Reflective Thermal Insulation Coatings Market Size, Energy Efficiency Demand, and Urban Heat Mitigation

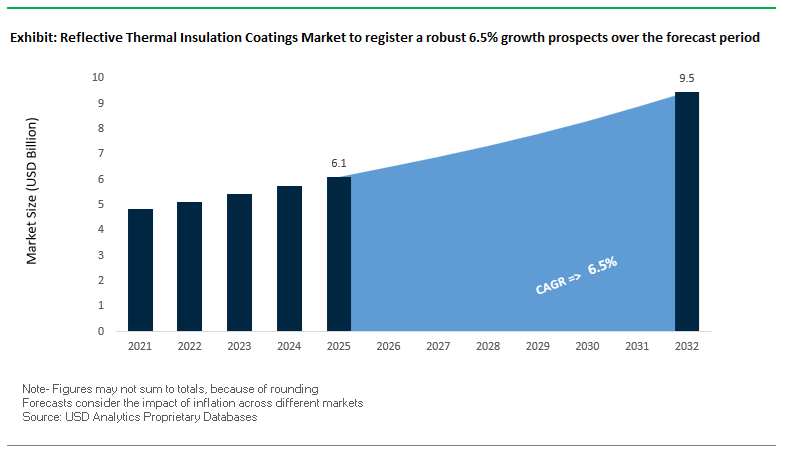

The global Reflective Thermal Insulation Coatings Market was valued at $6.1 billion in 2025 and is projected to grow at a CAGR of 6.5% through 2032, reaching $9.5 billion by 2032. Growth is driven by rising demand for energy-efficient building materials, industrial heat management solutions, and climate-responsive infrastructure, particularly in regions facing high solar exposure and urban heat island effects.

Reflective thermal insulation coatings are engineered to reduce heat absorption and enhance thermal emissivity, thereby lowering surface temperatures and indoor cooling loads. These coatings are widely used across commercial buildings, residential roofing, industrial storage tanks, pipelines, and transportation systems, where controlling heat transfer is critical for both energy savings and asset protection.

A key structural driver is the global push toward decarbonization and energy efficiency in buildings, supported by stricter regulations and green building certifications. Reflective coatings contribute directly to reducing HVAC energy consumption, making them a preferred solution for cool roofs, facades, and industrial thermal management systems.

Additionally, the integration of advanced materials such as aerogels, infrared-reflective pigments, and composite fillers is enhancing the performance of these coatings, enabling higher reflectivity and lower thermal conductivity without compromising durability or aesthetics.

Market Analysis: Radiative Cooling Systems, IR-Reflective Pigments, and Smart Energy Integration Driving Market Evolution

Recent developments in the Reflective Thermal Insulation Coatings Market highlight a convergence of advanced material science, policy-driven adoption, and energy integration technologies. In May 2025, AkzoNobel introduced a two-layer “sunscreen” coating system, combining a radiative cooling topcoat with an aerogel-based thermal barrier layer. Field trials demonstrated up to a 10% reduction in surface temperatures, showcasing the effectiveness of multi-layer thermal management approaches.

High-performance coatings are expanding into industrial applications. PPG’s CORAFLON® Platinum coatings are being positioned for data centers and cold storage facilities, leveraging their high Solar Reflectance Index (SRI) to reduce cooling loads in energy-intensive environments.

Material innovation is advancing rapidly. Research from IIT Bombay led to the commercialization of a hydrophobic epoxy composite coating incorporating cenospheres, achieving significant reductions in thermal conductivity and up to 93% reduction in cooling loads under peak solar conditions. This highlights the growing role of composite and nano-engineered materials in enhancing thermal insulation performance.

Policy-driven adoption is accelerating market penetration. In Latin America (2026), municipal mandates for reflective roofing in public housing projects are driving widespread use of high-albedo coatings, reducing indoor temperatures by 4–6°C and supporting large-scale energy efficiency initiatives.

Integration with renewable energy systems is also emerging. The adoption of anti-reflective coatings in photovoltaic (PV) systems is enabling optimized Building-Integrated Photovoltaics (BIPV), where reflective coatings manage excess heat while PV surfaces maximize energy absorption, creating a balanced thermal-energy ecosystem.

Regulatory compliance is influencing pigment technology. The transition to REACH-compliant, chrome-free infrared reflective pigments (2026) allows manufacturers to produce dark-colored coatings with high solar reflectance, overcoming traditional limitations of heat absorption in darker surfaces.

Regional innovation is addressing environmental challenges. Jotun’s “Cool Shades” expansion in the Middle East (2025) incorporates dust-resistant binder technologies, maintaining thermal performance up to 50% longer in desert environments where particulate accumulation typically degrades reflectivity.

Strategic focus is also shifting toward industrial energy management. Hempel’s “Accelerate to Win” strategy (2026) emphasizes reflective coatings for tanks and pipelines, reducing heat-induced evaporation losses and improving operational efficiency in energy infrastructure.

Market Trend: U.S. Federal Net-Zero Mandates Accelerating Adoption of High-SRI Reflective Coatings in Public Infrastructure

The reflective thermal insulation coatings market in the United States is being structurally reshaped by federal decarbonization mandates, particularly under Executive Order 14057 and updated DOE Part 433 energy efficiency standards. These frameworks require federal buildings to achieve net-zero emissions by 2045, with immediate emphasis on energy-efficient retrofits beginning in the 2025–2026 period. As a result, high-reflectivity roof coatings are transitioning from optional upgrades to mandatory specifications across government-owned and leased facilities.

A critical performance requirement introduced in 2026 procurement guidelines is durability of reflectivity. Coatings must maintain a Solar Reflectance Index of at least 85% after three years of simulated weathering. This requirement is driving a shift away from low-cost reflective paints toward high-performance elastomeric and silicone-based coatings that offer long-term reflectivity retention under UV and environmental exposure.

Operational efficiency gains are substantial. Internal DOE pilot studies indicate that compliant reflective coatings reduce peak cooling loads by 15% to 22% in federal office buildings. This enables downsizing of HVAC systems during replacement cycles, reducing both capital expenditure and long-term energy consumption. In humid regions such as the southeastern United States, high-emittance coatings have demonstrated an additional benefit by reducing humidity-driven HVAC cycling by approximately 30%, extending compressor lifespans by three to five years.

These combined energy savings and asset optimization benefits are positioning reflective thermal insulation coatings as a foundational technology in federal energy management strategies and large-scale building retrofits.

Market Trend: India ECBC 2024 Enforcement Driving Reflective Coating Adoption for Urban Heat Island Mitigation

India’s commercial construction sector is witnessing a rapid increase in demand for reflective thermal insulation coatings following the enforcement of the Energy Conservation Building Code 2024 by the Bureau of Energy Efficiency. As of 2026, compliance with Super ECBC standards has become mandatory for large commercial developments, with explicit requirements targeting the reduction of urban heat island effects through roof reflectivity.

The regulation mandates a minimum initial solar reflectance of 0.70 and thermal emittance of 0.75 for buildings exceeding 1,000 square meters. These thresholds effectively eliminate the use of traditional dark roofing materials without reflective coatings, driving widespread adoption of high-performance cool roof systems across metropolitan regions.

The macro-level energy impact is significant. Estimates from regulatory authorities indicate that large-scale deployment of ECBC-compliant reflective coatings could reduce national grid demand by approximately 1.7 billion kilowatt-hours annually. This reduction is particularly critical as India expands its electric vehicle charging infrastructure and faces increasing peak load pressures in urban centers.

Field data from 2026 commercial installations in cities such as Hyderabad and Delhi further highlights the performance benefits. Buildings utilizing compliant reflective coatings are maintaining indoor ceiling temperatures between 4°C and 7°C lower than peak outdoor ambient conditions. This temperature reduction improves occupant comfort while reducing reliance on air conditioning systems, reinforcing the role of reflective coatings in sustainable urban development.

Market Opportunity: Aerogel-Enhanced Reflective Coatings Unlocking High-Performance Thermal Insulation for LNG and Cryogenic Infrastructure

The expansion of global liquefied natural gas infrastructure is creating a high-value opportunity for aerogel-enhanced reflective thermal insulation coatings. These advanced materials combine the high solar reflectance of traditional coatings with the ultra-low thermal conductivity of silica aerogels, delivering superior insulation performance in extreme temperature environments.

Thermal conductivity benchmarks for 2026 aerogel-based coatings range between 0.012 and 0.015 watts per meter-kelvin, making them approximately three times more effective than conventional ceramic-filled coatings at equivalent thickness. This performance advantage is particularly valuable in cryogenic applications where minimizing heat transfer is critical to maintaining stored product stability.

In LNG storage tanks, the application of a thin aerogel-reflective coating layer has been shown to reduce passive heat ingress and subsequent boil-off rates by 12% to 18%. This reduction translates into substantial cost savings for terminal operators by preserving stored fuel and improving overall system efficiency.

Additionally, these coatings address long-standing challenges related to corrosion under insulation. Traditional insulation systems often create moisture traps that accelerate corrosion of underlying metal surfaces. Fluid-applied aerogel coatings eliminate these gaps, reducing corrosion-related maintenance costs by up to 40% over a ten-year lifecycle. This combination of thermal efficiency and durability positions aerogel-enhanced coatings as a premium solution in energy infrastructure and cryogenic storage applications.

Market Opportunity: Self-Cleaning Hydrophobic Reflective Coatings Enhancing Solar PV Efficiency in Desert Environments

The rapid expansion of solar photovoltaic installations in arid regions is generating strong demand for multifunctional reflective coatings that combine thermal management with self-cleaning properties. In desert environments, dust accumulation significantly reduces solar panel efficiency, creating a need for coatings that can mitigate soiling while maintaining high reflectivity.

Advanced hydrophobic coatings developed for 2026 applications demonstrate the ability to reduce dust deposition by 90% to 92% compared to untreated surfaces. This is achieved through engineered surface chemistry that minimizes particle adhesion and promotes natural cleaning through wind and minimal moisture exposure.

Performance improvements in energy output are substantial. In environments where daily efficiency losses of 0.7% to 0.8% are typical due to dust accumulation, self-cleaning reflective coatings enable recovery rates of over 93% between maintenance cycles. This represents a significant improvement compared to standard panels, which often recover only around 60% of lost efficiency without frequent manual cleaning.

Water conservation is an additional advantage. By reducing the frequency of manual cleaning operations by approximately 75%, these coatings can save up to 500,000 liters of water per megawatt of installed capacity annually. This is particularly important in regions facing water scarcity and aligns with broader sustainability initiatives such as regional green development programs.

The integration of reflectivity, hydrophobicity, and durability is establishing these coatings as a critical technology in optimizing solar energy generation in harsh environmental conditions, supporting both energy efficiency and resource conservation objectives.

Reflective Thermal Insulation Coatings Market Share and Segmentation Insights: Liquid Coatings Dominance and Contractor-Led Application Growth

By Coating Form: Liquid Reflective Coatings Lead with On-Site Applicability and Ease of Use

The liquid coating segment dominated the reflective thermal insulation coatings market with an overwhelming 83.4% share in 2025, driven by its unmatched ease of application, flexibility, and compatibility with diverse substrates. Liquid formulations, typically based on acrylic, silicone, or polyurethane coatings enhanced with ceramic or glass microspheres, can be applied using spray, roller, or brush methods, making them ideal for both new construction and retrofit projects. These coatings are widely used across roofs, walls, storage tanks, pipelines, and industrial equipment, delivering effective solar reflectance and thermal insulation performance. A key advantage is their field application capability, allowing on-site coating of existing infrastructure without the need for factory-based processing, unlike powder or vacuum-deposited coatings. This versatility significantly reduces installation costs and downtime, accelerating adoption across commercial buildings, industrial facilities, and energy-efficient construction projects, thereby reinforcing the dominance of liquid reflective insulation coatings.

By Sales Channel: Professional Contractor Networks Dominate with Performance Assurance and Compliance Expertise

The professional contractor and applicator networks segment accounted for a leading 55.6% share of the reflective thermal insulation coatings market in 2025, reflecting the critical importance of skilled application and performance validation. The effectiveness of reflective coatings depends heavily on proper surface preparation, primer application, and achieving the required dry film thickness (typically 15–30 mils), which necessitates trained professionals. Contractors ensure coatings deliver optimal thermal insulation, durability, and adhesion performance across varied environmental conditions. Additionally, commercial and industrial end users increasingly require verified energy savings and sustainability compliance, including documentation of solar reflectance index (SRI), thermal emittance, and energy efficiency metrics for certifications such as LEED and ENERGY STAR. Contractor networks play a vital role in providing this validation, along with application warranties and performance guarantees. As demand rises for energy-efficient building coatings and sustainable insulation solutions, contractor-led channels continue to drive market growth and adoption.

Competitive Landscape of the Reflective Thermal Insulation Coatings Market

PPG Leads Market with End-to-End Thermal Coating Solutions and Data Center Focus

PPG Industries, Inc. is the technological leader in the reflective thermal insulation coatings market, leveraging its comprehensive product portfolio and application expertise. In 2026, the company showcased its solutions at Data Center World, emphasizing coatings that reduce HVAC cooling loads in hyperscale facilities. Its SIGMAGLIDE® and SIGMASHIELD® systems are being adapted with thermal and dielectric properties, enabling dual functionality for industrial and EV applications. PPG’s integrated approach—from pretreatment to topcoat—accelerates project timelines and enhances efficiency for large-scale infrastructure developments.

AkzoNobel Drives Aesthetic-Functional Innovation with Infrared-Reflective Coatings

AkzoNobel N.V. is a major player in the reflective thermal insulation coatings market, focusing on combining performance with design. Its “Rhythm of Blues™” collection integrates infrared-reflective pigments, allowing darker colors to maintain high solar reflectance levels. Through its Cool Chemistry® technology, the company enables 15–20% energy savings by reducing roof surface temperatures by up to 28°C. AkzoNobel is also expanding globally with new facilities in the Middle East and pursuing a merger with Axalta, strengthening its position in the reflective coatings segment.

Nippon Paint Leads APAC Growth with High-Performance Heat-Reflective Coatings

Nippon Paint Holdings Co., Ltd. is a dominant force in the Asia-Pacific reflective coatings market, driven by strong demand in industrial and residential sectors. Its THERMOEYE system delivers surface temperature reductions of up to 20°C, significantly lowering cooling energy requirements. The company has reported rapid growth in demand, supported by large-scale initiatives such as Japan’s “Repainting Energy Roof” program. Its strong regional presence and focus on climate-adaptive solutions position it as a leader in heat mitigation technologies.

Sherwin-Williams Expands Market Reach with Ceramic-Based Thermal Barrier Technologies

The Sherwin-Williams Company is a key player in the reflective thermal insulation coatings market, leveraging its strong performance coatings segment. Its Ultra 7000® and EnviroLastic® systems utilize hollow ceramic microspheres to reduce heat transfer in industrial applications such as storage tanks and pipelines. The company’s expansion into South America, supported by the Suvinil acquisition, strengthens its presence in high-growth construction markets. Its focus on rapid-return-to-service coatings enhances operational efficiency for infrastructure projects.

BASF Strengthens Market with Advanced Resin Technologies and Integrated Thermal Solutions

BASF SE plays a critical role in the reflective thermal insulation coatings market as a supplier of advanced resins and coating technologies. Its latest innovation includes a single-layer waterborne 2K system that combines primer, topcoat, and thermal insulation, reducing application steps and material usage by up to 50%. BASF is also transitioning its European operations to renewable electricity, lowering the carbon footprint of its products. Its expertise in high-temperature insulation materials positions it as a leader in aerospace and power generation coatings.

Jotun Leads Durability and Regional Dominance with Advanced Reflective Coating Systems

Jotun Group is a dominant player in the reflective thermal insulation coatings market, particularly in Asia-Pacific and the Middle East. Its Jotashield Extreme series utilizes pigment-encapsulation technology to maintain high solar reflectance and prevent degradation over time. The company is also developing coatings for district heating and LNG cold-chain systems, reducing energy losses in thermal distribution networks. Its integration of AI-driven formulation tools enables customized solutions based on geographic conditions, reinforcing its leadership in durable and climate-adaptive coatings.

India Emerging as a Cool Roof Policy Powerhouse Driving Thermal Insulation Coatings Demand

India is rapidly becoming a global leader in the reflective thermal insulation coatings market, driven by aggressive policy implementation and rising climate challenges. The full-scale rollout of Telangana’s Cool Roof Policy (2025) mandates high Solar Reflective Index (SRI) coatings for large commercial and government buildings, significantly boosting demand for cool roof coatings and energy-efficient insulation solutions.

Government frameworks such as the Energy Conservation Building Code (ECBC) are further accelerating adoption by targeting substantial energy savings in commercial infrastructure. Massive infrastructure redevelopment, including over 1,000 railway stations, is driving the use of solar-reflective coatings that reduce interior temperatures by up to 5°C. Technological innovation is also advancing, with the introduction of nanotechnology-based elastomeric coatings offering thermal insulation, waterproofing, and antimicrobial protection. Additionally, increased application in cold-storage logistics for agriculture and expansion of domestic manufacturing by companies like Asian Paints and JSW are strengthening India’s position as a high-growth market.

China Scaling Smart Reflective Coatings with Nanotechnology and Energy-Efficient Infrastructure

China is transitioning toward high-performance thermal insulation coatings by integrating advanced nanotechnology and smart materials into its construction and industrial sectors. The development of AI-driven smart reflective coatings using phase change materials (PCMs) allows adaptive thermal resistance based on environmental conditions, marking a significant innovation in energy-efficient coatings.

Policy support under the updated 14th Five-Year Plan is prioritizing green manufacturing, accelerating the adoption of aqueous and low-VOC coating systems. China’s infrastructure expansion, particularly in 5G base stations and data centers, is driving demand for dielectric thermal coatings that can reduce cooling energy consumption by up to 15%. Manufacturing advancements such as digital twin coating systems are improving application accuracy for hollow glass microsphere coatings. Furthermore, China’s dominance in EV manufacturing is boosting the use of aerogel-based thermal barriers for battery safety, reinforcing its leadership in high-performance insulation technologies.

United States Driving PFAS-Free Innovation and Energy-Efficient Building Retrofits

The United States reflective insulation coatings market is being reshaped by regulatory mandates and sustainability-focused investments. The EPA’s PFAS-free regulations (2025–2026) are pushing manufacturers toward bio-based and environmentally compliant coating formulations, particularly in architectural and industrial applications.

Federal initiatives under the Inflation Reduction Act (IRA) are encouraging the use of thin-film aerogel composites that enhance both thermal insulation and fire resistance. Updated Department of Transportation (DOT) regulations are favoring high-performance materials such as polyurethane and aerogel coatings by setting stricter limits on thermal conductance. Key applications include the growing demand for low-emissivity (Low-E) coatings in battery manufacturing facilities, ensuring stable process environments. Additionally, innovations such as blockchain-based material tracking systems and trade policies supporting domestic production are strengthening supply chain resilience and market competitiveness.

Germany Leading Sustainable Thermal Coating Innovations with EPBD Compliance and Green Steel Integration

Germany is at the forefront of the European reflective thermal insulation coatings market, driven by stringent sustainability regulations and advanced industrial capabilities. Compliance with the EU Energy Performance of Buildings Directive (EPBD) is making reflective coatings a standard requirement for building retrofits, significantly boosting demand across residential and commercial sectors.

Technological advancements such as transparent heat-reflective coatings using precious metal wire technology (HeiQ Xpectra) are improving building energy efficiency by enhancing wall insulation performance. Germany’s focus on sustainability is further evident in the adoption of hydrogen-based green steel substrates paired with low-temperature curing coatings, reducing energy consumption during manufacturing. Digitalization initiatives, including blockchain-based lifecycle tracking, are improving transparency in coating materials. High demand for antimicrobial reflective coatings and ongoing R&D in graphene-enhanced coatings for offshore applications highlight Germany’s leadership in innovation and sustainability.

Saudi Arabia’s Mega Projects Accelerating Demand for High-Performance Thermal Insulation Coatings

Saudi Arabia is emerging as a critical growth region in the thermal insulation coatings market, driven by large-scale infrastructure developments under Vision 2030. Mega projects such as NEOM and “The Line” are creating substantial demand for fusion-bonded epoxy thermal coatings used in underground utilities and modular construction.

Regulatory frameworks such as the Saudi Building Code (SBC 601) are mandating advanced insulation solutions to combat extreme desert temperatures. Technological innovations, including solar-reflective coatings capable of reducing surface temperatures by up to 15°C, are enhancing infrastructure resilience. The oil and gas sector remains a key application area, utilizing phenolic epoxy thermal linings for high-temperature operations. Additionally, expansion of manufacturing facilities by global players like Jotun and Hempel is strengthening local production capabilities, while growing housing demand is boosting adoption of cool roof membranes across residential developments.

Brazil Strengthening Thermal Coatings Demand Through Agribusiness and Industrial Applications

Brazil’s reflective thermal insulation coatings market is strongly influenced by its robust agribusiness sector and industrial expansion. Government policies, including anti-dumping duties on imported coated steel, are supporting domestic production and increasing the adoption of high-performance acrylic thermal coatings.

Key applications include abrasion-resistant coatings for grain silos and mining equipment, which help prevent heat-related material degradation. Infrastructure initiatives such as the Nova Indústria Brasil (NIB) plan are promoting energy-efficient coating technologies through financial incentives. Technological advancements include the adoption of ZAM alloy-compatible coatings, offering superior corrosion resistance in harsh environments. Additionally, increasing demand for foam-based insulation systems in commercial buildings reflects the country’s growing focus on long-term energy efficiency and sustainability.

Japan Advancing Urban Heat Management with Precision Reflective Coating Technologies

Japan is focusing on mitigating urban heat challenges through advanced reflective thermal coatings, particularly in densely populated metropolitan areas. Government subsidies for heat-reflective roof coatings in cities like Tokyo and Osaka are driving adoption amid rising heat-related health concerns.

Technological innovation includes the development of oxygen-scavenging reflective films that enhance thermal protection and UV resistance, particularly for specialized applications such as healthcare packaging. Industrial demand remains strong for epoxy-based thermal coatings, known for their durability and resistance to extreme conditions. Investments in clean-room facilities are supporting the development of smart thermal packaging solutions with NFC monitoring capabilities, while product innovations such as self-healing reflective coatings are enhancing durability in consumer electronics. Expansion of waterborne UV coating production further supports automotive and appliance industries, reinforcing Japan’s role in high-precision thermal insulation technologies.

Reflective Thermal Insulation Coatings Market Report Scope

Reflective Thermal Insulation Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.1 Billion

|

|

Market Size (2032)

|

$9.5 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Technology (Reflective Coatings, Insulative Coatings, Hybrid Coatings), By Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, Specialty, Bio-based Resins), By Coating Form (Liquid, Powder Coatings, Vacuum-Deposited), By Substrate Compatibility (Concrete and Masonry, Metal, Plastics and Composites, Wood), By Application Area (Building Envelope, Industrial Equipment, Transportation Components, Cold Chain and Logistics), By End-Use Industry (Building and Construction, Oil and Gas, Automotive and Transportation, Aerospace and Defense, Power Generation, Manufacturing and General Industrial), By Functional Additive (Ceramic Microspheres, Glass Bubbles, Silica Aerogels, Nano-materials), By Sales Channel (Direct Sales, Specialty Insulation Distributors, Professional Contractor and Applicator Networks)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, BASF SE, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Jotun Group, Axalta Coating Systems Ltd., Hempel A/S, Sika AG, RPM International Inc., Dow Chemical Company, Mascoat, Superior Products International II, Inc., Hy-Tech Thermal Solutions, LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Reflective Thermal Insulation Coatings Market Segmentation

By Technology

- Reflective Coatings

- Insulative Coatings

- Hybrid Coatings

By Resin Type

- Acrylic

- Epoxy

- Polyurethane

- Silicone

- Specialty

- Bio-based Resins

By Coating Form

- Liquid

- Powder Coatings

- Vacuum-Deposited

By Substrate Compatibility

- Concrete and Masonry

- Metal

- Plastics and Composites

- Wood

By Application Area

- Building Envelope

- Industrial Equipment

- Transportation Components

- Cold Chain and Logistics

By End-Use Industry

- Building and Construction

- Oil and Gas

- Automotive and Transportation

- Aerospace and Defense

- Power Generation

- Manufacturing and General Industrial

By Functional Additive

- Ceramic Microspheres

- Glass Bubbles

- Silica Aerogels

- Nano-materials

By Sales Channel

- Direct Sales

- Specialty Insulation Distributors

- Professional Contractor and Applicator Networks

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Reflective Thermal Insulation Coatings Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Jotun Group

- Axalta Coating Systems Ltd.

- Hempel A/S

- Sika AG

- RPM International Inc.

- Dow Chemical Company

- Mascoat

- Superior Products International II, Inc.

- Hy-Tech Thermal Solutions, LLC

*- List not Exhaustive