Optical Coating Equipment Market Size, Thin-Film Deposition Systems, and Precision Optics Manufacturing Outlook

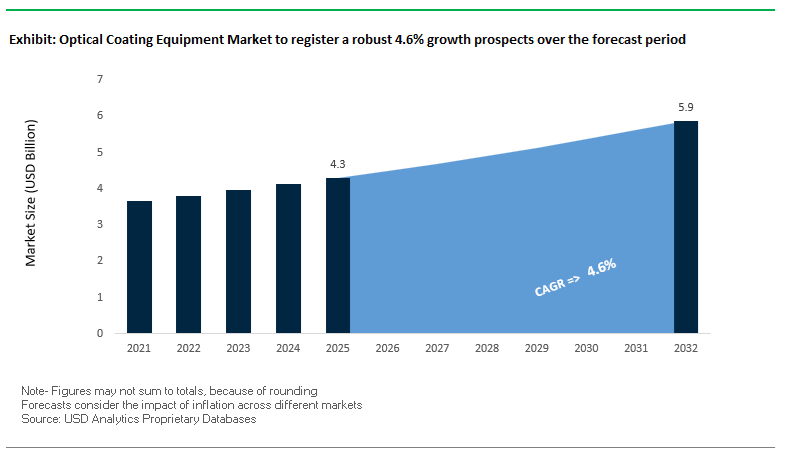

The global optical coating equipment market was valued at $4.3 billion in 2025 and is projected to reach $5.9 billion by 2032, expanding at a CAGR of 4.6%. Growth is driven by rising demand for thin-film deposition equipment, ion beam sputtering (IBS) systems, atomic layer deposition (ALD) tools, spin coating systems, and high-vacuum evaporation equipment across semiconductors, photonics, AR/VR optics, MEMS, and precision lens manufacturing. These systems are critical for producing anti-reflective (AR) coatings, optical filters, dielectric mirrors, and high-precision photonic components.

A key growth driver is the rapid advancement of semiconductor lithography, AR/VR devices, and optical communication systems, where coating precision at the nanometer and sub-nanometer scale is essential. Increasing demand for extreme ultraviolet (EUV) lithography optics, photonic sensors, and waveguide displays is pushing manufacturers toward high-accuracy, repeatable, and scalable coating equipment. Additionally, the expansion of consumer electronics, automotive LiDAR systems, and medical optics is further accelerating adoption.

The market is also benefiting from advancements in process automation, integrated deposition-inspection workflows, and sustainable manufacturing technologies, which improve yield, throughput, and energy efficiency. Regionally, Asia-Pacific dominates due to strong semiconductor and electronics manufacturing, while Europe and North America lead in high-end optical equipment innovation and R&D.

Market Analysis: Ion Beam Precision, MEMS Expansion, and AR/VR Optics Driving Equipment Innovation

The optical coating equipment industry is undergoing significant transformation driven by technological innovation, strategic consolidation, and expanding applications in next-generation photonics and semiconductor manufacturing. In February 2026, Veeco Instruments announced a merger with Axcelis Technologies, combining expertise in Ion Beam Sputtering (IBS) with advanced high-energy processing capabilities. This consolidation is expected to strengthen capabilities in laser optics, semiconductor devices, and precision coating systems.

Precision manufacturing technologies are seeing strong demand growth. Bühler Leybold Optics reported record orders in January 2026 for its Ion Beam Figuring (IBF) technology, driven by demand from the semiconductor lithography sector, where sub-nanometer surface accuracy is required for EUV optics. This highlights the increasing importance of ultra-precision finishing technologies in enabling next-generation chip fabrication.

Strategic partnerships are accelerating innovation in MEMS and photonics packaging. In March 2026, Evatec AG partnered with C2MI to deploy CLUSTERLINE® 300 systems, expanding capabilities in thin-film processing for MEMS and advanced optical packaging. Additionally, Evatec’s collaborations with Silicon Austria Labs and Qualcomm Technologies (November 2024) on PEALD (Plasma Enhanced Atomic Layer Deposition) are advancing the production of RFFE components and optical filters, critical for high-frequency communication systems.

Product innovation is also targeting broader market accessibility and precision control. Coburn Technologies’ January 2026 launch of the Velocity LTE spin coating system provides semi-automated, high-precision coating solutions for ophthalmic lenses and industrial applications, enabling smaller labs to achieve consistent coating quality. Meanwhile, Shincron’s November 2025 roadmap focuses on high-vacuum evaporation systems optimized for mass production of AR/VR waveguide optics, addressing the growing demand for immersive display technologies.

Sustainability and operational efficiency are becoming increasingly important. Evatec achieved validation for its science-based emissions reduction targets in May 2025, positioning itself as a leader in low-carbon manufacturing for coating equipment. Its recognition as an “Excellent Supplier” by Silex further underscores the importance of reliable deposition systems in high-volume MEMS and sensor production.

Integration of manufacturing workflows is also enhancing production efficiency. Evatec’s September 2024 collaboration with Onto Innovation focuses on combining deposition and inspection processes for panel-level packaging, improving yield and reducing defects in optoelectronics manufacturing.

Regional expansion strategies continue to strengthen market positioning. Bühler Group’s April 2024 expansion in China supports the growing demand for optical coatings in smartphone lenses and display technologies, reinforcing Asia-Pacific’s dominance in electronics manufacturing.

Market Trend: Ion Beam Sputtering Equipment Advancing LiDAR Optical Coatings for Autonomous Vehicles

The optical coating equipment industry is witnessing accelerated adoption of ion beam sputtering technology in automotive LiDAR systems, driven by the stringent performance requirements of Level 3 and higher autonomous driving platforms. As LiDAR systems increasingly operate at 1550 nm wavelengths, maintaining high signal-to-noise ratios and minimizing optical losses has become critical, positioning IBS coating equipment as a preferred solution for precision optical components.

IBS systems enable the production of ultra-low reflectance anti-reflective coatings, achieving residual reflectance values below 0.005%. This level of optical performance is essential for minimizing back-reflections that can interfere with detector sensitivity in high-resolution LiDAR modules. The dense film structure produced by IBS, typically in the range of 2.2 to 2.3 g/cm³ for silica layers, eliminates porosity-related issues such as moisture absorption and spectral drift. As a result, IBS-coated optics demonstrate exceptional environmental stability, with less than 0.1% spectral shift across extreme temperature cycles from −40°C to +105°C, meeting automotive-grade reliability standards.

Laser durability is another critical performance parameter. IBS coatings support laser damage thresholds exceeding 4 GW/cm² under pulsed laser conditions, ensuring long-term reliability of LiDAR transmitters and optical windows over vehicle lifetimes exceeding 15 years. These characteristics are driving strong demand for IBS optical coating equipment in advanced driver-assistance systems and autonomous vehicle platforms, where optical precision and durability are non-negotiable.

Market Trend: Magnetron Sputtering Systems Scaling AR Coating Production in Consumer Electronics Displays and Cameras

Consumer electronics manufacturing is driving a parallel shift toward magnetron sputtering equipment for high-volume optical coating applications, particularly in anti-reflective coatings for displays and camera lenses. As device manufacturers push for higher durability, optical clarity, and production efficiency, magnetron sputtering is increasingly replacing traditional electron-beam evaporation systems in mass production environments.

Throughput advantages are a primary driver of this transition. In-line magnetron sputtering systems achieve cycle times that are 40% to 60% faster than high-capacity e-beam coaters for standard multi-layer AR stacks. This improvement is largely attributed to the elimination of lengthy cooling and vacuum venting cycles, enabling continuous production workflows that are critical for large-scale electronics manufacturing.

Mechanical durability of sputtered films is significantly higher compared to conventional coatings. Magnetron-deposited films exhibit five to ten times greater abrasion resistance, meeting stringent standards such as MIL-C-48497A for severe wear conditions. This is particularly important for smartphone displays and camera optics, which are subject to frequent mechanical contact and environmental exposure.

Uniformity control is another key advantage. Advanced magnetron sputtering systems maintain thickness uniformity within ±0.5% across large substrates, including Gen 5 glass panels used in display manufacturing. This precision ensures consistent optical performance across large production batches, reducing defect rates and improving yield. As consumer electronics continue to scale in volume and complexity, magnetron sputtering equipment is becoming a core technology for high-throughput, high-precision optical coating production.

Market Opportunity: US CHIPS and Science Act Driving Investment in Advanced Optical Coating Equipment for Semiconductor Lithography

The implementation of the US CHIPS and Science Act is creating a substantial growth opportunity for optical coating equipment manufacturers, particularly those serving the semiconductor and advanced optics sectors. With significant federal funding and incentives directed toward domestic semiconductor manufacturing, demand for high-precision coating equipment is increasing across the supply chain.

The legislation provides a 25% investment tax credit for capital equipment used in semiconductor fabrication, including vacuum coating systems for lithography optics and EUV mask production. This financial support is accelerating the procurement of advanced coating technologies, particularly those capable of meeting the extreme precision requirements of next-generation semiconductor processes.

EUV lithography presents unique technical challenges that are driving innovation in coating equipment. Reflective multilayer coatings, typically based on molybdenum-silicon structures, must achieve reflectivity levels above 70% at 13.5 nm wavelengths while maintaining surface roughness below 0.1 nm RMS. Achieving these specifications requires highly controlled deposition environments and advanced process monitoring capabilities, creating demand for next-generation IBS and magnetron sputtering systems.

The convergence of federal funding, technological complexity, and semiconductor scaling is positioning optical coating equipment as a critical enabler of advanced chip manufacturing, creating long-term opportunities for equipment suppliers with expertise in ultra-precision deposition technologies.

Market Opportunity: China MIIT Localization Strategy Accelerating Domestic Demand for Optical Coating Equipment

China’s Ministry of Industry and Information Technology is driving a strategic push toward domestic production of high-end optical coating equipment under its 2026 to 2030 industrial development plan. This initiative identifies optical coating systems as a core industrial technology, with a focus on reducing reliance on imported equipment and strengthening local supply chains.

The plan sets ambitious targets to increase the localization rate of advanced coating equipment, including IBS and magnetron sputtering systems, from approximately 30% to more than 60% by 2030. This shift is creating significant opportunities for domestic equipment manufacturers, particularly those developing critical subsystems such as broadband optical monitoring solutions and high-power ion sources.

Government support mechanisms are reinforcing this transition. Under the “Little Giant” program, companies focusing on strategic technologies are eligible for subsidies covering up to 30% of research and development expenditures. This financial backing is accelerating innovation and enabling local firms to compete with established global suppliers.

The rapid expansion of China’s new energy vehicle and consumer electronics sectors further amplifies demand for optical coating equipment. With annual production of new energy vehicles exceeding 10 million units, the need for locally sourced LiDAR sensors and optical components is increasing. This is creating a domestic backlog for coating equipment that aligns with national industrial policy and reduces exposure to international trade restrictions. These combined factors position China as a major growth engine for the optical coating equipment industry over the coming decade.

Optical Coating Equipment Market Share and Segmentation Insights

Vacuum Coaters Capture 35.6% Share Driven by Broad Application Range and Lower Capital Investment

The optical coating equipment market by equipment type is led by vacuum coaters, accounting for 35.6% of the global market share in 2025, due to their unmatched versatility and cost-effectiveness in optical thin-film deposition. These systems, including thermal evaporation and electron-beam (e-beam) vacuum coaters, are widely used to produce anti-reflective coatings, high-reflective mirrors, bandpass filters, and beam splitters across industries such as optics, photonics, display technologies, and precision lenses. A key advantage is their broad material compatibility, enabling deposition of a wide range of dielectric and metallic layers. Additionally, vacuum coaters offer lower capital expenditure and maintenance costs compared to high-power sputtering systems, making them highly attractive for both R&D environments and small-to-medium scale production. This balance of flexibility and affordability reinforces their dominance in the global optical coating equipment market.

Industrial Scale Systems Hold 62.7% Share Driven by Mass Production of Consumer Optics and Electronics

In the optical coating equipment market by system configuration, industrial-scale systems dominate with a 62.7% market share in 2025, reflecting the growing demand for high-volume optical component manufacturing. These large-scale systems are essential for producing smartphone camera lenses, eyewear, flat-panel displays, and automotive head-up display (HUD) optics, all of which require multi-layer thin-film coatings with high precision and repeatability. Industrial coaters feature large vacuum chambers (1.5–2.5 meters in diameter), automated loading systems, and continuous process control, enabling efficient mass production. The rapid expansion of the consumer electronics and mobile device market, particularly the demand for anti-reflective coatings and IR-cut filters, continues to drive investment in industrial-scale equipment. As a result, industrial systems remain the backbone of the global optical coating equipment industry, supporting scalable and cost-efficient production.

Competitive Landscape of the Optical Coating Equipment Market

Bühler Group Strengthens Optical Coating Leadership with AI-Driven Deposition Systems

Bühler Group’s Leybold Optics division remains a global benchmark in high-vacuum optical coating equipment, particularly for eyewear and precision optics applications. Despite a 15.2% decline in advanced materials orders in 2026, the company maintained profitability through its customer service segment, contributing 38.3% of total revenue. Bühler is advancing its HELIOS and SYRUS platforms with AI-driven process control, reducing particulate defects by 40% and improving production efficiency. With an installed base of over 30,000 machines, the company benefits from recurring revenue through long-term service agreements. Its leadership in anti-reflective and filter coating technologies positions it strongly in the growing ophthalmic lens market.

Evatec Leads Thin-Film Innovation with High-Throughput Wafer-Level Coating Solutions

Evatec AG is a key innovator in the thin-film deposition equipment market, specializing in wafer-level optics and MicroLED manufacturing. In 2026, the company introduced the CLUSTERLINE® 200 platform, enabling high-volume production with exceptional film uniformity for advanced photonics and RF filters. Its HEXAGON platform incorporates Arctic Etch technology, enhancing reliability for fan-out wafer-level packaging in high-performance chips. The BAK system family has surpassed 2,000 installations, offering flexible multilayer coating capabilities. Additionally, the SOLARIS® inline sputter system supports ultra-high throughput of up to 1,200 pieces per hour, positioning Evatec as a leader in mass-scale optical coating and semiconductor integration technologies.

Optorun Expands Global Footprint with Semiconductor-Driven Optical Coating Equipment Growth

Optorun Co., Ltd. is a major supplier in the optical coating equipment market, particularly for smartphone and EV manufacturing ecosystems. The company forecasts revenues exceeding ¥53.2 billion in 2026, supported by a 43% recovery in optical component demand. Its strategic transition into a silicon photonics-focused enterprise highlights its commitment to next-generation technologies. Optorun is investing ¥21.6 billion to expand production across Asia, mitigating geopolitical risks and strengthening supply chains. Notably, its ALD equipment segment has experienced a 71% growth surge, driven by demand for sub-nanometer precision coatings in semiconductor manufacturing, reinforcing its position in advanced coating equipment solutions.

Veeco Instruments Drives Advanced Optical Coating Capabilities with Ion Beam Technologies

Veeco Instruments Inc. is a leader in ion beam sputtering and MOCVD technologies, critical for high-performance optical and telecommunications components. In 2026, the company advanced its market position through a merger with Axcelis Technologies, creating a strong platform for next-generation power electronics and optical systems. Veeco secured major orders for its Lumina and Spector® platforms, supporting the production of indium-phosphide-based components for high-speed data centers. Its Spector® IBS system is widely recognized for delivering low-loss, high-durability optical coatings used in aerospace and defense. Additionally, Veeco is innovating in metasurface waveguide fabrication, enabling enhanced AR/VR device performance.

Shincron Advances Precision Thin-Film Deposition with Next-Generation Sputtering Technology

Shincron Co., Ltd. is a pioneer in vacuum thin-film deposition equipment, known for its high-reliability sputtering and radical assisted sputtering (RAS) technologies. In 2026, the company launched a next-generation sputtering system designed for high-precision crystalline thin films, addressing demand for advanced materials like AlScN in sensors and piezoelectric devices. Shincron plays a crucial role in automotive applications, particularly in coatings for displays and head-up display systems requiring zero-defect performance. Its proprietary RAS technology enables low-temperature deposition of dense optical films, supporting flexible electronics and wearable devices. With a strong global support network, Shincron ensures minimal downtime in high-volume optical manufacturing environments.

China Optical Coating Equipment Market: Display Manufacturing Scale and Photonics Self-Reliance

China is rapidly emerging as a global leader in optical coating equipment, transitioning from a major consumer to a producer of advanced deposition systems. The development of Gen 10.5 PECVD equipment, capable of achieving ±2% thickness uniformity on large 3-meter glass substrates, is enabling mass production for OLED display leaders like BOE.

Government-backed initiatives such as the “Photonics Valley” program in Wuhan—supported by over $15 billion in investment—are accelerating domestic capabilities in lithography and thin-film equipment. The market is also benefiting from strong demand in renewable energy, particularly anti-reflective coating systems for bifacial solar glass, aligned with China’s target of 1,200 GW renewable capacity. Regulatory policies like Green Vacuum Standards 2026 are driving the shift toward energy-efficient vacuum technologies, while innovations such as inline sputtering systems for ITO alternatives are strengthening supply chain independence.

United States Optical Coating Equipment Market: Defense Photonics and Semiconductor Reshoring

The United States leads in high-end optical coating equipment, particularly for defense, aerospace, and semiconductor applications. Investments under the CHIPS and Science Act have triggered over $1.2 billion in new infrastructure for ion-beam sputtering (IBS) and e-beam evaporation systems, supporting next-generation photonics and satellite optics.

Technological advancements include real-time broadband monitoring systems, enabling precise control of multi-layer coatings exceeding 200 layers. The U.S. is also pioneering equipment for directed-energy (laser weapon) optics, requiring extreme precision and durability. Regulatory initiatives such as the DoD’s Critical Materials mandate are pushing optimization in rare-earth material usage. Expansion by companies like Optimax and NACL highlights the country’s focus on infrared and night-vision optical coating systems, reinforcing leadership in defense photonics.

Germany Optical Coating Equipment Market: Precision Engineering and Industry 4.0 Integration

Germany remains the global benchmark for precision optical coating equipment, driven by its expertise in vacuum engineering and Industry 4.0 integration. Innovations such as Bühler Leybold’s Helios 2026 system incorporate AI-driven predictive maintenance, reducing downtime by up to 18% in high-volume operations.

Technological advancements include the use of digital twin simulations to optimize deposition processes and particle behavior within vacuum chambers. Germany is also investing in roll-to-roll (R2R) sputtering systems for flexible electronics, supported by research institutions like Fraunhofer. Key applications include interference filter coating systems for medical imaging and endoscopy, where precision is critical. Government incentives for energy efficiency and compliance with REACH 2026 regulations are further driving innovation in sustainable coating equipment.

Japan Optical Coating Equipment Market: Ultra-Precision and Deep-UV Innovation Leadership

Japan’s market is defined by its leadership in ultra-precision optical coating equipment, particularly for UV and deep-UV (DUV) applications. The development of ultra-low-loss mirror coating systems, achieving reflectivity above 99.999%, is enabling cutting-edge applications such as gravity-wave detection and advanced lithography.

Major players like Nikon and Canon are investing heavily in atomic-level coating technologies to support next-generation semiconductor manufacturing at the 2 nm node. Japan is also advancing equipment for AR/VR waveguide coatings, enabling high-refractive-index deposition on plastic substrates. Government initiatives under Society 5.0 are promoting IoT-enabled smart coating systems, while milestones such as 10 wafers/hour throughput in ALD systems highlight Japan’s efficiency leadership in advanced photonics manufacturing.

South Korea Optical Coating Equipment Market: OLED and Energy Storage Innovation Hub

South Korea is leveraging its dominance in OLED displays and EV battery technologies to drive innovation in optical coating equipment. The deployment of hybrid thin-film encapsulation (TFE) systems, combining ALD and inkjet printing, is significantly extending the lifespan of foldable OLED displays.

Technological breakthroughs such as the K-ALD system are enabling high-speed coating of EV battery separators with nano-ceramic layers, improving safety and thermal performance. The country is also advancing equipment for 6G photonic integrated circuits, requiring deposition precision of ±1 nm. Government initiatives like the K-Semiconductor Belt strategy are supporting domestic development of advanced sputtering systems. Infrastructure investments in display equipment clusters, such as in Asan, are reinforcing South Korea’s role as a global innovation hub.

Taiwan Optical Coating Equipment Market: Semiconductor Precision and High-Throughput Innovation

Taiwan’s optical coating equipment market is heavily driven by its semiconductor and CMOS image sensor (CIS) industries, requiring ultra-clean, high-precision deposition technologies. Investments by companies like TSMC are focusing on in-situ monitoring systems, reducing wafer defects and improving yield in advanced chip manufacturing.

Technological advancements include dual-ion source sputtering systems, enabling precise coating of optical interposers used in AI chip packaging. Key applications include anti-reflective and NIR-cut coatings for automotive sensors, applied at the wafer level. Regulatory initiatives under the Green Foundry 2026 framework are promoting material recovery and sustainability. Infrastructure expansion in Hsinchu Science Park is further strengthening Taiwan’s leadership in high-throughput, precision optical coating equipment.

Optical Coating Equipment Market Report Scope

Optical Coating Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.3 Billion

|

|

Market Size (2032)

|

$5.9 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Deposition Technology (Physical Vapor Deposition, Chemical Vapor Deposition, Atomic Layer Deposition, Advanced Plasma Reactive Sputtering), By Equipment Type (Vacuum Coaters, Sputtering Systems, Box Coaters, In-line Coaters, Batch Coaters, Cluster Tools), By Coating Function (Anti-Reflective, High-Reflective, Filter Coating Systems, Beam Splitter Coating Systems, Transparent Conductive Coating, Electrochromic and Photochromic Coating Systems), By Substrate Compatibility (Glass, Plastics, Metals, Infrared, Semiconductor Wafers), By Application (Consumer Electronics, Semiconductors and Photonics, Automotive, Aerospace and Defense, Solar Energy, Medical and Healthcare, Telecommunications, AR), By System Configuration (Industrial Scale Systems, R and D, Pilot Plant Systems)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Bühler Group, Optorun Co., Ltd., Shincron Co., Ltd., Evatec AG, ULVAC, Inc., Veeco Instruments Inc., Satisloh AG, Mustang Vacuum Systems, Solayer GmbH, Von Ardenne GmbH, Denton Vacuum, LLC, Coburn Technologies, Inc., Plasma-Therm LLC, BOC Edwards, OptoTech Optikmaschinen GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Optical Coating Equipment Market Segmentation

By Deposition Technology

- Physical Vapor Deposition

- Thermal Evaporation

- Electron Beam

- Ion-Assisted Deposition

- Ion Beam Sputtering

- Magnetron Sputtering

- Chemical Vapor Deposition

- Plasma-Enhanced CVD

- Low-Pressure CVD

- Atomic Layer Deposition

- Advanced Plasma Reactive Sputtering

By Equipment Type

- Vacuum Coaters

- Sputtering Systems

- Box Coaters

- In-line Coaters

- Batch Coaters

- Cluster Tools

By Coating Function

- Anti-Reflective

- High-Reflective

- Filter Coating Systems

- Beam Splitter Coating Systems

- Transparent Conductive Coating

- Electrochromic and Photochromic Coating Systems

By Substrate Compatibility

- Glass

- Plastics

- Metals

- Infrared

- Semiconductor Wafers

By Application

- Consumer Electronics

- Semiconductors and Photonics

- Automotive

- Aerospace and Defense

- Solar Energy

- Medical and Healthcare

- Telecommunications

- AR

By System Configuration

- Industrial Scale Systems

- R and D

- Pilot Plant Systems

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Optical Coating Equipment Industry

- Bühler Group

- Optorun Co., Ltd.

- Shincron Co., Ltd.

- Evatec AG

- ULVAC, Inc.

- Veeco Instruments Inc.

- Satisloh AG

- Mustang Vacuum Systems

- Solayer GmbH

- Von Ardenne GmbH

- Denton Vacuum, LLC

- Coburn Technologies, Inc.

- Plasma-Therm LLC

- BOC Edwards

- OptoTech Optikmaschinen GmbH

*- List not Exhaustive