Digitized Surface Engineering and Aerospace Demand Driving Steady Expansion

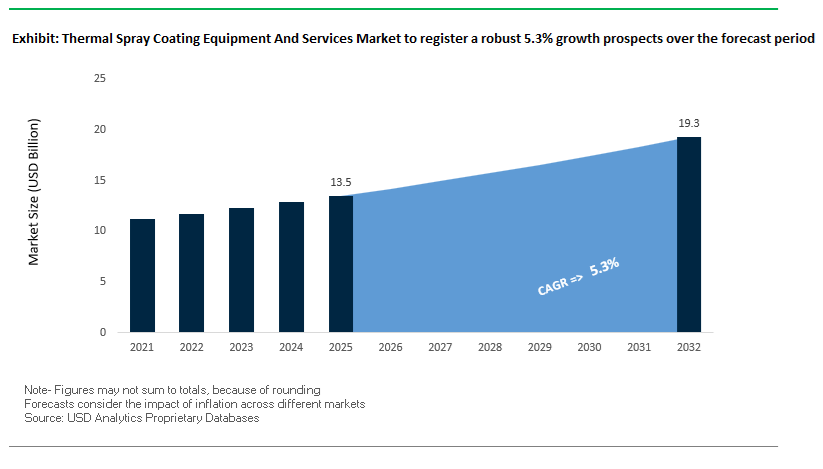

The global Thermal Spray Coating Equipment and Services Market is expanding steadily, driven by increasing demand for advanced surface engineering solutions across aerospace, energy, medical devices, and heavy industry. The market was valued at $13.5 billion in 2025 and is projected to reach $19.4 billion by 2032, growing at a CAGR of 5.3% during 2025–2032. This growth reflects the critical role of thermal spray technologies in enhancing component durability, wear resistance, corrosion protection, and thermal insulation in high-performance environments.

A primary structural driver is the rising demand for thermal barrier coatings (TBCs) and wear-resistant surfaces in aerospace and power generation. Technologies such as plasma spraying, high-velocity oxy-fuel (HVOF), and cold spray systems are widely used to apply ceramic, metallic, and cermet coatings that extend component lifespans and improve efficiency. As turbine engines and industrial equipment operate at increasingly higher temperatures and stress levels, thermal spray solutions are becoming indispensable for performance optimization and lifecycle cost reduction.

Another key trend is the rapid adoption of digitalized and automated coating systems, integrating Industrial Internet of Things (IIoT) capabilities for real-time monitoring and process control. These systems enable manufacturers to achieve greater precision, consistency, and scalability, particularly in high-volume aerospace production. Additionally, the expansion of medical applications, including orthopedic and dental implants, is driving demand for biocompatible coating materials and high-purity powder systems.

The market is also witnessing increasing demand for outsourced coating services, as companies seek specialized expertise and capital-efficient solutions. Service providers offering end-to-end coating solutions, including surface preparation, coating application, and post-treatment, are gaining traction, particularly in regions with strong aerospace and industrial manufacturing ecosystems.

Market Analysis: IIoT-Enabled Platforms, Aerospace Capacity Expansion, and Strategic Acquisitions Reshaping Competitive Landscape

The thermal spray coating equipment and services market is undergoing transformation through digital innovation, capacity expansion, and consolidation-driven growth, reflecting the increasing complexity of advanced coating applications. In March 2026, Oerlikon Metco expanded its MyMetco digital platform to include the full MetcoMed™ materials portfolio, enabling medical device manufacturers to directly procure high-purity thermal spray powders. This move enhances supply chain efficiency and supports the growing demand for biocompatible surface coatings.

Digitalization is a major competitive differentiator. Oerlikon’s Surface Two™ platform (July 2025) introduces a scalable, IIoT-enabled thermal spray system that provides real-time process monitoring and automation, reducing variability and improving coating consistency. This platform is further supported by ATL Turbine Services’ November 2025 investment, which integrates the system into production lines to achieve process excellence in turbine component coatings.

Capacity expansion is strengthening service capabilities in key industries. Praxair Surface Technologies (Linde) completed a February 2026 expansion of its North American facility, adding high-capacity HVOF and plasma spray lines to meet growing demand from aerospace and energy sectors. This investment highlights the increasing scale and complexity of next-generation turbine components.

Strategic acquisitions are consolidating market leadership. Bodycote’s February 2026 acquisition of Spectrum Thermal Processing enhances its presence in the U.S. aerospace and defense corridor, while its January 2026 launch of a precision thermal spray service line focuses on advanced cermet coatings for mission-critical applications. Additionally, the integration of Ellison Surface Technologies (2024–2025) further strengthens Bodycote’s position as a global leader in surface engineering services.

Material innovation is also advancing. Wall Colmonoy’s May 2025 scaling of nickel, cobalt, and iron-based hardfacing alloys improves powder flowability and performance in automated spray systems, supporting the transition toward high-efficiency, automated coating processes.

Infrastructure investments are supporting long-term innovation. Oerlikon’s June 2024 opening of an Advanced Coating Technology Center in Westbury, NY provides a dedicated hub for R&D and specialized coating services, particularly for aerospace and power generation applications. Furthermore, the Oerlikon–MTU Aero Engines partnership (July 2024) to establish a smart thermal spray factory underscores the industry’s move toward standardized, digitized coating production for next-generation engine programs.

Market Trend: FAA and SAE AMS 2439/2440 ESA Mandates Drive Digitalization of Thermal Spray Equipment

The 2025 updates to AMS 2439 and AMS 2440 have fundamentally redefined process control requirements in aerospace thermal spray operations by elevating Equipment System Accuracy from a recommended practice to a mandatory certification criterion. Under 2026 enforcement, coating systems must maintain mass flow and powder feed precision within ±1% of set parameters, supported by continuous, time-stamped digital logging. This requirement is accelerating the retirement of manual and semi-automated spray systems that lack integrated data acquisition capabilities. Tier-1 aerospace repair stations are increasingly standardizing on fully digital, sensor-driven platforms that enable real-time monitoring of gas flow, particle velocity, and deposition rates. The operational impact is substantial, with validated reductions of approximately 35% in bond strength variability across coated components. This improvement directly addresses historical issues of adhesion drift in rotating turbine parts, where inconsistency previously led to elevated rejection rates and rework costs. As certification frameworks prioritize traceability and reproducibility, digital process control is becoming a core differentiator in the thermal spray equipment and services market.

Market Trend: EU REACH Annex XVII Cobalt Restrictions Accelerate Shift Toward Cobalt-Free Thermal Spray Powders

The regulatory classification of cobalt as a Category 1B carcinogen under EU REACH is driving a significant material transition within the thermal spray coatings ecosystem. Effective August 29, 2026, facilities using tungsten carbide-cobalt powders must comply with stringent emission control protocols, including the deployment of HEPA-grade filtration systems capable of capturing 99.99% of airborne particulates at the source. These requirements are increasing operational complexity and cost, particularly for legacy facilities designed around cobalt-based systems. In response, the industry is witnessing a rapid shift toward cobalt-free “green powder” alternatives, including tungsten carbide-nickel-molybdenum-chromium blends and iron-based amorphous alloys. Adoption of these materials has increased by approximately 40% in 2026, particularly in sectors such as mining and hydraulics where worker exposure risks are highest. This transition is not only compliance-driven but is also influencing performance optimization strategies, as manufacturers seek to match or exceed the wear resistance and toughness traditionally associated with WC-Co systems. The cobalt restriction is therefore acting as a catalyst for both material innovation and process redesign across the thermal spray coatings industry.

Market Opportunity: Robotic HVOF Systems Enhance Productivity and Coating Integrity for Large-Bore Engine Components

Robotic High-Velocity Oxygen Fuel systems are emerging as a critical solution for coating large-bore diesel engine components in maritime and power generation sectors. The shift away from hard chrome plating is driven by both environmental regulations and the superior performance characteristics of HVOF-applied coatings. In 2026, robotic systems equipped with pre-programmed spray trajectories are achieving highly uniform coating deposition, with porosity levels below 0.5%. This near-dense microstructure significantly reduces the risk of pinhole corrosion, which is a common failure mode in high-pressure engine environments. Additionally, tungsten carbide-nickel chromium coatings applied via robotic HVOF demonstrate up to four times longer service life compared to traditional chrome plating, particularly in engines operating with high-sulfur alternative fuels that accelerate wear. Automation also delivers measurable productivity gains, with coating cycle times reduced by approximately 25% relative to semi-automated systems. This reduction in processing time directly translates to shorter dry-dock durations for commercial vessels, improving asset utilization and operational efficiency. As industries seek to optimize both performance and throughput, robotic HVOF systems are becoming a cornerstone technology in advanced thermal spray applications.

Market Opportunity: Cold Spray Technology Expands Structural Repair Capabilities for Lightweight Aerospace Components

Cold Spray technology is rapidly gaining adoption as a high-performance repair solution in aerospace and defense maintenance operations, particularly for lightweight alloys such as aluminum and magnesium. By utilizing supersonic particle deposition at relatively low temperatures, Cold Spray eliminates the formation of heat-affected zones, preserving the original microstructure and mechanical properties of the substrate. In 2026, portable Cold Spray systems are enabling field repairs of high-strength aluminum alloys such as Al-7075, achieving coating porosity below 1.2% and tensile strengths exceeding 260 MPa in compliance with MIL-STD-3021. Beyond static strength, fatigue performance has also been validated, with repaired aluminum panels sustaining approximately 500,000 cycles at a tensile stress of 103 MPa, demonstrating suitability for long-term structural applications. The technology is also delivering significant cost savings in the restoration of magnesium components, such as rotorcraft gearbox housings, with reclamation rates reaching up to 90% for parts previously deemed unserviceable. By reducing reliance on component replacement and enabling rapid, on-site repairs, Cold Spray is positioning itself as a transformative capability within the thermal spray equipment and services industry.

Thermal Spray Coating Equipment and Services Market Share and Segmentation Insights: Offering Segment Trends Driving Industry Adoption

Services Segment Leads with 50.9% Share Fueled by Cost Efficiency and Technical Expertise

The services segment dominates the thermal spray coating equipment and services market with a 50.9% market share in 2025, driven by strong demand for outsourced coating solutions across aerospace, automotive, oil & gas, and industrial manufacturing sectors. High **capital costs of thermal spray systems—including HVOF, plasma spray, and arc spray technologies ranging from $150,000 to $2 million—**encourage companies to rely on specialized service providers rather than investing in in-house equipment. This trend is accelerating growth in the thermal spray services market, contract coating services, and surface engineering solutions industry. Additionally, the process requires precise parameter control such as gas flow rates, particle velocity, temperature, and standoff distance, making skilled expertise critical. Service providers employ highly trained engineers and coating specialists to ensure optimal coating performance, durability, and adherence to industry standards. As a result, outsourcing not only reduces operational risk but also enhances coating quality, reinforcing the segment’s leadership in the global thermal spray coatings market.

Semi-Automatic Systems Capture 47.4% Share Balancing Flexibility and Precision in Coating Applications

The semi-automatic operation mode segment holds the largest share at 47.4% in the thermal spray coating market in 2025, reflecting its optimal balance between automation efficiency and operational flexibility. Within the industrial coating equipment and thermal spray technology market, semi-automatic systems—typically featuring robotic spray gun manipulators combined with manual part loading—enable consistent coating thickness across complex geometries and precision components. This makes them highly suitable for mid-volume production environments, including job shops and mid-tier manufacturing facilities. Industries rely on these systems for applications such as roll coating, pump shaft restoration, hydraulic cylinder repair, and wear-resistant coatings, where both accuracy and adaptability are critical. Furthermore, semi-automatic systems support quick changeovers between different part types, reducing downtime and improving throughput. This combination of precision control, scalability, and cost-effectiveness positions semi-automatic systems as the preferred choice in the thermal spray equipment and coating services market.

Competitive Landscape Analysis of the Thermal Spray Coating Equipment and Services Market

Oerlikon Metco Leading Integrated Thermal Spray Equipment and Digital Coating Solutions

Oerlikon Metco (Oerlikon Group) remains a dominant force in the thermal spray coating equipment and services market, following its 2026 transition into a pure-play surface technology leader. By divesting non-core segments, the company has focused capital on advanced thermal spray systems and additive manufacturing solutions. It is targeting an EBITDA margin of 17.5% in 2026, supported by a portfolio of over 2,000 coating materials and high-performance HVOF systems. Its proprietary Digital Twin diagnostics technology ensures near-zero scrap rates in complex ceramic coatings, particularly in aero-engine applications. With operations in 38 countries, Oerlikon offers a comprehensive equipment + consumables ecosystem, ensuring recurring revenue and strong OEM partnerships.

Linde Expanding EB-PVD and EV Battery Thermal Spray Service Capabilities

Linde plc, through Praxair Surface Technologies, is a key player in the thermal spray coating services market, particularly in high-value aerospace applications. The company specializes in EB-PVD coatings and automated HVOF services, supporting major engine programs such as GE9X and LEAP with complete thermal barrier coating lifecycle management. Linde is also expanding into EV battery thermal management coatings, utilizing thin-film ceramic sprays to mitigate thermal runaway risks in lithium-ion systems. Backed by its industrial gas expertise, the company offers integrated “Gas + Spray” service contracts, leveraging oxygen, hydrogen, and argon supply chains. This vertical integration strengthens its position in the advanced surface engineering and coating services market.

Bodycote Scaling Global Thermal Spray Service Network with Sustainable Technologies

Bodycote plc is strengthening its presence in the thermal spray coating services market through strategic expansion and sustainability initiatives. Its 2026 aerospace and defense acquisition reinforces its leadership in specialist thermal processing and coating services. With over 150 facilities globally, Bodycote provides scalable outsourcing solutions, enabling Tier-1 manufacturers to access advanced coatings without capital-intensive infrastructure. The company reported £727.1 million in revenue in 2025, with a 121% surge in operating profit driven by specialized technologies. Its deployment of on-site hydrogen generation systems reduces Scope 1 emissions and enhances supply chain resilience, positioning Bodycote as a leader in sustainable thermal spray coating services.

Kennametal Advancing Superalloy Coatings for Extreme Wear and Energy Applications

Kennametal Inc., through its Stellite™ brand, plays a critical role in the thermal spray coating equipment and consumables market, particularly in superalloy-based coatings. The company is recognized for its cobalt and nickel-based powders and wires that deliver superior wear and corrosion resistance in oil & gas and power generation industries. Its latest laser-cladding and thermal spray powders support the replacement of hazardous hard chrome plating, aligning with global environmental regulations. Kennametal’s coatings can extend component service life by up to 400%, making them essential in mining and energy applications. Additionally, its investment in high-entropy alloy coatings offers enhanced durability in geothermal environments.

Saint-Gobain Driving Ceramic Consumables and Automated Spray Cell Innovation

Saint-Gobain (Surface Solutions) is a leading player in the thermal spray coating consumables market, supplying critical ceramic materials such as alumina, zirconia, and titania that account for nearly 25% of global plasma spray volume. In 2026, the company expanded its ZirPro production capacity to meet rising demand in the medical implant coatings segment. Saint-Gobain is also advancing partnerships with automation firms to deliver turnkey robotic spray cells, integrating materials with advanced filtration systems. Its powder recovery initiatives support circular economy goals by recycling overspray materials, reinforcing its leadership in sustainable and high-efficiency coating solutions.

United States Advancing Thermal Spray Technologies Through MRO and Cold Spray Innovations

The United States continues to lead the thermal spray coating equipment and services market, driven by strong demand from aerospace, defense, and high-performance industrial applications. A major technological advancement in 2026 includes the expanded deployment of Laser-Assisted Cold Spray (LACS) by the Department of Defense, enabling in-situ repair of aluminum and titanium components. This innovation significantly reduces replacement costs while enhancing lifecycle efficiency for aerospace structures.

Product innovation is accelerating with the introduction of next-generation Suspension Plasma Spray (SPS) systems, designed for depositing nanostructured coatings on turbine engine components. Infrastructure investments, such as Oerlikon Metco’s expanded service hubs, are strengthening capabilities in HVOF coating services for commercial aviation. Regulatory shifts, particularly the phase-out of hexavalent chromium, are driving adoption of environmentally compliant thermal spray alternatives like tungsten carbide coatings. The U.S. is also witnessing increased adoption in biomedical applications, including plasma-sprayed hydroxyapatite coatings for implants, as well as automotive applications through dedicated bore-coating facilities.

Germany Driving Smart Factory Integration and Hydrogen-Compatible Coating Solutions

Germany is emerging as a leader in automated thermal spray coating systems, integrating Industry 4.0 technologies to enhance precision and efficiency. The establishment of the Berlin-based Hydrogen-Turbine Service Hub highlights the country’s focus on coatings capable of withstanding hydrogen combustion environments, a critical requirement for next-generation energy systems.

Technological advancements include the implementation of digital twin-enabled thermal spray booths, allowing real-time optimization of coating parameters and achieving highly precise thickness control. Government initiatives such as the Sustainable Surface Technology 2030 program are supporting SMEs in transitioning to high-efficiency HVAF systems. Strategic investments by companies like Linde are improving process efficiency by reducing gas consumption in plasma spray operations.

Germany’s expertise extends to renewable energy applications, where thermal spray coatings are widely used for offshore wind turbine components to resist corrosion and wear. The commercialization of high-entropy alloy powders is further enhancing coating performance in extreme environments, positioning Germany at the forefront of advanced thermal spray technologies.

China’s Industrial Scale Expansion and Supply Chain Control in Thermal Spray Coatings

China is rapidly strengthening its position in the thermal spray equipment and services market by focusing on large-scale industrialization and supply chain integration. Regulatory actions aimed at securing tungsten processing capabilities have accelerated domestic production of high-purity carbide powders, ensuring global competitiveness in HVOF coating services.

Technological breakthroughs include the commercialization of warm spray technology for copper-based coatings, offering enhanced density and performance at lower operational costs. Infrastructure investments, particularly in the Tianjin aviation MRO cluster, have led to the deployment of advanced robotic spray cells for engine maintenance.

Government initiatives mandating thermal spray coatings for high-speed rail refurbishments are driving large-scale adoption across infrastructure sectors. China also dominates in dielectric thermal spray coatings for semiconductor equipment, protecting components from aggressive processing environments. Expansion in ceramic powder production is further supporting growth in medical and industrial coating applications, reinforcing China’s leadership in mass-scale thermal spray solutions.

India’s Rapid Growth Driven by Defense Localization and Industrial Expansion

India is emerging as a key growth market in the thermal spray coating services industry, supported by strong government initiatives and increasing demand across defense, infrastructure, and heavy industries. The establishment of dedicated thermal spray centers for the Advanced Medium Combat Aircraft (AMCA) program highlights India’s focus on indigenous aerospace capabilities.

Technological advancements include the development of cost-effective electric arc spray systems, improving durability of agricultural equipment and reducing maintenance costs. Strategic investments by global players and local partners are expanding maintenance and repair (MRO) networks across major industrial hubs, supporting sectors such as steel and cement.

Infrastructure applications are growing, with thermal spray coatings being implemented in high-speed rail systems like Vande Bharat Express to enhance durability and reduce operational noise. Government incentives under the PLI Scheme 2.0 are promoting domestic manufacturing of thermal spray equipment, reducing reliance on imports. Additionally, the use of thermal sprayed aluminum coatings in coastal oil and gas facilities is improving corrosion resistance, positioning India as a strong player in industrial thermal spray applications.

Japan’s Leadership in Precision Thermal Spray Systems and Electronics Applications

Japan continues to lead in precision thermal spray coating technologies, particularly for electronics, semiconductors, and advanced materials. The commercialization of vacuum plasma spray (VPS) systems is enabling the production of ultra-dense coatings for next-generation solid-state batteries, supporting innovation in energy storage technologies.

Product innovations such as smart spray guns with integrated sensors are enhancing coating efficiency by monitoring powder behavior in real time, reducing waste and improving quality. Industrial expansion includes specialized clean-room coating facilities that cater to the semiconductor sector’s demand for anti-static and high-purity coatings.

Investments in high-purity metal powders, including molybdenum and tantalum, are strengthening Japan’s supply chain for high-temperature applications. Updated Japanese Industrial Standards are setting global benchmarks for coating performance, particularly in medical and electronics sectors. Japan is also expanding applications in consumer products, including thermal spray coatings for wearable devices, highlighting its role in high-value, precision-driven markets.

Saudi Arabia’s Expansion in Thermal Spray Coatings for Energy and Infrastructure Protection

Saudi Arabia is rapidly advancing in the thermal spray coating market, driven by large-scale infrastructure projects and the need for durable coatings in extreme environmental conditions. The development of specialized MRO centers, such as the facility in NEOM, is enhancing local capabilities for maintaining solar and energy infrastructure.

Government initiatives under Vision 2030 are promoting the adoption of thermal sprayed aluminum (TSA) coatings for desalination plants and coastal infrastructure, replacing traditional galvanization methods. Technological innovations include sand-abrasion resistant coatings designed to protect oil and gas equipment from harsh desert conditions.

Expansion by global service providers is strengthening the domestic supply chain, supporting localization efforts for energy sector maintenance. Thermal spray coatings are also being deployed on gas turbines to improve efficiency under high ambient temperatures. Regulatory updates, including green building codes mandating long-life coatings, are further driving demand for high-performance thermal spray solutions in Saudi Arabia’s infrastructure and energy sectors.

Thermal Spray Coating Equipment And Services Market Report Scope

Thermal Spray Coating Equipment And Services Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.5 Billion

|

|

Market Size (2032)

|

$19.4 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Offering (Equipment, Services, Consumables), By Technology (Combustion Flame Spray, Electrical Energy Spray, Cold Spray, Laser Cladding), By Material (Metals and Alloys, Ceramics, Carbides, Intermetallics, Polymers, Abradables and Composites), By Operation Mode (Manual, Semi-Automatic, Fully Automatic), By End-User Industry (Aerospace and Defense, Automotive and Transportation, Energy and Power Generation, Oil and Gas, Healthcare and Medical Devices, Steel and Heavy Metal Processing, Electronics and Semiconductors, Industrial Machinery, Mining and Agriculture)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Oerlikon Metco, Praxair Surface Technologies, Inc., Bodycote plc, Saint-Gobain S.A., Curtiss-Wright Corporation, Höganäs AB, Kennametal Inc., Sulzer Ltd., The Lincoln Electric Company, Castolin Eutectic, Wall Colmonoy, Flame Spray Technologies B.V., GTV Verschleißschutz GmbH, Metallisation Limited, Progressive Surface

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Thermal Spray Coating Equipment And Services Market Segmentation

By Offering

- Spray Guns and Nozzles

- Feeder Systems

- Control Systems and Software

- Specialized Booths and Enclosures

- Dust Collection and Environmental Systems

- Auxiliary Equipment

- Coating Application Services

- Maintenance, Repair, and Overhaul

- Process Consulting and Technical Support

- Surface Preparation and Finishing

By Technology

- Conventional Flame Spray

- High-Velocity Oxy-Fuel

- High-Velocity Air-Fuel

- Detonation Gun

- Plasma Spray

- Electric Arc Wire Spray

- Cold Spray

- Laser Cladding

By Material

- Metals and Alloys

- Ceramics

- Carbides

- Intermetallics

- Polymers

- Abradables and Composites

By Operation Mode

- Manual

- Semi-Automatic

- Fully Automatic

By End-User Industry

- Aerospace and Defense

- Automotive and Transportation

- Energy and Power Generation

- Oil and Gas

- Healthcare and Medical Devices

- Steel and Heavy Metal Processing

- Electronics and Semiconductors

- Industrial Machinery

- Mining and Agriculture

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Thermal Spray Coating Equipment And Services Industry

- Oerlikon Metco

- Praxair Surface Technologies, Inc.

- Bodycote plc

- Saint-Gobain S.A.

- Curtiss-Wright Corporation

- Höganäs AB

- Kennametal Inc.

- Sulzer Ltd.

- The Lincoln Electric Company

- Castolin Eutectic

- Wall Colmonoy

- Flame Spray Technologies B.V.

- GTV Verschleißschutz GmbH

- Metallisation Limited

- Progressive Surface

*- List not Exhaustive