Specialty Resins Market Valuation 2025–2034: $8.4 Billion to $14.4 Billion at 6.2% CAGR Accelerated by Bio-Based Epoxy, AI Manufacturing, and Circular Thermoplastics

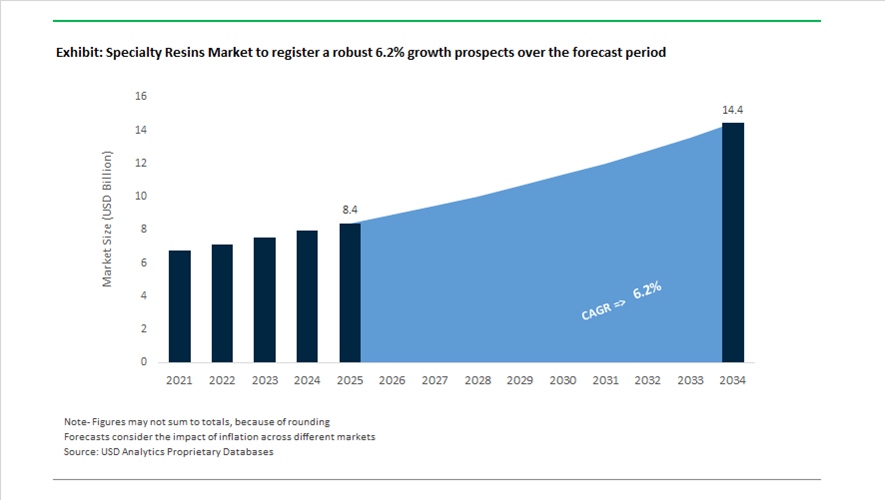

The global specialty resins market is valued at $8.4 billion in 2025 and is projected to reach $14.4 billion by 2034, expanding at a CAGR of 6.2%. Growth is driven by increasing demand for high-performance epoxy resins, specialty acrylics, thermoset systems, bio-based polyamides, liquid thermoplastic composites, and ultra-low VOC curing agents across aerospace, construction, automotive lightweighting, industrial flooring, electronics, and CASE applications. The market is shifting toward ISCC PLUS-certified bio-circular resins, SVHC-free epoxy systems, recyclable thermoplastics, and AI-optimized manufacturing platforms. Regulatory pressure on volatile organic compounds and hazardous substances is accelerating the adoption of next-generation resin chemistries engineered for cold curing, recyclability, and carbon footprint reduction.

Strategic restructuring began in March 2024 when BASF inaugurated its second dispersions production line at the Daya Bay site in Huizhou and rebranded regional facilities as BASF Specialty Material Huizhou and Jiangsu to reflect a pivot toward high-value applications. In October 2024, Evonik announced the divestment of its standard polyester and polyolefin resin businesses, redirecting capital toward liquid polybutadienes and specialty acrylics for medical packaging and tire performance. In December 2024, Hexion completed the acquisition of Smartech, integrating AI-powered manufacturing analytics into specialty resin production to enhance yield optimization and environmental efficiency in wood panel and industrial thermoset systems. In March 2025, BASF and Sika launched Baxxodur® EC 151, an amine building block that reduces VOC emissions by up to 90% while enabling rapid curing at low outdoor temperatures between 5°C and 10°C.

Portfolio upgrades and sustainability-driven innovation accelerated in 2025. In June 2025, Hexion consolidated five global laboratories into a centralized Innovation Lab in Dublin, Ohio to accelerate thermoset resin development for aerospace and construction. At the European Coatings Show in 2025, Westlake Epoxy introduced its EpoVIVE™ sustainable portfolio featuring ISCC PLUS mass-balanced bio-circular epoxy systems and SVHC-free formulations for industrial flooring and protective coatings. In December 2025, Arkema announced the proposed sale of its impact modifiers and processing aids business to concentrate on higher-value specialty materials, with transaction completion expected in Q1 2026.

Circular composite technology and geographic expansion defined early 2026. In January 2026, Arkema commenced operations at its Rilsan® Clear transparent polyamide facility in Singapore, supplying bio-based high-performance resins for optics, electronics, and medical devices. At JEC World in February 2026, Arkema showcased progress with Elium® liquid thermoplastic resins enabling fully recyclable composite structures. In February 2026, Henkel agreed to acquire Stahl for €2.1 billion, integrating specialty coatings and resin technologies into its Adhesive Technologies platform for automotive and premium packaging applications. In the same month, Westlake Epoxy expanded its distribution partnership with Brenntag across South and West India to strengthen access to EPON™ and EPIKURE™ resin systems for construction and CASE markets. These strategic acquisitions, AI-enabled manufacturing upgrades, low-VOC hardener launches, bio-based polyamide expansions, and recyclable composite advancements are reshaping the specialty resins market trajectory toward 2034.

Key Trends and High-Value Opportunities in the Specialty Resins Market

High-Temperature Resin Qualification for EV Thermal Management Systems

The Specialty Resins Market is experiencing a decisive shift as electric vehicle platforms transition toward 800V and higher-voltage architectures, fast-charging cycles, and increasingly compact battery pack designs. These developments have elevated thermal resilience, flame resistance, and dielectric stability from desirable attributes to mandatory qualification criteria. Specialty epoxy systems, modified polyphenylene ether, and silicone-based encapsulants are now being specified to maintain mechanical and electrical integrity at continuous operating temperatures exceeding 150°C while containing thermal runaway propagation within increasingly stringent safety windows.

OEM qualification benchmarks are tightening rapidly. In April 2025, SABIC demonstrated the performance of its Stamax 30YH570 long-glass-fiber polypropylene resin for battery module housings. This specialty resin enables intercellular wall thicknesses as low as 1 mm, delivering meaningful weight reduction at the pack level while meeting UL 2596 thermal and mechanical safety requirements during runaway events. Such design freedom is critical as automakers pursue higher energy density without increasing vehicle mass.

Direct material innovation is accelerating in parallel. Asahi Kasei’s 2025 testing of its Xyron G532Z modified polyphenylene ether resin confirmed that a 3 mm plate could withstand exposure to an 850°C flame for more than five minutes without burn-through. This aligns with emerging global regulatory expectations for a minimum five-minute containment window, reinforcing specialty resins as core safety-enabling materials rather than passive structural components in next-generation EV platforms.

Low-Dielectric Specialty Resins for 5G mmWave and Early 6G Infrastructure

The global rollout of 5G millimeter-wave networks and early-stage 6G research programs is reshaping material demand in advanced electronics. High-frequency signal transmission places extreme constraints on dielectric constant and dissipation factor, pushing conventional PCB resin systems beyond their functional limits. Specialty resins with ultra-low loss characteristics are now essential to minimize signal attenuation and phase distortion in high-density interconnects, particularly for AI accelerators and data center processors.

A notable technological inflection occurred in December 2025 when Toray Industries announced a photo-definable polyimide sheet optimized for glass core substrates. This resin enables simultaneous redistribution layer patterning and Through-Glass Via filling, reducing elastic modulus by roughly one-third versus conventional materials. The resulting suppression of glass cracking under thermal cycling directly addresses one of the most critical yield risks in high-density packaging for advanced AI and networking chips.

Capacity expansion is following demand signals from hyperscale infrastructure. Throughout 2025, Mitsubishi Gas Chemical and Panasonic reported sustained investment in ultra-low-loss resin production for next-generation PCB laminates. These materials are increasingly specified for sub-10 micron via processing, where dimensional stability and thermal expansion control are as critical as electrical performance. As AI server density increases, low-dielectric specialty resins are becoming strategic bottlenecks rather than interchangeable inputs.

Circular-by-Design Bio-Based and Recyclable Thermoset Resins

The wind energy and marine sectors are confronting an end-of-life challenge for composite-intensive assets such as turbine blades and hull structures. This has created a high-margin opportunity for specialty resins engineered around circularity principles, including reversible cross-linking chemistries and bio-based feedstocks derived from lignin and itaconic acid. These systems aim to preserve the mechanical toughness of traditional epoxies while enabling material recovery at scale.

In October 2025, Toray introduced a breakthrough recycling technology capable of decomposing carbon fiber reinforced plastics while retaining more than 95% of the tensile strength of recovered fibers. By chemically breaking down three-dimensional crosslinked thermosetting resins at substantially lower temperatures than pyrolysis, this process reduces CO₂ emissions by over 50%. Such performance materially improves the economics of composite recycling and positions circular thermosets as viable alternatives to landfill or energy recovery.

Commercial adoption is gaining momentum. Ineos Composites expanded its Envirez portfolio in late 2025, offering unsaturated polyester resins with significant renewable content. These materials are now being qualified for fiberglass-reinforced boat hulls, bridge components, and wind-related structures, demonstrating parity with petroleum-based incumbents in pultrusion and compression molding while enabling sustainability-driven procurement decisions.

Radiation-Curable Resins for Additive Manufacturing and Digital Packaging

The acceleration of localized, on-demand production is driving rapid adoption of radiation-curable resin systems across additive manufacturing and digital printing. UV and LED-curable specialty resins deliver near-instant cure, zero or near-zero VOC emissions, and sharply reduced energy intensity, aligning directly with global green factory and decarbonization initiatives.

Industrial-scale validation is advancing quickly. At the Formnext exhibition in November 2025, Arkema and Axtra3D announced the qualification of N3xtDimension flame-retardant and water-soluble resins for high-speed stereolithography. These UV-curable formulations are engineered for aerospace and electronics applications, maintaining mechanical integrity at temperatures approaching 150°C while enabling complex geometries at production-scale throughput.

Energy efficiency metrics reinforce the opportunity. Data presented at RadTech 2025 indicates that LED-curable industrial finishes can reduce operational CO₂ emissions by up to 40% compared with conventional thermal curing ovens. As a result, specialty acrylate and urethane oligomers are becoming the default choice for high-resolution digital packaging, signage, and industrial coatings, where speed, sustainability, and precision converge to redefine competitive advantage in the specialty resins market.

Specialty Resins Market Share and Segmentation Insights

Thermoset Resins Dominate the Specialty Resins Market Through Superior Mechanical and Thermal Properties

Thermoset resins accounted for 52.80% of the specialty resins market in 2025, making them the leading resin type across high-performance materials applications. Thermoset systems such as epoxy, polyurethane, unsaturated polyester, phenolic, and silicone resins form crosslinked polymer networks that provide excellent thermal stability, chemical resistance, and mechanical durability. These properties support their use in protective coatings, composite materials, electrical insulation systems, and structural adhesives. A major 2025 industry driver is the growing demand for lightweight composite materials, particularly in automotive and aerospace manufacturing, where thermoset resins enable glass fiber and carbon fiber reinforced components that replace metal structures while maintaining strength and durability.

Automotive and Transportation Sector Drives Specialty Resin Consumption

Automotive and transportation represent the largest application segment in the specialty resins market, accounting for 32.80% of global demand in 2025 due to the extensive use of advanced polymer materials in vehicle manufacturing. Specialty resins are used in composite body panels, structural components, coatings, adhesives, and electrical insulation materials. The scale of global vehicle production supports sustained consumption of these high-performance materials. A key 2025 market trend is the evolving material requirements associated with electric vehicle development, where specialty resins are increasingly used for battery enclosures, lightweight structural components, motor insulation systems, and thermally conductive materials required for battery thermal management and high-voltage electronic systems.

Specialty Resins Market Competitive Landscape

The specialty resins market in 2026 is defined by biomass-balanced polymers, EV battery-grade binders, and advanced photopolymers for additive manufacturing. Industry leaders are accelerating decarbonization, near-zero SVOC coatings, and radar-transparent resin systems while expanding capacity in Asia and North America to capture high-growth electronics and mobility applications.

BASF Scales Biomass-Balanced Dispersions and Near-Zero SVOC Resin Technologies for Sustainable Coatings

BASF is leading specialty resins innovation through Verbund integration and low-carbon polymer technologies. Its Dahej and Mangalore plants achieved REDcert² certification, enabling biomass-balanced water-based dispersions for the South Asian market. The company introduced specialty binders supporting automotive “liquid metal” finishes, including Tesseract Blue. BASF has expanded its application scope toward lithium-ion battery anode binders through restructured specialty materials facilities in China. Its near-zero SVOC dispersion technology is gaining traction in indoor coatings aligned with global air quality regulations. Strong integration in acrylic monomers ensures cost-efficient production of high-performance resins.

Evonik Advances High-Performance Polymer Resins and 3D Printing Materials Through Innovation Growth Strategy

Evonik is repositioning toward high-margin specialty resins by focusing on biosolutions, circularity, and energy transition materials. Its portfolio includes PEEK-based resins for medical implants and polymer powders for industrial 3D printing, which recorded strong growth in 2025. The company filed 246 patents in 2025, reinforcing its leadership in bio-based and biodegradable resin technologies. With total sales of €12.9 billion, Evonik maintains profitability through ultra-high purity materials for semiconductor and electronics applications. Its long-term strategy targets €1.5 billion in incremental innovation-driven revenue. The company continues to expand advanced polymer solutions for additive manufacturing and high-performance engineering applications.

Arkema Expands PVDF Resin Capacity and Bio-Based Polyamide Leadership for EV and Electronics Markets

Arkema is strengthening its specialty resins portfolio through targeted investments in high-performance and bio-based materials. The $20 million expansion at its Calvert City site triples PVDF resin capacity for EV battery separators. Its Rilsan® Clear polyamide facility in Singapore enhances global supply of transparent, bio-based engineering resins for electronics and eyewear. Arkema reported €1,251 million EBITDA in 2025, supported by strong recurring cash flow and high-margin specialty segments. Strategic acquisitions, including Dow’s laminating adhesives business, reinforce its acrylic integration. The company continues to lead in sustainable polyamides and advanced adhesive resins for packaging and mobility applications.

Covestro Accelerates Smart Resin Systems and Circular Polycarbonates for Automotive and Electronics Applications

Covestro is advancing specialty resins through circular economy integration and smart material systems. Its Shanghai competence center expansion enables Film Insert Molding for sensor-integrated automotive components. The Pingtung site achieved ISCC PLUS certification, supporting bio-circular attributed resin production in Asia. Covestro launched the CQ-Configurator digital tool to optimize CO₂ footprint and sustainability metrics in polyurethane applications. Its Bayblend® RE polycarbonate uses 25% bio-circular feedstock, targeting EV battery housings and electronics. The company’s focus remains on smart surfaces, radar-compatible materials, and low-carbon resin technologies.

Huntsman Strengthens Polyurethane Resin Portfolio with Carbon-Neutral Innovations and Catalyst Expansion

Huntsman is expanding its specialty resin capabilities through advanced polyurethane systems and catalyst technologies. The Petfurdo facility expansion enhances production of JEFFCAT® catalysts for energy-efficient insulation and low-emission resins. Its carbon-neutral polyurethane innovations target automotive, construction, and footwear sectors. Huntsman reported approximately $6 billion in revenue in 2025, driven by performance materials and advanced chemical segments. Strategic restructuring is enabling a shift away from commodity surfactants toward aerospace-grade and high-performance resins. The company continues to focus on MDI-based systems for next-generation energy-efficient materials.

Mitsubishi Chemical Focuses on Bio-Based Engineering Resins and Circular Polymer Technologies for Sustainable Applications

Mitsubishi Chemical is transitioning toward high-performance and sustainable resin solutions through portfolio optimization and green chemistry innovation. The company is exiting polyester resins for toner applications by mid-2026 to focus on higher-growth segments. Its SoarnoL™ gas barrier resin offers PFAS-free coating solutions for sustainable food packaging. DURABIO™ bio-based engineering plastic is gaining adoption in EV applications, offering high transparency and durability. Mitsubishi is advancing chemical recycling of acrylic resins to enable closed-loop material systems. Its strategy emphasizes carbon-neutral production and high-performance specialty resins for automotive and packaging sectors.

United States Specialty Resins Market Anchored in Battery, Semiconductor, and Construction Demand

The United States specialty resins market is being structurally reshaped by the convergence of lithium-ion battery manufacturing, advanced semiconductor fabrication, and resilient construction activity. In February 2025, Arkema announced a 15% capacity expansion of its PVDF specialty resin facility in Calvert City, Kentucky. This project directly targets high-performance binder resins required for domestic EV battery gigafactories and semiconductor-grade components, reinforcing the U.S. strategy of securing critical materials onshore. Parallel to this, Huntsman Corporation and Dow Chemical have intensified Gulf Coast R&D programs focused on ultra-pure epoxy and polyimide resins, which are essential for next-generation chip encapsulation and 5G and 6G printed circuit boards.

Regulatory and policy frameworks are further accelerating innovation. State-level PFAS restrictions, particularly in California, have triggered a rapid transition toward non-fluorinated specialty resins for water-repellent textiles and packaging. At the same time, the U.S. Department of Energy expanded grant programs in late 2025 to support carbon-negative resin development, encouraging collaborations between resin producers and carbon-capture startups. With U.S. construction spending reaching approximately $2.2 trillion in early 2025, demand for epoxy-based flooring systems, structural adhesives, and high-durability coatings continues to provide a stable downstream pull for specialty resin suppliers.

Germany Specialty Resins Market Defined by Semiconductor Inputs and Circular Economy Disclosure

Germany’s specialty resins industry is increasingly characterized by its role as a European semiconductor chemical hub and a regulatory testbed for circular polymer systems. In October 2025, BASF announced the construction of an electronic-grade ammonium hydroxide plant in Ludwigshafen. This facility strengthens the upstream purity chain for BASF’s Dispersions and Resins division, supporting European chip manufacturing ecosystems that demand ultra-low contamination inputs. In parallel, BASF and Carlyle finalized a carve-out of specialty resins and coatings into a standalone entity, insulating high-margin specialty portfolios from upstream petrochemical volatility.

Sustainability and circularity requirements are reshaping product design. Germany’s updated Circular Economy Act mandates disclosure of recycled-content potential, accelerating the development of specialty resins compatible with enzymatic depolymerization and chemical recycling. At Formnext 2025 in Frankfurt, German producers showcased UV-curable resins with 40% bio-based content tailored for precision industrial additive manufacturing. Complementing this trend, Evonik operationalized a new epoxy-polyester hybrid resin line in late 2024 to support high-voltage insulation applications aligned with European grid modernization initiatives.

Japan Specialty Resins Market Driven by Electronic Purity and Lightweight Mobility

Japan remains a global benchmark for ultra-high-purity and application-specific specialty resins, particularly in electronics and advanced mobility. In October 2025, Evonik opened its Alu5 facility in Yokkaichi, producing fumed alumina additives that enhance scratch resistance and thermal stability in high-performance coating resins. This integration reflects Japan’s emphasis on functional additives that elevate resin performance in demanding electronics and automotive environments.

Strategic portfolio realignment is also underway. Mitsui Chemicals formally exited the toner binder resin segment in fiscal 2025, reallocating capital toward Vision 2030 growth areas such as high-index optical resins and semiconductor materials. Japanese Tier-1 suppliers have simultaneously advanced CFRTP specialty resins, achieving weight reductions of up to 20% in automotive components. To meet the contamination thresholds of 2 nm chip fabrication, domestic producers have implemented Class 100 cleanroom resin packaging lines, reinforcing Japan’s leadership in electronic-grade resin purity.

Singapore Specialty Resins Market as a Regional High-Heat and Sustainable Materials Hub

Singapore continues to function as a strategic Asia-Pacific hub for high-heat and specialty engineering resins. In late 2024, SABIC completed a $170 million expansion of its ULTEM PEI resin facility, positioning the site to serve aerospace and healthcare demand across the region during the 2025–2026 cycle. These applications require polymers with exceptional thermal stability, flame resistance, and dimensional integrity.

Sustainability credentials are becoming equally central. In late 2025, Arkema achieved ISCC PLUS certification for its acrylic and liquid polyester resin operations serving the Singapore and Malaysia corridor. This certification enables the regional rollout of bio-attributed specialty coatings for e-mobility and industrial applications, reinforcing Singapore’s role as a launchpad for sustainable resin technologies across Southeast Asia.

India Specialty Resins Market Accelerated by Incentives and Infrastructure Build-Out

India’s specialty resins market is transitioning from import dependence to domestic capability, supported by policy incentives and infrastructure expansion. The Production-Linked Incentive 2.0 scheme has catalyzed an estimated $2.5 billion investment cycle through 2025, encouraging domestic players such as Sudarshan Chemical and Fineotex to expand into high-performance organic and functional resins. These investments are aimed at serving coatings, textiles, and industrial adhesive markets with locally produced specialty grades.

Infrastructure-linked demand is reinforcing this growth. In 2025, Arkema finalized mass-balance certification at its Navi Mumbai facility, enabling the production of sustainable polyester powder resins for smart city and urban infrastructure projects. As India scales construction, transportation, and digital infrastructure, specialty resins engineered for durability, low emissions, and sustainability are becoming a core component of domestic materials supply chains.

Comparative Snapshot: Specialty Resins Industry by Country

Specialty Resins Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Specialty Resin Focus

|

Structural Direction

|

|

United States

|

EV batteries and semiconductors

|

PVDF, epoxy, polyimide

|

Onshoring and carbon-negative R&D

|

|

Germany

|

Semiconductor inputs and circularity

|

Bio-based and recyclable resins

|

Portfolio carve-outs and disclosure

|

|

Japan

|

Electronics and lightweight mobility

|

Optical, CFRTP, high-purity resins

|

Purity leadership and portfolio shift

|

|

Singapore

|

Aerospace and healthcare

|

High-heat engineering resins

|

Regional sustainability hub

|

|

India

|

Infrastructure and localization

|

Organic and powder resins

|

Incentive-led capacity expansion

|

Specialty Resins Market Report Scope

Specialty Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.4 Billion

|

|

Market Size (2034)

|

$14.4 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Resin Type (Thermoset Resins, Thermoplastic Specialty Resins, Functional and Effect Resins), By Function (Protection and Anti-Corrosion, Electrical and Thermal Insulation, Adhesion and Bonding, Lightweighting and Structural Reinforcement), By Application (Automotive and Transportation, Electrical and Electronics, Building and Construction, Aerospace and Defense, Healthcare and Medical, Consumer Goods and Lifestyle)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., SABIC, Arkema S.A., Evonik Industries AG, Huntsman Corporation, Mitsui Chemicals, Inc., Hexion Inc., DIC Corporation, Mitsubishi Chemical Group, Solvay S.A., Eastman Chemical Company, Toray Industries, Inc., Covestro AG, Nan Ya Plastics Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Resins Market Segmentation

By Resin Type

- Thermoset Resins

- Thermoplastic Specialty Resins

- Functional and Effect Resins

By Function

- Protection and Anti-Corrosion

- Electrical and Thermal Insulation

- Adhesion and Bonding

- Lightweighting and Structural Reinforcement

By Application

- Automotive and Transportation

- Electrical and Electronics

- Building and Construction

- Aerospace and Defense

- Healthcare and Medical

- Consumer Goods and Lifestyle

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Resins Industry

- BASF SE

- Dow Inc.

- SABIC

- Arkema S.A.

- Evonik Industries AG

- Huntsman Corporation

- Mitsui Chemicals, Inc.

- Hexion Inc.

- DIC Corporation

- Mitsubishi Chemical Group

- Solvay S.A.

- Eastman Chemical Company

- Toray Industries, Inc.

- Covestro AG

- Nan Ya Plastics Corporation

*- List not Exhaustive