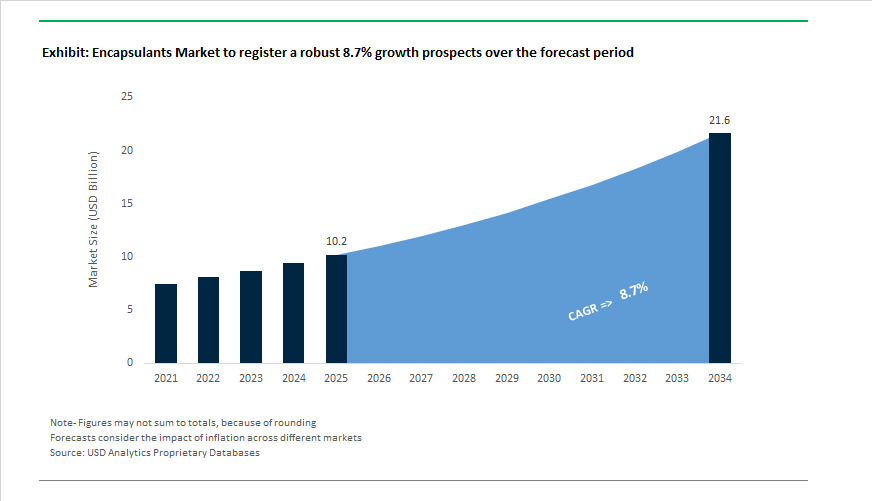

Encapsulants Market to Reach $21.6 Billion by 2034 at 8.7% CAGR Driven by High-Efficiency Solar Modules and Advanced Electronics Packaging

The Encapsulants Market is projected to expand from $10.2 billion in 2025 to $21.6 billion by 2034, registering a robust CAGR of 8.7%. Growth is being propelled by accelerated deployment of high-efficiency photovoltaic (PV) technologies, electrification of mobility, and miniaturization in semiconductor packaging. In February 2024, the Fraunhofer Institute for Solar Energy Systems (ISE) introduced its TEC (Through-passivated Edge Contact) module architecture, which requires advanced edge-sealing and next-generation encapsulation systems to preserve passivation efficiency. This innovation intensified demand for higher-performance encapsulant films capable of resisting moisture ingress and maintaining optical clarity under prolonged UV exposure.

Solar manufacturers have significantly expanded production capacity to meet global decarbonization targets. In May 2025, RenewSys India added eight new encapsulant manufacturing lines at its Khopoli facility, increasing total capacity to 30 GW across 19 lines. The expansion focuses on anti-acid encapsulants and POE films tailored for bifacial and TOPCon modules. Earlier, in December 2024, Cybrid Technologies launched RayBo, a specialized encapsulant for TOPCon cells that converts harmful UV radiation into beneficial blue light while maintaining over 99% initial power after intensive durability testing. Huasun’s December 2024 840 MWp HJT module supply agreement with PowerChina further amplified demand for POE and EPE encapsulation films, as heterojunction cells require superior moisture barriers compared to conventional EVA-based systems. Strengthening supply chain stability, RenewSys signed a 400 MW encapsulant supply agreement with ZNShine Solarworld in December 2025, covering deliveries through early 2026 amid tightening global procurement cycles.

Electronics and power applications are expanding the encapsulant market beyond photovoltaics. In 2025, Bosch integrated AI-driven vision systems into semiconductor packaging lines to detect micro-defects in encapsulated MEMS sensors and power electronics, significantly reducing failure rates in automotive systems. Concurrently, LG Electronics transitioned to silicone-based encapsulation materials for next-generation EV inverter modules, prioritizing thermal stability and vibration resistance over conventional epoxy resins. Dow reinforced its solar and building-integrated photovoltaic ecosystem by expanding its DOWSIL™ PV portfolio through 2024 and 2025, introducing six new silicone-based sealants for long-term moisture protection and structural bonding. Siemens Energy introduced encapsulated smart transformers in 2024, utilizing epoxy and polyurethane systems to enhance durability in decentralized renewable grids exposed to extreme heat and humidity.

Emerging curing technologies and pharmaceutical carve-outs are reshaping niche segments. The adoption of UV-LED curable encapsulants accelerated during 2025–2026, enabling ultra-fast curing cycles suitable for wearables and medical electronics that cannot tolerate heat-based processing. These materials reduce manufacturing energy intensity while supporting miniaturization trends in IoT devices. In parallel, Lonza completed the carve-out of its Capsules & Health Ingredients (CHI) segment in April 2025, enabling the standalone business to continue innovation in pharmaceutical-grade capsule encapsulation while Lonza refocused capital on its CDMO platform. Collectively, advances in POE film engineering, AI-enabled defect detection, UV-LED curing chemistry, and silicone-based high-temperature encapsulation are positioning the market to serve high-reliability solar modules, EV power electronics, smart grids, and precision medical packaging over the next decade.

Transformative Trends and High-Growth Opportunities Reshaping the Encapsulants Market

Advanced Semiconductor Packaging and Heterogeneous Integration Accelerating Demand for High-Reliability Underfill Encapsulants

The rapid proliferation of Artificial Intelligence and High-Performance Computing workloads has shifted semiconductor innovation from traditional transistor scaling toward heterogeneous integration and advanced packaging architectures. As chipmakers adopt 2.5D and 3D integration platforms with thousands of fine-pitch interconnects, the demand for high-performance underfill encapsulants capable of protecting dense, thermally stressed interconnects has intensified. In January 2026, TSMC announced plans to nearly double its CoWoS advanced packaging capacity to 115,000 wafers per month by the end of 2026, up from 70,000 in 2025. This scaling directly propels consumption of capillary underfill materials engineered for large-format AI dies and chiplet-based architectures.

Capital expenditure trends reinforce this structural shift. Amkor Technology reported $904.6 million in 2025 capital expenditures, primarily targeting advanced packaging equipment and the construction of its new Arizona facility to regionalize high-performance encapsulation services. In parallel, Henkel commercialized Loctite Eccobond UF 9000AE in April 2024, a capillary underfill designed for AI and HPC dies exceeding 40 mm by 40 mm, offering 20% faster flow to encapsulate more than 2,000 interconnects in heterogeneous integration systems. These investments and material innovations position advanced semiconductor encapsulants as a core growth pillar within the global encapsulants market.

Solar Manufacturing Expansion and POE Film Adoption Driving High-Efficiency Encapsulant Demand

Global energy security initiatives and next-generation photovoltaic technologies are revitalizing the solar encapsulants segment, moving beyond traditional EVA toward higher-performance Polyolefin Elastomer films. In February 2026, First Solar reported 2025 net sales of $5.22 billion, reflecting an 18% year-over-year increase, while commissioning a 3.5 GW Louisiana facility scheduled for late 2026 that will integrate advanced encapsulants into its CuRe module platform. This U.S. manufacturing expansion aligns with domestic content policies and strengthens regional demand for high-efficiency encapsulant films.

India’s Production Linked Incentive Scheme further accelerated global solar capacity, with module manufacturing reaching 144 GW per annum by the end of 2025, a 99% increase over 2024. This surge is driving localized demand for POE encapsulants favored in n-type and bifacial modules due to superior moisture barrier properties and mitigation of Potential-Induced Degradation. Industry insights from K 2025 indicate that POE films have captured a significant share in high-efficiency utility-scale projects, positioning advanced solar encapsulant materials as a strategic growth vector within the global encapsulants market.

Ultra-Low Stress and High Thermal Conductivity Materials Unlocking 3D-IC and Chiplet Opportunities

As semiconductor architectures evolve toward vertical stacking and chiplet integration, thermal density and mechanical stress management have emerged as critical performance constraints. Academic research highlighted in Nature Communications during 2025 demonstrated that Cu-Cu hybrid bonding requires encapsulants with near-zero warpage to prevent TSV strain, accelerating the development of liquid compression molding materials capable of operating at lower temperatures and reducing the thermal budget for sensitive 3D-IC stacks. These ultra-low stress encapsulants are increasingly essential for AI ASICs and high-power computing platforms.

Material innovation is translating into measurable productivity gains. Henkel introduced low-energy epoxy resins in late 2024 that achieved a 10 to 12% reduction in MEMS encapsulation production costs, creating growth momentum in wearable electronics and medical devices requiring ultra-thin protective layers. Meanwhile, King Yuan Electronics announced record 2026 capital expenditures of NT$39.37 billion to expand testing and burn-in capacity, including specialized chambers to evaluate high-thermal-conductivity encapsulants used in chiplet-based AI systems. These developments underscore the expanding opportunity for thermally conductive, low-stress encapsulation solutions in next-generation semiconductor packaging.

Sustainable and Recyclable Encapsulants Enabling Circular Photovoltaic Module Design

With large volumes of solar panels approaching end-of-life, sustainability mandates are reshaping encapsulant material design toward recyclability and circularity. In May 2025, SOLAR MATERIALS commissioned Germany’s first industrial-scale photovoltaic recycling plant with a capacity of 10,000 tons per year, equivalent to approximately 500,000 panels. The facility focuses on recovering high-purity silver and silicon, a process significantly facilitated by easy-delamination encapsulant films that enable efficient material separation.

Innovation in perovskite photovoltaics is further accelerating sustainable encapsulant development. Researchers at Linköping University published findings in February 2025 demonstrating repeated recycling of perovskite solar cells using water as a solvent, enabled by water-soluble or environmentally benign encapsulants that replace toxic solvents such as dimethylformamide. Policy frameworks such as the Ecodesign for Sustainable Products Regulation, combined with projections of 60 GW of European module production capacity by 2028, are expected to mandate higher recyclability standards, favoring mono-material polyolefin encapsulant solutions over complex multi-layer laminates. These circular design imperatives position sustainable encapsulants as a high-growth opportunity within the global encapsulants market.

Encapsulants Market Share and Segmentation Insights

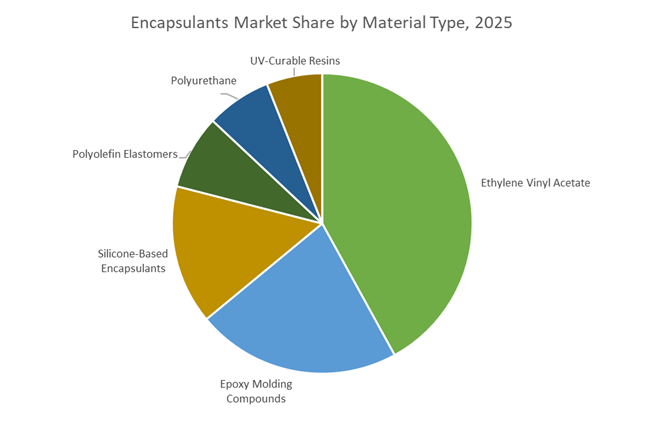

Ethylene Vinyl Acetate Leads Material Adoption Across Solar and Electronics Encapsulation

Ethylene Vinyl Acetate (EVA) accounts for 42% of global encapsulants market share in 2025, driven primarily by its dominant use in solar photovoltaic modules. EVA’s optical transparency, strong adhesion to glass and backsheets, low-temperature lamination, and cost efficiency make it the industry standard for protecting solar cells while maximizing light transmission. Epoxy molding compounds represent a significant secondary segment, serving as the backbone of semiconductor packaging by safeguarding integrated circuits from moisture ingress, thermal stress, and mechanical damage. Silicone-based encapsulants maintain an important position in automotive electronics, LEDs, and aerospace due to superior temperature resistance and flexibility. Polyolefin elastomers are gaining momentum as next-generation PV encapsulants, offering enhanced electrical insulation and recyclability. Polyurethane remains niche for industrial potting, while UV-curable resins are emerging in consumer electronics and display manufacturing, enabling faster production cycles and precision encapsulation.

Solar Photovoltaics Drives Nearly Half of Global Encapsulant Consumption

Solar photovoltaics represent 48% of total encapsulant demand in 2025, supported by accelerating renewable energy installations and declining solar module costs worldwide. EVA sheets dominate this segment, providing long-term environmental protection for solar cells against moisture, UV exposure, and thermal cycling. Semiconductor packaging forms the second-largest application, fueled by expanding production of AI processors, memory devices, and advanced logic chips requiring high-reliability encapsulation. Automotive electronics is a fast-growing segment, driven by vehicle electrification and ADAS deployment, with encapsulants protecting power modules, sensors, and control units in harsh operating environments. Consumer electronics maintain steady demand across displays, wearables, and portable devices, while industrial and power applications utilize encapsulants in inverters, wind turbines, and control systems where durability and electrical insulation are critical for long service life.

Competitive Landscape of the Encapsulants Market

The global encapsulants market in 2026 is shaped by material science leaders and solar-film specialists competing across electronic encapsulants, photovoltaic (PV) encapsulation films, thermal interface materials, and advanced semiconductor packaging, with innovation focused on AI electronics, EV power modules, N-type solar cells, and circular resin platforms.

Dow Inc. accelerates solar POE and electronic encapsulants through circular material science

Dow holds a top-tier position across silicone electronic encapsulants and polyolefin (POE) solar films, anchored by its DOWSIL™ and ENGAGE™ portfolios. The 2025 launch of DOWSIL™ TC-6015, a high-thermal-conductivity encapsulant, directly targets heat management in AI-server power modules and EV inverters. Through its Sadara JV, Dow secures low-cost ethylene feedstocks, reinforcing leadership in POE encapsulants as N-type solar cells dominate 2026 installations. Its “Material Circularity” strategy scales Renuva technology to integrate bio-attributed and recycled inputs into encapsulant resins. Massive backward integration, from cracker to finished film, enables Dow to control resin purity while delivering consistent performance for electronics, EV, and photovoltaic encapsulation applications.

Henkel AG delivers system-level electronic encapsulation for advanced semiconductor packaging

Henkel is the global benchmark for electronic-grade underfills and capillary encapsulants, projecting over USD 2 billion in 2026 revenue from its Electronics & Industrial segment. Its solutions are critical for flip-chip underfills, WLCSP, and BGA packaging, supporting 3nm and emerging 2nm chipsets. In late 2025, Henkel opened a Global Technology Center in Shanghai to serve APAC semiconductor fabs and EV battery manufacturers. Strategic asset acquisitions strengthened its thermal interface material portfolio, enabling “Total Thermal Management” alongside encapsulation. Henkel differentiates through System-in-Package co-engineering, where encapsulants are optimized with conductive adhesives to eliminate delamination under thermal stress, positioning the company as a preferred partner for mobile electronics and automotive sensor reliability.

Hangzhou First commands global solar encapsulation with POE leadership

Hangzhou First is the world’s largest solar encapsulation film producer, controlling 50%+ of the global PV encapsulants market. For 2026, the company targets 2.5 billion square meters of annual capacity, aligned with the global 500GW+ solar installation rate. Its EPE co-extruded films blend EVA affordability with POE moisture resistance, while 2026 production lines increasingly prioritize pure POE films, essential for preventing PID in TOPCon and HJT N-type modules. Expansion into Vietnam and Thailand mitigates trade tariffs and strengthens Western supply access. Hangzhou First’s scale, cost efficiency, and N-type specialization position it as the primary encapsulation partner for utility-scale solar developers and module manufacturers worldwide.

Mitsui Chemicals advances premium EVA and optical encapsulants for next-generation applications

Mitsui Chemicals operates in the high-value segment of the encapsulants market, serving automotive glazing, optoelectronics, and premium solar. Its TAFMER™ and SOLAR EVAS™ elastomers are recognized for ultra-high clarity and adhesion in harsh outdoor environments. A bio-based EVA encapsulant introduced in 2025 supports eco-luxury automotive glass and transparent BIPV systems. In early 2026, Mitsui expanded its Singapore facility to increase output of high-performance polyolefin elastomers for advanced PV modules. Beyond solar, Mitsui supplies high-purity liquid encapsulants for LEDs and optical sensors, engineered to resist yellowing over 50,000+ operating hours, reinforcing its niche leadership in durable, precision encapsulation materials.

H.B. Fuller builds Western solar and aerospace encapsulation scale with specialty adhesives

H.B. Fuller has emerged as a major Western encapsulants supplier following its STR solar acquisition, emphasizing resilient “Made in USA” supply chains. Under Project Quantum Leap (2025 to 2026), the company targets 20%+ EBITDA margins, with Engineering Adhesives, including encapsulants, as the primary growth driver toward USD 630 to 660 million adjusted EBITDA in 2026. Innovation includes a thermoplastic encapsulant for thin-film solar modules that cuts lamination cycle times by approximately 20%. H.B. Fuller also dominates North American aerospace and defense electronics encapsulation, where MIL-SPEC performance and long-term hermetic sealing are mandatory, positioning the company as a critical supplier for high-reliability electronics.

Japan: Advanced Packaging Leadership Anchored in AI and Power Electronics

Japan continues to consolidate its global leadership in high-reliability encapsulants through coordinated investments across semiconductors, AI infrastructure, and power electronics. In September 2025, Panasonic Industry announced a multi-year plan to double production capacity for high-performance circuit board materials that are fully compatible with next-generation encapsulants. This expansion is directly linked to surging demand from AI servers, cloud data centers, and advanced ICT infrastructure, where thermal stability and long-term reliability of encapsulated components are critical procurement criteria through 2028.

Material innovation is accelerating in parallel. Kyocera Corporation is preparing to commence operations at its new Nagasaki semiconductor materials plant by 2026, designed to scale ceramic packages and epoxy molding compounds for advanced chip packaging. At the same time, Sumitomo Bakelite reported a sharp rise in demand for high-thermal-conductivity encapsulants used in GPU boards for AI workloads. Its strategy emphasizes integrated thermal management solutions, including high-heat-resistant encapsulants tailored for power devices. Japan’s R&D edge was further reinforced in December 2025 when Shin-Etsu Chemical, working with IMEC, achieved a world-record breakdown voltage on 300mm GaN substrates, creating new requirements for high-voltage-stable encapsulants in next-generation power electronics. Strengthening ecosystem collaboration, 3M joined the JOINT3 consortium in September 2025 to co-develop advanced packaging and encapsulation materials for chiplet and fan-out architectures.

United States: Performance Encapsulants for EVs, Aerospace, and Data Centers

The United States encapsulants market is being reshaped by rapid electrification, domestic semiconductor expansion, and AI-driven material innovation. In 2025, Dow received major industry recognition for its DOWSIL™ TC-6015 thermally conductive encapsulant, engineered for EV power inverters. The product delivers meaningful reductions in operating temperature and module weight, aligning with U.S. OEM priorities around efficiency, range, and compact design. Dow also expanded its DOWSIL™ CC-8000 conformal coating series in mid-2025, introducing UV and dual-moisture curing systems that accelerate production cycles for complex PCB geometries used in aerospace and 5G infrastructure.

Supply chain resilience and digital acceleration are emerging as parallel themes. In November 2025, Solvay signed a definitive agreement with Noveon Magnetics to supply rare earth oxides starting in 2026. While focused on magnets, this integration indirectly influences encapsulant demand by localizing high-performance assemblies that require stable thermal and chemical protection. Complementing physical supply chains, 3M launched its Ask 3M AI assistant and Digital Materials Hub in December 2025, aimed at accelerating custom encapsulant formulation for EV, data center, and power electronics customers through 2026.

India: Localization Momentum Across Electronics, Automotive, and Solar

India’s encapsulants market is transitioning from import dependence toward localized production, supported by electronics manufacturing, renewable energy expansion, and multinational capacity investments. In 2025, Henkel inaugurated its largest Indian manufacturing facility in Pune, positioning the site as a regional hub for encapsulants and potting compounds serving automotive electronics and industrial applications. This investment reflects growing confidence in India’s role as a long-term electronics manufacturing base rather than a purely downstream market.

Ecosystem development is accelerating. Sumitomo Bakelite began active market development in late 2025, supporting evaluation phases at domestic semiconductor initiatives in Maharashtra and Bangalore ahead of a 2026 production ramp-up. On the renewable side, the Ministry of New and Renewable Energy reported cumulative solar capacity exceeding 107 GW by March 2025. This scale has directly driven demand for PID-resistant EVA and POE encapsulant films across rooftop and utility-scale projects, making solar encapsulation one of the fastest-growing application segments in India.

Germany (European Union): Aerospace Qualification and Sustainable Reformulation

Germany’s encapsulants market is shaped by stringent qualification standards and sustainability-driven reformulation. Henkel is investing €20 million through 2025 to modernize its Bopfingen facility, with a focus on advanced polyurethane and hotmelt encapsulant systems that incorporate sustainable raw materials. These upgrades are aligned with 2026 EU packaging, automotive, and wood industry requirements, where lifecycle transparency and emissions reduction are becoming procurement prerequisites.

Aerospace-grade validation further underscores Germany’s position in high-reliability materials. In April 2025, Panasonic Industry achieved European Space Agency qualification for its MEGTRON7 PCB materials. This milestone highlights the extreme performance thresholds required for encapsulant-compatible substrates in space and defense applications, reinforcing Germany’s role as a reference market for long-life, mission-critical encapsulation technologies.

China: Solar Scale-Up and Semiconductor Localization

China remains a volume and scale driver in the global encapsulants market, particularly in solar and semiconductors. In May 2025, Alishan Green Energy announced plans to expand solar encapsulant capacity from 4.2 GW to 15 GW by 2026, directly supporting the rollout of high-power-density TOPCon and HJT modules. This expansion reflects continued policy support for solar manufacturing scale and efficiency improvements.

On the semiconductor side, the Ministry of Industry and Information Technology issued a joint industrial work plan in late 2025 targeting more than 5% annual growth in chemical value-added through 2026. High-end semiconductor molding compounds and encapsulants are explicitly included, with incentives aimed at reducing reliance on imported specialty grades and strengthening domestic supply chains for advanced packaging.

Thailand: Emerging Manufacturing Base for AI Server Materials

Thailand is positioning itself as a strategic manufacturing node for global AI infrastructure. In September 2025, Panasonic Industry committed 17 billion yen to construct a new facility at its Ayutthaya plant, scheduled to begin operations in November 2027. The site will focus on low-transmission-loss circuit board materials designed for AI servers, directly influencing regional demand for compatible high-performance encapsulants as global data center capacity scales.

Encapsulants Market: Country-Level Strategic Snapshot

Encapsulants Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Key Strategic Developments

|

Structural Implication

|

|

Japan

|

AI servers and power electronics

|

Capacity doubling, GaN breakthroughs, packaging consortia

|

Global benchmark for high-reliability encapsulants

|

|

United States

|

EVs, aerospace, data centers

|

Award-winning silicones, AI-driven formulation

|

Performance-led, innovation-intensive market

|

|

India

|

Electronics localization, solar

|

New manufacturing hubs, solar capacity surge

|

Rapid shift from import to domestic supply

|

|

Germany

|

Aerospace and sustainability

|

ESA qualification, plant modernization

|

Reference market for ultra-reliable systems

|

|

China

|

Solar and semiconductor scale

|

GW-level encapsulant expansion, MIIT incentives

|

High-volume, localized specialty production

|

|

Thailand

|

AI server infrastructure

|

New materials manufacturing investment

|

Emerging export-oriented encapsulation hub

|

Encapsulants Market Report Scope

Encapsulants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.2 Billion

|

|

Market Size (2034)

|

$21.6 Billion

|

|

Market Growth Rate

|

8.7%

|

|

Segments

|

By Material Type (Ethylene Vinyl Acetate, Polyolefin Elastomers, Epoxy Molding Compounds, Silicone-Based Encapsulants, Polyurethane, UV-Curable Resins), By Technology (Liquid Encapsulation, Film-Based Encapsulation, Compression Molding, Transfer Molding, Underfill), By Application (Solar Photovoltaics, Semiconductor Packaging, Automotive Electronics, Consumer Electronics, Industrial and Power Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Dow Inc., Panasonic Industry Co., Ltd., Sumitomo Bakelite Co., Ltd., Shin-Etsu Chemical Co., Ltd., 3M Company, Kyocera Corporation, Huntsman Corporation, H.B. Fuller Company, Sika AG, Nagase & Co., Ltd., Nitto Denko Corporation, Resonac Corporation, Hangzhou First Applied Material Co., Ltd., Solvay S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Encapsulants Market Segmentation

By Material Type

- Ethylene Vinyl Acetate

- Polyolefin Elastomers

- Epoxy Molding Compounds

- Silicone-Based Encapsulants

- Polyurethane

- UV-Curable Resins

By Technology

- Liquid Encapsulation

- Film-Based Encapsulation

- Compression Molding

- Transfer Molding

- Underfill

By Application

- Solar Photovoltaics

- Semiconductor Packaging

- Automotive Electronics

- Consumer Electronics

- Industrial and Power Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Encapsulants Industry

- Henkel AG & Co. KGaA

- Dow Inc.

- Panasonic Industry Co., Ltd.

- Sumitomo Bakelite Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- 3M Company

- Kyocera Corporation

- Huntsman Corporation

- H.B. Fuller Company

- Sika AG

- Nagase & Co., Ltd.

- Nitto Denko Corporation

- Resonac Corporation

- Hangzhou First Applied Material Co., Ltd.

- Solvay S.A.

*- List not Exhaustive