Silicone Gel Market Valuation 2025–2034: $3.4 Billion to $6.3 Billion at 7% CAGR Driven by EV Power Modules and Sustainable Personal Care Formulations

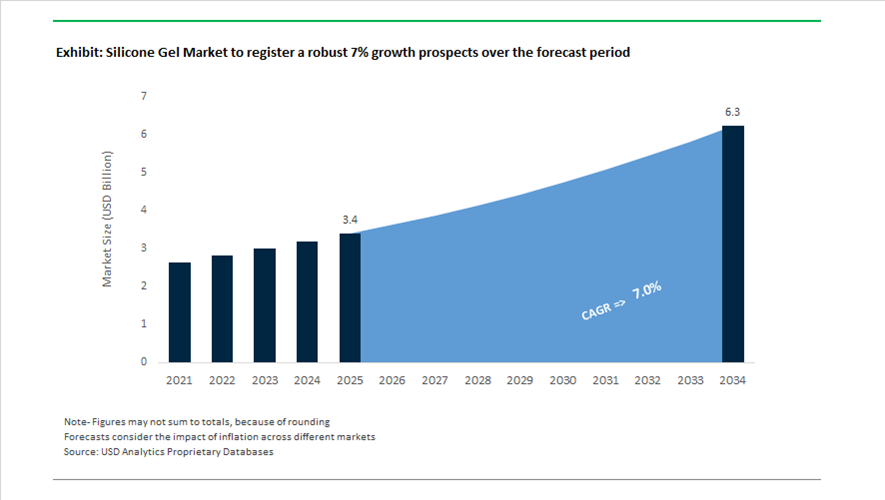

The global silicone gel market is valued at $3.4 billion in 2025 and is projected to reach $6.3 billion by 2034, expanding at a CAGR of 7%. Growth is underpinned by rising demand for thermally conductive silicone gels in electric vehicle power electronics, renewable energy inverters, and high-voltage insulation systems, alongside expanding applications in advanced wound care and premium personal care formulations. Silicone gels provide dielectric insulation, vibration damping, stress relief, optical clarity, and superior thermal stability, making them essential for encapsulation of insulated gate bipolar transistor modules, sensors, and LED assemblies. Increasing electrification across automotive platforms and the proliferation of high-temperature semiconductor modules operating above 150°C are structurally elevating demand for high-performance two-part silicone gel systems.

In April 2024, KCC Corporation completed the full acquisition of Momentive Performance Materials, consolidating global leadership in specialized silicone chemistries, including automotive-grade encapsulation gels and construction sealant technologies. In July 2024, Shin-Etsu Silicones showcased cosmetic-grade silicone gel formulations positioned as sustainable alternatives to microplastics, responding to regulatory pressure against synthetic polymer beads in personal care products. In October 2024, Momentive Technologies acquired Sibelco’s spherical alumina and silica business, strengthening the supply chain for thermally conductive fillers integrated into silicone gel matrices used in high-power electronics. These acquisitions and product demonstrations illustrate vertical integration across filler technology and gel formulation chemistry.

Product innovation accelerated through 2025 as EV power density and renewable energy installations expanded. In September 2025, Dow introduced DOWSIL™ EG-4175, a two-part silicone gel engineered for seventh-generation IGBT stacks capable of withstanding junction temperatures up to 180°C. This formulation addresses thermal cycling stress and mechanical strain in EV inverters and solar power modules, reinforcing silicone gel adoption in electrified mobility. In November 2025, Dow launched its “Beauty in Harmony” portfolio at in-cosmetics Asia, featuring silicone resin gum film formers such as DOWSIL™ FC-5012 and conditioning fluids aligned with high-performance, sustainability-focused cosmetic trends across Asian markets.

Shin-Etsu further expanded specialty gel chemistries in 2025 with alkyl-modified silicone crosspolymer gels such as X-22-6695B, swelled in jojoba oil and designed as PEG-free emulsifiers and thickeners for high-SPF sunscreen systems. These formulations enhance sensory profile, film integrity, and water resistance while maintaining organic compatibility. The convergence of EV thermal management requirements, semiconductor encapsulation reliability standards, sustainable cosmetic innovation, and advanced filler integration is positioning silicone gels as a critical material platform across mobility, energy, and high-performance consumer applications through 2034.

High-Impact Trends and Strategic Opportunities in the Global Silicone Gel Market

Medical Device Shift Toward Soft-Skin Adhesives and Sensor-Grade Encapsulation

The silicone gel market is undergoing a structural transformation driven by the rapid clinical adoption of wearable and patch-based medical devices for chronic disease management. Leading MedTech companies are increasingly specifying silicone gels that combine soft-skin adhesion, long-wear comfort, and low-temperature processability to protect increasingly delicate flexible electronics. Unlike conventional elastomers, silicone gels offer controlled tack, breathability, and low modulus, allowing sensors to remain conformal to the skin for extended periods without irritation or signal drift.

In late 2025, Elkem Silicones expanded its Silbione LSR Select portfolio to support overmolding of sensitive electronics at temperatures as low as 80 degrees Celsius. This capability is a critical enabler for continuous glucose monitors and ECG patches, where excessive heat can degrade sensor accuracy. These material advances are directly aligned with the projected $151.8 billion wearable medical device market by 2029, as manufacturers scale production of skin-mounted diagnostic platforms. Regulatory momentum reinforces this trend. As of December 2025, the U.S. Food and Drug Administration has steadily expanded its Sensor-based Digital Health Technology authorizations, with home healthcare applications now representing more than 52% of wearable medical revenues. Silicone gels are increasingly embedded in device specifications due to their ability to maintain electrical conductivity and adhesion stability over multi-day wear cycles.

Qualification of Silicone Gels for 800V EV and Next-Generation Power Electronics

Electrification of the automotive powertrain is imposing a new qualification regime for silicone gels used in power modules, inverters, and converters. As EV platforms transition toward 800 volt architectures and higher switching frequencies, silicone gels are being formally specified as the primary potting and stress-relief layer capable of surviving continuous junction temperatures above 175 degrees Celsius. These gels absorb thermo-mechanical stress, protect against partial discharge, and maintain dielectric integrity under aggressive thermal cycling.

In September 2025, Dow introduced DOWSIL EG-4175, a two-part silicone gel engineered for seventh-generation insulated gate bipolar transistor modules. The material supports continuous operation at 180 degrees Celsius and delivers dielectric strength of 23 kilovolts per millimeter, directly addressing the reliability requirements of high-voltage EV inverters and renewable energy converters. Advanced formulations now incorporate self-healing characteristics that enable micro-crack recovery during thermal cycling, extending module life. This capability is particularly relevant in Asia-Pacific markets, led by China, where the automotive electronics potting segment exceeded $400 million in annual value in 2025, underpinned by the world’s largest EV manufacturing ecosystem.

Thermal Management Solutions for AI Accelerators and 3D Chip Architectures

The rapid escalation of AI workloads is pushing semiconductor thermal design power into the kilowatt range, exposing the limitations of traditional thermal interface materials. This has created a high-value opportunity for thermally conductive silicone gels that can conform to irregular geometries in advanced packaging architectures, including chiplets and 3D integrated circuits. Unlike rigid pastes or foils, silicone gels provide both heat transfer and mechanical stress relief, a dual requirement in high-interconnect-density designs.

At late 2025 industry summits, thermal management was consistently identified as the primary bottleneck for scaling 3D IC systems. Advanced packaging players such as Silicon Box, which shipped approximately 100 million units from its Singapore facility in 2025, are increasingly evaluating silicone underfills with enhanced thermal conductivity to manage localized heat fluxes. Growth opportunities are particularly strong for silver-filled and low-viscosity hybrid silicone gels that can be precisely dispensed and compete with indium foils at the die-to-lid interface. In AI servers, maintaining mechanical compliance across the thermal interface is as critical as conductivity, positioning advanced silicone gels as a strategic material class rather than a commodity TIM.

Rapid-Cure Silicone Gel Kits for Infrastructure and Energy Asset Maintenance

Aging infrastructure and geographically remote energy assets are generating demand for field-ready silicone gel systems that enable fast, reliable repairs under harsh conditions. Two-part rapid-cure silicone gel kits are increasingly specified for on-site sealing and insulation of electrical junctions in offshore wind farms, substations, and subsea cable networks, where downtime carries high economic penalties. These materials are engineered to cure within minutes at ambient temperatures, even in saline or high-humidity environments.

In April 2025, at the AMPP Annual Conference, Henkel highlighted its expanding portfolio for critical infrastructure protection through its Loctite and CSNRI brands. The focus on proactive maintenance solutions directly addresses the estimated $1.3 trillion in annual global infrastructure repair requirements. Public investment in offshore wind and coastal power grids is further expanding demand for silicone gels with exceptional UV resistance and saltwater durability. Field-applied silicone gel kits allow technicians to perform airtight, long-lasting repairs without specialized equipment, materially reducing outage risk and extending asset service life across energy and utility networks.

Silicone Gel Market Share and Segmentation Insights

Two-Component Silicone Gels Lead Market Demand for Electronics Encapsulation and Medical Device Protection

Two-component silicone gels accounted for 42.80% of the silicone gel market in 2025, reflecting their widespread adoption in applications requiring reliable curing performance and flexible mechanical properties. These systems provide controlled pot life, adjustable hardness, and deep curing capability, enabling consistent manufacturing for applications such as electronics encapsulation and medical device protection. Two-component gels deliver excellent moisture resistance, electrical insulation, and vibration damping, making them essential for protecting sensitive electronic components. A major 2025 industry trend is the increasing demand for advanced electronics protection materials, where silicone gels are engineered with tailored properties including thermal conductivity, optical clarity, and substrate adhesion for applications such as LED lighting systems, power modules, and automotive sensors.

Electrical & Electronics Applications Drive Silicone Gel Consumption for Component Protection

Electrical and electronics represent the largest application segment in the silicone gel market, accounting for 38.60% of total demand in 2025 due to the need for reliable protection of delicate electronic components. Silicone gels are widely used for potting, encapsulation, and protective coatings in electronic assemblies, providing electrical insulation, moisture protection, vibration absorption, and thermal stability. Their soft gel structure reduces mechanical stress on sensitive components while maintaining environmental protection. A key 2025 demand driver is the rapid growth of automotive electronics, where vehicles increasingly incorporate sensors, power electronics modules, and control units. Silicone gel formulations designed for automotive systems provide high-temperature resistance, long-term reliability, and vibration durability required for under-hood and harsh operating environments.

Silicone Gel Market Competitive Landscape

The 2026 silicone gel market is driven by high-voltage EV architectures, AI data center cooling, and PFAS-free formulations. Key players are advancing dielectric gels, thermally conductive materials, and bio-based carriers to support power electronics, semiconductor manufacturing, and sustainable personal care applications.

Dow leads AI cooling and EV power electronics with high-temperature DOWSIL™ gel innovations

Dow Inc. (Dow Consumer & Electronics) is a dominant force in silicone gels, leveraging its DOWSIL™ portfolio to address thermal management challenges in EVs and AI infrastructure. The launch of DOWSIL™ EG-4175 enables operation at up to 180°C, supporting Generation 7 IGBT modules used in 800V EV systems, solar inverters, and wind turbines. Its Shanghai Cooling Science Studio accelerates R&D for advanced thermal gels like TC-3080, targeting high-performance computing and immersion cooling. Dow’s self-healing gel technologies enhance long-term reliability by repairing micro-cracks in electronic systems. With 2025 sales of approximately $43 billion, the company is targeting $2 billion EBITDA uplift through its Transform to Outperform strategy. This positions Dow at the forefront of high-performance silicone gel solutions.

Shin-Etsu expands carbon-neutral silicone gels with large-scale investments and sustainable product roadmap

Shin-Etsu Chemical is strengthening its leadership in environmentally friendly silicone gels through its Green Silicones™ initiative, offering carbon-neutral certified products aligned with Scope 3 targets. The company is deploying over ¥100 billion in investments to expand production capacity for high-performance gels in automotive sensors, aerospace electronics, and medical devices. Its newly established Sustainable Silicone Business Development Department coordinates global rollout of eco-friendly and recyclable silicone gel technologies. Strong financial performance, with projected ¥2.4 trillion revenue and ¥635 billion operating income in 2026, supports continued innovation. Expansion across Japan and Thailand enhances supply chain resilience. This strategy positions Shin-Etsu as a key supplier of sustainable and semiconductor-grade silicone gels.

Wacker focuses on specialty silicone gels for EV modules supported by PACE efficiency program

Wacker Chemie AG is optimizing its silicone gel portfolio under the Project PACE initiative, targeting over €300 million in annual savings by 2026. The company forecasts EBITDA between €550 million and €700 million, supported by recovery in specialty chemicals demand. Wacker is prioritizing addition-curing silicone gels for high-reliability potting applications in EV power modules, particularly within the European automotive sector. Its shift toward hyperpure semiconductor-grade materials enhances margins and aligns with electronics market growth. A Gold EcoVadis sustainability rating strengthens its competitive positioning in regulated EU markets. This focused strategy enables Wacker to capture high-value opportunities in power electronics and advanced manufacturing.

Elkem advances bio-based silicone gels and circular chemistry through strategic portfolio transformation

Elkem Silicones is undergoing strategic realignment in 2026, exploring divestment of its Silicones division to sharpen focus on silicon and carbon materials. The company introduced the PURESIL™ ORG series, including bio-based elastomer gels derived from sunflower carriers, offering biodegradable alternatives for personal care formulations. Its Industrial Symbiosis initiative reduces carbon footprint by recycling hydrochloric acid waste into raw materials, improving sustainability metrics. Elkem reported NOK 7.5 billion operating income in 2025, with its Silicones segment achieving 23% EBITDA growth. Recognition through SEAL Sustainability Awards highlights its leadership in circular chemistry. This positions Elkem as a pioneer in eco-designed silicone gel solutions.

Merck scales semiconductor-grade silicone gels with €500 million Taiwan megasite and Level Up program

Merck KGaA is strengthening its position in high-purity silicone gels through its Electronics segment and global Level Up investment program exceeding €3 billion. The inauguration of its 150,000 m² Kaohsiung megasite enables large-scale production of specialty gels and materials for AI chips and advanced semiconductor nodes. The company projects 2026 net sales between €20.0 billion and €21.1 billion, with strong growth driven by semiconductor demand. Its portfolio includes patternable gels and high-purity materials for high-NA EUV lithography and advanced interconnect technologies. Strategic acquisitions and R&D investments reinforce its science-led innovation model. This positions Merck as a critical supplier in next-generation semiconductor and AI hardware ecosystems.

United States: Power Electronics Reliability and Cleanroom-Grade Expansion

The United States silicone gel industry is being structurally reshaped by electrification, semiconductor localization, and healthcare material innovation. In September 2025, Dow launched DOWSIL™ EG-4175, a high-reliability silicone gel engineered for 800V electric vehicle architectures. Designed to withstand continuous operation up to 180°C, the material directly addresses thermal stress challenges in seventh-generation IGBT modules used in advanced traction inverters. Beyond EVs, U.S.-based developers have introduced intrinsic self-healing silicone gels that autonomously repair micro-cracks caused by thermal cycling. This capability is particularly relevant for power modules in solar inverters and wind turbine converters, where maintenance access is limited and lifecycle reliability is a procurement priority.

Federal industrial policy is reinforcing domestic demand. Following the rollout of $52.7 billion under the CHIPS Act, U.S. silicone producers have expanded cleanroom-grade silicone gel production to support new semiconductor mega-fabs in Arizona and Ohio, where contamination control and ionic purity are non-negotiable. Healthcare is emerging as a parallel growth vector, supported by the FDA’s 2025 guidance on long-term absorbable materials, which has accelerated adoption of drug-loaded silicone gel sheets for hypertrophic scar management. At the formulation level, sustainability considerations are now embedded, with major U.S. chemical clusters transitioning to PFAS-free surfactant systems to stay ahead of tightening EPA mandates. Infrastructure resilience is another driver, as silicone dielectric gels are increasingly specified in grid-scale battery energy storage systems to mitigate moisture-induced short circuits in high-humidity coastal regions.

Germany: Bio-Based Transition and Medical-Grade Differentiation

Germany’s silicone gel market is increasingly defined by carbon reduction, regulatory leadership, and high-margin medical applications. At COMPAMED 2025, Wacker Chemie AG introduced SILPURAN® eco 2114, the industry’s first silicone gel derived from biogenic methanol, delivering an estimated 28% reduction in production-related carbon footprint. This launch reflects a broader shift among German manufacturers toward bio-attributed feedstocks as energy costs rise and downstream customers demand verifiable sustainability credentials. In parallel, German research institutions published late-2025 findings on programmable release profiles in silicone gel adhesives, enabling next-generation transdermal drug delivery systems with precise burst and steady-state dosing characteristics.

Medical and regulatory considerations are converging. Wacker’s 2025 introduction of a silicone gel capable of withstanding gamma radiation sterilization marks a strategic departure from reliance on ethylene oxide processes, aligning with hospital sterilization preferences and regulatory scrutiny. The German Chemical Industry Association reported a sector-wide pivot toward specialty silicones in 2025, as producers seek to offset structural energy cost pressures through higher-margin automotive and med-tech gels. Germany is also at the forefront of regulatory enforcement, spearheading the EU REACH 2026 roadmap that mandates silicone gels contain less than 0.1% of D4, D5, and D6 siloxanes, effectively accelerating reformulation across the European supply chain.

Japan: Precision Purity and Sustainable Materials Breakthroughs

Japan’s silicone gel industry continues to differentiate through ultra-high purity standards, recyclability breakthroughs, and tight integration with electronics and mobility ecosystems. In January 2025, Wacker Asahikasei Silicone commissioned a new Tsukuba production line dedicated to silicone-based thermal interface materials and gels for traction batteries, reinforcing Japan’s role in EV thermal management. Semiconductor-driven demand is equally pronounced, with Japanese manufacturers standardizing 7N and 8N purity levels for silicone gels used in wafer-level and advanced packaging, a prerequisite for AI accelerator and logic devices where ionic contamination directly impacts yield.

Material innovation has addressed long-standing sustainability constraints. In November 2025, Shin-Etsu Chemical announced the development of a recyclable thermoplastic silicone gel that can be reshaped under heat, overcoming the traditional limitations of thermoset systems. This advance aligns with corporate strategies such as Shin-Etsu Polymer’s “Global & Growth 2027” plan, which prioritizes silicone-based medical tubing, catheter systems, and gels as core high-value segments. Beyond electronics and healthcare, new soft-gel formulations released in 2025 are being deployed to protect ADAS camera sensors, combining vibration damping with optical clarity to support increasingly sensor-dense vehicle platforms.

China: Regulatory Consolidation and Volume-Led Electronics Demand

China remains the largest global consumer of silicone gels, with demand anchored in consumer electronics, solar photovoltaics, and food-contact applications. The issuance of GB 4806.16-2025 by the National Health Commission in September 2025 introduced stringent VOC limits for silicone gels used in food-contact scenarios, compelling widespread reformulation and compliance investments ahead of the 2026 enforcement timeline. In consumer electronics, domestic producers such as Hoshine Silicon scaled production of ultra-soft silicone gels to support miniaturization trends in 5G smartphones, where space constraints and shock absorption requirements are intensifying.

Environmental policy is reshaping industry structure. The Ministry of Ecology and Environment’s 2025 directives accelerated the closure of smaller, high-pollution silicone plants, consolidating production within integrated green chemical parks that offer better emissions control and feedstock efficiency. In the energy sector, China continues to dominate global consumption of silicone gels for solar PV junction box potting. The 2025 transition toward UV-stable gel formulations reflects module manufacturers’ push to extend operational lifetimes to 30 years, supporting bankability requirements for utility-scale solar projects.

South Korea: Semiconductor Packaging and Bio-Based Cosmetics Pivot

South Korea’s silicone gel industry is closely aligned with semiconductor packaging and premium consumer applications. In 2025, Wacker Chemie AG inaugurated an additional specialty silicone production line in Jincheon to supply advanced potting gels for the K-Semiconductor Belt. Demand is being driven by the rapid adoption of High Bandwidth Memory (HBM3e), where low-metal-content silicone gels are essential to prevent ionic contamination in three-dimensional stacked architectures used in AI and high-performance computing.

Corporate integration is enabling portfolio expansion. Following its full merger with Momentive Performance Materials, KCC Corporation launched a 2025 initiative focused on developing fully bio-based elastomer and gel systems for the premium K-Beauty cosmetics segment. This move reflects South Korea’s broader strategy of combining materials science expertise with brand-driven consumer markets, while maintaining a strong foothold in semiconductor-grade silicone gel technologies.

Comparative Snapshot: Silicone Gel Industry by Country

Silicone Gel Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Differentiation

|

|

United States

|

EV power electronics, semiconductors

|

Self-healing gels, cleanroom-grade production

|

|

Germany

|

Med-tech, sustainability compliance

|

Bio-methanol gels, gamma-sterilizable systems

|

|

Japan

|

Semiconductors, EV thermal management

|

7N–8N purity, recyclable thermoplastic gels

|

|

China

|

Consumer electronics, solar PV

|

Volume scale, UV-stable and food-compliant gels

|

|

South Korea

|

HBM packaging, premium cosmetics

|

Low-metal gels, bio-based cosmetic formulations

|

Silicone Gel Market Report Scope

Silicone Gel Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$6.3 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Product Form (Soft Silicone Gels, Silicone Gel Sheets & Films, Two-Component Silicone Gels, UV-Cured Silicone Gels), By Chemical Composition (Polysiloxane Gels, Silicone Elastomer Gels, Vinyl-Terminated Gels, Phenyl-Functional Gels), By Application (Medical & Healthcare, Electrical & Electronics, Automotive, Cosmetics & Personal Care, Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co. Ltd., Momentive Performance Materials Inc., Elkem ASA, Evonik Industries AG, Gelest Inc., Hoshine Silicon Industry Co. Ltd., CHT Group, Siltech Corporation, Specialty Silicone Products Inc., KCC Corporation, Zhejiang Xinan Chemical Industrial Group, Nusil Technology, Applied Silicone Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicone Gel Market Segmentation

By Product Form

- Soft Silicone Gels

- Silicone Gel Sheets & Films

- Two-Component Silicone Gels

- UV-Cured Silicone Gels

By Chemical Composition

- Polysiloxane Gels

- Silicone Elastomer Gels

- Vinyl-Terminated Gels

- Phenyl-Functional Gels

By Application

- Medical & Healthcare

- Electrical & Electronics

- Automotive

- Cosmetics & Personal Care

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicone Gel Industry

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co. Ltd.

- Momentive Performance Materials Inc.

- Elkem ASA

- Evonik Industries AG

- Gelest Inc.

- Hoshine Silicon Industry Co. Ltd.

- CHT Group

- Siltech Corporation

- Specialty Silicone Products Inc.

- KCC Corporation

- Zhejiang Xinan Chemical Industrial Group

- Nusil Technology

- Applied Silicone Corporation

*- List not Exhaustive