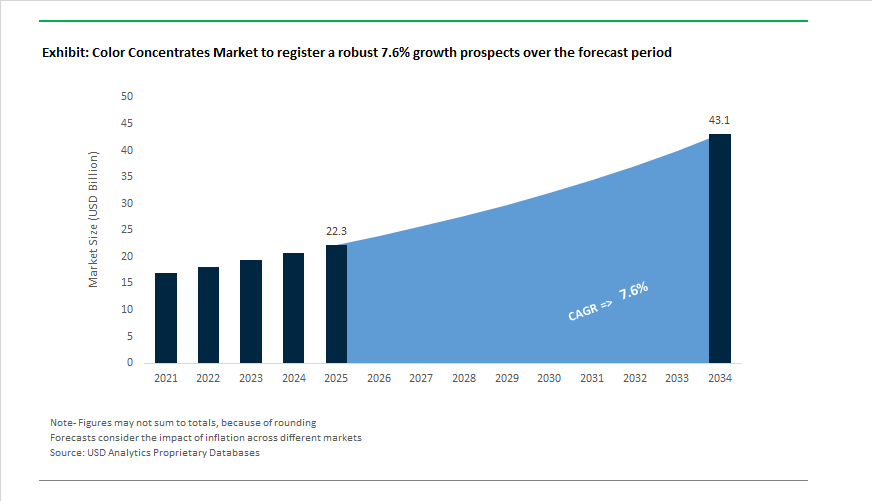

Color Concentrates Market Outlook 2025–2034: $22.3 Billion to $43.1 Billion at 7.6% CAGR Driven by Circular Masterbatches and PFAS-Free Innovation

The global Color Concentrates Market is projected to expand from $22.3 billion in 2025 to $43.1 billion by 2034, registering a CAGR of 7.6%. Growth is supported by rising demand for high-performance masterbatches, pigment concentrates, and liquid color systems across packaging, automotive, consumer electronics, medical devices, textiles, and building materials. Increasing regulatory scrutiny around PFAS, heavy metals, titanium dioxide, and carbon footprint disclosure is accelerating reformulation strategies. Manufacturers are prioritizing recyclable polypropylene, recycled nylon, sustainable PET, and circular feedstock-based masterbatches to align with 2026 sustainability mandates and global extended producer responsibility frameworks.

Industry consolidation reshaped competitive positioning in 2025. In March 2025, Sudarshan Chemical Industries Limited completed the acquisition of Germany-based Heubach Group, forming the world’s second-largest pigment producer with operations across 19 international sites. The transaction integrates Heubach’s advanced pigment technologies and legacy Clariant pigment assets into Sudarshan’s portfolio, strengthening global supply of organic and inorganic pigments for color concentrates. In parallel, ADEKA introduced ADK TRANSPAREX™ during late 2024–2025, achieving a record haze value of 2.2 in polypropylene clarifying concentrates, enabling recyclable PP to replace glass and less-recyclable clear plastics in premium packaging applications. These developments signal intensified competition in high-clarity and performance pigment concentrates for monomaterial packaging systems.

Sustainability and circular economy initiatives accelerated innovation across 2024–2026. Cabot Corporation launched REPLASBLAK® circular black masterbatches during 2024–2025, the first ISCC PLUS-certified black concentrates incorporating certified circular feedstocks through EVOLVE® Sustainable Solutions. In February 2026, Ampacet introduced Natura Jet at Plastindia 2026, replacing traditional carbon black with naturally derived carbon for deep black hues in consumer electronics and durable goods. Avient expanded its Hiformer™ Non-PFAS liquid masterbatch portfolio into Asia in January 2026, addressing global restrictions on per- and polyfluoroalkyl substances in polyolefin film processing. In February 2026, Avient launched Nymax™ REC recycled nylon concentrates targeting fire-resistant construction components. LyondellBasell confirmed in 2025–2026 that its MoReTec-2 chemical recycling facility in Houston will produce circular feedstocks capable of generating virgin-quality masterbatches from post-consumer plastic waste, strengthening long-term sustainable pigment supply.

Advanced application-driven technologies further diversified the color concentrates ecosystem. Ampacet introduced the HyperLustre TiO2-free collection in 2024–2025, delivering semi-translucent pearlescent effects in PET packaging while improving recyclability in high-speed recovery streams. Tosaf unveiled polyphthalamide-based masterbatches in May 2024 designed for high-heat engineering plastics in automotive electronics. Clariant showcased antimony-free AddWorks™ titanium catalyst solutions at K 2025 in October 2025, addressing supply risks following China’s 2024 export restrictions on antimony. Americhem launched ISO 10993-tested PFAS-free medical-grade masterbatches in February 2026, targeting robotic surgery and drug delivery systems requiring strict traceability. Sherwin-Williams introduced its AI-powered Color Expert app in May 2024, enabling digital-to-formulation translation of customized color schemes into industrial masterbatch production. These developments highlight strong mid-to-high single-digit growth potential through 2034, supported by regulatory-driven reformulation, circular raw materials integration, and high-performance specialty pigment technologies across global end-use industries.

Key Trends and Strategic Opportunities Transforming the Color Concentrates Market

Circular Economy Compliance and NIR-Sortable Black Masterbatches as a Defining Sustainability Trend

The circular economy mandate has evolved into a binding regulatory driver reshaping the global color concentrates market. The Ecodesign for Sustainable Products Regulation, enforced from July 2024, introduced a 2025 to 2027 Working Plan targeting substances of concern that inhibit recyclability, directly pressuring color concentrate manufacturers to eliminate heavy-metal pigments and conventional carbon black formulations that disrupt Near-Infrared sorting systems. According to the 2024 Sustainable Packaging Innovation assessments by the U.S. Plastics Pact, traditional carbon black can cause up to a 100% loss of plastic value during automated sorting, making NIR-sortable black masterbatches a baseline requirement for brands targeting 100% recyclable packaging and compliance with ESG and recycled content mandates.

In response to these regulatory and industrial sustainability requirements, Avient Corporation launched the OnColor REC line in August 2024, incorporating pigments derived from recycled end-of-life tires. These sustainable color concentrates meet REACH and RoHS certifications while reducing Product Carbon Footprint in injection molding and extrusion applications. The transition toward recyclable masterbatches, low-PCF pigments, and heavy-metal-free colorant systems has repositioned color concentrates from aesthetic additives to compliance-critical components in circular plastics value chains.

EV Lightweighting, Sensor-Transparent Formulations, and High-Voltage Orange Standards as a High-Growth Automotive Trend

The rapid expansion of the electric vehicle market is accelerating demand for high-performance color concentrates engineered for lightweighting, thermal resistance, and functional safety identification. In its 2024 to 2025 Automotive Color Trends report, BASF Coatings introduced the ROUTING collection emphasizing functional aesthetics, including sensor-transparent masterbatches that allow LiDAR and radar signal transmission through polymer body panels for Level 3 autonomous EVs. This integration of electromagnetic transparency with aesthetic performance reflects the growing convergence of color science and automotive electronics.

To extend battery range, OEMs are replacing metal components with high-performance plastics, driving adoption of Long Glass Fiber reinforced masterbatches. In May 2024, Tosaf launched a specialized carrier system for polyphthalamide enabling coloration of heat-resistant under-the-hood EV electronics without compromising mechanical stiffness. Simultaneously, EV safety standards mandate High-Voltage Orange RAL 2003 for cables and connectors, prompting demand for ultra-stable orange masterbatches with up to 15-year thermal color fastness. These requirements are reinforcing the automotive segment as a premium, technology-driven growth engine within the global color concentrates market.

Chemical Recycling-Compatible Colorants Unlocking Opportunities in Advanced Recycling Feedstocks

As mechanical recycling approaches technical limits, chemical recycling and depolymerization technologies are creating a high-value opportunity for monomer-compatible color concentrates. At K 2025, BASF, in collaboration with ZF Group and Mercedes-Benz, demonstrated successful depolymerization of PA6 from end-of-life vehicle oil pans into caprolactam, enabling closed-loop automotive-to-automotive recycling. This innovation highlights the need for purification-safe pigments and masterbatches that do not contaminate monomer recovery stages, ensuring recycled polyamides achieve virgin-equivalent aesthetic and performance standards.

Investment trends reinforce this opportunity. In March 2025, Altana AG announced a 30% increase in its €180 million investment budget targeting sustainability and digitalization across its chemical divisions, with R&D focused on mass-balance compatible colorants for advanced recycling feedstocks. As regulatory pressure intensifies around recycled content, Scope 3 emissions, and circular polymer ecosystems, depolymerization-friendly masterbatches are positioned as a strategic growth lever in the global color concentrates industry.

Molded-In-Color and Paint Elimination Technologies Driving High-Performance Aesthetic Opportunities

The transition toward molded-in-color solutions and paint elimination strategies represents a transformative opportunity in surface finishing economics. Nippon Paint announced next-generation In-Mold Coating technology for 2025 that integrates molding and coating processes, reducing CO2 emissions by approximately 60% compared to traditional painting booths by eliminating drying ovens and VOC emissions. This aligns with decarbonization targets and strengthens demand for high-performance color concentrates capable of delivering Class A finishes directly from the mold.

In January 2024, Ampacet introduced permanent high-contrast laser-markable masterbatch technology for dark plastic substrates, eliminating secondary labeling and printing that hinder recyclability. Further supporting the paint elimination shift, a January 2026 collaboration between PPG and 4Plastic developed repair coatings for non-painted textured plastic components. As OEMs adopt bare textured exteriors to reduce weight and cost, demand for UV-stable, scratch-resistant, weatherable molded-in-color masterbatches is projected to accelerate, positioning high-performance aesthetic concentrates as a premium growth segment within the global color concentrates market.

Color Concentrates Market Share and Segmentation Insights

Form-Based Segmentation: Solid Masterbatch Leads as Dust-Free Processing Gains Priority

Solid masterbatch dominates the color concentrates market with 72% share in 2025, driven by ease of handling, excellent pigment dispersion, and minimal dust generation in injection molding and blow molding operations. Pelletized formats support automated dosing and consistent coloration in high-volume plastics processing. Liquid color concentrates maintain a significant presence in engineering plastics, offering superior dispersion and precise metering in materials such as rigid PVC, polycarbonate, and nylon, while enabling faster color changeovers. Powdered concentrates now represent the smallest segment due to hygiene, dusting, and moisture sensitivity challenges, although they remain relevant for rotomolding and select PVC applications. Across all formats, manufacturers are accelerating the shift toward dust-free, easy-to-dose systems to improve workplace safety, streamline production, and support Industry 4.0 automation initiatives in polymer compounding and conversion facilities.

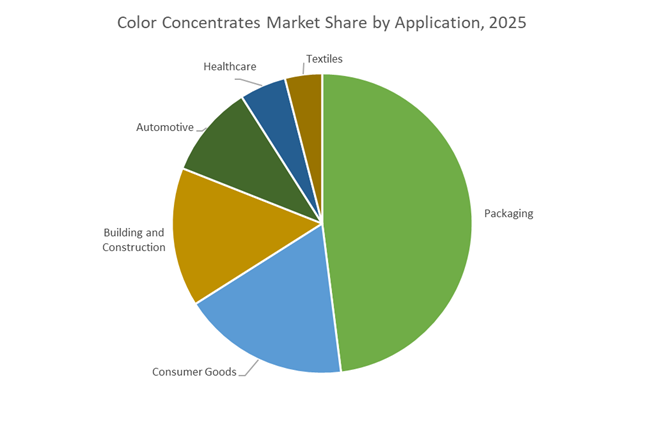

Application Landscape: Packaging Leads Consumption as Automotive and Healthcare Demand Performance Grades

Packaging accounts for 48% of total color concentrate demand, spanning rigid bottles and caps to flexible films and bags, where color supports brand differentiation, UV protection, and functional barrier properties in food and beverage packaging. Consumer goods form a major segment, requiring vibrant hues, metallic effects, and tight batch-to-batch color consistency for toys, appliances, and electronics housings. Building and construction applications utilize concentrates in PVC pipes, window profiles, decking, and roofing membranes, where coloration also contributes to UV stability and heat reflectance. Automotive applications demand high-temperature-resistant concentrates for under-hood components and weatherable grades for exterior parts, with growing preference for lighter shades to reduce cabin heat absorption. Healthcare represents a specialized segment requiring biocompatible colorants for medical devices and pharmaceutical packaging, while textiles increasingly adopt dope-dyed fibers using concentrates to eliminate water-intensive dyeing and improve sustainability.

Competitive Landscape of the Color Concentrates Market

The Color Concentrates Market is led by vertically integrated masterbatch producers and specialty compounders advancing healthcare-grade colorants, sustainable pigments, and real-time color management technologies. Competitive differentiation centers on PFAS-free lubricious systems, recyclable black masterbatches, molecular-level dispersion, and functional hybrid concentrates for packaging, automotive, medical, and agricultural films. Market leaders are scaling global manufacturing footprints, accelerating PCR-compatible color solutions, and embedding digital color matching to reduce waste. Strategic priorities increasingly focus on sustainability at scale, conductive polymers for EV platforms, and high-speed extrusion compatibility across flexible and rigid plastics.

Avient dominates healthcare and high-performance masterbatches with Concept-to-Commercialization scale

Avient Corporation strengthened its leadership following the acquisition of Clariant’s Masterbatch business, emerging as the industry’s largest color concentrates supplier. Its OnColor™ masterbatches and Mevopur™ healthcare-grade colorants are produced in ISO 13485-certified facilities, supporting regulated medical applications. In early 2026, Avient launched GlideTech™ Formulations, a non-PFAS lubricious technology that eliminates secondary catheter coatings. Strategically, Avient is driving Sustainability at Scale, promoting NEUSoft Express colors in the US with a record 14-day lead time for urgent healthcare projects. With over 50 manufacturing sites worldwide, Avient delivers end-to-end Concept to Commercialization services, including advanced computer-aided color matching.

Ampacet accelerates recyclable packaging aesthetics with bio-derived black masterbatches

Ampacet is a dominant force in global packaging, supplying color concentrates to a large share of flexible films and rigid bottles. The company leads in white and black masterbatches and additives optimized for high-speed film extrusion. At Plastindia 2026, Ampacet introduced Natura Jet, a bio-derived black masterbatch delivering piano-black aesthetics without traditional carbon black, improving recyclability. It also launched HyperLustre, a TiO2-free semi-translucent PET masterbatch creating pearlescent effects for premium beauty packaging. Ampacet is expanding its LIAD Smart in-line color management systems, enabling real-time correction on production floors and reducing material waste by up to 50%.

Cabot strengthens conductive black concentrates for EV and energy storage platforms

Cabot Corporation maintains global leadership in carbon black, offering vertically integrated control from raw feedstock to finished black masterbatch pellets. As of February 2026, Cabot reported approximately USD 3.93 billion in market capitalization with trailing twelve-month revenue of USD 3.61 billion. The company finalized acquisition of Mexico Carbon Manufacturing in early 2026, reinforcing supply of conductive and specialty black concentrates across the Americas. Cabot is the standard for automotive exteriors and conductive polymers used in EV battery housings and electronic shielding. Innovation momentum includes pending patents for carbon nanotube-polymer composites tailored for dry-processed battery electrodes, advancing next-generation energy storage materials.

LyondellBasell integrates polymer science with premium pharmaceutical color solutions

LyondellBasell’s Advanced Polymer Solutions division delivers high-performance color concentrates and compounds backed by global polyolefin leadership. The company is pursuing a Full Portfolio Approach in India and MEA, combining virgin resins with Circulen recycled and renewable color solutions. At Plastindia 2026, LYB showcased Asepthene MD 8150 IN, a premium white masterbatch designed for pharmaceutical applications requiring ultra-low odor and taste. Deep integration of Catalloy and Hyperzone technologies enables pre-colored, high-impact plastics for automotive components. LYB’s molecular-level dispersion capabilities allow precise color control during polymerization, creating ready-to-use materials optimized for demanding packaging and mobility applications.

hubergroup expands custom color manufacturing with energy-curing concentrates

hubergroup Chemicals has rapidly evolved from printing inks into a global supplier of specialty color concentrates, operating under a Chemicals-as-a-Service model. Its portfolio includes UV-curable oligomers, monomers, and high-intensity pigments for plastics, paints, and coatings. At PAINT INDIA 2026, hubergroup unveiled an expanded Custom Manufacturing program, enabling customers to co-develop proprietary color formulations. The company significantly increased its Asia and Africa footprint during 2025 to 2026, positioning itself as a high-tech alternative to commodity suppliers. Recent innovations include Energy Curing concentrates that enable ultra-fast drying and high color saturation for sensitive food-packaging applications.

Tosaf pioneers hybrid functional masterbatches for agricultural and industrial films

Tosaf Group specializes in functional masterbatches that combine color with technical performance such as anti-fog, anti-static, and UV protection. The company is particularly strong in agricultural and industrial films, where color consistency must withstand extreme ultraviolet exposure. Tosaf has integrated multiple regional acquisitions across Europe and the US, delivering a Local Touch, Global Reach service model. It dominates specialty additives for greenhouse covers and irrigation tubing, using color as a functional light-spectrum filter to improve crop yields. Strategically, Tosaf is developing Hybrid Masterbatches that consolidate multiple additives into single solutions, simplifying converter inventories and streamlining production of complex industrial components.

United States: High-Dispersion Masterbatches and Rapid PFAS-Free Conversion

The United States color concentrates industry is experiencing a technology-led upgrade driven by dispersion efficiency, sustainability mandates, and process automation across packaging, additive manufacturing, and specialty plastics. In 2025, Chroma Color Corporation fully commercialized its patented G3 technology, which integrates the pigment loading advantages of liquid color with pelletized handling stability. This innovation has materially reduced let-down ratios for packaging converters, improving color consistency while lowering total pigment usage per unit of output. The technology is gaining traction among high-speed extrusion and injection molding operations where dispersion uniformity directly impacts scrap rates and cycle times.

Regulatory pressure has further accelerated formulation shifts. State-level PFAS restrictions in Maine and California prompted U.S. manufacturers to transition approximately 90% of polymer processing aid masterbatches to fluoro-free chemistries by late 2025. Ampacet emerged as a frontrunner through its PROFLOW 1449 series, which delivers processing efficiency without siloxane or fluoropolymer additives. Sustainability innovation is also advancing in carbon black systems. In November 2024, Cabot Corporation launched REPLASBLAK, the first circular black masterbatch to achieve ISCC PLUS certification, enabling high-opacity coloration while incorporating certified circular content. Beyond packaging, new applications are emerging. In 2025, MechNano partnered with Bomar to introduce a low-viscosity masterbatch for 3D printing that combines color delivery with carbon nanotube-based mechanical reinforcement. Operational efficiency gains are reinforcing competitiveness, as major U.S. plants in Texas and Ohio deployed LIAD Smart blending systems in late 2025, cutting material waste during color changeovers through real-time gravimetric dosing.

China: Recyclability Standards and Ultra-Fine Dispersion for EV and Medical Applications

China’s color concentrates market is being reshaped by mandatory recyclability standards, targeted green R&D funding, and capacity expansion aligned with electric vehicle and medical-grade plastics. In August 2025, the State Administration for Market Regulation issued nine national standards governing recycled plastics, effective February 1, 2026. These standards explicitly require that color concentrates do not interfere with polymer detectability in automated sorting systems, forcing reformulation away from traditional opaque pigments toward NIR-compatible and low-interference color systems.

On the production side, BASF inaugurated a high-performance dispersant line in Nanjing in late 2025, leveraging Controlled Free Radical Polymerization to enable ultra-fine pigment dispersion for domestic EV components. This capability is critical for thin-wall automotive parts where color uniformity, surface aesthetics, and thermal stability must coexist. Strategic policy support is reinforcing innovation. Under the 2025–2026 Petrochemical Industry Roadmap, the Chinese government allocated significant R&D funding for zero-residue liquid colorants designed to prevent injector fouling in high-pressure medical molding processes. Export readiness is also tightening. Effective January 2026, the China Petroleum and Chemical Industry Federation began administering new masterbatch quality benchmarks to ensure compliance with EU and USFDA food-contact migration limits, raising the bar for formulation purity and traceability across the export-oriented color concentrates segment.

Germany: Circular Compliance and Bio-Based Color Concentrate Leadership

Germany stands at the forefront of regulatory-driven transformation in the color concentrates industry, with circular economy enforcement and bio-based innovation shaping competitive differentiation. In anticipation of the EU Packaging and Packaging Waste Regulation taking effect in August 2026, German masterbatch producers have standardized NIR-detectable Rec-NIR Black solutions to replace conventional carbon black in opaque packaging. This transition ensures compatibility with near-infrared sorting systems, safeguarding recyclability without sacrificing visual opacity.

Bio-based coloration is advancing rapidly. Lifocolor expanded its Lifocolor Bio portfolio in 2025, introducing color concentrates formulated with carriers derived entirely from renewable resources. These products are specifically engineered for compostable flexible films, addressing the growing demand for end-to-end sustainable packaging systems. Regulatory oversight on recycled content is intensifying in parallel. The European Commission confirmed new legal frameworks for early 2026 that tighten documentation requirements for recycled plastic imports, prompting German concentrate producers to implement digital Product Passports for additive traceability. Infrastructure investments are supporting faster customization. In September 2025, Lifocolor commissioned an automated sampling facility in Lichtenfels, enabling rapid prototyping of custom hues in application-realistic formats and significantly reducing customer lead times for color approval.

India: Localization of High-Load Masterbatches and Export-Oriented Pigment Integration

India’s color concentrates industry is scaling through localization incentives, sustainability partnerships, and rising demand from textiles, aerospace, and advanced polymers. Under the 2025 Production Linked Incentive Scheme 2.0, the government realized investments exceeding $21 billion in specialty chemicals, with a substantial allocation directed toward domestic production of high-end spinning masterbatches for the textile sector. This policy support is reducing reliance on imports while improving consistency in fiber coloration for large-volume yarn producers.

Sustainability-driven collaboration is gaining momentum. In mid-2025, Plastiblends India Ltd. partnered with regional recyclers to launch the BlueEdge masterbatch series, designed to neutralize yellowing in post-consumer recycled resins used in premium applications. Sector-specific demand is also diversifying. Increased domestic aviation spending has driven the development of anti-static and flame-retardant color concentrates for aircraft interiors, aligned with updated 2025 safety certifications. On the supply side, India’s transition to a net exporter of pigments in FY 2024–25 has enabled deeper domestic integration of azo and phthalocyanine pigments into high-load masterbatches, strengthening India’s export positioning across Southeast Asia.

Brazil: Bio-Polymer Compatibility and Climate-Resilient Color Systems

Brazil’s color concentrates industry is benefiting from strong alignment with bio-polymers, agriculture-driven demand, and regional logistics optimization. In 2025, Cromex S/A introduced advanced UV-stabilized masterbatches tailored for greenhouse films used in agribusiness. These formulations are engineered to extend service life under intense solar radiation, addressing durability challenges specific to tropical and subtropical farming environments.

Brazil’s leadership in bio-polymers is reinforcing innovation pathways. The country remains a global hub for Braskem I’m green bio-polyethylene, driving strong demand for color concentrates that preserve full bio-based integrity without compromising color strength or processability. Logistics efficiency is emerging as a competitive lever. In late 2025, major Brazilian compounders implemented just-in-time localized compounding units to serve the Mercosur trade bloc, reducing transportation-related emissions and improving responsiveness to regional color demand fluctuations.

Comparative Snapshot: Country-Level Strategic Direction in the Color Concentrates Industry

Color Concentrates Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Application Focus

|

Direction of Color Concentrate Innovation

|

|

United States

|

PFAS bans and dispersion efficiency

|

Packaging and additive manufacturing

|

High-dispersion, fluoro-free, circular blacks

|

|

China

|

Recyclability standards and EV growth

|

Automotive and medical plastics

|

Ultra-fine, zero-residue, CFRP-enabled colors

|

|

Germany

|

PPWR compliance and bio-based materials

|

Sustainable packaging

|

NIR-detectable and renewable-carrier concentrates

|

|

India

|

Localization incentives and pigment exports

|

Textiles and aerospace

|

High-load, recycled-content-compatible masterbatches

|

|

Brazil

|

Bio-polymer leadership and agribusiness

|

Agriculture and packaging

|

UV-stabilized, bio-compatible color systems

|

Color Concentrates Market Report Scope

Color Concentrates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$22.3 Billion

|

|

Market Size (2034)

|

$43.1 Billion

|

|

Market Growth Rate

|

7.6%

|

|

Segments

|

By Form (Solid Masterbatch, Liquid Color Concentrates, Powdered Concentrates), By Pigment Type (Inorganic Pigments, Organic Pigments, Specialty and Effect Pigments), By Carrier Resin (Polyethylene, Polypropylene, Polystyrene, Polyethylene Terephthalate, Bio-based and Biodegradable Polymers), By Application (Packaging, Automotive, Consumer Goods, Building and Construction, Textiles, Healthcare)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avient Corporation, Ampacet Corporation, LyondellBasell Industries N.V., Clariant AG, Cabot Corporation, A. Schulman LLC, BASF SE, DIC Corporation, Plastiblends India Limited, Cromex S.A., Americhem Inc., Tosaf Group, Gabriel-Chemie GmbH, Chroma Color Corporation, Penn Color Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Color Concentrates Market Segmentation

By Form

- Solid Masterbatch

- Liquid Color Concentrates

- Powdered Concentrates

By Pigment Type

- Inorganic Pigments

- Organic Pigments

- Specialty and Effect Pigments

By Carrier Resin

- Polyethylene

- Polypropylene

- Polystyrene

- Polyethylene Terephthalate

- Bio-based and Biodegradable Polymers

By Application

- Packaging

- Automotive

- Consumer Goods

- Building and Construction

- Textiles

- Healthcare

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Color Concentrates Industry

- Avient Corporation

- Ampacet Corporation

- LyondellBasell Industries N.V.

- Clariant AG

- Cabot Corporation

- Schulman LLC

- BASF SE

- DIC Corporation

- Plastiblends India Limited

- Cromex S.A.

- Americhem Inc.

- Tosaf Group

- Gabriel-Chemie GmbH

- Chroma Color Corporation

- Penn Color Inc.

*- List not Exhaustive