self-sufficiency and photovoltaics

|

CMP silica and solar sealant additives

|

Policy-driven capacity scaling

|

|

Germany

|

Energy efficiency and carve-outs

|

Silica additives and bio-polyols

|

Standalone investment and process innovation

|

|

India

|

Infrastructure and R&D clusters

|

Silica fume and nano-silica

|

Demand-led domestic capability building

|

Specialty Silica Market Report Scope

Specialty Silica Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.9 Billion

|

|

Market Size (2034)

|

$13.1 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Product Type (Precipitated Silica, Fumed Silica, Silica Gel, Colloidal Silica, Fused Silica, Specialty Silica Derivatives), By Application (Tires and Rubber, Paints and Coatings, Personal Care, Electronics and Semiconductors, Food and Animal Feed, Agriculture, Adhesives and Sealants)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries AG, Solvay S.A., Cabot Corporation, Wacker Chemie AG, W. R. Grace and Company, Qemetica, Akzo Nobel N.V., Nouryon, Merck KGaA, Madhu Silica Pvt. Ltd., Tosoh Corporation, Tokuyama Corporation, Agsco Corporation, Sibelco Group, KCC Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Silica Market Segmentation

By Product Type

- Precipitated Silica

- Fumed Silica

- Silica Gel

- Colloidal Silica

- Fused Silica

- Specialty Silica Derivatives

By Application

- Tires and Rubber

- Paints and Coatings

- Personal Care

- Electronics and Semiconductors

- Food and Animal Feed

- Agriculture

- Adhesives and Sealants

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Silica Industry

- Evonik Industries AG

- Solvay S.A.

- Cabot Corporation

- Wacker Chemie AG

- W. R. Grace and Company

- Qemetica

- Akzo Nobel N.V.

- Nouryon

- Merck KGaA

- Madhu Silica Pvt. Ltd.

- Tosoh Corporation

- Tokuyama Corporation

- Agsco Corporation

- Sibelco Group

- KCC Corporation

*- List not Exhaustive