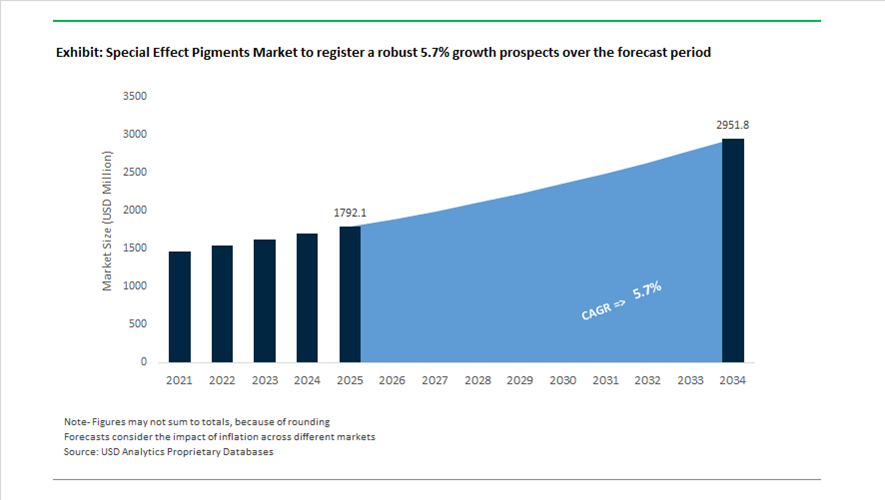

Special Effect Pigments Market Valuation 2025–2034: $1,792.1 Million to $2,951.5 Million at 5.7% CAGR Driven by Automotive Interference Effects and Sensor-Compatible Coatings

The global special effect pigments market is valued at $1,792.1 million in 2025 and is projected to reach $2,951.5 million by 2034, expanding at a CAGR of 5.7%. Growth is fueled by increasing adoption of pearlescent pigments, metallic effect pigments, interference pigments, quinacridones, aluminum flake pigments, and near-infrared (NIR) functional pigments across automotive coatings, industrial finishes, plastics, cosmetics, and smart mobility components. Automotive OEMs are prioritizing multi-angle color travel, liquid-metal aesthetics, radar transparency, and LiDAR detectability, driving demand for advanced mica-based and aluminum-based effect pigments. Simultaneously, cosmetic brands are expanding use of high-chroma shimmer pigments to enhance premium product positioning.

In January 2024, the Toyo Ink Group rebranded as artience group, signaling a strategic shift toward specialty chemicals and high-value pigment technologies. In October 2024, Sudarshan Chemical Industries announced its acquisition of Germany-based Heubach Group, creating a global pigment platform integrating Heubach’s advanced technological portfolio with Sudarshan’s cost-efficient manufacturing base. In December 2024, Runaya and ECKART formed a partnership to establish a sustainable aluminum powder facility in India, producing spherical atomized aluminum granules essential for metallic and special effect pigments. During 2024–2026, Toyo Ink India initiated construction of a Gujarat plant, scheduled for April 2026 commissioning, increasing capacity 3.5 times to support solvent-based adhesive and pigment binder demand in automotive interiors.

Technological innovation accelerated in 2025. At the European Coatings Show in March 2025, ECKART introduced radar-transparent pigment pastes such as SILVERSHINE Hydro Platinum, engineered to maintain metallic aesthetics while allowing autonomous vehicle sensors to operate through coated surfaces. In July 2025, Sun Chemical launched a new Chione Electric effect pigment tailored for cosmetics and personal care applications, delivering high-intensity shimmer and chromatic depth. BASF Coatings unveiled its 2025–2026 automotive color trends in late 2025, featuring Tesseract Blue with green-violet interference effects and Phygital Magnetar achieving liquid-metal visuals through two-coat systems. In August 2025, Merck KGaA completed the €665 million sale of its global Surface Solutions business to Global New Material International, rebranding the unit as Susonity and marking Merck’s exit from the pigments segment to focus on electronics and healthcare.

Capacity optimization and functional pigment advancements intensified in 2026. In February 2026, Sun Chemical announced a $10 million investment at its Newport, Delaware facility to expand quinacridone pigment production for premium automotive and industrial coatings. The same period saw Sun Chemical debut Spectrasense™ Black K 0089 FK at PlastIndia, designed for NIR management to enable LiDAR-detectable plastic components in smart vehicles. Earlier in 2025, ECKART introduced STANDART® Zinc Matt Black flake pigments providing corrosion protection and deep matte finishes without additional topcoats, reducing coating process steps. These developments underscore how automotive sensor integration, corrosion-resistant matte finishes, sustainable aluminum sourcing, and cosmetic-grade chromatic innovation are driving the evolution of the special effect pigments market toward $2.95 billion by 2034.

Strategic Trends and High-Value Opportunities in the Special Effect Pigments Market

OEM Vertical Integration in Automotive Aesthetic Design

Automotive OEMs are increasingly internalizing color and effect pigment development to counter the visual homogenization created by electric vehicle platform convergence. As aerodynamic constraints standardize body shapes, light interaction, depth, and chromatic movement have emerged as primary brand identifiers. This has pushed OEMs away from off-the-shelf pigment catalogs toward proprietary, co-developed effect systems that are tightly integrated with vehicle identity and lifecycle control.

A clear signal of this shift emerged in October 2025, when PPG announced a landmark collaboration with Xiaomi EV under the “100 Colors Project.” The partnership focuses on exclusive automotive finishes such as Amethyst Purple, which employs advanced interference pigments to generate deep luster and multi-angle chromatic effects tailored specifically for the YU7 model series. This approach allows OEMs to lock in visual exclusivity while controlling pigment performance across manufacturing, repair, and aftermarket touch-up cycles.

In parallel, BASF Coatings unveiled its 2025–2026 Automotive Color Trends titled DRIVING THE PROXY, highlighting the rise of “functional aesthetics.” Pigments such as TESSERACT BLUE leverage engineered interference structures that shift between violet and green depending on viewing angle. Critically, these systems are being optimized to remain compatible with LiDAR and sensor-based driver assistance technologies, ensuring that high-effect metallic finishes do not compromise autonomous or semi-autonomous vehicle safety. This convergence of design, optics, and sensor compatibility is redefining specification standards for special effect pigments in the EV era.

Regulatory Substitution Accelerating the Shift to Synthetic Micas

Global regulatory tightening around pigment safety and traceability is reshaping the competitive landscape, particularly in cosmetics and personal care. The EU Omnibus Act VII, with full implementation scheduled for September 1, 2025, and Regulation (EU) 2024/197 have reclassified several substances previously used in mineral-based effect pigments as CMR, triggering mandatory reformulation and product recalls ahead of the late-2025 deadline.

This regulatory inflection point has accelerated the transition from natural mica to Synthetic Fluorphlogopite, commonly referred to as synthetic mica. These materials offer higher purity, controlled particle morphology, and consistent sparkle without the heavy-metal contamination risks and supply chain opacity associated with natural mica mining. For brands, synthetic micas are no longer a premium option but a compliance requirement, particularly in markets subject to EU and California Proposition 65 standards.

Market structure is adjusting accordingly. In August 2025, Merck KGaA completed the €665 million divestment of its Surface Solutions pigment business to Global New Material International, which subsequently rebranded the unit as Susonity. This strategic realignment enables Merck to focus on electronics and life sciences, while GNMI scales high-purity pearlescent pigment production to meet the new global safety and regulatory benchmarks. The transaction underscores how compliance pressure is driving consolidation and specialization within the special effect pigments market.

High-Durability Architectural Pigments Aligned with AAMA 2605 Standards

The architectural coatings segment is emerging as a high-margin opportunity for special effect pigment suppliers capable of meeting AAMA 2605 specifications. This “Superior Performing” standard requires coatings to retain color and gloss integrity for a minimum of 10 years under aggressive environmental exposure, including UV radiation, humidity, and temperature cycling.

To qualify, pigments must withstand extended South Florida outdoor exposure testing, widely regarded as the industry’s most demanding weatherability benchmark. Leading manufacturers such as Sun Chemical, part of DIC Corporation, expanded Perylene pigment capacity in Ludwigshafen in late 2025 to support demand for high-performance reds and maroons used in commercial facades and landmark architectural projects.

The economic value proposition is compelling. While standard AAMA 2603 coatings typically carry one-year warranties, systems formulated with encapsulated, high-durability effect pigments can support 10- to 20-year warranty offerings. This durability premium enables coating formulators and pigment suppliers to capture significantly higher margins while aligning with infrastructure owners’ lifecycle cost reduction goals.

Embedding Security through Signature and Taggant Pigments

Escalating counterfeiting risks in pharmaceuticals and premium spirits are opening a specialized, high-value niche for security-enabled special effect pigments. As regulatory frameworks such as the U.S. Drug Supply Chain Security Act mandate end-to-end traceability, brands are seeking covert authentication features that are difficult to replicate and seamlessly integrated into packaging materials.

Signature pigments, including Optical Variable Inks and taggant-based systems with unique luminescent or magnetic responses, are increasingly being embedded directly into plastic containers, closures, and label inks. This approach transforms the pigment itself into a security feature rather than an external additive. At K 2025, Sun Chemical and DIC Corporation showcased advanced pigment platforms that combine luxury color-shift aesthetics with covert authentication signatures.

These dual-function pigments provide a strong deterrent against counterfeiting while preserving premium visual appeal. For pigment suppliers, this represents a defensible growth segment where pricing is driven by intellectual property, customization, and brand protection value rather than volume, reinforcing the strategic importance of innovation-led differentiation in the special effect pigments market.

Special Effect Pigments Market Share and Segmentation Insights

Pearlescent Pigments Lead the Special Effect Pigments Market Through Versatile Visual Effects

Pearlescent pigments accounted for 42.80% of the special effect pigments market in 2025, making them the most widely used pigment type across high-value decorative and functional applications. These pigments create distinctive soft luster, depth, and iridescent optical effects, which are widely used in automotive coatings, cosmetics, plastics, and printing inks to deliver premium visual aesthetics. Their ability to produce elegant and natural-looking finishes supports broad adoption across consumer and industrial products. A significant 2025 innovation trend is the expansion of synthetic mica-based pearlescent pigments, which offer superior brightness, purity, and color saturation compared with natural mica substrates while addressing sustainability and supply chain concerns associated with traditional mica mining.

Automotive Industry Drives Global Demand for Special Effect Pigments in Premium Coatings

Automotive represents the largest end-use segment in the special effect pigments market, accounting for 34.80% of global consumption in 2025 due to the extensive use of effect pigments in automotive coatings. Vehicle manufacturers rely on pearlescent, metallic, and color-shifting pigments to create distinctive finishes that enhance brand identity and product differentiation. These pigments contribute to high-gloss appearance, color depth, and unique visual effects that appeal to consumers seeking premium vehicle aesthetics. A key 2025 industry trend is the increasing importance of electric vehicle design differentiation, where automakers use advanced effect pigments to develop signature color palettes, subtle metallic finishes, and multi-angle color-shifting effects that emphasize innovation and premium positioning in the growing EV market.

Special Effect Pigments Market Competitive Landscape

The global special effect pigments market in 2026 is driven by radar-transparent pigments, synthetic mica innovation, and multi-layer interference coatings. Industry leaders are focusing on PFAS-free, heavy-metal-free formulations, AI-driven color matching, and high-performance pigments for automotive, cosmetics, and smart packaging applications.

Merck Advances High-Purity Effect Pigments for Smart Packaging and AI-Enabled Anti-Counterfeiting Applications

Merck KGaA is strengthening its position in special effect pigments with €21.1 billion in 2025 net sales and continued investment in high-margin Surface Solutions. Its strategic restructuring enables focus on high-purity pigments used in semiconductor devices, smart packaging, and pharmaceutical anti-counterfeiting systems. The company is integrating laser-markable pigments to enable digital traceability and unique product identification in AI-driven supply chains. Its R&D focus includes bio-compatible pearlescent pigments tailored for clean-beauty and regulated cosmetic applications. Merck’s emphasis on high-performance pigments aligns with demand for precision optical effects and functional coatings. Its integration of science-led innovation supports advanced applications in electronics and life sciences.

Sun Chemical Expands High-Chroma Automotive Pigments and Sustainable Color Selection Tools

Sun Chemical is reinforcing its leadership in high-performance pigments through strategic investment and product innovation across automotive and packaging sectors. Its $10 million expansion in Newport enhances production of Quinacridone pigments for durable, high-chroma automotive coatings. The Paliocrom® Brilliant Ruby pigment delivers exceptional flop behavior and color intensity using coated aluminum flakes. Its Glacier™ Exterior Ceramic White, based on synthetic mica, provides weather-resistant, high-purity white finishes for automotive and architectural applications. The Pigment Finder platform integrates product carbon footprint data, enabling formulators to select sustainable pigments aligned with EU regulations. Sun Chemical’s focus on high-performance colorants and digital tools strengthens its competitive edge.

ECKART Leads Radar-Transparent Pigment Innovation for Autonomous Vehicle and Industrial Coating Applications

ECKART, part of ALTANA Group, is pioneering radar-transparent effect pigments critical for Level 3 autonomous vehicle coatings. Its SILVERSHINE Hydro Platinum pigments allow sensor transparency while maintaining metallic aesthetics, addressing key automotive safety requirements. The GO:FUTURE initiative highlights its focus on sustainable and digitalized pigment production. Innovations such as STANDART® Zinc Matt Black deliver corrosion protection combined with functional aesthetics for industrial coatings. The company’s Trend Colours 2026 palette reflects demand for emotionally responsive surfaces with interference effects. Strong financial backing and increased R&D investment support its leadership in advanced pigment technologies.

Sudarshan Chemical Strengthens Integrated Color Systems and NIR-Detectable Pigments Following Heubach Acquisition

Sudarshan Chemical Industries has emerged as a global leader in integrated pigment solutions following its acquisition of Heubach. Its transition to application-ready color systems enhances value delivery across automotive, coatings, and plastics markets. The launch of Sudafast Red 313D strengthens its presence in high-performance printing inks and special effect pigments. Its NIR-detectable pigments enable automated recycling of dark and metallic plastics, supporting circular economy goals. The company’s focus on PFAS-free, lead-free, and chrome-free pigment lines aligns with global regulatory standards. Sudarshan’s expanded portfolio and innovation capabilities position it strongly in sustainable pigment technologies.

Kuncai Drives Synthetic Mica Innovation and Ethical Pigment Production for High-Performance Applications

Kuncai Pigments is redefining the special effect pigments market through vertically integrated synthetic mica production, offering superior surface uniformity and durability compared to natural mica. Its pigments enable precise color control and enhanced shatter resistance for automotive and cosmetic applications. The company is advancing TiO2-coated pigment technologies, optimizing layer thickness for high-purity gold and yellow effects. As a member of the Responsible Mica Initiative, Kuncai promotes ethical sourcing and reduced environmental impact. Its pigments demonstrate high-temperature stability, making them suitable for plastic masterbatches and industrial coatings. Kuncai’s focus on sustainability and advanced material performance strengthens its competitive positioning.

United States Special Effect Pigments Market Reconfigured by M&A and Sensor-Compatible Innovation

The United States special effect pigments market has entered a consolidation-led growth phase, anchored by asset realignment and rapid innovation tied to autonomous mobility. In late 2025, Global New Material International completed the acquisition of Merck KGaA’s Surface Solutions business, transitioning the Savannah, Georgia site to the Susonity brand. The facility is now focused on high-chroma pearlescent pigments optimized for North American automotive coatings, strengthening domestic access to premium optical effects. Parallel to consolidation, U.S. manufacturers have accelerated the commercialization of PFAS-free process aids for metallic flake dispersion in response to EPA final rules issued across 2024–2025, ensuring compliance for food-contact packaging and industrial coatings without sacrificing dispersion quality.

Technology roadmaps are increasingly defined by vehicle electronics. Supported by the CHIPS Act and expanding ADAS requirements, U.S. R&D programs are scaling infrared-reflective and radar-transparent pigments that avoid interference with sensors, a prerequisite for 2026 model-year OEM specifications. Production resilience has improved as Sun Chemical, part of DIC Group, resolved bottlenecks in Benda-Lutz COMPAL aluminum pigments using a pelletized format that removes solvent-borne transport risks. Aesthetic leadership continues with the mid-2025 launch of Lumina HD Exterior Sienna, a synthetic mica pigment engineered to deliver high-definition liquid-metal effects for premium SUV finishes.

Germany Special Effect Pigments Market Anchored by Ethical Sourcing and Waterborne Compliance

Germany remains the reference market for engineered pearlescence, combining ethical sourcing, waterborne compliance, and automotive-grade precision. Following Merck KGaA’s divestment in August 2025, the Gernsheim site commenced operations under the GNMI/Susonity banner, supported by an employment guarantee through 2032 that preserves German engineering standards in pigment synthesis. This continuity has reinforced Germany’s role in high-performance interference pigments for OEM coatings. Sustainability is now embedded in design language. BASF’s 2024–2025 Color Trends report, Routing, introduced Harbinger’s Ink, a deep-black effect pigment incorporating carbon-negative components and biodegradable flakes aligned with EU sustainability mandates.

Regulatory compliance has reshaped formulations and processes. To meet EU Industrial Emissions Directive requirements, German coaters have prioritized hydro-dispersible metallic powders such as the HYDRORENE line, delivering up to 40% VOC reduction in refinish systems. Capacity expansion for synthetic fluorophlogopite has accelerated to replace natural mica, addressing ethical sourcing expectations in cosmetics and personal care while stabilizing optical consistency. These shifts collectively position Germany as the premium, regulation-ready supplier for effect pigments across automotive, beauty, and industrial coatings.

China Special Effect Pigments Market Scaled by EV Integration and Capacity Leadership

China’s special effect pigments market is defined by industrial integration, export scale, and rapid adoption in electric mobility. In 2024–2025, BASF Coatings expanded operations at Zhanjiang, integrating ColorBrite waterborne basecoats with advanced pearlescent pigments to serve fast-growing domestic EV programs. The October 2025 partnership between BASF and Xiaomi formalized a three-year initiative to develop 100 exclusive automotive colors, leveraging dual-layer clearcoats and crystal-like pigments such as Amethyst Purple for smart mobility platforms.

Capacity leadership underpins competitiveness. With the integration of European assets, Chinese-owned entities now control more than 40% of global pearlescent pigment capacity, supported by domestic synthetic mica production that compresses global cost curves. Regulatory enforcement is tightening quality thresholds. The late-2025 implementation of GB 4806.16-2025 has mandated high-purity organic and inorganic effects for food packaging, eliminating trace heavy metals in recycled plastics and accelerating adoption of cleaner pigment chemistries across domestic and export markets.

Japan Special Effect Pigments Market Led by Precision Optics and Luxury EV Design

Japan continues to lead in precision effect pigments for electronics and premium mobility, where optical control and miniaturization are paramount. The Onahama site, now operating under the GNMI/Susonity structure, remains the global benchmark for ultra-thin glass flake pigments used in 8K displays, high-end smartphone housings, and advanced interference effects. These “color-travel” pigments are increasingly specified for emerging 6G hardware, where angle-dependent reflectance and minimal thickness are critical.

Design innovation extends into automotive luxury. In 2025, Japanese design centers introduced the Scintillation color profile, delivering a refined liquid-metal appearance through a new low-emission basecoat architecture tailored for luxury EVs. This approach balances visual depth with environmental performance, reinforcing Japan’s position at the intersection of electronics-grade precision and premium automotive aesthetics.

Comparative Snapshot: Country-Level Special Effect Pigments Dynamics

Special Effect Pigments Market County Level Snapshot

|

Country / Region

|

Primary Demand Drivers

|

Strategic Focus Areas

|

Structural Impact

|

|

United States

|

Automotive, ADAS, packaging

|

Sensor-safe pigments, PFAS-free dispersion

|

M&A-led capacity and compliance

|

|

Germany

|

Automotive OEMs, cosmetics

|

Ethical mica, waterborne metallics

|

Premium, regulation-ready supply

|

|

China

|

EVs, exports, packaging

|

Integrated basecoats, capacity scale

|

Global cost and volume leadership

|

|

Japan

|

Displays, smartphones, luxury EVs

|

Ultra-thin flakes, interference optics

|

Precision-led differentiation

|

Special Effect Pigments Market Report Scope

Special Effect Pigments Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1792.1 Million

|

|

Market Size (2034)

|

$2951.5 Million

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Pearlescent Pigments, Metallic Pigments, Luminescent Pigments, Variable & Functional Effect Pigments), By Substrate Type (Natural Mica-Based, Synthetic Mica-Based, Glass Flake-Based, Metal Flake-Based), By End-Use Industry (Automotive, Cosmetics & Personal Care, Plastics, Paints & Coatings, Printing Inks)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Global New Material International, BASF SE, DIC Corporation, Altana AG, Sudarshan Chemical Industries Ltd., Silberline Manufacturing Co., Toyo Aluminium K.K., CQV Co. Ltd., The Shepherd Color Company, Geotech International B.V., Sensient Technologies Corporation, Kobo Products Inc., Plasmonics Inc., Yantai i-Suo New Material, Kolortek Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Special Effect Pigments Market Segmentation

By Product Type

- Pearlescent Pigments

- Metallic Pigments

- Luminescent Pigments

- Variable & Functional Effect Pigments

By Substrate Type

- Natural Mica-Based

- Synthetic Mica-Based

- Glass Flake-Based

- Metal Flake-Based

By End-Use Industry

- Automotive

- Cosmetics & Personal Care

- Plastics

- Paints & Coatings

- Printing Inks

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Special Effect Pigments Industry

- Global New Material International

- BASF SE

- DIC Corporation

- Altana AG

- Sudarshan Chemical Industries Ltd.

- Silberline Manufacturing Co.

- Toyo Aluminium K.K.

- CQV Co. Ltd.

- The Shepherd Color Company

- Geotech International B.V.

- Sensient Technologies Corporation

- Kobo Products Inc.

- Plasmonics Inc.

- Yantai i-Suo New Material

- Kolortek Co. Ltd.

*- List not Exhaustive