Laser Cladding Market Size, Additive Manufacturing Integration, and High-Precision Surface Engineering Outlook

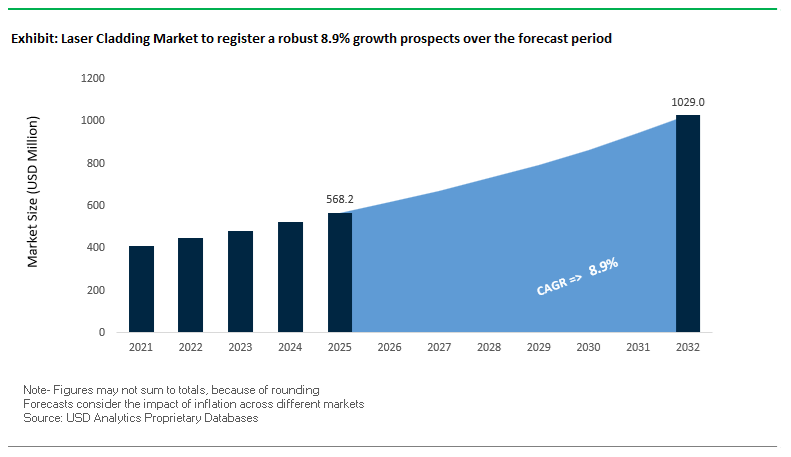

The global laser cladding market was valued at $568.2 million in 2025 and is projected to reach $1,032 million by 2032, expanding at a strong CAGR of 8.9%. This accelerated growth is driven by increasing adoption of laser cladding systems, directed energy deposition (DED), high-speed laser cladding (EHLA), and additive surface engineering technologies across aerospace, oil & gas, mining, automotive, and power generation industries. These technologies are increasingly replacing conventional repair and coating methods due to their ability to deliver high-precision material deposition, minimal dilution, and superior metallurgical bonding.

A key growth driver is the rising demand for component refurbishment and lifecycle extension, particularly in heavy industrial equipment, turbine components, and critical rotating machinery. Laser cladding enables cost-effective repair, corrosion resistance, and wear protection, significantly reducing downtime and replacement costs. Additionally, the transition toward additive manufacturing and hybrid manufacturing systems is accelerating the integration of laser cladding into CNC machines and robotic platforms, enabling complex geometries and high-performance coatings on advanced materials.

The market is also benefiting from advancements in high-power fiber lasers, blue laser technology, and real-time process monitoring, which are improving deposition rates, energy efficiency, and coating quality. Growth in electric vehicle (EV) manufacturing, semiconductor fabrication, and renewable energy infrastructure is further expanding the application scope of laser cladding, particularly for high-conductivity materials and high-temperature alloys. Regionally, Europe leads in technology innovation and public funding initiatives, while Asia-Pacific is emerging as a high-growth region due to expanding industrial manufacturing and infrastructure investments.

Market Analysis: High-Power Laser Innovation, Digital Cladding Platforms, and Additive Manufacturing Partnerships Driving Market Evolution

The laser cladding industry is undergoing rapid technological transformation, driven by advancements in laser sources, strategic partnerships, and the convergence of additive manufacturing with surface engineering. In January 2026, IPG Photonics introduced an 8-kilowatt compact single-mode laser source, specifically engineered to enhance high-speed laser cladding and DED processes for aerospace-grade alloys, significantly improving deposition precision and throughput. In parallel, Coherent Corp. launched a new range of high-power fiber lasers optimized for large-scale industrial cladding, targeting high-deposition-rate applications in mining and oil & gas equipment refurbishment.

The adoption of laser cladding as a replacement for traditional repair methods is gaining momentum. In November 2025, Eurobearings integrated Meltio’s laser-wire DED technology for the repair of industrial bearings, marking a shift from conventional welding to precision cladding techniques for critical rotating equipment. This transition underscores the growing importance of laser-based repair technologies in reducing maintenance costs and improving component performance.

Digitalization and system integration are also reshaping the competitive landscape. Oerlikon Metco’s Surface Two™ platform, launched in July 2025, represents a next-generation digital thermal spray and laser cladding system with real-time process monitoring, enabling improved quality control for large industrial components. Furthermore, Oerlikon’s March 2025 partnership with 3D Systems integrates advanced material science with robotic delivery systems, targeting high-precision applications in semiconductors and energy infrastructure.

Innovation in laser technology is expanding material compatibility and application flexibility. TRUMPF’s May 2025 acquisition stake in Laserline GmbH strengthens its position in blue laser technology, which is critical for processing highly reflective materials such as copper, widely used in EV components and advanced electronics. Complementing this, Meltio’s February 2025 launch of the M600 and Engine Blue systems introduces blue laser heads that enable cladding of complex geometries with high thermal and electrical conductivity, supporting next-generation manufacturing requirements.

Public funding and collaborative initiatives are accelerating market commercialization. In August 2024, the European Union allocated €15 million to the European Laser Cladding Innovation Alliance (ELCIA) to advance EHLA technology, positioning it as a sustainable alternative to hard chrome plating in automotive and aerospace sectors. Additionally, the July 2024 collaboration between Oerlikon and MTU Aero Engines to establish a digitized laser cladding factory in Switzerland highlights the move toward fully automated, smart manufacturing environments for jet engine component repair.

Material innovation continues to support performance enhancements. Höganäs AB expanded its Amperit® powder portfolio in May 2024, introducing nickel-based superalloy powders designed for extreme heat and corrosion resistance in applications such as waste-to-energy plant boilers.

Market Trend: Tungsten Carbide Laser Cladding Driving Performance Gains in Mining Ground Engaging Tools (GET)

Laser cladding technology is witnessing accelerated adoption in mining and earthmoving applications, particularly for Ground Engaging Tools (GET) such as bucket teeth, shovel lips, and grader blades. The shift from conventional hardfacing welding toward tungsten carbide (WC)-based laser cladded coatings is being driven by the need for superior wear resistance, geometry retention, and operational efficiency. Laser-cladded WC-Ni matrices are demonstrating significant performance advantages, with ASTM G65 abrasion testing indicating volume loss below 1.5 mm³, outperforming Chromium Carbide Overlay (CCO) solutions by three to five times. This substantial improvement in abrasion resistance is directly influencing lifecycle cost optimization strategies across large-scale mining operations.

A critical technical differentiator lies in the microstructural integrity achieved through laser cladding. The low Heat Affected Zone (HAZ) prevents dissolution of carbide particles, enabling components to retain approximately 92% to 95% of their original hardness levels, typically ranging between 1600 HV and 2200 HV. This structural stability ensures consistent wear performance even under extreme abrasive conditions such as iron ore and oil sands extraction. Additionally, laser cladding enables the formation of self-sharpening edges on GET components, reducing drag forces in high-compaction soils and improving excavation efficiency. Field data indicates a 5% to 8% reduction in diesel consumption for hydraulic excavators, positioning laser cladding as a key enabler of fuel efficiency and sustainability in mining operations.

From an asset management perspective, laser-cladded components are delivering service life extensions of up to 350 to 500 hours, compared to 80 to 120 hours for conventional heat-treated steel tools. This translates into fewer replacements, reduced downtime, and improved productivity metrics, making laser cladding a critical technology in predictive maintenance and cost control strategies within the mining sector.

Market Trend: Aerospace Transition from Hard Chrome Plating to High-Speed Laser Cladding for Compliance and Fatigue Performance

The aerospace industry is undergoing a structural transition away from Hard Chrome Plating (HCP) toward advanced laser cladding technologies, driven by stringent environmental regulations targeting hexavalent chromium (CrVI) and the need for enhanced component durability. High-Speed Laser Cladding (HSLC) is emerging as a superior alternative, offering significant improvements in fatigue strength, processing efficiency, and coating integrity for critical aerospace components such as landing gear systems.

One of the most decisive advantages of laser cladding is its ability to preserve base material fatigue strength. HSLC-treated components retain approximately 95% of their original fatigue performance, whereas traditional HCP processes can reduce fatigue life by 20% to 50% due to hydrogen embrittlement. This improvement is critical in aerospace applications where cyclic loading conditions demand high structural reliability and safety margins. Furthermore, laser cladding delivers substantial gains in production efficiency, enabling deposition of 0.5 mm to 1.5 mm coatings in a single pass at speeds reaching 200 cm² per minute. In contrast, HCP processes typically require prolonged immersion times of 15 to 24 hours to achieve comparable coating thicknesses.

Material integrity and bonding performance further reinforce the shift toward laser cladding. Ultrasonic inspections of laser-cladded stainless-steel coatings, particularly on 420-grade substrates, consistently reveal zero porosity and metallurgical bond strengths exceeding 400 MPa. This level of adhesion significantly surpasses the mechanical bonding achieved through electroplating, reducing the risk of coating delamination under operational stress. Additionally, the elimination of toxic waste streams associated with CrVI processing has resulted in up to 60% reduction in chemical disposal costs for aerospace MRO facilities. This aligns with broader ESG mandates and regulatory compliance frameworks, accelerating adoption across global aerospace OEMs and maintenance providers.

Market Opportunity: U.S. DOE Investment Accelerating Laser Cladding Adoption for Nuclear Reactor Life Extension

Government-backed funding initiatives are creating substantial growth opportunities for laser cladding technologies in the nuclear energy sector. The U.S. Department of Energy, through programs under the Office of Energy Efficiency and Renewable Energy and the Advanced Materials and Manufacturing Technologies Office, has prioritized Directed Energy Deposition (DED) and laser cladding for in-situ repair of aging nuclear infrastructure. These initiatives are specifically targeting degradation issues in Type 304 and 316 stainless steel reactor components affected by Irradiation-Assisted Stress Corrosion Cracking (IASCC).

Funding allocations in the 2025 to 2026 cycles are enabling the development of advanced repair methodologies that meet stringent nuclear safety standards. Experimental validation has demonstrated that laser-cladded pressure vessel components can withstand rapid thermal shock cycles ranging from 300°C to 20°C without interface delamination. This capability is critical for ensuring structural integrity under fluctuating operational conditions associated with Extended Power Uprates (EPU). The ability to deploy remote-head laser cladding systems within reactor cooling loops represents a significant advancement in maintenance practices, minimizing radiation exposure risks and operational disruptions.

Economic implications are equally substantial. Utilities adopting laser cladding for component repair are projected to achieve cost savings between $5 million and $12 million per outage by eliminating the need for full component replacement. These savings, combined with reduced downtime, position laser cladding as a strategic technology for lifecycle cost optimization in nuclear power generation. Moreover, DOE-led initiatives are aligned with long-term energy security objectives, targeting operational life extensions of up to 80 years for existing nuclear fleets. This creates a sustained demand pipeline for laser cladding solutions in high-value, safety-critical applications.

Market Opportunity: China’s MIIT Policy Support Driving Industrial-Scale Laser Cladding Deployment and Cost Competitiveness

China’s designation of laser cladding as a Strategic Advanced Manufacturing Technology under its 14th Five-Year Plan is creating a robust growth environment for the global laser cladding market. Policy-driven incentives, including tax credits and direct subsidies covering 15% to 25% of capital expenditure, are accelerating the adoption of high-power laser systems exceeding 6kW across industrial sectors. This level of financial support is significantly lowering entry barriers for manufacturers and expanding the installed base of laser cladding equipment.

A key outcome of this policy framework is the rapid localization of supply chains, particularly in high-purity metal powders such as Inconel, Stellite, and iron-based alloys. Domestic production capabilities have led to a 30% reduction in material costs since 2024, enhancing the cost competitiveness of Chinese laser cladding service providers in both domestic and export markets. This cost advantage is expected to influence global pricing dynamics and intensify competition in the additive manufacturing and surface engineering sectors.

Industrial deployment has reached substantial scale, with more than 1,200 large-format laser cladding systems installed across key industrial provinces including Shaanxi, Liaoning, and Shandong. These systems are primarily utilized in the remanufacturing of hydraulic roof supports within the coal mining industry, highlighting the role of laser cladding in circular economy initiatives and asset refurbishment strategies. In parallel, the development of national standards for laser cladding quality assessment is strengthening process consistency and aligning Chinese manufacturing practices with international ISO and ASTM frameworks.

This combination of policy support, cost optimization, and large-scale industrial integration positions China as a dominant force in the global laser cladding ecosystem, creating export opportunities, technology partnerships, and competitive pressure for international players seeking to expand in high-growth markets.

Laser Cladding Market Share and Segmentation Insights

Powder Laser Cladding Captures 78% Market Share Driven by Alloy Flexibility and Superior Surface Quality

The laser cladding market by process is overwhelmingly led by powder laser cladding, which accounts for approximately 78% of the global market share in 2025, making it the most widely adopted technology in advanced surface engineering. This dominance is driven by its exceptional material flexibility, allowing the use of diverse alloys such as cobalt-based, nickel-based, iron-based materials, carbides, and custom-engineered blends. These capabilities are critical for high-demand sectors like aerospace, oil & gas, mining, and power generation, where precision repair and coating performance are essential. Additionally, powder-based systems produce finer melt pools and thinner clad layers (0.5–2mm), ensuring a uniform surface finish with minimal post-machining requirements. Compared to wire laser cladding, this translates into lower operational costs, improved dimensional accuracy, and enhanced component lifespan, reinforcing its leadership in high-performance industrial applications.

Laser Cladding Services Hold 52% Share as Industries Prefer Cost-Efficient Outsourced Repair Solutions

In the laser cladding market by revenue stream, laser cladding services dominate with a 52% market share in 2025, reflecting a strong industry shift toward outsourced surface engineering solutions. Major end-use industries—including aerospace, heavy equipment, and power generation—prefer to send critical components such as turbine blades, hydraulic shafts, and impellers to specialized service providers rather than investing in in-house systems. This trend is largely driven by the high capital cost of laser cladding equipment, which ranges from $300,000 to $1.5 million, creating a significant barrier for small and mid-sized enterprises. Service-based models enable access to advanced laser cladding technology, wear-resistant coatings, and precision repair capabilities without upfront investment. As a result, the service segment continues to expand rapidly, supported by growing demand for cost-effective maintenance, repair, and overhaul (MRO) solutions across industrial sectors.

Competitive Landscape in the Laser Cladding Market

TRUMPF leads high-precision laser cladding innovation in Europe

TRUMPF holds a dominant position in the European laser cladding market, which accounts for over 46% of global share, leveraging its expertise in modular system design and high-precision integration. Its TruLaser Cell series enables advanced 3D laser metal deposition (LMD), supporting complex geometries and high-value industrial applications. The introduction of High-Speed Laser Cladding (EHLA) has significantly enhanced coating efficiency, achieving speeds up to 100 times faster than traditional processes. TRUMPF’s integration of AI-driven sensor systems for real-time melt pool monitoring ensures defect-free manufacturing, particularly in aerospace components. Its strong vertical integration across laser sources, optics, and software strengthens its leadership in automotive and medical device sectors, while its circular economy focus promotes repair and lifecycle extension of critical components.

Oerlikon Metco strengthens materials and equipment synergy for surface solutions

Oerlikon Metco continues to position itself as a global leader in surface engineering by integrating advanced materials with laser cladding systems. Its comprehensive “Materials + Equipment” ecosystem, including MetcoClad powders composed of cobalt, nickel, and iron-based alloys, supports high-performance deposition processes. Between 2025 and 2026, the company recorded a 6.5% growth in order intake, driven primarily by aviation and energy sectors. Oerlikon’s LaserClad™ turnkey systems combine powder feeders with high-efficiency diode lasers to deliver corrosion-resistant coatings. The company’s expansion in Asia-Pacific, particularly in India, reflects its strategic targeting of power generation and heavy machinery industries, reinforcing its global footprint and strengthening its position in high-demand industrial applications.

IPG Photonics drives fiber laser dominance in high-power cladding systems

IPG Photonics leads the fiber laser segment, which represents the fastest-growing technology category in the laser cladding market due to superior beam quality and efficiency. Its high-power continuous wave (CW) fiber lasers, delivering up to 10 kW output, enable rapid deposition rates across demanding sectors such as mining, oil and gas, and electric mobility. With an industry-leading beam quality (M² < 1.1) and high wall-plug efficiency, IPG systems offer significant operational advantages. The introduction of YLS-AMB (Adjustable Mode Beam) lasers allows precise control over core and ring beam distribution, optimizing cladding for crack-sensitive materials. Strategically, IPG is capitalizing on EV battery manufacturing growth by integrating cladding solutions for copper welding and thermal management components.

Coherent Corp. expands photonics integration for advanced manufacturing applications

Following its merger with II-VI, Coherent Corp. has emerged as a vertically integrated leader in advanced photonics and laser cladding technologies. Its HighLight FL series is optimized for large-area cladding and additive manufacturing, supporting diverse industrial requirements with multiple wavelength options, including direct diode and UV lasers. At Photonics West 2026, the company introduced AI-powered in-process monitoring systems and advanced thermal management solutions, enhancing reliability in semiconductor and clinical applications. Coherent’s integration of high-precision optics with robotic cladding cells enables scalable solutions for 3D printing and rapid prototyping. Its strong presence in North America, the second-largest laser cladding market, is driven by increasing demand from defense and semiconductor industries.

Höganäs AB enables advanced cladding through high-performance metal powders

Höganäs AB plays a critical role in the laser cladding value chain as a leading producer of metal powders essential for deposition processes. Its advanced alloy formulations support deposition thicknesses ranging from 0.5 mm to over 4 mm, with hardness levels reaching up to 68 HRC, making them suitable for extreme industrial environments. The company is focusing on sustainability by reducing Scope 1 and 2 emissions in powder production, aligning with evolving green manufacturing mandates in 2026. Recent innovations include high-entropy alloys and specialized carbide blends that deliver superior wear resistance for mining and tunneling applications. Höganäs also offers Digital Powder Services, enabling simulation-driven optimization of powder flow and chemistry prior to actual cladding operations.

Han’s Laser scales cost-efficient automation in Asia-Pacific laser cladding market

Han’s Laser is a key contributor to the rapid expansion of the Asia-Pacific laser cladding market, which is projected to grow at a CAGR of 14.4% through 2035. The company focuses on delivering cost-competitive, high-power fiber laser systems tailored for large-scale industrial applications. Its product portfolio ranges from entry-level workstations to advanced multi-axis robotic cladding centers designed for maritime, energy, and heavy engineering sectors. Han’s Laser is aggressively targeting the automotive brake disc cladding market as a sustainable alternative to hard chrome plating, aligning with tightening environmental regulations. With strong penetration in consumer electronics and electric vehicle sectors, the company emphasizes high-speed surface modification and continues to expand its presence across Southeast Asia and Europe.

Germany Laser Cladding Market: Precision Engineering Powerhouse Driving Industrial Automation

Germany stands as a global leader in the laser cladding market, driven by its strong foundation in precision engineering, advanced manufacturing technologies, and the widespread implementation of the Industrie 4.0 framework. The country continues to integrate laser cladding solutions within automotive manufacturing, semiconductor production, and mechanical engineering, making it a critical hub for innovation in Europe. Institutions such as the Fraunhofer Institute for Production Technology (IPT) are spearheading hybrid additive manufacturing technologies, combining wire-based and powder-based laser cladding to significantly enhance material deposition efficiency and process scalability.

Germany’s aggressive investments in Laser Parks, high-speed Extreme High-Speed Laser Material Deposition (EHLA) systems, and specialized MRO (Maintenance, Repair, and Overhaul) facilities are accelerating industrial adoption. The country also leads in the development of high-power direct diode lasers (DDL) for heat-processing applications, which are gaining rapid traction across industries. With early compliance to EU environmental and laser safety standards, Germany is setting benchmarks for green manufacturing practices, further strengthening its dominance in automotive stainless steel tube production and semiconductor equipment manufacturing.

China Laser Cladding Market: Scaling High-Volume Manufacturing with State-Driven Innovation

China’s laser cladding market is characterized by large-scale industrial deployment, cost competitiveness, and strong government backing, making it one of the fastest-evolving markets globally. The integration of laser cladding within the country’s Circular Economy initiatives highlights its strategic importance in reducing industrial waste and promoting remanufacturing. Rapid technological advancements in fiber laser systems, achieving wall-plug efficiencies exceeding 45%, are significantly improving process efficiency and lowering operational costs.

The presence of emerging domestic players such as Nanjing Zhongke Yu Chen Laser Technology and Jinan Senfeng Laser Technology underscores China’s shift toward technological self-reliance. Substantial investments in closed-loop control systems, real-time monitoring software, and smart manufacturing infrastructure are enabling precise and cost-effective cladding processes. Additionally, the development of remanufacturing zones for mining and petrochemical equipment is reinforcing China’s industrial ecosystem. The country is rapidly transitioning from a low-cost service provider to a global leader in high-speed laser cladding applications, particularly for hydraulic cylinders and large-scale industrial rotors.

United States Laser Cladding Market: Aerospace, Defense, and Energy Sector Dominance

The United States laser cladding market is driven by advanced aerospace, defense sustainment programs, and energy sector investments, positioning it as a leader in high-value applications. The Department of Defense’s initiatives, including the U.S. Army’s Component Repair Program (CRP), have validated laser cladding for over 120 components across aviation platforms, highlighting its critical role in extending asset lifecycle and reducing maintenance costs.

In the aerospace MRO sector, companies like American Cladding Technologies are leveraging laser cladding to repair turbofan engine components, achieving substantial cost savings compared to full replacements. The technology is also gaining momentum in the mining industry, where tungsten carbide cladding is enhancing the durability of centrifugal pump components. Additionally, innovations in Inconel and cobalt-based alloy cladding are addressing corrosion challenges in offshore oil and gas infrastructure. The expansion of mobile laser cladding service bureaus is further enabling on-site repair capabilities, while stringent OSHA regulations ensure safe handling of laser systems and metal powders.

Japan Laser Cladding Market: Robotics Integration and Micro-Precision Manufacturing Excellence

Japan’s laser cladding market is distinguished by its focus on robotics integration, micro-precision engineering, and semiconductor manufacturing, making it a hub for high-accuracy applications. The adoption of 6-axis robotic systems integrated with laser cladding heads is revolutionizing the repair of complex geometries, particularly in plastic injection molds and precision tooling.

The country is investing heavily in additive manufacturing hubs in Tokyo and Osaka, showcased through global events such as the Additive Manufacturing Expo. Laser cladding plays a vital role in tool and die repair, restoring cutting edges, and minimizing production downtime in high-precision industries. Japan is also advancing multi-material cladding technologies to develop functionally graded materials (FGMs), which are crucial for electronics and semiconductor applications. Supported by Green Transformation (GX) policies, Japan is promoting laser-based repair processes as a sustainable alternative to traditional manufacturing, especially in maintaining high-vacuum chambers and lithography equipment.

India Laser Cladding Market: Infrastructure Expansion Fueling High-Growth Opportunities

India is rapidly emerging as a high-growth laser cladding market, driven by expanding infrastructure in the energy, railways, and mining sectors. The increasing need for thermal power plant maintenance, particularly in protecting boiler tubes from high-temperature erosion, is significantly boosting demand for advanced cladding solutions.

Foreign direct investment (FDI) from European laser technology companies is accelerating the establishment of localized service centers for Indian Railways, enhancing operational efficiency and maintenance capabilities. Laser cladding is widely used in the repair of hydro-turbine blades, steam turbine rotors, and petrochemical components, offering superior metallurgical bonding compared to traditional thermal spray methods. Government initiatives such as “Make in India” are encouraging MSMEs to adopt laser-based additive manufacturing technologies through subsidies and policy support. The growing demand for coal mining equipment refurbishment further strengthens India’s position as a key market for industrial laser cladding applications.

United Kingdom Laser Cladding Market: Advancing Sustainable Aviation and Regulatory Excellence

The United Kingdom is positioning itself as a leader in sustainable aviation manufacturing and regulatory-driven laser cladding adoption. The implementation of Construction Products Reform (2026) and Civil Aviation Authority (CAA) certification standards is streamlining the qualification process for laser-clad flight-critical components, boosting industry confidence.

Technological advancements, particularly at the Manufacturing Technology Centre (MTC), include the development of AI-driven process monitoring systems that ensure zero-defect cladding operations. Laser cladding is extensively used in aerospace MRO activities, including compressor disk repair and abradable seal refurbishment, supported by partnerships with global players such as Lufthansa Technik. Government-backed programs through Innovate UK are funding Net Zero manufacturing initiatives, promoting environmentally sustainable production methods. Additionally, collaborations between the University of Sheffield’s Advanced Manufacturing Research Centre (AMRC) and aerospace OEMs are driving innovation in nickel-based superalloy powders, critical for high-performance turbine applications.

Laser Cladding Market Report Scope

Laser Cladding Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$568.2 Million

|

|

Market Size (2032)

|

$1032 Million

|

|

Market Growth Rate

|

8.9%

|

|

Segments

|

By Laser (Fiber Laser, Direct Diode Laser, CO2 Laser, Nd:YAG Laser, Disk Laser), By Power Output (High Power, Low Power), By Process (Powder Laser Cladding, Wire Laser Cladding), By Material (Nickel-based Alloys, Cobalt-based Alloys, Iron-based Alloys, Carbides and Carbide Blends, Ceramics and Cermets, Specialty Materials), By Application (Repair and Reconditioning, Surface Coating, Additive Manufacturing, Functional Prototyping), By End-Use Industry (Aerospace and Defense, Oil and Gas, Automotive and Transportation, Mining, Power Generation, Medical Devices, Industrial Machinery and Tooling, Marine and Shipbuilding), By Revenue Stream (System, Laser Cladding Services, Aftermarket and Consumables)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

TRUMPF Group, Oerlikon Metco, IPG Photonics Corporation, Coherent Corp., Höganäs AB, Han's Laser Technology Industry Group Co., Ltd., Meltio, Laserline GmbH, 3D Systems Corporation, Eurobearings Ltd., MTU Aero Engines AG, American Cladding Technologies, Nanjing Zhongke Yu Chen Laser Technology Co., Ltd., Jinan Senfeng Laser Technology Co., Ltd., Fraunhofer Institute for Production Technology (IPT)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Laser Cladding Market Segmentation

By Laser

- Fiber Laser

- Direct Diode Laser

- CO2 Laser

- Nd:YAG Laser

- Disk Laser

By Power Output

By Process

- Powder Laser Cladding

- Wire Laser Cladding

By Material

- Nickel-based Alloys

- Cobalt-based Alloys

- Iron-based Alloys

- Carbides and Carbide Blends

- Ceramics and Cermets

- Specialty Materials

By Application

- Repair and Reconditioning

- Surface Coating

- Additive Manufacturing

- Functional Prototyping

By End-Use Industry

- Aerospace and Defense

- Oil and Gas

- Automotive and Transportation

- Mining

- Power Generation

- Medical Devices

- Industrial Machinery and Tooling

- Marine and Shipbuilding

By Revenue Stream

- System

- Laser Cladding Services

- Aftermarket and Consumables

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Laser Cladding Industry

- TRUMPF SE + Co. KG

- OC Oerlikon Management AG

- Coherent Corp.

- IPG Photonics Corporation

- Laserline GmbH

- Höganäs AB

- Jenoptik AG

- Han’s Laser Technology Industry Group Co., Ltd.

- LaserBond Ltd.

- Titanova, Inc.

- Topclad B.V.

- Hayden Corp.

- American Cladding Technologies

- Alabama Specialty Products, Inc

- KUKA AG

*- List not Exhaustive