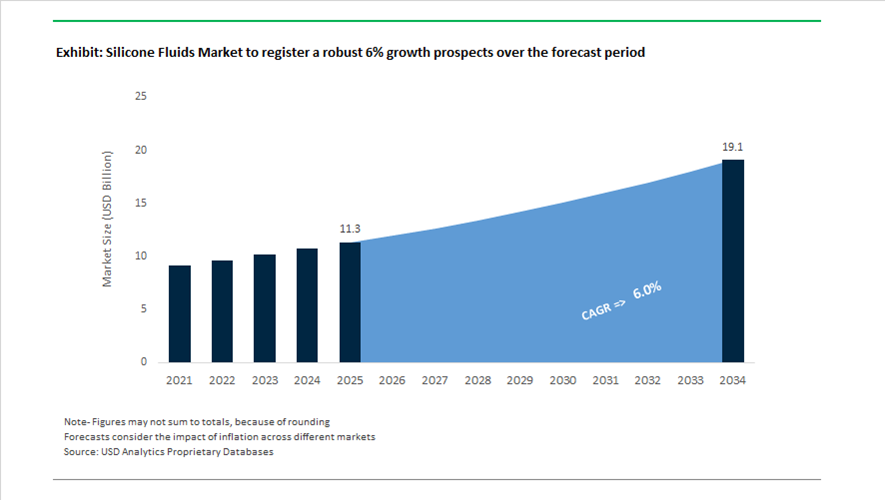

Silicone Fluids Market Valuation 2025–2034: $11.3 Billion to $19.1 Billion at 6% CAGR Anchored in EV Thermal Management and Sustainable Formulations

The global silicone fluids market is valued at $11.3 billion in 2025 and is projected to reach $19.1 billion by 2034, registering a CAGR of 6%. Expansion is driven by growing demand for polydimethylsiloxane (PDMS) fluids, silicone emulsions, dielectric cooling fluids, thermal interface materials, and specialty conditioning agents across automotive electrification, renewable energy storage, industrial coatings, personal care, and electronics manufacturing. Silicone fluids offer thermal stability, dielectric strength, hydrophobicity, lubricity, and oxidative resistance, making them critical in traction battery cooling systems, high-voltage insulation, 5G infrastructure, and advanced cosmetic formulations. Structural demand from EV battery packs, power electronics modules, and carbon-neutral material development is reshaping capital allocation within the global silicone value chain.

In March 2024, Dow Inc. and Corning Incorporated entered a strategic collaboration to develop silicon-based fluid technologies for 5G infrastructure and renewable energy storage, combining Dow’s fluid chemistry expertise with Corning’s advanced materials capabilities. In May 2024, Momentive Performance Materials completed the acquisition of specialized silicone assets from Elkem ASA, strengthening European production capacity for high-performance silicone fluid additives and securing supply chain integration. During 2024–2026, Shin-Etsu Chemical advanced construction of its ¥2.1 billion silicone plant in Zhejiang Province, China, scheduled for completion in February 2026. The facility is focused on high-functional silicone emulsions and environmentally optimized fluid formulations tailored for China’s electronics and industrial sectors.

Innovation in decarbonization and EV-focused thermal materials accelerated in 2025. In January 2025, Wacker launched a new production line in Japan for silicone-based Thermal Interface Materials designed to improve heat dissipation in traction batteries and power electronics for electric vehicles. In May 2025, Dow introduced Decarbia™ low-carbon silicone elastomer blends derived from decarbonized silicon metal feedstocks and verified through third-party lifecycle assessments. In April 2025, BASF finalized regulatory approval to acquire Solvay’s European silicones business, strengthening its position in specialized silicone fluids used in construction chemicals and industrial coatings. In November 2025, Dow unveiled DOWSIL™ CB-2251 Fluid at in-cosmetics Asia, engineered to enhance moisture retention and conditioning performance in premium hair care formulations.

Structural portfolio realignment and pricing adjustments defined early 2026. In February 2026, Elkem ASA signed a final agreement to divest the majority of its Silicones division to Bluestar, repositioning itself as a metals-focused company while Bluestar consolidates downstream silicone fluid and elastomer operations. The same month, Elkem’s MIRASIL™ N-DML 15 received recognition at the SEAL Awards for replacing volatile cyclic silicones in cosmetics with more sustainable long-chain alternatives. Effective February 1, 2026, Wacker implemented a price increase of up to 25% across silicone fluids, emulsions, and resins, citing the doubling of platinum prices required for addition-curing silicone chemistry. These developments highlight how electromobility, high-performance personal care, cost pressures in catalyst metals, and corporate restructuring are shaping competitive dynamics in the silicone fluids market through 2034.

High-Impact Trends and Strategic Opportunities in the Global Silicone Fluids Market

Dielectric Silicone Fluids Powering AI-Driven Immersion Cooling Architectures

The silicone fluids market is undergoing a structural demand shift as artificial intelligence workloads push data center power densities beyond the limits of conventional air cooling. AI training and inference facilities now routinely exceed 30 megawatts per site, with rack densities surpassing 100 kilowatts, forcing hyperscale operators to adopt single-phase immersion cooling. In this environment, dielectric silicone fluids are rapidly displacing mineral oils due to superior thermal stability, higher flashpoints, and long-term material compatibility with sensitive electronic components.

In 2025, hyperscale capital expenditure reached unprecedented levels, with Microsoft allocating approximately $80 billion and Amazon Web Services committing more than $100 billion toward AI-enabled data center infrastructure. Around 60% of new data center construction in 2025 occurred in the United States, where regulatory scrutiny and safety standards favor silicone dielectric fluids over hydrocarbon alternatives. Operational data from AI-focused facilities indicate that immersion-cooled systems can reduce cooling energy consumption by roughly 40%. Polydimethylsiloxane based silicone fluids are gaining preference because they maintain stable viscosity across wide temperature ranges, eliminating the sludging and oxidative degradation observed in mineral oils during continuous high-load operation.

Global Reformulation Pivot Driven by D4, D5, and D6 Regulatory Compliance

Regulatory developments in Europe are reshaping silicone fluid formulations worldwide, effectively setting a global compliance benchmark. The enforcement of EU REACH Regulation 2024/1328 has accelerated the transition toward low-cyclic volatile methylsiloxane fluids, transforming compliance from a regional requirement into a master formulation strategy for multinational brands. As of June 2024, expanded restrictions entered into force, with concentration limits above 0.1% by weight for D4, D5, and D6 scheduled for near-total prohibition across wash-off and leave-on cosmetic products by 2026 and 2027.

This regulatory cliff has triggered a rapid wave of portfolio renewal. In July 2025, Elkem introduced new PURESIL and MIRASIL low-cyclic silicone fluid platforms designed to replicate the sensory and performance attributes of traditional silicones while meeting sub-0.1% thresholds. In parallel, consumer goods leaders such as L’Oréal and Unilever have accelerated R and D investment into linear silicone fluids and bio-based alternatives to maintain market access in the European Union. The designation of cyclic siloxanes as Substances of Very High Concern has elevated compliant silicone fluids from optional reformulation choices to critical supply chain requirements.

Silicone Super-Spreaders Enabling Precision Agrochemical Delivery

Global food security pressures and the rapid expansion of sustainable farming practices are opening a differentiated opportunity for silicone fluids in agricultural adjuvants. With organic farmland surpassing 96 million hectares globally, growers are seeking solutions that improve pesticide efficacy while minimizing environmental impact. Silicone-based super-spreaders are emerging as a tactical enabler, dramatically enhancing droplet spread, rainfastness, and foliar uptake of active ingredients.

Research validated in 2025 demonstrates that silicone adjuvants enable spray droplets to spread up to ten times more effectively than conventional surfactants, facilitating rapid stomatal infiltration through the waxy leaf cuticle. This mechanism can reduce chemical runoff and lower reapplication frequency by an estimated 15 to 20%. Adoption is being further accelerated by precision agriculture technologies, particularly drone-based spraying. As the agricultural adjuvants market approaches $5.06 billion in 2025, silicone fluids are becoming the preferred carrier for ultra-low volume applications, allowing operators to cover larger acreage with less water and fewer chemical inputs.

Anti-Stiction Silicone Fluids for High-Speed EV Battery Manufacturing

The scale-up of electric vehicle battery production is creating a high-value opportunity for silicone fluids as process aids and functional coatings in roll-to-roll manufacturing. As gigafactories race to meet 2030 electrification targets, yield losses caused by film blocking, electrode sticking, and membrane tearing have emerged as critical bottlenecks. High-purity silicone fluids are increasingly applied as non-migrating anti-stiction coatings to prevent separator films and electrodes from adhering during high-speed processing.

The market for silicone materials in electric vehicles was valued at approximately $2.1 billion in 2024, with the fluids segment projected to deliver the fastest growth through 2030. Beyond thermal management, silicone fluids are becoming essential in silicon-based anode production, where polymer-silicone systems are used to manage the material’s 300% volumetric expansion during charge cycles. In a capacity-constrained battery sector, anti-stiction silicone coatings enable higher line speeds, reduce downtime for cleaning, and protect delicate membranes from damage. This positions silicone fluid suppliers as strategic process partners to large-scale battery manufacturers such as Tesla, Northvolt, and BYD, rather than commodity material vendors.

Silicone Fluids Market Share and Segmentation Insights

Straight Silicone Fluids Dominate the Silicone Fluids Market Due to Versatile Industrial Performance

Straight silicone fluids accounted for 52.80% of the silicone fluids market in 2025, establishing them as the most widely used silicone fluid category across industrial and specialty applications. Based primarily on polydimethylsiloxane (PDMS) chemistry, straight silicone fluids provide exceptional thermal stability, low surface tension, oxidation resistance, and chemical inertness, making them suitable for a wide range of uses including release agents, lubricants, defoamers, and hydraulic fluids. Their availability across a broad viscosity spectrum enables customization for diverse industrial formulations. A key 2025 industry development is the growing focus on viscosity grade optimization, where manufacturers supply silicone fluids in precisely controlled viscosity ranges tailored for specific applications such as foam control, mold release, and damping systems.

Industrial & Automotive Applications Drive Silicone Fluid Demand for High-Performance Lubrication and Processing

Industrial and automotive applications represent the largest segment in the silicone fluids market, accounting for 38.60% of total consumption in 2025 due to the extensive use of silicone fluids across manufacturing and mechanical systems. These fluids serve as mold release agents for plastics and rubber processing, specialty lubricants for high-temperature machinery, damping fluids for precision equipment, and defoamers in industrial processing. The large scale of global manufacturing activity continues to support strong consumption of silicone fluid formulations. A major 2025 market trend is the rising demand for high-performance lubricants capable of operating in extreme environments, where silicone-based lubricants offer superior thermal stability, oxidation resistance, and wide operating temperature ranges compared with conventional petroleum-based lubricants.

Silicone Fluids Market Competitive Landscape

The 2026 silicone fluids market is driven by demand for dielectric cooling fluids, VOC-compliant linear siloxanes, and carbon-neutral chemistries. Key players are advancing EV thermal fluids, immersion cooling solutions, and localized production to meet AI infrastructure growth and sustainability mandates.

Dow leads decarbonized silicone fluids with EV-grade thermal gels and fully integrated supply chain

Dow Inc. (Dow Consumer Solutions) is dominating the silicone fluids market through its Decarbia™ reduced-carbon platform and vertically integrated manufacturing model. The launch of DOWSIL™ EG-4175 supports next-generation EV power electronics, delivering thermal stability up to 180°C for 800V battery systems and renewable energy inverters. Its low-carbon silicone fluids, backed by Environmental Product Declarations, enable OEMs to meet Scope 3 emission targets. The Transform to Outperform initiative targets $2 billion EBITDA uplift, supported by $1 billion investment in AI-driven automation in 2026. Dow’s integrated feedstock-to-fluid value chain ensures supply security for electronics, automotive, and personal care sectors. This positions the company as a leader in high-performance, sustainable silicone fluid technologies.

Shin-Etsu expands high-purity silicone fluids with global investments and advanced cosmetic dispersants

Shin-Etsu Chemical is strengthening its leadership in high-purity silicone fluids through a ¥100 billion+ global investment strategy. The company forecasts ¥2.4 trillion in 2026 revenue with ¥635 billion operating income, driven by strong electronics materials demand. Its new cosmetic silicone dispersants address UV stability and formulation challenges in high-SPF, long-wear beauty products. Expansion of the Akron, Ohio facility enhances development of thermal management fluids and gap fillers for EV and aerospace markets. Renewable energy integration at its Thailand site reduces carbon intensity of siloxane production. This combination of innovation and sustainability reinforces Shin-Etsu’s dominance in electronics-grade and personal care silicone fluids.

Wacker boosts functional silicone fluid capacity and cost efficiency through Project PACE strategy

Wacker Chemie AG is optimizing its silicone fluids portfolio under Project PACE, targeting over €300 million in annual cost savings by 2026. The company expects EBITDA between €550 million and €700 million, supported by recovery in the Silicones segment. New large-scale production plants in China are expanding output of high-purity silicone fluids and emulsions for textiles, personal care, and industrial processing. Wacker’s strength in hyperpure polysilicon provides critical feedstock synergy for electronic-grade siloxanes. Strategic focus on high-margin specialty fluids enhances competitiveness amid silicon metal price volatility. This integrated approach positions Wacker as a key supplier in global silicone fluid markets.

Elkem transitions to silicon-focused strategy while advancing circular silicone fluid recycling capabilities

Elkem ASA is undergoing a structural transformation following the divestment of its Silicones division to Bluestar, marking a shift toward core silicon and carbon materials. The company reported NOK 31 billion operating income in 2025 and maintains global production across five continents. Prior to divestment, Elkem validated recycling of high consistency rubbers and silicone fluids, enabling circular reuse in industrial applications. Its CDP “A” rating highlights leadership in environmental performance and sustainable operations. The 2026 strategy focuses on carbon solutions and upstream silicon cost advantages. This repositioning strengthens Elkem’s role in the broader silicone value chain.

Evonik expands specialty silicone fluids for 3D printing and advanced manufacturing applications

Evonik Industries AG is advancing its silicone fluids portfolio within its Advanced Technologies segment, which generated €5.97 billion in 2025 revenue. The company reported 2025 adjusted EBITDA of €1.87 billion and projects €1.7–€2.0 billion in 2026. Its TEGO® Dispers 695 additive supports radiation-curing inks and high-speed industrial printing, enabling precision in 3D additive manufacturing. Rising demand for silicone fluids in membranes, foams, and advanced plastics highlights its role in next-generation materials. Evonik’s dynamic dividend policy ensures reinvestment flexibility for innovation-led growth. This strategy positions the company as a key innovator in high-performance siloxane-based fluids.

Japan: High-Purity Innovation Anchored in Thermal Management and EUV Lithography

Japan continues to anchor the global silicone fluids industry through precision chemistry, energy efficiency, and deep integration with advanced electronics and mobility platforms. In January 2025, Wacker Chemie AG inaugurated a specialty production facility in Tsukuba dedicated to silicone-based Thermal Interface Materials, reinforcing Japan’s leadership in heat-dissipating silicone fluids for power electronics and traction batteries. This investment directly supports the rapid adoption of immersion and gap-filler cooling solutions in next-generation EV platforms operating on 800-volt architectures. Parallel to this, Shin-Etsu Chemical announced the development of high-purity phenyl-silicone fluids with ultra-low volatility in late 2025, engineered specifically for Extreme Ultraviolet lithography environments where outgassing control is mission-critical.

Regulatory and policy alignment is further shaping product portfolios. Under Japan’s 2025 Greenhouse Gas Emission Intensity Index, domestic producers have materially reduced production intensity versus 1990 benchmarks, accelerating the shift toward low-energy cold-processing silicone fluids. Product innovation remains robust, with amino-functional silicone fluids launched at CITE Japan 2025 to improve fiber bonding in premium textiles and personal care formulations. The government’s designation of silicone precursors as Strategic Critical Materials has unlocked tax credits for bio-based silicon chemistry, while automotive demand is rapidly scaling dielectric silicone oils for battery immersion cooling, positioning Japan at the intersection of sustainability, electronics, and EV safety.

China: Regulatory Reset Driving Water-Borne Systems and Localized Self-Sufficiency

China’s silicone fluids market is undergoing a structural transition driven by regulation, cost dynamics, and domestic self-sufficiency goals. The issuance of the mandatory GB 4806.16-2025 standard by the National Health Commission in September 2025 introduced strict VOC limits for food-contact silicone fluids, setting a clear compliance timeline through September 2026. This regulatory milestone is accelerating reformulation toward low-VOC and water-borne silicone fluid emulsions. In parallel, Wacker Chemie AG expanded downstream silicone fluid capacity at its Zhangjiagang site in March 2025, reinforcing localized supply for specialty emulsions across food, personal care, and industrial applications.

Cost pressures have reshaped strategic priorities. With silicon metal prices rising sharply since 2023, Dow implemented price adjustments in April 2025 and pivoted its Chinese portfolio toward higher-margin medical and electronics-grade silicone fluids. Amendments to China’s Environmental Protection Tax Law in late 2025 expanded VOC tax pilots, further incentivizing water-borne systems. Infrastructure mandates under the 14th Five-Year Plan have driven sustained demand for silicone defoamers in modular wastewater treatment units, while domestic players such as Hoshine Silicon Industry have localized high-viscosity dimethyl silicone fluid production to serve aerospace and defense programs, reducing reliance on imports.

South Korea: Semiconductor-Led Demand and EV-Focused Fluid Specialization

South Korea’s silicone fluids industry is tightly coupled with its semiconductor and EV supply chains. In 2025, Wacker Chemie AG expanded its Jincheon site, adding dedicated capacity for specialized silicone fluids and sealants aligned with the K-Semiconductor Belt initiative. Complementing this, Shin-Etsu Chemical invested approximately $50 million in September 2025 to strengthen domestic supply of high-performance silicone components for electronics manufacturing.

Automotive electrification is a parallel growth engine. Following its full integration of Momentive Performance Materials, KCC Corporation entered strategic partnerships with Tier-1 automotive suppliers to develop dielectric silicone fluids optimized for EV battery packs. Semiconductor fabs operated by Samsung and SK Hynix have mandated ultra-low metal silicone fluids for wafer cleaning, pushing local manufacturers toward 7N-grade purification technologies. Sustainability initiatives gained traction in 2025 with the launch of low-carbon silicone elastomer blends using carbon-neutral silicon metal feedstocks, signaling a convergence of performance and environmental compliance.

United States: Decarbonization, Data Centers, and PFAS-Free Reformulation

The United States silicone fluids market is increasingly shaped by decarbonization policy, advanced cooling technologies, and regulatory pressure on legacy chemistries. In May 2025, Dow introduced its Decarbia™ portfolio, positioning low-carbon silicone fluids and elastomers backed by verified Environmental Product Declarations as a new industry benchmark. This aligns with federal sustainability procurement and infrastructure programs. Concurrently, the U.S. Department of Energy awarded grants in late 2025 to accelerate silicone-based immersion cooling fluids for high-density AI data centers, targeting substantial reductions in cooling-related energy consumption.

Semiconductor policy has reinforced demand for ultra-high purity silicone fluid precursors. CHIPS Act subsidies have driven the construction of on-site UHP chemical delivery systems for advanced logic nodes, expanding the addressable market for siloxane intermediates. In personal care, state-level restrictions on cyclic siloxanes have accelerated innovation in biodegradable and sugar-modified silicone fluids, showcased at SCC Suppliers’ Day 2025. Infrastructure investments across the Battery Belt have further increased the use of silane-siloxane water repellents to protect reinforced concrete, broadening non-consumer end-use demand.

European Union (Germany Focus): Restriction-Driven Innovation and Circular Processing

The European Union, led by Germany, is redefining the silicone fluids landscape through restrictive legislation and circular economy initiatives. Under updated REACH provisions effective June 6, 2026, products containing D4, D5, or D6 siloxanes above 0.1% by weight will be prohibited in multiple consumer applications, forcing accelerated reformulation across cosmetics and industrial fluids. German manufacturers have responded by prioritizing alternative linear and functional silicone fluids with improved environmental profiles.

Transparency and circularity are emerging as competitive differentiators. In December 2025, Evonik Industries published comprehensive Environmental Product Declarations for its PROTECTOSIL® range, setting new benchmarks for lifecycle disclosure in building protection fluids. Capacity expansion remains active, with Wacker Chemie AG and Evonik Industries jointly establishing a new specialty silicones site in Karlovy Vary, Czech Republic. Late-2025 pilot projects in Germany demonstrated depolymerization units capable of recycling waste silicone fluids back into high-purity monomers, aligning the sector with the EU’s Zero Pollution ambition.

Comparative Snapshot: Silicone Fluids by Country

Silicone Fluids Market County Level Snapshot

|

Region

|

Primary Demand Driver

|

Strategic Focus Area

|

|

Japan

|

EV thermal management, EUV lithography

|

High-purity phenyl fluids, dielectric oils

|

|

China

|

Regulation and infrastructure

|

Water-borne emulsions, defoamers, localization

|

|

South Korea

|

Semiconductors and EV batteries

|

Ultra-low metal fluids, dielectric EV oils

|

|

United States

|

Decarbonization and data centers

|

Low-carbon fluids, immersion cooling

|

|

EU (Germany)

|

REACH restrictions, circularity

|

D4/D5/D6 alternatives, recycled monomers

|

Silicone Fluids Market Report Scope

Silicone Fluids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.3 Billion

|

|

Market Size (2034)

|

$19.1 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Product Type (Straight Silicone Fluids, Modified Silicone Fluids, Silicone Emulsions), By Viscosity Range (Low Viscosity, Medium Viscosity, High Viscosity), By Application (Industrial & Automotive, Personal Care & Healthcare, Chemicals & Materials, Electronics & Energy, Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co. Ltd., Momentive Performance Materials Inc., Evonik Industries AG, Elkem ASA, Hoshine Silicon Industry Co. Ltd., Gelest Inc., Zhejiang Xinan Chemical Industrial Group, KCC Corporation, Kaneka Corporation, Siltech Corporation, CHT Group, Elkay Chemicals Pvt. Ltd., Hubei BlueSky New Material Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silicone Fluids Market Segmentation

By Product Type

- Straight Silicone Fluids

- Modified Silicone Fluids

- Silicone Emulsions

By Viscosity Range

- Low Viscosity

- Medium Viscosity

- High Viscosity

By Application

- Industrial & Automotive

- Personal Care & Healthcare

- Chemicals & Materials

- Electronics & Energy

- Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicone Fluids Industry

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co. Ltd.

- Momentive Performance Materials Inc.

- Evonik Industries AG

- Elkem ASA

- Hoshine Silicon Industry Co. Ltd.

- Gelest Inc.

- Zhejiang Xinan Chemical Industrial Group

- KCC Corporation

- Kaneka Corporation

- Siltech Corporation

- CHT Group

- Elkay Chemicals Pvt. Ltd.

- Hubei BlueSky New Material Inc.

*- List not Exhaustive