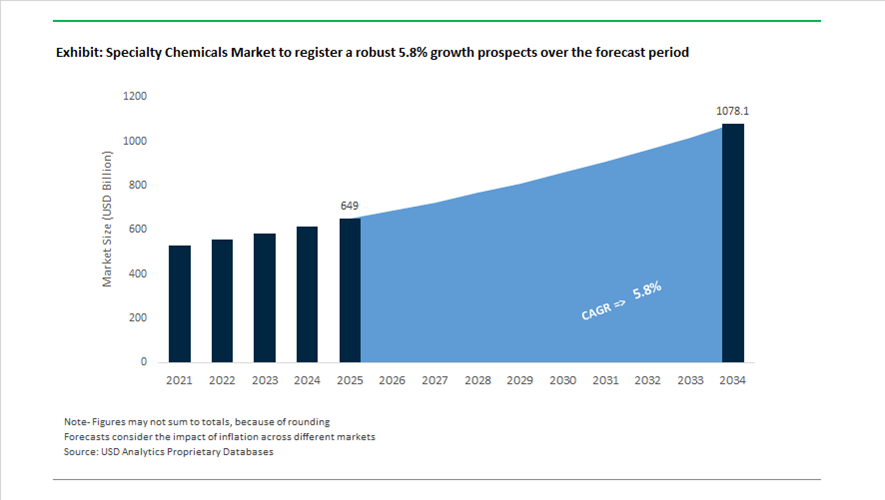

Specialty Chemicals Market Valuation 2025–2034: $649 Billion to $1,078 Billion at 5.8% CAGR Led by Portfolio Realignment, EV Materials, and High-Purity Electronics

The global specialty chemicals market is valued at $649 billion in 2025 and is projected to reach $1,078 billion by 2034, expanding at a CAGR of 5.8%. Growth is driven by increasing demand for high-performance polymers, construction chemicals, electronic-grade intermediates, specialty catalysts, advanced surfactants, flame retardants, pharmaceutical excipients, and battery materials. Unlike commodity chemicals, specialty chemicals are application-specific, performance-driven, and characterized by higher margins, intellectual property intensity, and regulatory compliance requirements. Structural growth drivers include electric vehicle battery expansion, semiconductor fabrication scaling, green hydrogen and renewable fuels, sustainable construction, and PFAS-related regulatory shifts across Europe and North America.

In early 2024, Gujarat Ambuja Exports commissioned a 100 TPD sorbitol unit at Hubli, strengthening India’s pharmaceutical excipient and oral care supply chain. In 2024, BASF expanded Ultramid polyamide capacity in Asia to support electric vehicle battery enclosures and flame-retardant components. In January 2025, Saint-Gobain completed its $1.025 billion acquisition of Fosroc, expanding its construction chemicals and sealants footprint across high-growth emerging markets. In March 2025, Cosmo Specialty Chemicals introduced COSEAL-601, a high-performance heat-seal coating engineered for aluminum foil laminates operating between 120–160°C, enhancing packaging line efficiency for food and pharmaceutical applications. In May 2025, UPL launched Superform as an independent $1.1 billion specialty chemistries subsidiary targeting agriculture, healthcare, mining, and flame retardants.

Strategic divestitures and joint ventures reshaped competitive positioning during 2025. In January 2025, Evonik and Fuhua Tongda Chemicals formed a joint venture to produce specialty-grade hydrogen peroxide in Leshan, China, with supply for semiconductor, solar, and food packaging sectors expected in the first half of 2026. In August 2025, Evonik inaugurated a world-scale alkoxides plant in Singapore, serving Asia-Pacific demand for biodiesel catalysts and synthetic intermediates. In October 2025, BASF divested its decorative paints business to Sherwin-Williams, exiting consumer-facing segments to refocus on core industrial specialty chemicals and surface technologies. In September 2025, Solvay announced the cessation of trifluoroacetic acid production in Germany by early 2026, aligning with tightening PFAS regulations and shifting focus toward aluminum brazing flux technologies.

Cross-border acquisitions and technology-driven expansion continued into 2026. In December 2025, Anupam Rasayan signed a $150 million agreement to acquire Jayhawk Fine Chemicals, establishing its first U.S. manufacturing footprint to serve semiconductor, electronics, and aviation customers with high-value chemistries. The same month, NEXTCHEM signed a binding agreement to acquire Ballestra Group for €126.5 million, adding proprietary technologies in surfactants, oleochemicals, and fluorine derivatives critical for solar cell and lithium-ion battery production, with closing expected in the first half of 2026. These transactions, combined with EV-focused polymer expansion, semiconductor-grade peroxide investments, PFAS-driven portfolio restructuring, and advanced catalyst manufacturing, are shaping the specialty chemicals market trajectory toward $1.08 trillion by 2034.

Key Trends and High-Impact Opportunities in the Specialty Chemicals Market

Strategic Capital Reallocation from Commodities to High-Margin Specialty Segments

The specialty chemicals market is undergoing a decisive capital realignment as Tier-1 chemical producers systematically exit low-margin, cyclical commodity businesses and redeploy capital toward structurally resilient, technology-intensive specialty segments. This shift reflects a fundamental change in shareholder expectations, where return on invested capital, pricing power, and downstream integration now outweigh volume-led scale advantages.

A defining example is the October 2025 Capital Market Update by BASF, which confirmed a disciplined reduction of group CAPEX to approximately €16 billion for the 2025–2028 period. Rather than signaling contraction, this move reflects sharper capital discipline. BASF is closing legacy commodity units such as adipic acid and cyclododecanone at Ludwigshafen while prioritizing high-value assets, including semiconductor-grade sulfuric acid facilities designed to serve advanced electronics manufacturing. This reallocation underscores a strategic pivot toward businesses with higher switching costs, tighter customer integration, and superior margin stability.

A parallel transformation is visible at Dow, which in July 2025 outlined a portfolio optimization strategy targeting more than $6 billion in incremental earnings by 2026. Dow’s emphasis has shifted decisively toward Performance Materials & Coatings, with downstream silicones and liquid cooling chemistries positioned at the core of EV battery thermal management and stationary energy storage systems. By moving away from merchant hydrocarbons and toward application-specific materials, Dow is reinforcing the broader industry trend of monetizing specialty functionality rather than feedstock arbitrage.

Policy-Driven Security Sourcing and Reshoring of Fine Chemical Intermediates

Geopolitical volatility and public health resilience have elevated fine chemicals and pharmaceutical intermediates from commercial inputs to strategic national assets. Governments in the United States and Europe are increasingly using policy instruments, regulatory fast-tracking, and public funding to mandate domestic production of critical APIs and Key Starting Materials, structurally reshaping sourcing decisions across the specialty chemicals value chain.

In August 2025, the U.S. administration established the Strategic API Reserve through executive order, embedding pharmaceutical security into national industrial policy. The SAPIR framework incentivizes domestic specialty chemical manufacturers via the FDA PreCheck mechanism, which compresses regulatory timelines for new pharmaceutical manufacturing facilities. This effectively creates a protected demand environment for U.S.-based producers capable of complex, multi-step organic synthesis at GMP standards.

A similar resilience-first doctrine is now embedded in Europe through the EU Critical Medicines Act, endorsed in late 2025. By prioritizing supply security over lowest-cost sourcing in public procurement, the Act establishes a Union List of Critical Medicines and allocates funding for Strategic Projects that onshore API and KSM production. For specialty chemical suppliers, this policy environment is converting geopolitical risk into a durable, policy-backed demand driver that favors regional production, technical depth, and regulatory credibility over pure cost competitiveness.

Custom Additives for Next-Generation Battery Chemistries

The rapid evolution of battery technologies is creating one of the highest-barrier growth opportunities within the specialty chemicals market. As energy storage systems diversify from LFP to high-nickel NMC and silicon-anode architectures, battery manufacturers are increasingly dependent on ultra-high-purity additives that operate at ppb impurity thresholds and are co-designed with cell chemistries.

By late 2025, demand for advanced lithium-ion battery binders reached a structural inflection point, with high-performance cathode binders accounting for nearly 60% of technical demand within the segment. Specialty producers such as Arkema and Solvay are accelerating the development of non-PFAS binder systems that maintain adhesion and elasticity in silicon-rich anodes while aligning with emerging environmental regulations.

Beyond binders, electrolyte innovation has become a critical value lever. The mechanical instability of silicon particles during cycling has driven demand for proprietary SEI-enhancing additives. Mid-2025 company disclosures confirm active co-development programs between specialty chemical suppliers and battery OEMs for additives such as lithium difluoro(oxalato)borate, designed to stabilize interphases and extend cycle life. These application-specific formulations are embedding specialty chemical suppliers deeper into battery qualification cycles, raising switching costs and long-term contract visibility.

Enzymatic and Fermentation-Based Pathways for Clean-Label Actives

The flavors, fragrances, and cosmetics segment is undergoing a structural shift as brands pursue clean-label positioning, traceability, and carbon reduction without sacrificing consistency or scalability. This is catalyzing a bio-revolution within specialty chemicals, where enzymatic synthesis and fermentation-based pathways are replacing traditional petrochemical routes for high-value actives.

In 2025, advances in microbial conversion of lignin and ferulic acid enabled bio-based vanillin to reach true industrial scale. Borregaard has expanded its lignin-based vanillin platform, offering a wood-derived, nature-identical alternative that meets global demand for sustainable flavoring while decoupling supply from fossil-based guaiacol routes.

Parallel momentum is visible in personal care and fine fragrances. Givaudan and International Flavors & Fragrances are scaling enzymatic synthesis for actives such as squalane and resveratrol. Industry trials conducted in August 2025 demonstrated that enzymatic pathways can reduce carbon footprints by approximately 30% versus conventional extraction or chemical synthesis, while delivering superior purity. This enables specialty chemical producers to capture a measurable green premium, positioning bio-enabled actives as both a sustainability and margin expansion engine within the specialty chemicals market.

Specialty Chemicals Market Share and Segmentation Insights

Pharmaceutical Fine Chemicals Lead the Specialty Chemicals Market Through High-Value Drug Manufacturing Inputs

Pharmaceutical fine chemicals accounted for 24.80% of the specialty chemicals market in 2025, reflecting the high value and technical complexity of chemicals used in pharmaceutical production. This segment includes active pharmaceutical ingredients, advanced intermediates, and high-purity excipients required for modern drug development and manufacturing. These compounds demand stringent quality control, specialized synthesis routes, and regulatory compliance, which contribute to their premium market value. Pharmaceutical manufacturers rely on reliable fine chemical suppliers to support clinical development, commercial drug manufacturing, and specialty therapeutic production. A key 2025 industry trend is the increasing adoption of continuous flow manufacturing in pharmaceutical synthesis, enabling more efficient production of APIs and intermediates while improving process consistency, reducing production costs, and strengthening pharmaceutical supply chain resilience.

Pharmaceutical & Healthcare Sector Drives Specialty Chemical Demand Across Drug Development

Pharmaceutical and healthcare represent the largest end-use segment in the specialty chemicals market, accounting for 28.40% of total demand in 2025 due to the broad range of specialized chemicals required in pharmaceutical production. Drug manufacturing utilizes high-purity intermediates, excipients, reagents, catalysts, and purification materials, creating significant demand for specialty chemical inputs. The sector’s stringent regulatory standards and complex manufacturing requirements support the development of high-performance chemical products. A major 2025 market driver is the continued growth of biologics, cell therapies, and advanced therapeutics, which require specialized inputs such as cell culture media components, growth factors, purification resins, and formulation stabilizers, expanding the scope and value of specialty chemicals used in modern pharmaceutical manufacturing.

Specialty Chemicals Market Competitive Landscape

The global specialty chemicals market in 2026 is defined by green chemistry adoption, EV battery material innovation, and Verbund-style integration. Leading players are optimizing portfolios, scaling regional production, and investing in high-performance materials to mitigate supply chain risks and capture growth in advanced electronics, agriculture, and sustainable applications.

BASF Expands Verbund Integration and High-Performance Materials with Zhanjiang Steam Cracker and TPU Innovation

BASF SE is reinforcing its leadership in specialty chemicals through its “Winning Ways” transformation, highlighted by the commissioning of a 1-million-ton ethylene steam cracker at its Zhanjiang Verbund site powered by renewable energy. Portfolio optimization efforts include divestment of non-core assets to prioritize Agricultural Solutions and Coating Systems. The launch of Freeflex® E 130 TPU nano-membrane targets sustainable apparel and industrial filtration applications. BASF is also advancing its North American footprint with a $1 billion MDI expansion in Louisiana, securing supply of key intermediates. Its integrated Verbund model enhances feedstock efficiency and cost competitiveness. The company’s focus on high-performance materials and regional production strengthens its position in the global specialty chemicals market.

Evonik Strengthens Advanced Technologies Portfolio and Capital Discipline Through Network Optimization and ROCE Focus

Evonik Industries AG is advancing its specialty chemicals strategy by prioritizing high-margin Advanced Technologies and specialty additives. The company reported €1.87 billion EBITDA in 2025 despite declining sales, demonstrating resilience in performance materials. Closure of its Maryland silica plant reflects ongoing network optimization to consolidate production into efficient global hubs. Its new dividend policy linking payouts to 40%–60% of net income underscores disciplined capital allocation. Growth in membranes for gas separation and 3D printing polymers highlights its innovation strength. Evonik’s focus on ROCE improvement and specialty applications enhances profitability and long-term competitiveness.

Clariant Expands Sustainable Specialty Chemicals and High-Margin Additives Through China Capacity Growth and Regulatory Innovation

Clariant AG is strengthening its competitive position through sustainability-driven expansion and innovation in specialty chemicals. The CHF 80 million expansion of its Daya Bay facility boosts production of ethoxylation derivatives for pharmaceuticals and home care applications. Its Dispersogen™ PSL 100 polymeric dispersant supports advanced biological crop protection formulations. Regulatory approval for Licocare RBW renewable wax additives enhances its leadership in food-contact sustainable materials. Integration of Lucas Meyer Cosmetics supports margin expansion toward a 19%–21% target. Clariant’s focus on high-margin additives and regional production strengthens its presence in Asia-Pacific markets.

Arkema Accelerates Specialty Materials Growth with Battery Binder Innovation and Portfolio Realignment

Arkema S.A. is transitioning into a pure-play specialty materials leader, focusing on EV battery technologies and advanced polymers. Its Kynar® Flex LBG 2600 PVDF binder improves battery manufacturing efficiency through low-temperature processing. The opening of a dry coating laboratory supports development of solvent-free battery production technologies. Divestment of its MBS copolymers business reallocates capital toward high-growth specialty additives. The Incellion™ binder portfolio enhances performance of silicon-based battery anodes. Arkema’s alignment with energy transition trends strengthens its position in high-value specialty materials markets.

Solvay Strengthens Essential Chemistry Portfolio with Decarbonization and Cost Leadership Initiatives

Solvay S.A. is reinforcing its position in specialty chemicals through its focus on essential chemistry and operational efficiency. The company achieved a 20.7% EBITDA margin in 2025, supported by €101 million in cost savings. Strategic restructuring includes capacity optimization and site closures in Europe to improve competitiveness. Its 29% reduction in Scope 1 and 2 emissions aligns with decarbonization targets and regulatory requirements. Growth in soda ash and peroxide demand, particularly in healthcare sterilization, supports revenue stability. Solvay’s emphasis on cost leadership and sustainable production strengthens its competitive positioning.

LANXESS Strengthens Consumer Protection and Specialty Additives Portfolio Through Cost Optimization and Strategic Divestments

LANXESS AG is executing a consolidation strategy to enhance financial stability and focus on high-margin specialty chemicals. The company achieved €150 million in savings under its FORWARD! program and is targeting an additional €100 million by 2028. Reduction in net financial liabilities to €2.023 billion strengthens its balance sheet following divestment of its Urethane Systems business. The Consumer Protection segment remains a key growth driver with a 15.4% EBITDA margin, supported by demand for antimicrobial and water treatment solutions. Workforce adjustments in Germany reflect cost management initiatives. LANXESS’s focus on specialty additives and consumer-facing applications enhances its market resilience.

China Specialty Chemicals Market Rebalanced Toward Electronic-Grade Self-Sufficiency

China’s specialty chemicals industry is moving from volume-driven expansion to value-stabilized growth under a coordinated national framework. In late 2025, the Ministry of Industry and Information Technology finalized the Growth Stabilization Plan for 2025–2026, targeting average annual growth above 5% in chemical value added, with explicit prioritization of high-end polyolefins and electronic chemicals. A core objective is semiconductor independence. China has mandated an increase in domestic self-sufficiency for critical lithography and etching intermediates from 85% to above 90% by the end of 2026, specifically for 7 nm and 5 nm nodes. This mandate is driving accelerated investment in purification technologies, specialty reagents, and process controls across electronic-grade supply chains.

Feedstock resilience and compliance are reinforcing this shift. New directives strictly cap conventional refining while incentivizing coal-to-methanol integration and CCUS demonstration projects to stabilize inputs for specialty resins. Industrial execution is visible at scale. BASF SE operationalized new specialty surfactant and high-performance polyamide lines at its Zhanjiang Verbund site in 2025, representing a multibillion-euro commitment to localized specialty manufacturing. Regulatory tightening is also shaping formulations. The late-2025 implementation of GB 4806.16-2025 has forced adoption of high-purity organic and inorganic effects in food packaging, eliminating trace heavy metals in recycled plastic pigments. Complementing this, BASF commissioned a Controlled Free Radical Polymerization dispersant line in Nanjing in November 2025 to enhance stability and performance of specialty additives for industrial coatings.

United States Specialty Chemicals Market Defined by Reshoring, CHIPS Act Purity, and TSCA Transitions

The United States specialty chemicals market is being reshaped by reshoring imperatives, semiconductor-driven purity thresholds, and regulatory substitution. The Society of Chemical Manufacturers & Affiliates 2026 Outlook highlights a decisive pivot in contract manufacturing, with esterification now leading specialized processes at more than half of surveyed firms, doubling since 2024. This reflects a broader move toward resilient domestic supply for pharmaceuticals, coatings, and advanced intermediates. CHIPS Act incentives have accelerated investment in ultra-high purity reagents. Companies such as Air Liquide are investing heavily in electronic chemicals, including a USD 250 million project in Boise, Idaho, while Analog Devices expanded U.S. operations to secure inputs for advanced fabrication, collectively elevating entry barriers across specialty reagent markets.

Regulatory and sustainability pressures are reinforcing portfolio shifts. The Environmental Protection Agency finalized TSCA risk management rules in 2025 covering several specialty solvents, forcing rapid transitions toward low-VOC and halogen-free alternatives. Bio-manufacturing is gaining scale through partnerships. In April 2025, IFF and Kemira launched AlphaBio to commercialize renewable specialty materials for personal care and industrial uses. Regionally, Georgia and Michigan emerged as investment hubs in 2025, securing more than USD 50 billion combined for EV battery chemicals and advanced materials. In packaging, Avient introduced a non-PFAS Hiformer process aid with antioxidants in late 2025, supporting compliance-driven reformulation across consumer markets.

India Specialty Chemicals Market Accelerated by Policy Scale and Export Orientation

India’s specialty chemicals industry is scaling rapidly through coordinated policy instruments and export competitiveness. The Production-Linked Incentive scheme for bulk drugs, with an outlay of ₹6,940 crore, has enabled domestic manufacturing of 41 key starting materials, materially reducing import dependence and strengthening pharmaceutical supply security. Parallel infrastructure policy under the Petroleum, Chemicals and Petrochemical Investment Regions framework targets USD 213 billion in cumulative investment by 2030 across four major regions, anchoring integrated specialty clusters with shared utilities and logistics.

Bio-based innovation and capacity build-out are differentiators. The BioE3 Policy launched in late 2024 provides capital subsidies for bio-foundries producing specialty polymers from agricultural waste, accelerating commercialization beyond pilot scale. Gujarat has consolidated its role as a specialty hub. Perstorp, part of PCG, commissioned an ISCC Plus-certified pentaerythritol plant in Sayakha in early 2025 with 40,000 metric tonnes of annual capacity, its largest Asian investment. Export momentum remains strong. Specialty chemicals account for roughly 80% of India’s chemical exports, with record 2025 shipments of agrochemical intermediates and performance dyes to the United States and Brazil. Feedstock diversification continues as Gulshan Polyols and Sukhjit Starch expanded sorbitol and specialty sweetener capacity to serve pharmaceutical and oral care markets.

Germany Specialty Chemicals Market Anchored by Niche Leadership and Green Feedstocks

Germany’s specialty chemicals sector is demonstrating resilience through niche dominance and green feedstock integration despite energy cost pressures. In October 2025, Alzchem Group AG reported a 9% increase in specialty segment sales, driven by record demand for high-purity creatine under the Creapure brand and defense-related nitroguanidine. Capacity expansion is targeted and value-led. Alzchem is preparing to commission a world-scale guanidine nitrate plant in the second half of 2026 to serve automotive airbag and pharmaceutical intermediate markets.

Sustainability is operationalized across portfolios. Evonik Industries AG expanded POLYVEST polybutadiene capacity at its Marl site during 2024–2025, securing supply for high-performance rubber applications. Green feedstock integration is advancing at Bitterfeld, where Verbio commenced an ethenolysis plant in 2025, producing bio-based specialty molecules such as 9-DAME and 1-decene for detergents and lubricants. Water treatment specialists have transitioned 30% of flocculant portfolios to bio-based solutions to meet forthcoming 2026 EU Water Framework Directive requirements, reinforcing Germany’s premium, compliance-ready positioning.

Brazil Specialty Chemicals Market Boosted by Fiscal Incentives and Bio-Agriculture

Brazil’s specialty chemicals industry is entering an incentive-driven expansion phase following approval of the Special Programme for the Sustainability of the Chemical Industry in November 2025. The program provides up to USD 555 million annually in tax credits for producers reinvesting at least 8% of revenues into R&D, explicitly incentivizing a shift from naphtha toward natural gas and bio-based feedstocks. Braskem is expected to be a primary beneficiary, with potential annual gains estimated at USD 380 million from 2026.

Agricultural biosolutions are a core growth vector. Brazil has become the world’s fastest-growing market for biopesticides, and in late 2025 FMC Corporation launched new fungi-based bioinsecticides targeting corn and soybean pests. Infrastructure investment is reinforcing competitiveness. Braskem approved a BRL 4.2 billion expansion of its Rio de Janeiro complex in October 2025 to modernize ethylene and polyethylene assets, improving energy efficiency and enabling tighter integration with specialty derivatives.

Comparative Snapshot: Country-Level Specialty Chemicals Dynamics

Specialty Chemicals Market County Level Snapshot

|

Country / Region

|

Core Policy Driver

|

Strategic Focus Areas

|

Structural Impact

|

|

China

|

Growth stabilization, self-sufficiency

|

Electronic chemicals, CFRP additives

|

Value-focused consolidation

|

|

United States

|

Reshoring, CHIPS Act, TSCA

|

5N purity reagents, bio-materials

|

Resilient domestic supply

|

|

India

|

PLI, PCPIR, BioE3

|

Export-led specialties, bio-polymers

|

Rapid scale and cost advantage

|

|

Germany

|

Niche leadership, green feedstocks

|

Guanidines, bio-flocculants

|

Premium, compliance-ready output

|

|

Brazil

|

PRESIQ incentives

|

Bio-feedstocks, biopesticides

|

R&D-led expansion

|

Specialty Chemicals Market Report Scope

Specialty Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$649 Billion

|

|

Market Size (2034)

|

$1078 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Specialty Chemical Type (Agrochemicals, Electronic Chemicals, Pharmaceutical Fine Chemicals, Specialty Polymers, Construction Chemicals, Water Treatment Chemicals, Food & Feed Additives, Personal Care & Cosmetic Chemicals, CASE Chemicals), By End-Use Industry (Pharmaceutical & Healthcare, Electronics & Semiconductors, Agriculture, Automotive & Transportation, Building & Construction, Consumer Goods, Oil & Gas & Energy Storage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Evonik Industries AG, DuPont de Nemours Inc., Solvay S.A., Eastman Chemical Company, Clariant AG, Lanxess AG, Mitsubishi Chemical Group, Arkema S.A., Nouryon, Albemarle Corporation, Huntsman Corporation, Wacker Chemie AG, SABIC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Chemicals Market Segmentation

By Specialty Chemical Type

- Agrochemicals

- Electronic Chemicals

- Pharmaceutical Fine Chemicals

- Specialty Polymers

- Construction Chemicals

- Water Treatment Chemicals

- Food & Feed Additives

- Personal Care & Cosmetic Chemicals

- CASE Chemicals

By End-Use Industry

- Pharmaceutical & Healthcare

- Electronics & Semiconductors

- Agriculture

- Automotive & Transportation

- Building & Construction

- Consumer Goods

- Oil & Gas & Energy Storage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Chemicals Industry

- BASF SE

- Dow Inc.

- Evonik Industries AG

- DuPont de Nemours Inc.

- Solvay S.A.

- Eastman Chemical Company

- Clariant AG

- Lanxess AG

- Mitsubishi Chemical Group

- Arkema S.A.

- Nouryon

- Albemarle Corporation

- Huntsman Corporation

- Wacker Chemie AG

- SABIC

*- List not Exhaustive