Web Coating Equipment Market Growth Supported by Semiconductor Miniaturization and Precision Manufacturing Demand

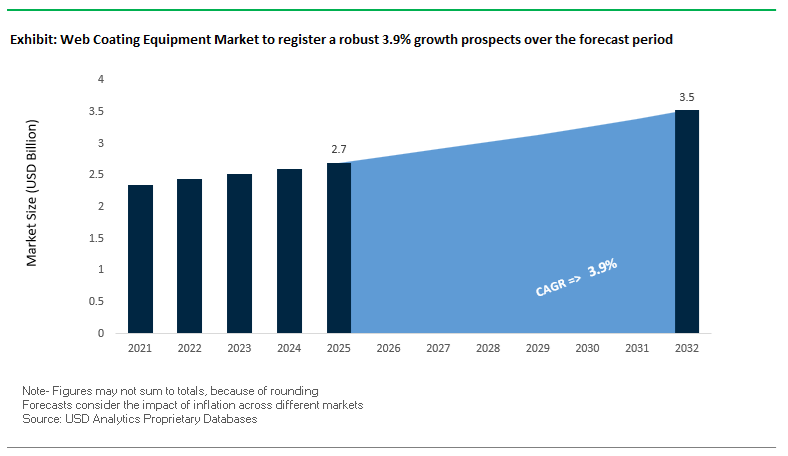

The global Web Coating Equipment Market was valued at $2.7 billion in 2025 and is projected to grow at a CAGR of 3.9% between 2025 and 2032, reaching $3.5 billion by 2032. This steady growth reflects increasing demand for high-precision coating, thin-film deposition, and roll-to-roll processing technologies across industries such as semiconductors, flexible electronics, packaging, medical devices, and energy systems.

A primary growth driver is the rapid evolution of semiconductor manufacturing, particularly the transition toward advanced nodes (sub-5nm and emerging 2nm technologies). Web coating equipment plays a critical role in enabling uniform thin-film deposition, material modification, and surface engineering, which are essential for improving transistor performance, chip density, and device efficiency. Additionally, the expansion of AI, high-performance computing (HPC), and advanced packaging technologies is accelerating demand for ultra-precise coating systems capable of operating at atomic-scale tolerances.

The market is also benefiting from the growth of energy transition technologies, including fuel cells, batteries, and hydrogen production systems. Web coating equipment is increasingly used in the production of electrodes, membranes, and bipolar plates, where consistent coating thickness and material uniformity are critical for performance and durability. Furthermore, the rise of flexible packaging, printed electronics, and medical coatings is driving demand for advanced roll-to-roll and extrusion-based coating systems that enable high throughput, reduced material waste, and scalability.

Technological advancements in automation, precision dispensing, and hybrid coating processes (such as sputtering, extrusion, and slot-die coating) are enhancing equipment efficiency and operational flexibility. Manufacturers are focusing on digital control systems, inline quality monitoring, and modular equipment architectures to improve productivity and reduce downtime.

Overall, the Web Coating Equipment Market is transitioning toward high-precision, automation-driven, and application-specific solutions, supporting next-generation manufacturing across semiconductor, energy, and advanced materials industries.

Market Analysis: Semiconductor Innovation, Strategic Acquisitions, and Automation Advancements Reshaping Market Dynamics

The Web Coating Equipment Market is undergoing a transformation driven by semiconductor innovation, strategic consolidation, and increasing automation, redefining competitive positioning across key end-use sectors. A major technological milestone is Applied Materials’ launch of 2nm logic deposition systems (February 2026) at SEMICON Korea, which introduces atomic-scale material engineering capabilities essential for next-generation semiconductor fabrication. These advancements are directly influencing the evolution of precision web and thin-film coating equipment, enabling unprecedented levels of uniformity and performance.

Complementing this, Applied Materials’ Kinex™ hybrid bonding and Xtera™ epitaxial deposition systems continue to set new benchmarks in advanced packaging and AI-driven chip architectures, reinforcing the demand for ultra-precise coating and deposition technologies. These innovations highlight the growing convergence between web coating equipment and semiconductor process engineering.

Strategic acquisitions and consolidation are also reshaping the competitive landscape. Tesla Automation’s acquisition of Manz AG assets (March 2025) strengthens its in-house capabilities for battery and electronic component coating, aligning with the rapid expansion of EV manufacturing. Similarly, Greatech Technology’s acquisition of Manz Slovakia (April 2025) enhances its footprint in automated equipment manufacturing for semiconductor and medical applications in Europe. Davis-Standard’s acquisition of FB Balzanelli (October 2025) and consolidation of its Canadian operations further demonstrate a trend toward integrated web-handling and coating system capabilities, improving global service delivery and technological integration.

Innovation in coating line technology remains a key differentiator. Von Ardenne’s launch of a fully automated bipolar plate production line (March 2025) introduces advanced magnetron sputtering techniques capable of coating both sides simultaneously, a critical advancement for fuel cell and hydrogen energy systems. Meanwhile, Davis-Standard’s recognition for extrusion and coating innovation (January 2026) underscores the importance of high-speed, precision coating lines in packaging and industrial applications.

Market players are also navigating macroeconomic and operational challenges. Nordson Corporation’s 2026 strategy emphasizes expansion in precision dispensing and coating technologies for semiconductor and medical sectors, following strong financial performance in 2025. In contrast, Bobst Group’s cautious 2026 outlook, including dividend adjustments, reflects geopolitical uncertainties and tariff pressures impacting the printing and converting equipment segment.

Market Trend: EU PPWR 2025/40 Driving Transition to Waterborne Barrier Coating Equipment

The implementation of the EU Packaging and Packaging Waste Regulation (EU) 2025/40 is fundamentally transforming the web coating equipment market, particularly by accelerating the shift toward waterborne barrier coating technologies. With full enforcement scheduled for August 12, 2026, packaging manufacturers are rapidly replacing legacy wax and polyethylene lamination lines with advanced coating systems designed for recyclable paper-based packaging.

A key regulatory driver is the strict limitation on PFAS substances in food-contact packaging, capped at less than 25 parts per billion for individual compounds as of 2026. This requirement is forcing converters to decommission conventional coating lines and invest in specialized web coating equipment capable of handling PFAS-free waterborne dispersions.

The Design for Recyclability mandate is also influencing equipment selection, as coatings must be compatible with standard hydropulping processes. This has resulted in a surge in demand for high-precision metering rod and reverse gravure coating systems optimized for low-viscosity aqueous formulations. Industry estimates indicate a 40% increase in installations of such equipment, highlighting the rapid transition toward sustainable packaging machinery and eco-friendly coating technologies.

Market Trend: U.S. DOE Industrial Decarbonization Driving Electrification of Web Coating Drying Systems

The U.S. Department of Energy Industrial Decarbonization Program is driving a major technological shift in the web coating equipment market, particularly in drying and curing systems. By 2026, more than $6 billion in federal funding has been allocated to support industrial electrification, accelerating the replacement of natural gas-fired ovens with energy-efficient alternatives.

This transition is leading to widespread adoption of near-infrared and UV-LED curing systems in web coating lines. These technologies enable faster drying cycles, reduced energy consumption, and improved process control compared to traditional convection ovens.

From an operational standpoint, electrified curing systems offer significant advantages, including a reduction in oven footprint by 30% to 50% and a decrease in energy-related carbon emissions by up to 60%. These improvements are aligning web coating operations with global net-zero targets while enhancing production efficiency. The shift toward electric curing technologies is therefore becoming a key differentiator for equipment manufacturers competing in the sustainable industrial machinery market.

Market Opportunity: Slot-Die Coating Systems Enabling High-Precision Battery Electrode Manufacturing

The rapid expansion of electric vehicle battery production is creating substantial opportunities for slot-die coating equipment in the global web coating machinery market. Slot-die coating has emerged as the preferred technology for battery electrode manufacturing due to its ability to deliver precise, uniform coatings for high-performance lithium-ion cells.

Advanced 2026 slot-die systems are achieving cross-web thickness tolerances of ±1.5% or better, ensuring consistent coating quality and preventing performance issues such as thermal hotspots in battery cells. This level of precision is critical for improving battery efficiency and safety in electric vehicles.

In addition to precision, modern slot-die equipment supports high-speed production, maintaining coating uniformity at line speeds exceeding 100 meters per minute. This represents a significant increase in throughput compared to legacy coating methods, enabling gigafactories to scale production efficiently.

Process optimization is further enhanced through patch-coating technology, which minimizes material waste by reducing edge trimming and startup losses by approximately 15%. This is particularly valuable given the high cost of battery active materials, improving overall return on investment for manufacturers.

Market Opportunity: Multi-Layer Extrusion Coating Systems Driving Advanced Flexible Packaging Solutions

The growing demand for mono-material recyclable packaging is creating new opportunities for multi-layer extrusion coating equipment in the web coating market. While sustainability goals emphasize material simplification, they also require advanced barrier performance, driving the adoption of multi-manifold extrusion die systems capable of applying multiple functional layers in a single pass.

Modern extrusion coating equipment can produce up to five-layer structures, enabling the integration of ultra-thin barrier materials such as ethylene vinyl alcohol and specialized polyamides within recyclable polyethylene substrates. These configurations achieve oxygen transmission rates below 1.0 cubic centimeters per square meter per day, meeting the stringent barrier requirements of food and pharmaceutical packaging.

Technological advancements in nano-layer extrusion are allowing manufacturers to apply functional layers as thin as 2 microns, reducing overall plastic usage by approximately 20% while maintaining packaging integrity. This contributes to both sustainability targets and cost optimization in flexible packaging production.

Operational flexibility is also improving with modular extrusion systems that reduce changeover times by up to 45%. This capability enables converters to efficiently handle smaller production runs and customized packaging formats, supporting the growing demand for personalized and just-in-time packaging solutions in sectors such as organic food and specialty consumer goods.

Web Coating Equipment Market Share and Segmentation Insights

Roll Coating Leads with 28.6% Share Due to High-Speed Efficiency and Cost Advantage

The roll coating segment dominates the web coating equipment market with a 28.6% market share in 2025, driven by its high-speed processing capability, operational simplicity, and cost efficiency. In the industrial coating equipment and continuous web processing market, roll coating methods—including reverse roll, gravure roll, and kiss roll systems—enable the application of uniform and precise coatings on substrates such as paper, plastic films, and metal foils at speeds reaching up to 1,000 meters per minute. This makes them highly suitable for packaging, label, and flexible film applications, where throughput and consistency are critical. Additionally, roll coating systems offer a lower capital investment compared to advanced technologies like slot die and extrusion coating, making them an attractive option for mid-volume converting operations. As demand grows for efficient, scalable, and cost-effective coating solutions, roll coating continues to lead the global web coating equipment market.

Packaging Industry Dominates with 43.2% Share Fueled by Flexible Packaging Expansion

The packaging segment leads the web coating equipment market with a 43.2% market share in 2025, driven by rapid growth in flexible packaging, labeling, and consumer goods applications. Within the packaging machinery and coating technology market, web coating equipment is extensively used to apply barrier coatings, adhesives, and protective lacquers to films, foils, and paper substrates, supporting industries such as food and beverage, personal care, and household products. A key growth driver is the increasing demand for high-performance packaging materials with enhanced barrier properties, including moisture resistance, oxygen barrier, and grease resistance. Additionally, packaging converters operate continuous high-speed web lines, requiring reliable and efficient coating systems such as roll, slot die, and extrusion coaters to maintain production throughput. As global demand for sustainable, lightweight, and high-barrier packaging solutions rises, the packaging industry continues to drive expansion in the web coating equipment market.

Competitive Landscape Analysis of the Web Coating Equipment Market

Nordson Leads Precision Slot-Die Coating for EV Batteries and Medical Applications

Nordson Corporation is a leading player in the web coating equipment market, reporting a 9% CAGR in its coating equipment division as of 2026. The company specializes in slot-die coating technology, with its EDI® slot dies and Premier™ coating heads enabling simultaneous application of up to three functional layers, a critical requirement in EV battery and hydrogen fuel cell manufacturing. Nordson’s closed-loop Automatic Profile Control (APC) system achieves on-spec production 3–4 times faster than traditional methods, significantly reducing material scrap. The company is also targeting medical-grade web coating systems, offering cleanroom-compatible solutions for transdermal patches and diagnostic devices.

Bobst Strengthens Flexible Packaging with Advanced Vacuum Web Coating Systems

Bobst Group SA is a major competitor in the web coating equipment market, particularly in vacuum web coating and flexible packaging solutions. Despite a 14.2% decline in overall sales in 2025, its flexible packaging segment showed resilience due to demand for water-based barrier coatings and recyclable packaging materials. In 2026, Bobst introduced the EXPERT K5 metallizer with the iMA (Integrated Metallization Assistant) for real-time production monitoring. The company is advancing AlOx and SiOx barrier coating technologies, supporting mono-material packaging recyclability. Its MASTER M5 flexo press integrates inline coating and converting, eliminating secondary processing steps and improving production efficiency.

Davis-Standard Advances Extrusion and Digital Process Control for Web Coating Systems

Davis-Standard, LLC is enhancing its position in the web coating equipment market through innovation in extrusion coating and process automation. The integration of Deacro, Brampton Engineering, and Gamma Machinery into Davis-Standard Canada strengthens its R&D capabilities in web handling and converting technologies. Its DS-eVUE process control system provides predictive maintenance and real-time feedback for high-speed barrier film production and medical tubing applications. The company is also upgrading legacy equipment with energy-efficient components to support bio-based resin processing, aligning with sustainability trends. Its 2026 industry recognition highlights its leadership in simplifying operator interfaces and improving coating line efficiency.

Applied Materials Expands Thin-Film Web Coating for Flexible Electronics and Displays

Applied Materials, Inc. is a key player in the web coating equipment market, particularly in large-area roll-to-roll coating systems for flexible electronics, OLED displays, and solar cells. The company reported USD 7.01 billion in Q1 2026 revenue and is investing in its EPIC Center to accelerate commercialization of advanced coating technologies. Its expertise in high-vacuum deposition systems supports the production of flexible substrates used in next-generation electronics and smart materials. By aligning its specialty coating assets with semiconductor systems, Applied Materials is strengthening its position in thin-film precision coating for high-growth electronics applications.

Kroenert Drives High-Throughput and Digital Twin Innovation in Web Coating Equipment

Kroenert GmbH & Co KG is innovating in the web coating equipment market with advanced high-throughput and digital solutions. The company developed a double-sided curtain coating line capable of applying functional coatings on both sides of substrates simultaneously, effectively doubling production efficiency. Kroenert is also targeting renewable energy applications, providing coating systems for solar panel backsheets and hydrogen fuel cell membranes. Its transition toward digital twin manufacturing enables operators to simulate and optimize coating processes before deployment, reducing startup risks and improving operational efficiency. This positions Kroenert as a leader in next-generation automated coating systems.

China’s Gigafactory-Scale Expansion Driving Global Web Coating Equipment Leadership

China has established itself as the global powerhouse in the web coating equipment market, primarily driven by its dominance in lithium-ion battery manufacturing and flexible electronics production. Large-scale investments in wide-web slot-die coating lines, reaching widths up to 1,600mm, are enabling high-speed electrode production for electric vehicle (EV) batteries. This industrial scale is further supported by strategic investments in the Pearl River Delta, positioning the region as a hub for advanced roll-to-roll (R2R) coating technologies.

Technological innovation is accelerating China’s competitive edge. The commercialization of intermittent coating technologies delivering precise coating weight accuracy at high line speeds is improving manufacturing efficiency. Government initiatives such as “Made in China 2025” are encouraging the localization of high-end coating equipment, reducing reliance on imports. Additionally, strict VOC recovery regulations are driving the adoption of closed-loop drying systems, aligning production with environmental standards. China’s leadership in separator film coating for EV batteries further reinforces its position as a key driver of global demand for advanced web coating solutions.

United States: Advanced Functional Coatings and AI-Integrated Equipment Innovation

The United States web coating equipment market is evolving toward high-precision, specialized applications aligned with the energy transition and semiconductor manufacturing. Significant investments under the CHIPS and Science Act are supporting the development of advanced coating equipment for flexible printed circuits and semiconductor components. The growing demand for hydrogen fuel cells is also driving the development of hybrid R2R systems that integrate coating with inline laser patterning technologies.

Innovation in automation and quality control is a defining feature of the U.S. market. AI-driven defect detection systems using high-speed imaging are enabling real-time identification of micro-defects, significantly improving production quality. The expansion of battery manufacturing facilities in the “Battery Belt” is increasing demand for next-generation anode coating equipment. Additionally, regulatory pressure under the Clean Air Act is accelerating the transition toward waterborne and UV-curable coating equipment, reducing emissions while enhancing production efficiency. Applications such as smart window films and electrochromic coatings are further expanding the scope of high-precision web coating technologies in the U.S. market.

Germany: Precision Engineering and Industry 4.0 Integration in Coating Equipment

Germany continues to lead in high-end web coating equipment through its focus on precision engineering and Industry 4.0 integration. Advanced technologies such as digital twin-enabled coating lines are enabling virtual commissioning and predictive maintenance, significantly improving operational efficiency. German manufacturers are also pioneering ultra-thin coating technologies capable of achieving sub-micron layer uniformity across wide-format substrates, which is critical for applications such as organic photovoltaics.

Sustainability is a key driver in Germany’s equipment innovation. Alignment with the EU Circular Economy Action Plan is pushing the development of systems capable of processing recycled substrates without compromising coating performance. Investments in tandem coating systems are reducing carbon footprints by enabling simultaneous multi-layer coating processes. Germany’s leadership in flexible packaging and pharmaceutical barrier films is supported by highly specialized coating equipment, while regions such as Silicon Saxony are emerging as hubs for advanced thin-film technologies in microelectronics manufacturing.

Japan: Nanotechnology Integration and Ultra-Precision Coating Systems

Japan’s web coating equipment market is defined by its emphasis on ultra-precision engineering and nanotechnology integration. Advanced curtain coating systems are being developed for applications such as multi-layered ceramic capacitors (MLCCs), which are essential for next-generation communication technologies. Innovations in tension-control systems are enabling the coating of ultra-thin substrates without deformation, a critical requirement for high-performance electronics and display technologies.

Government support from organizations such as METI is driving the development of next-generation coating equipment for emerging applications like perovskite solar cells. Japan is also investing heavily in cleanroom-certified coating lines to meet the stringent requirements of semiconductor and medical industries. Key applications include TAC film coating for flat-panel displays and advanced membrane coating for carbon capture technologies. These advancements highlight Japan’s leadership in high-precision, high-value web coating equipment solutions.

South Korea: High-Density Battery Coating and Semiconductor Equipment Growth

South Korea is emerging as a global leader in advanced web coating equipment, particularly in the battery and semiconductor sectors. The country’s “K-Battery” initiative is driving the development of dual-layer slot-die coating technologies, enabling the simultaneous application of multiple materials to improve battery energy density. This innovation is critical for next-generation EV batteries and energy storage systems.

Technological advancements in high-speed vacuum drying are addressing key manufacturing challenges, such as preventing defects in thick-film coatings. Significant investments by major companies are expanding production capacity for wide-web R2R coating equipment to meet global demand. South Korea is also a leading supplier of coating equipment for polarizing films used in advanced display technologies such as OLED and QLED. Government-backed initiatives such as the “K-Semiconductor Strategy” are further supporting the development of domestic coating equipment capabilities, reinforcing the country’s position in high-tech manufacturing.

India: Emerging Manufacturing Hub for Web Coating Equipment

India is rapidly transitioning from a net importer to a growing manufacturing hub in the web coating equipment market, driven by industrialization and government support. Initiatives such as the Production Linked Incentive (PLI) scheme for advanced battery storage are accelerating the localization of coating equipment manufacturing. The development of Electronic Manufacturing Clusters (EMCs) is further supporting the integration of high-speed coating and lamination technologies in the electronics sector.

Market trends indicate a strong shift toward sustainable manufacturing, with increasing adoption of water-based coating equipment in industries such as textiles and flexible packaging. The entry of global OEMs into the Indian market is enhancing local capabilities by establishing assembly and service centers, reducing lead times and improving accessibility. Key application areas include solar backsheet coating and agricultural film production, both of which are experiencing rapid growth. Regulatory pressure from environmental authorities is also encouraging the upgrade of legacy systems to modern, energy-efficient coating equipment, further driving market expansion.

Switzerland: Precision Micro-Coating and Medical Application Leadership

Switzerland occupies a unique niche in the global web coating equipment market, specializing in high-precision, low-volume applications for medical and pharmaceutical industries. The development of micro-gravure coating systems is enabling the production of advanced transdermal drug delivery patches, where precise dosage control is critical. These technologies highlight Switzerland’s expertise in ultra-precision manufacturing.

Innovation is centered on quality assurance and advanced inspection systems, including non-contact thickness measurement technologies that ensure complete product validation at the micron level. Switzerland is also leading in coating equipment for biosensor production and diagnostic strips, supporting the growth of healthcare and point-of-care testing markets. Additional applications include security printing and advanced membrane coating for water purification systems. Strict regulatory compliance with Swissmedic and FDA standards ensures that all equipment meets rigorous validation requirements, reinforcing Switzerland’s leadership in high-value, specialized coating equipment solutions.

Web Coating Equipment Market Report Scope

Web Coating Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2032)

|

$3.5 Billion

|

|

Market Growth Rate

|

3.9%

|

|

Segments

|

By Coating Method (Slot Die Coating, Roll Coating, Extrusion Coating, Curtain Coating, Dip Coating, Spray Coating, Comma Coating), By Substrate Type (Film and Thin Plastics, Paper and Paperboard, Foil, Non-wovens and Textiles, Composites), By Degree of Automation (Automatic Web Coating Lines, Semi-Automatic Equipment, Manual), By Equipment Configuration (Stand-alone Coating Stations, Integrated Turnkey Lines, Modular Coating Units), By Drying and Curing Technology (Thermal, UV, Infrared), By End-User Industry (Packaging, Electronics, Energy, Medical and Pharmaceutical, Automotive, Textile and Leather)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nordson Corporation, Dürr Group, Applied Materials, Inc., Bühler Group, Bobst Group SA, KROENERT GmbH and Co KG, Davis-Standard, LLC, New Era Converting Machinery, Inc., Yasui Seiki Co., Ltd., Coatema Coating Machinery GmbH, Toray Engineering Co., Ltd., Mirwec Coating, Hirano Tecseed Co., Ltd., Dongjin Semichem Co., Ltd., Webcontrol Machinery Corp.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Web Coating Equipment Market Segmentation

By Coating Method

- Slot Die Coating

- Roll Coating

- Extrusion Coating

- Curtain Coating

- Dip Coating

- Spray Coating

- Comma Coating

By Substrate Type

- Film and Thin Plastics

- Paper and Paperboard

- Foil

- Non-wovens and Textiles

- Composites

By Degree of Automation

- Automatic Web Coating Lines

- Semi-Automatic Equipment

- Manual

By Equipment Configuration

- Stand-alone Coating Stations

- Integrated Turnkey Lines

- Modular Coating Units

By Drying and Curing Technology

By End-User Industry

- Packaging

- Electronics

- Energy

- Medical and Pharmaceutical

- Automotive

- Textile and Leather

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Web Coating Equipment Industry

- Nordson Corporation

- Dürr Group

- Applied Materials, Inc.

- Bühler Group

- Bobst Group SA

- KROENERT GmbH & Co KG

- Davis-Standard, LLC

- New Era Converting Machinery, Inc.

- Yasui Seiki Co., Ltd.

- Coatema Coating Machinery GmbH

- Toray Engineering Co., Ltd.

- Mirwec Coating

- Hirano Tecseed Co., Ltd.

- Dongjin Semichem Co., Ltd.

- Webcontrol Machinery Corp.

*- List not Exhaustive