Mold Release Agents Market 2025–2034: PFAS Elimination, Bio-Based Formulations, and High-Performance Composites Driving $9.2 Billion Outlook

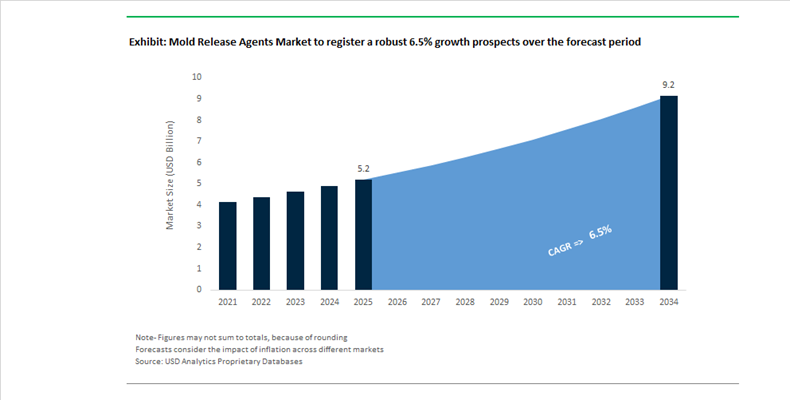

The Mold Release Agents Market is projected to expand from $5.2 billion in 2025 to $9.2 billion by 2034, registering a CAGR of 6.5%. Growth is being shaped by regulatory elimination of PFAS-based chemistries, rising demand for high-durability composite tooling systems, and the acceleration of water-based and carrier-free technologies. Industrial users across tire manufacturing, aerospace composites, thermoforming, die-casting, and engineered wood are shifting toward sustainable formulations that reduce transfer, minimize tool contamination, and improve cycle efficiency. Environmental mandates in Europe and North America are redefining formulation chemistry, forcing suppliers to innovate around fluorine-free slip systems and low-VOC solvent carriers while maintaining release performance at elevated mold temperatures.

In September 2025, Chem-Trend confirmed that it had surpassed its 2025 objective of transitioning a significant portion of its portfolio to PFAS-free formulations. This milestone aligns with global pressure to remove persistent fluorinated compounds from industrial processing. Earlier, at Tire Technology Expo 2024, Chem-Trend introduced next-generation tire molding solutions designed to reduce residue buildup and improve press restart efficiency, directly enhancing throughput in high-volume tire plants. Leadership restructuring in March 2024, with the appointment of a new CEO, marked a strategic pivot toward digitalized customer interfaces and accelerated development of water-based aerospace and composite release systems. The integration of Deurowood® additives further strengthened Chem-Trend’s engineered wood and decorative panel footprint, expanding its multi-sector positioning.

Bio-based innovation is gaining measurable traction. In May 2024, Kao Corporation launched LUNAFLOW RA, a solvent-free and fluorine-free mold release agent utilizing cellulose nanofibers inspired by pitcher plant surface biology. This biomass-derived formulation delivers high durability with reduced reapplication frequency in rubber and resin molding operations. Similarly, Stoner Molding Solutions expanded its TraSys® semi-permanent water-based line through 2024–2025, including TraSys 9825 for hot compression molding. In April 2025, Stoner introduced the B445 denesting agent, a food-safe silicone-based release solution engineered for thermoforming and extrusion packaging lines to reduce static and improve cycle consistency. In aerospace, Marbocote introduced TRE45 ECO, capable of thermal stability up to 450°C for carbon fiber and steel tooling applications, addressing advanced composite curing requirements.

Upstream raw material strategies are also evolving. In October 2025, Wacker Chemie AG launched the PACE cost optimization initiative, refocusing its silicone and polymer divisions toward high-margin sectors including electromobility and renewable energy—both heavy consumers of precision mold release technologies. Across 2025, manufacturers increasingly aligned feedstock sourcing with the Acetone One-Step Process to reduce the carbon intensity of solvent intermediates used in release formulations. This shift supports ESG-driven procurement strategies among automotive and electronics OEMs. The cumulative effect of PFAS phase-out mandates, cellulose-based innovation, semi-permanent water-based systems, and carbon-conscious feedstock integration is repositioning the mold release agents industry toward higher performance, regulatory-compliant, and sustainability-optimized chemistries across global manufacturing ecosystems.

Mold Release Agents Market Trends and Opportunities

Trend: Mandatory Transition to PFAS-Free Mold Release Formulations in Automotive Manufacturing

The mold release agents market is undergoing a structural reset as automotive OEMs and Tier 1 suppliers accelerate the elimination of PFAS-based chemistries from molding operations. This shift is being driven by converging regulatory, legal, and supply chain risks rather than voluntary sustainability positioning. Under the finalized PFAS reporting rule issued by the U.S. Environmental Protection Agency, manufacturers are required to disclose all intentionally added PFAS used since 2011, with the formal reporting window opening in July 2025. Parallel state-level actions such as Vermont’s Act 54, which bans intentionally added PFAS in several industrial product categories from January 2026, are forcing immediate audits of mold release inventories across automotive production lines.

OEM substitution roadmaps are amplifying this transition. In April 2025, Freudenberg introduced PFAS-free sealing materials for electric powertrain systems, including alternatives to fluorinated elastomers and FKM compounds. These material shifts require compatible mold release agents that preserve surface integrity, enable downstream painting, and avoid adhesion failures. In response, silicone-based and hybrid polymer release systems are rapidly replacing fluorinated formulations. Anticipating broader EU restrictions following REACH scientific evaluations expected to conclude by 2026, Shin-Etsu Silicone launched fully PFAS-free silicone emulsions in mid-2025. These systems deliver the low surface tension required for complex automotive geometries while eliminating long-term environmental persistence, positioning PFAS-free release agents as the new baseline for compliant vehicle manufacturing.

Trend: Scaling Renewable Energy Manufacturing with Water-Based Semi-Permanent Release Systems

The rapid scale-up of offshore wind and composite-intensive renewable energy infrastructure is reshaping demand patterns within the mold release agents market. Wind turbine blade manufacturers are pushing blade lengths beyond 100 meters, increasing mold surface complexity and cycle-time sensitivity. To meet these demands while aligning with VOC reduction targets, producers are standardizing on water-based, semi-permanent mold release systems. At the Wind Turbine Blades Europe congress in December 2025, manufacturers highlighted solvent-free production as a strategic imperative, citing measurable reductions in hazardous air pollutants and improved worker safety without sacrificing release durability.

Water-based semi-permanent systems are also delivering operational efficiency gains. Advanced solutions from suppliers such as Chem-Trend are being integrated into automated spray-up and vacuum infusion processes. These systems minimize mold fouling and residue buildup, reducing mold cleaning frequency and extending the service life of high-value composite tooling. In parallel, energy price volatility has accelerated the adoption of concentrated water-based formulations that lower transportation weight and carbon footprint. As turbine OEMs embed circular economy metrics into 2030 sustainability commitments, water-based semi-permanent release agents are becoming the preferred standard across large-scale renewable energy manufacturing.

Opportunity: High-Temperature Mold Release Agents for HP-RTM EV Structures

The electrification of mobility is creating a high-margin opportunity for mold release agents engineered for High-Pressure Resin Transfer Molding processes. HP-RTM is increasingly used for mass production of carbon fiber reinforced plastic components such as battery enclosures, crash structures, and vehicle chassis. These applications demand release agents capable of withstanding extreme thermal and mechanical stress. High-performance polymers like PEEK and PEKK, commonly used in structural brackets, exhibit glass transition temperatures above 140°C and continuous use temperatures approaching 260°C. Release agents must therefore maintain chemical stability up to 250°C to prevent part seizure, surface defects, or mold damage.

Internal mold release additives are gaining traction as cycle time optimization becomes critical. By blooming to the surface during resin cure, these internal systems reduce the need for external reapplication and can shorten production cycles by up to 40% in complex geometries such as B-pillars and roof frames. Emerging Liquid Compression Molding processes further reinforce this opportunity by requiring release agents that support zero-pressure resin deposition, ensuring delicate fiber preforms remain undisturbed during rapid injection. Suppliers capable of certifying thermal endurance, compatibility with fast-curing resins, and consistent performance across high-volume EV platforms are positioned to capture disproportionate value in this segment.

Opportunity: Food-Grade Mold Release Solutions for Sustainable Molded Fiber Packaging

The global shift from single-use plastics toward molded fiber packaging is unlocking a fast-growing opportunity for food-contact compliant mold release agents. As regulators push fiber-based alternatives derived from bagasse, wheat straw, bamboo, and other agricultural residues, manufacturers require release chemistries that enable clean demolding without compromising compostability, aesthetics, or food safety. The EU Packaging and Packaging Waste Regulation mandates that a growing share of food packaging be reusable or recyclable by 2030, accelerating investment in thermoformed fiber and processed pulp technologies.

This transition is driving demand for non-silicone, plant-based release agents that meet FDA and EU food-contact standards. In mid-2025, industry initiatives introduced clean-label emulsifiers such as hydrolyzed sunflower lecithin, offering biodegradable oil-in-water release layers suitable for high-speed automated lines. At the same time, agricultural waste valorization in regions like India and Southeast Asia is expanding the use of non-wood pulp substrates, including paddy waste and mycelium-based materials. These novel fibers require specialized wax and wax ester-based release agents tailored to higher moisture content and variable fiber morphology. As molded fiber packaging scales across food service, quick-service restaurants, and retail trays, food-grade mold release agents are emerging as a critical enabler of sustainable packaging economics and regulatory compliance.

Mold Release Agents Market Share and Segmentation Insights

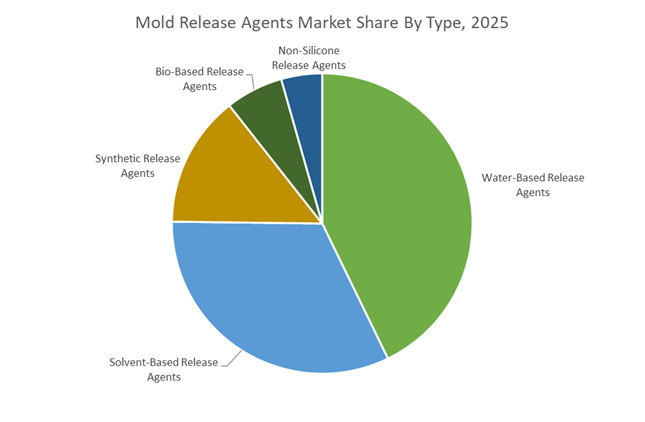

Water-Based Release Agents Lead Mold Release Agents Market Driven by Environmental Compliance and Advanced Formulations

Water-based release agents accounted for 42.80% of the Mold Release Agents Market share in 2025, making them the dominant product category across industrial molding processes. These release agents are widely used in plastic injection molding, rubber molding, composite molding, die casting, and polyurethane processing, where they prevent molded parts from adhering to mold surfaces and ensure clean demolding without damaging the finished component. Water-based formulations have gained widespread adoption because they offer low volatile organic compound (VOC) emissions, improved worker safety, and regulatory compliance, which are increasingly important in manufacturing environments subject to environmental regulations. Compared with solvent-based alternatives, water-based release agents also reduce fire hazards and workplace exposure risks. In 2025, technological advancements have significantly improved water-based release agent performance. New formulations incorporate nano-scale release additives, advanced emulsification systems, and improved surface-active agents, enabling multiple mold releases per application and improved mold surface protection while maintaining environmentally friendly characteristics required by modern manufacturing regulations.

Automotive and Transportation Sector Drives the Largest Demand for Mold Release Agents

Automotive and transportation accounted for 34.80% of the Mold Release Agents Market share in 2025, making vehicle manufacturing the largest end-use sector for release agent technologies. Modern automotive production involves numerous molding processes including plastic injection molding for dashboards and interior panels, die casting for engine and transmission components, polyurethane molding for seating systems, and composite molding for lightweight structural components. Each of these processes requires specialized mold release formulations to ensure consistent part quality, efficient production cycles, and minimal mold maintenance. The large-scale production volumes of passenger vehicles, commercial vehicles, and transportation equipment continue to drive significant demand for release agents in automotive manufacturing plants worldwide. In 2025, the automotive industry's shift toward lightweight vehicle structures using carbon fiber composites and glass fiber reinforced plastics has increased demand for advanced release agents formulated for high-temperature composite curing processes, resin transfer molding (RTM), and prepreg manufacturing systems, supporting the production of structural composite parts used to reduce vehicle weight and improve energy efficiency.

Mold Release Agents Market Competitive Landscape

The mold release agents market in 2026 is driven by semi-permanent coatings, water-based low-VOC formulations, and integrated clean-seal-release systems. Competitive differentiation centers on thermal stability, ultra-thin film deposition (<5 µm), and compatibility with automated composite and lightweight manufacturing processes.

Henkel drives semi-permanent mold release efficiency with FREKOTE® and integrated clean-seal-release systems

Henkel AG & Co. KGaA leads the mold release agents market through its LOCTITE® FREKOTE® platform, engineered for multi-release performance without transfer contamination. Its semi-permanent coatings chemically bond with mold surfaces, enabling high-precision composite molding in aerospace and marine applications. The FREKOTE® Aqualine® C-600 water-based solution addresses regulatory pressure by delivering low-VOC, non-flammable performance with reduced mold fouling in FRP processes. Henkel’s “lowest cost per release” strategy is reinforced by FMS mold sealers that extend coating durability and reduce downtime by up to 20%. Its integrated Clean-Seal-Release ecosystem enhances tool life, process consistency, and operational efficiency.

Wacker strengthens silicone-based release technologies with cost-efficient and sustainable material innovations

Wacker Chemie AG is advancing high-performance silicone mold release agents aligned with EV, semiconductor, and medical manufacturing requirements. Its PACE program targets over €300 million in annual cost savings, strengthening competitiveness in specialty silicones. Wacker’s innovations in liquid silicone rubber (LSR) and specialty elastomers require precision release chemistries for defect-free molding. The expansion of its specialty silanes technology center in China enhances localized formulation capabilities for high-growth Asian markets. With biomethanol-based silicones and EcoVadis Gold sustainability credentials, Wacker is positioning itself as a leader in low-carbon, high-purity release solutions. Its expertise in silicone chemistry ensures superior thermal stability and surface performance.

Dow integrates mold release chemistry with construction and polyurethane growth through global supply chain optimization

Dow Inc. is leveraging its “Transform to Outperform” strategy to enhance productivity and expand its performance solvents and release agent portfolio. With approximately $40 billion in 2025 sales, Dow is focusing on polyurethane and construction chemicals where release agents are critical for insulation, automotive seating, and precast concrete applications. Its solutions improve surface finish, reduce adhesion, and enhance operational efficiency in infrastructure projects. Dow integrates release agents within a broader material science ecosystem, supported by AI-driven supply chain optimization. This ensures consistent product availability across global manufacturing hubs. Its scale, integration, and application diversity strengthen its competitive positioning in industrial release solutions.

Shin-Etsu leads high-purity silicone release agents for semiconductor and food-safe molding applications

Shin-Etsu Chemical Co., Ltd. dominates the Asian mold release agents market with high-purity silicone formulations tailored for electronics and food packaging. Its oil, emulsion, and water-soluble release agents offer exceptional heat resistance, low surface tension, and chemical inertness. The KM-97 series provides industry-leading anti-blocking and low-migration performance for food-contact applications. Shin-Etsu’s Green Silicones™ initiative addresses global environmental compliance by reducing volatile siloxanes and improving product safety. Its vertically integrated silicone supply chain ensures consistent quality for semiconductor encapsulation and precision molding. The company’s versatility across complex geometries strengthens its leadership in high-spec applications.

Daikin delivers fluoropolymer-based ultra-low friction release coatings for high-performance industrial applications

Daikin Industries, Ltd. is differentiating itself through advanced fluorochemical-based mold release technologies, particularly PTFE and FEP coatings. Its FEP coating powders create pinhole-free, chemically resistant surfaces that enable long-lasting release performance in aggressive resin molding environments. Daikin’s expansion into the Global South enhances its supply of high-performance coatings for emerging industrial markets. The company is targeting high-growth sectors such as lithium-ion batteries, data centers, and medical devices, where low friction and biocompatibility are critical. Its solution-based approach and strong operating performance in 2026 highlight resilience despite macroeconomic challenges. Daikin’s fluoropolymer expertise positions it at the premium end of the mold release agents market.

United States: Regulatory Disclosure, PFAS Exit, and Digitalized Application Control

The United States mold release agents market is being reshaped by a combination of regulatory disclosure requirements, accelerated PFAS phase-outs, and capital investment in high-value manufacturing. The June 5, 2025 TSCA Section 8(d) final rule issued by the U.S. Environmental Protection Agency extends the deadline to May 22, 2026 for the submission of unpublished health and safety studies covering 16 chemicals commonly used in high-performance mold release formulations. This requirement is increasing compliance costs while simultaneously favoring suppliers with well-documented toxicological datasets and reformulated low-risk chemistries. In parallel, the U.S. Food and Drug Administration has elevated food chemical safety within its 2026 Human Food Program priorities, accelerating the shift toward certified food-grade release agents based on bio-derived vegetable oils for packaging and food-contact molding applications.

From an industrial perspective, capacity expansion and formulation innovation remain central. Henkel completed a USD 30 million expansion of its Brandon, South Dakota facility in September 2025, doubling the site to 70,000 square feet to support advanced adhesives, coatings, and release systems for EV battery housings and electronics molding. At the same time, Chem-Trend reached a major inflection point by fully discontinuing PFAS-containing products across its global operations, transitioning U.S. automotive and aerospace customers to water-based Zyvax and Mavcoat portfolios. Supporting these chemistry shifts, U.S. manufacturers are adopting SprayIQ and DilutionIQ digital monitoring platforms during the 2025–2026 procurement cycle, enabling real-time dosage control that reduces waste and improves consistency in high-volume die casting and polyurethane molding.

Germany: Microplastic Compliance, Water-Based Portfolios, and AI-Led Formulation Design

Germany’s mold release agents market is tightly aligned with European sustainability and chemical control frameworks, with Regulation (EU) 2023/2055 acting as a primary catalyst. German producers have completed the transition to intentionally added microplastic-free internal and external release agents to meet the October 2025 information and reporting obligations, prompting widespread reformulation toward water-based and polymer-dispersed systems. According to 2025 sustainability stewardship disclosures, leading German chemical groups now report water-based products accounting for approximately 75% of their European release agent portfolios, a strategic response to tightening VOC emission costs under EU environmental policy.

Innovation is increasingly data-driven. German R&D centers are deploying AI-enabled predictive modeling to shorten development cycles for semi-permanent release agents designed for high-temperature composite and aerospace molding. These tools simulate surface energy, thermal stability, and demolding performance before pilot-scale synthesis, materially reducing time to qualification. In a high-value niche application, Evonik expanded its collaboration with InVitria in November 2025 to supply recombinant human serum albumin as a coating material for micro-molded biopharmaceutical components, reinforcing Germany’s role in precision medical molding where release agent purity and residue control are commercially decisive.

China: Silicone Capacity, EV Die Casting, and Feedstock Policy Alignment

China’s mold release agents market is evolving through a combination of upstream capacity additions, policy support for advanced materials, and downstream demand from electric vehicle manufacturing. Shin-Etsu Chemical is scheduled to complete its new silicone emulsions plant in Zhejiang Province by February 2026, significantly expanding the availability of environmentally oriented silicone-based release agents for plastics, rubber, and composite molding across East Asia. This expansion aligns with the September 2025 petrochemical stabilization work plan from the Ministry of Industry and Information Technology, which prioritizes high-end polyolefins and advanced fine chemicals as strategic feedstocks for next-generation internal release systems.

Regulatory adjustments are also influencing cost structures. The withdrawal and amendment of Quality Control Orders for polypropylene and vinyl chloride monomer during late 2025 introduced short-term pricing volatility for raw materials used in molding agents, incentivizing localized sourcing and reformulation. On the demand side, China’s rapidly expanding EV supply chain is a major pull factor. High-volume aluminum die casting for vehicle structures has driven the adoption of micro-spray release technologies that cut chemical consumption by up to 30% per cycle, improving both cost efficiency and environmental performance in large-scale foundry operations.

India: Quality Control Orders, Infrastructure Demand, and ESG Spillover Effects

India’s mold release agents market is being shaped by regulatory standardization and infrastructure-led consumption. In late 2025, the Department of Chemicals and Petrochemicals issued multiple gazette notifications updating Quality Control Orders for fatty acids and copolymers, tightening import specifications for key inputs used in lubricating oils and release pastes. These measures are pushing domestic formulators toward higher-purity raw materials and documented supply chains, particularly for automotive and industrial molding applications.

Demand-side momentum is coming from construction and transport infrastructure. The national push toward precast concrete for highway and urban projects has generated a 15% year-on-year increase in demand for specialized concrete release agents, with clear preference for water-soluble formulations that leave no surface residue and support faster curing cycles. Although located outside India, the 2025 commissioning of a solar-powered release agent manufacturing site in Valinhos, Brazil, serving global emerging markets, has set a new ESG reference point. Multinational suppliers active in India are increasingly expected to mirror this low-carbon operating model, influencing procurement decisions by infrastructure and OEM customers.

Comparative Overview: Country-Level Dynamics in the Mold Release Agents Market

Mold Release Agents Market County Level Snapshot

|

Country / Region

|

Primary Policy Driver

|

Industrial Focus Area

|

Technology Shift

|

Strategic Impact

|

|

United States

|

TSCA 8(d), FDA food safety

|

EV, electronics, food packaging

|

PFAS-free, digital dosing

|

Compliance-led premiumization

|

|

Germany

|

EU microplastic and VOC rules

|

Aerospace, medical molding

|

Water-based, AI-designed agents

|

Sustainability-driven innovation

|

|

China

|

MIIT petrochemical plan, EV growth

|

Aluminum die casting, plastics

|

Silicone emulsions, micro-spray

|

Scale efficiency and localization

|

|

India

|

QCO updates, infrastructure push

|

Precast concrete, automotive

|

Water-soluble formulations

|

Standards-driven demand growth

|

Mold Release Agents Market Report Scope

Mold Release Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.2 Billion

|

|

Market Size (2034)

|

$9.2 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Type (Water-Based Release Agents, Solvent-Based Release Agents, Bio-Based Release Agents, Synthetic Release Agents, Non-Silicone Release Agents), By Technology Channel (Internal Release Agents, External Release Agents, Semi-Permanent Release Agents, Sacrificial Release Agents), By Application (Die Casting, Polyurethane Molding, Rubber Molding, Composite Molding, Plastic Molding, Concrete and Wood-Composite Processing, Food Processing and Pharmaceutical Tableting), By End-Use Industry (Automotive and Transportation, Aerospace and Defense, Construction and Infrastructure, Electronics and Electrical, Healthcare and Medical Devices, Consumer Goods and Packaging)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Chem-Trend, Henkel, Wacker Chemie, Daikin Industries, Shin-Etsu Chemical, Dow, Evonik Industries, Michelman, Lantor, Croda International, McGee Industries, Miller-Stephenson, Marbocote, Chukyo Yushi, Moresco

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Mold Release Agents Market Segmentation

By Type

- Water-Based Release Agents

- Solvent-Based Release Agents

- Bio-Based Release Agents

- Synthetic Release Agents

- Non-Silicone Release Agents

By Technology Channel

- Internal Release Agents

- External Release Agents

- Semi-Permanent Release Agents

- Sacrificial Release Agents

By Application

- Die Casting

- Polyurethane Molding

- Rubber Molding

- Composite Molding

- Plastic Molding

- Concrete and Wood-Composite Processing

- Food Processing and Pharmaceutical Tableting

By End-Use Industry

- Automotive and Transportation

- Aerospace and Defense

- Construction and Infrastructure

- Electronics and Electrical

- Healthcare and Medical Devices

- Consumer Goods and Packaging

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Mold Release Agents Market

- Chem-Trend

- Henkel

- Wacker Chemie

- Daikin Industries

- Shin-Etsu Chemical

- Dow

- Evonik Industries

- Michelman

- Lantor

- Croda International

- McGee Industries

- Miller-Stephenson

- Marbocote

- Chukyo Yushi

- Moresco

*- List not Exhaustive