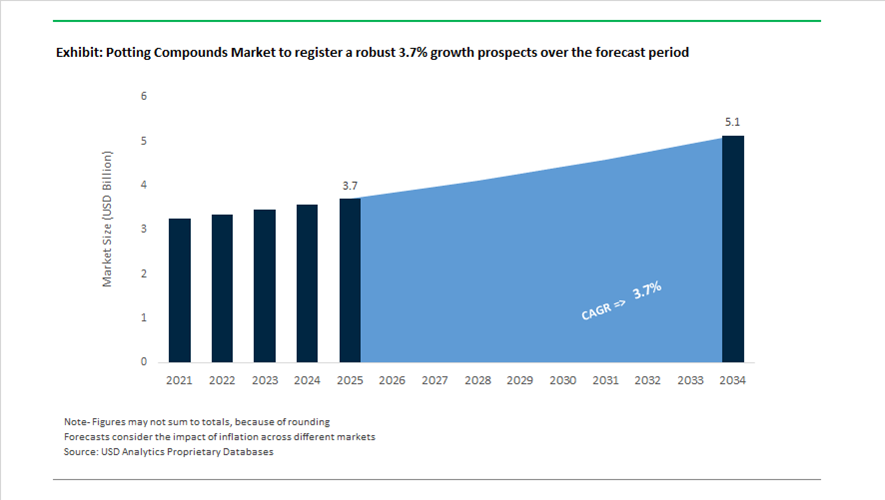

Potting Compounds Market Valued at $3.7 Billion in 2025, Forecast to Reach $5.1 Billion by 2034 at 3.7% CAGR

The global potting compounds market is valued at $3.7 billion in 2025 and is projected to reach $5.1 billion by 2034, expanding at a CAGR of 3.7%. Demand is being driven by rapid electrification, expansion of EV power electronics, growth in renewable energy infrastructure, and increasing miniaturization of industrial and medical electronic assemblies. The market spans polyurethane potting compounds, silicone encapsulants, epoxy resins, thermally conductive gels, dual-cure systems, UV-curable materials, and bio-based electronic encapsulants. Performance requirements are intensifying, particularly in high-voltage insulation, thermal conductivity, partial discharge resistance, low ionic contamination, and regulatory-compliant photoinitiator systems.

Product innovation accelerated in 2024 with automotive and electronics-specific formulations. In May 2024, Henkel introduced Loctite SI 5035, a dual-cure silicone combining UV and moisture curing for complete polymerization in shadowed areas, alongside Loctite AA 5832 polyacrylate designed for electronic assembly. These dual-cure technologies address automated manufacturing challenges in automotive control units and sensor modules. In 2025, regulatory alignment became a focal point. In May 2025, Dymax launched TPO-free light-curable materials in response to European regulatory scrutiny on Trimethylbenzoyl phosphine oxide photoinitiators, ensuring compliance in industrial potting and bonding operations. In late 2025, Dymax expanded into digital health applications with its 2000-MW series for medical wearables, eliminating isobornyl acrylate to mitigate skin irritation risks in continuous-contact devices.

Electrification and EV powertrain developments dominated 2025 launches. In September 2025, Dow introduced DOWSIL™ EG-4175 Silicone Gel engineered for high-voltage EV modules, particularly silicon carbide and gallium nitride semiconductors, delivering insulation stability and stress relief under elevated temperatures. In November 2025, Henkel launched Loctite SI 5643 and SI 5637 thermally conductive silicone potting compounds for EV inverters and on-board chargers, optimized for automated dispensing through low viscosity and fast curing characteristics. In November 2025, WEVO-CHEMIE developed EN 45545-2 rail-approved transformer potting materials emphasizing partial discharge resistance and high thermal conductivity for rolling stock electrification projects. In October 2025, Dymax released its 9773 Ruggedized Adhesive meeting NASA ASTM E595 low outgassing standards, targeting aerospace and satellite electronics where vacuum stability and minimal volatile emissions are mandatory.

Sustainability and advanced material integration are influencing competitive positioning into 2026. In June 2025, H.B. Fuller highlighted progress toward bio-based content integration within its Swift®melt and electronic-grade adhesive portfolio, alongside eco-efficiency upgrades at German and UAE manufacturing sites featuring closed-loop raw material drum recycling systems. In January 2026, Henkel expanded its electronics protection range with Loctite STYCAST US 8000 A/B, a two-component polyurethane potting compound with ultra-low ionic content below 20 ppm to prevent corrosion and silver migration in high-humidity industrial power environments. In early 2026, Dow partnered with Vestas to develop graphene-infused potting compounds designed to reduce junction temperatures in offshore wind converters by up to 40%, enhancing energy conversion efficiency and extending equipment lifespan.

The potting compounds market is increasingly defined by thermally conductive silicone encapsulants for EVs, ultra-low ionic polyurethane systems for power electronics, TPO-free UV-curable potting materials, biocompatible wearable encapsulants, rail-certified transformer compounds, NASA-qualified aerospace adhesives, graphene-enhanced renewable energy potting solutions, and bio-based sustainable formulations. Electrification trends, regulatory reformulation requirements, and renewable energy investments continue to reshape application demand across automotive, aerospace, medical, rail, and wind power electronics sectors.

Trends and Opportunities in the Potting Compounds Market

Engineering for Extreme Environments in EV and Renewable Infrastructure

The potting compounds market is undergoing a structural upgrade as electric vehicles and renewable energy systems push electronic assemblies into harsher electrical, thermal, and mechanical environments. The transition toward 800V EV architectures, higher power densities, and compact integration of motor, inverter, and on-board charger assemblies is redefining material performance expectations. Potting compounds are no longer treated as secondary protective materials; they are now engineered as multifunctional system enablers that combine high dielectric insulation, thermal conductivity, vibration damping, and long-term chemical resistance within a single formulation.

This shift is clearly visible in recent product launches. In November 2025, Henkel expanded its EV-focused portfolio with the introduction of Loctite SI 5643 and SI 5637. These low-viscosity silicone potting compounds are optimized for power electronics, where they support efficient heat dissipation from inverters and DC-DC converters while maintaining electrical isolation under sustained voltages and temperatures exceeding 150°C. Their fast-curing profiles also address the need for high-throughput manufacturing in EV assembly lines.

At a broader industry level, publicly released 2024–2025 technical data from Dow and Henkel highlights a decisive move toward UV-moisture dual-cure mechanisms. These systems eliminate the need for prolonged oven curing, reducing energy consumption and enabling void-free encapsulation of densely packed ECU connectors and ADAS modules. As EV and renewable OEMs increasingly evaluate suppliers on both performance and carbon footprint metrics, such process efficiency gains are becoming as strategically important as dielectric strength or thermal conductivity.

Automation-Ready Formulations for High-Mix, High-Volume Manufacturing

The proliferation of IIoT devices, smart infrastructure, and decentralized sensor networks is forcing manufacturers to rethink how potting compounds are applied at scale. Manual or semi-manual batch potting is rapidly being replaced by automated, precision dispensing systems designed for high-mix production environments. As a result, formulators are prioritizing compounds with tightly controlled rheology, predictable flow behavior, and consistent cure profiles to minimize waste and reduce total applied cost.

By mid-2025, leading electronics manufacturers had begun integrating digital twin technologies into their potting workflows. Real-time monitoring of viscosity, dispense pressure, and flow rates allows manufacturers to proactively adjust process parameters, cutting unplanned downtime by roughly 20% and virtually eliminating scrap caused by air entrapment or incomplete encapsulation in complex, multi-layer circuit boards. These gains are particularly critical in sectors such as industrial automation and smart energy, where device complexity is rising while price pressure remains intense.

Rapid-cure innovation is further accelerating adoption. One-part, deep-light-curing potting compounds such as Loctite SI 5035 enable immediate post-cure testing after UV exposure. This capability shortens takt times, reduces factory floor footprint, and supports the mass production of connected devices at the scale required for global IoT rollouts. In this context, automation-compatible potting compounds are evolving from consumables into productivity enablers embedded directly into smart manufacturing strategies.

Biocompatible Reliability in Medical Implants and Wearables

The medical electronics segment represents one of the most attractive margin pools for potting compound suppliers, driven by stringent regulatory frameworks and the long service life expected of implantable devices. The release of ISO 10993-1:2025 in November 2025 has fundamentally reshaped qualification requirements, replacing checklist-based compliance with lifecycle-oriented risk assessment. Medical device OEMs now require comprehensive chemical characterization, toxicological data, and long-term stability evidence for materials used in implants designed to operate for more than a decade.

This regulatory shift favors suppliers capable of delivering fully documented, biocompatible potting systems. The miniaturization of active implantable medical devices is further intensifying demand for advanced epoxies and silicones with ultra-low moisture vapor transmission rates. As next-generation hearing aids, neurostimulators, and cardiac monitors integrate advanced semiconductor nodes, even microscopic moisture ingress can compromise performance. Potting compounds that provide hermetic-like protection without adding bulk are therefore becoming mission-critical components rather than optional safeguards.

Transition to Sustainable and Reversible Potting Systems

Sustainability regulation is opening a new opportunity frontier centered on repairability and circular design. The EU’s Ecodesign for Sustainable Products Regulation, effective June 2025, and the broader Right to Repair movement are forcing electronics manufacturers to reconsider permanent encapsulation strategies. Under upcoming repairability scoring frameworks, products that cannot be disassembled or serviced risk losing market access or consumer preference in Europe.

This regulatory environment is catalyzing R&D into thermally reversible, debondable, or selectively dissolvable potting compounds. Such systems allow high-value components like motors, power supplies, and control units to be repaired or recovered at end of life instead of scrapped. Early adoption is emerging in industrial electronics and premium consumer devices, where repairability directly impacts total cost of ownership and sustainability ratings.

Investment patterns underscore this transition. In April 2024, a collaborative initiative involving Dow, Henkel, and Kraton focused on reducing the carbon footprint of industrial adhesives and sealants. The initiative serves as a template for the potting compounds market’s shift toward phthalate-free chemistries, bio-based tackifiers, and circular material design. This direction aligns with the fact that more than 70% of EU electronics manufacturers are now conducting full supply-chain impact assessments to comply with evolving circular economy legislation.

Potting Compounds Market Share and Segmentation Insights

Epoxy Resin Potting Compounds Lead Electronic Protection and Power Module Encapsulation

Epoxy resins accounted for 42.80% of the Potting Compounds Market by resin type in 2025, reflecting their widespread use in electronic encapsulation and component protection applications. Epoxy based potting compounds provide strong adhesion, chemical resistance, electrical insulation, and mechanical strength required for protecting electronic assemblies in automotive electronics, industrial control systems, and power modules. Their ability to resist moisture, vibration, and thermal cycling makes epoxy systems the preferred resin chemistry for demanding electronic environments. In 2025, development of thermally conductive epoxy potting compounds has accelerated, with formulations incorporating alumina, boron nitride, and silica fillers to improve heat dissipation in power electronics used in electric vehicles, renewable energy systems, and industrial power control units.

Automotive Electronics and Electric Vehicle Systems Drive Potting Compound Demand

Automotive applications represented 38.60% of the Potting Compounds Market by end user industry in 2025, driven by the growing number of electronic control modules used in modern vehicles. Engine control units, powertrain electronics, sensors, lighting modules, and advanced driver assistance systems require potting compounds to protect sensitive components from vibration, humidity, and thermal stress. The electrification of vehicles has significantly increased the use of power electronics and battery management systems that require advanced encapsulation materials. In 2025, electric vehicle battery module potting has emerged as a key growth driver, with specialized compounds designed to provide structural support, thermal conductivity, flame resistance, and electrical insulation in high density battery pack assemblies.

Potting Compounds Market Competitive Landscape

The global potting compounds market in 2026 is evolving toward high-reliability encapsulation, driven by EV battery systems, AI data centers, and industrial electronics. Key competition centers on ultra-low ionic content, dual-cure chemistries, and thermally conductive polyurethane and silicone systems enabling void-free, high-performance protection.

Henkel Leads Ultra-Low Ionic Polyurethane Potting for High-Reliability Electronics

Henkel dominates the potting compounds industry through its advanced polyurethane encapsulation systems tailored for mobility and electronics. The launch of Loctite STYCAST US 8000 A/B in 2026 underscores its leadership in ultra-low ionic content (<20 ppm) materials, preventing silver migration in power electronics. With a high UL 746 RTI rating of 140°C, the product addresses thermal endurance requirements in EV and industrial automation systems. Henkel reported €20.5 billion in 2025 sales, with Adhesive Technologies driving growth via electronics protection solutions. Strategic acquisitions totaling €1.2 billion strengthen its encapsulation portfolio and global reach. Its room-temperature curing technologies enable energy-efficient manufacturing, positioning Henkel as a key enabler of sustainable, high-volume electronics production.

Dow Accelerates Silicone-Based Potting Innovation Through AI-Driven Restructuring

Dow is reshaping its potting compounds portfolio by prioritizing high-value silicone encapsulation for harsh-environment electronics. Under its “Transform to Outperform” strategy, the company is targeting $2 billion in EBITDA improvement through AI integration and workforce optimization. The shutdown of basic siloxane capacity in the UK reflects a pivot toward specialty DOWSIL™ potting materials with superior purity and rheological control. Despite a 7% decline in 2025 sales to $40 billion, Dow’s cost optimization initiatives are positioning it for recovery in 2026. Its silicone potting compounds are critical for LED optics, aerospace sensors, and defense-grade electronics requiring optical clarity and durability. Dow’s focus on automation and advanced material science reinforces its competitiveness in next-generation thermal management solutions.

3M Integrates AI and Digital Tools to Redefine Potting Material Selection and Scalability

3M is transforming the potting compounds landscape through its digital-first material innovation strategy. The launch of “Ask 3M” at CES 2026 enables rapid identification and deployment of advanced encapsulation materials for EVs and AI-driven electronics. The company is investing in Expanded Beam Optical (EBO) production to support hyperscale data center infrastructure, where precision potting ensures sensor reliability. Its transition to an “Agentic Enterprise” integrates robotics into manufacturing, improving consistency and reducing defects in potting applications. 3M is also focusing on recyclable and reworkable encapsulation materials to support circular electronics design. This convergence of AI, automation, and materials science positions 3M as a leader in scalable, next-generation potting solutions.

H.B. Fuller Drives Customized Potting Solutions for High-Growth Electronics and Medical Markets

H.B. Fuller differentiates itself through a highly customized approach to potting compounds, with over 50% of its portfolio tailored to specific customer requirements. The company reported strong financial performance with $170 million Q4 2025 EBITDA and a 19% margin, reflecting demand for specialty adhesives and encapsulants. Its “Project ONE” initiative is optimizing manufacturing efficiency, supported by $160 million in planned 2026 capital expenditure. H.B. Fuller’s product portfolio now addresses 92% of the total addressable market, driven by expansion into sustainable electronics and functional coatings. Its expertise in precision formulation makes it a preferred partner for medical devices and industrial sensors requiring unique encapsulation properties. This customer-centric model strengthens its position in high-margin, application-specific markets.

ELANTAS Strengthens High-Voltage Insulation Leadership Through Strategic R&D Investments

ELANTAS is a key specialist in high-voltage insulation and potting compounds, particularly for energy and e-mobility applications. Its CHF 12.5 million investment in the Breitenbach Sustainable Technology Hub highlights its commitment to advanced insulation research through 2026. Following the Von Roll acquisition, ELANTAS has consolidated its high-voltage testing capabilities, setting new benchmarks in electrical insulation performance. The company focuses on liquid insulating materials that enable compact, high-efficiency electric motors and transformers. As part of ALTANA Group, ELANTAS reinvests approximately 7% of sales into R&D, ensuring continuous innovation in polymer encapsulation technologies. Its specialization in high-voltage and energy transition applications positions it as a critical supplier in EV and renewable infrastructure markets.

Master Bond Delivers High-Thermal Conductivity and Dual-Cure Potting for Advanced Electronics

Master Bond leads in engineered-to-order potting compounds designed for extreme performance environments. Its EP54TC epoxy, launched in 2026, offers thermal conductivity above 6 W/m·K, addressing heat dissipation challenges in power electronics. The introduction of UV26DCMed highlights its advancement in dual-cure (UV + heat) systems, accelerating assembly in medical device manufacturing. Products like Supreme 10HTLV and MasterSil 800Med demonstrate its focus on structural durability and biocompatibility, supporting both industrial and healthcare applications. The company’s solutions meet stringent ISO standards, including non-cytotoxicity requirements for medical electronics. Master Bond’s niche expertise in high-performance, application-specific formulations makes it a preferred partner for mission-critical encapsulation challenges.

Germany: EV Powertrain Integration and Circular Materials Leadership

Germany’s potting compounds market in 2025 is being reshaped by electrified mobility integration, feedstock sustainability mandates, and aerospace-grade certification. In November 2025, Henkel launched Loctite SI 5643 and Loctite SI 5637 globally, thermal potting compounds engineered for x-in-1 EV powertrains that integrate inverters and on-board chargers into compact assemblies. This shift toward multifunctional modules is elevating demand for thermally conductive, vibration-resistant potting materials capable of long-term stability under high power density. Regulatory pressure is also accelerating formulation change. Following the EU’s 2025 phthalate-free mandate, German producers transitioned toward PVC-based compound systems, including ranges such as Darex COV, to remove phthalate plasticizers while preserving viscosity control and dielectric performance.

Process efficiency and circularity are advancing in parallel. New curing protocols adopted across German chemical hubs in mid-2025 reduced required curing temperatures by 15°C, delivering an estimated 20% reduction in potting-related carbon footprint. Aerospace qualification further strengthened the market’s premium segment, as German suppliers secured 2025 certification from European Union Aviation Safety Agency for low-outgassing silicone potting resins used in satellite telecommunications modules. Circular materials are entering the value chain. In September 2025, Dow and Gruppo Fiori announced a polyurethane recycling process tailored for automotive waste, targeting reintegration of post-consumer content into new industrial potting formulations. Germany’s market trajectory reflects a convergence of EV integration, certified performance, and circular chemistry.

India: Electronics Localization and Public Utility Reliability

India’s potting compounds industry is expanding rapidly on the back of electronics localization, infrastructure investment, and stricter quality benchmarks. The Electronics Component Manufacturing Scheme notified on April 8, 2025, with an outlay of ₹22,919 crore, explicitly targets domestic production of electro-mechanical components and sub-assemblies, lifting demand for localized potting solutions across PCB enclosures and lithium-ion cells. By September 30, 2025, committed investments under the scheme reached ₹1.15 lakh crore, nearly doubling initial expectations and creating sustained offtake for epoxy and silicone potting compounds tailored to India’s thermal and humidity conditions.

Public infrastructure requirements are reinforcing technical specifications. In October 2025, the Union Ministry approved seven electronics value chain projects totaling ₹5,532 crore, many centered on high-value components that require precision potting for environmental insulation. Concurrently, the Bureau of Indian Standards introduced new purity and performance benchmarks in 2025 for epoxy potting resins used in public utility transformers, targeting moisture ingress as a primary failure mode. These standards are pushing suppliers toward higher dielectric strength, lower ionic contamination, and improved adhesion to copper and aluminum substrates. India’s market profile is thus defined by scale-driven localization coupled with rising quality thresholds.

United States: Onshoring, Low-GWP Processing, and Grid Protection

The United States potting compounds market in 2025 is anchored in onshoring of electronic materials, low-GWP processing innovation, and grid resilience investments. H.B. Fuller expanded its Millennium technology line with ECO 2 Driven blowing agents, replacing high-GWP propellants in industrial adhesive and potting dispensing systems and aligning with tightening environmental expectations. Supply security is strengthening under federal industrial policy. Following milestones under the CHIPS Act, U.S. firms including 3M and DuPont expanded domestic electronic-grade production lines in late 2025, securing low-ion potting compounds for defense and medical electronics.

Materials sustainability is also advancing upstream. In October 2025, Dow achieved ISCC PLUS certification at its Freeport, Texas facility, enabling production of bio-circular MDI for sustainable polyurethane potting resins. Downstream demand is being reinforced by public funding. The U.S. Department of Energy released 2025 grants supporting high-performance potting compounds that protect grid-scale battery busbars against extreme thermal cycling. Together, these dynamics position the U.S. as a market prioritizing secure supply, low-emissions processing, and critical infrastructure protection.

China: Thermal Innovation and Manufacturing Standardization at Scale

China continues to lead in high-volume adoption of potting compounds, driven by thermal management innovation, EV electrification, and manufacturing standardization. In November 2025, Dow opened its first Cooling Science Studio in Shanghai, a dedicated R&D hub focused on advanced thermal potting and cooling solutions for data centers and high-power electronics. Market pull is especially strong in EV battery systems. China dominates the global busbar potting segment, with regional manufacturers reporting accelerating adoption of epoxy systems for EV battery busbars and sustained double-digit growth into early 2026.

OEM standardization is reinforcing demand consistency. Leading automakers such as BYD and NIO standardized two-component silicone potting for motor controllers in 2025, improving heat dissipation and durability in humid coastal environments. Regulatory alignment is sharpening manufacturing practices. The Ministry of Industry and Information Technology published a 2026 roadmap prioritizing UV-cured potting technologies to reduce VOC emissions in mass-market electronics assembly. China’s market profile is defined by scale, OEM standardization, and rapid uptake of low-VOC curing technologies.

South Korea: Semiconductor Miniaturization and High-Temperature Performance

South Korea’s potting compounds industry is tightly linked to advanced semiconductor packaging and memory innovation. In late 2025, Korean chemical leaders commercialized hyper-flexible silicone resins capable of maintaining dielectric strength above 200°C, addressing the thermal demands of next-generation high bandwidth memory modules. These materials are critical as packaging density increases and thermal margins narrow in advanced computing applications.

Government policy is reinforcing this trajectory. The national Electronics Roadmap for 2025–2030 includes targeted subsidies for domestic development of low-viscosity epoxy potting compounds that support miniaturization at the 2 nm semiconductor node. This focus is driving formulation advances in flow control, void minimization, and adhesion to ultra-fine interconnects. South Korea’s market is therefore characterized by precision performance requirements aligned with semiconductor super-cluster expansion.

Comparative Overview of Country-Level Dynamics in the Potting Compounds Industry

Potting Compounds Market County Level Snapshot

|

Country

|

Strategic Focus Areas

|

Implications for Potting Compounds

|

|

Germany

|

EV integration, phthalate-free feedstocks, circular PU

|

Premium thermal and compliant formulations

|

|

India

|

Electronics localization, utility standards

|

Scaled demand for high-reliability epoxy systems

|

|

United States

|

Onshoring, low-GWP processing, grid protection

|

Secure supply of electronic-grade and sustainable resins

|

|

China

|

Thermal R&D, EV busbars, UV curing

|

High-volume adoption with standardized specifications

|

|

South Korea

|

Semiconductor miniaturization, high-temperature silicones

|

Advanced materials for memory and logic packaging

|

Potting Compounds Market Report Scope

Potting Compounds Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.7 Billion

|

|

Market Size (2034)

|

$5.1 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Resin Type (Epoxy Resins, Polyurethane Resins, Silicone Resins, Polyester Systems, Polyamides & Polyolefins, Acrylic Resins), By Curing Technology (Thermal Curing, Room Temperature Curing, UV & Light Curing), By Function (Thermal Management, Electrical Insulation, Corrosion & Moisture Protection, Mechanical Protection), By End-User Industry (Automotive, Electronics, Aerospace & Defense, Energy & Power, Industrial Equipment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Dow Inc., 3M Company, H.B. Fuller Company, ELANTAS GmbH, Wacker Chemie AG, Momentive Performance Materials, Huntsman Corporation, Sika AG, Shin-Etsu Chemical Co. Ltd., DuPont de Nemours Inc., Master Bond Inc., MG Chemicals, Lord Corporation, Dymax Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Potting Compounds Market Segmentation

By Resin Type

- Epoxy Resins

- Polyurethane Resins

- Silicone Resins

- Polyester Systems

- Polyamides & Polyolefins

- Acrylic Resins

By Curing Technology

- Thermal Curing

- Room Temperature Curing

- UV & Light Curing

By Function

- Thermal Management

- Electrical Insulation

- Corrosion & Moisture Protection

- Mechanical Protection

By End-User Industry

- Automotive

- Electronics

- Aerospace & Defense

- Energy & Power

- Industrial Equipment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Potting Compounds Industry

- Henkel AG & Co. KGaA

- Dow Inc.

- 3M Company

- H.B. Fuller Company

- ELANTAS GmbH

- Wacker Chemie AG

- Momentive Performance Materials

- Huntsman Corporation

- Sika AG

- Shin-Etsu Chemical Co. Ltd.

- DuPont de Nemours Inc.

- Master Bond Inc.

- MG Chemicals

- Lord Corporation

- Dymax Corporation

*- List not Exhaustive