Market Overview: Black Masterbatches Market Growth Driven by Circular Pigments, EV Component Demand, and AI Dispersion Technologies (2025–2034)

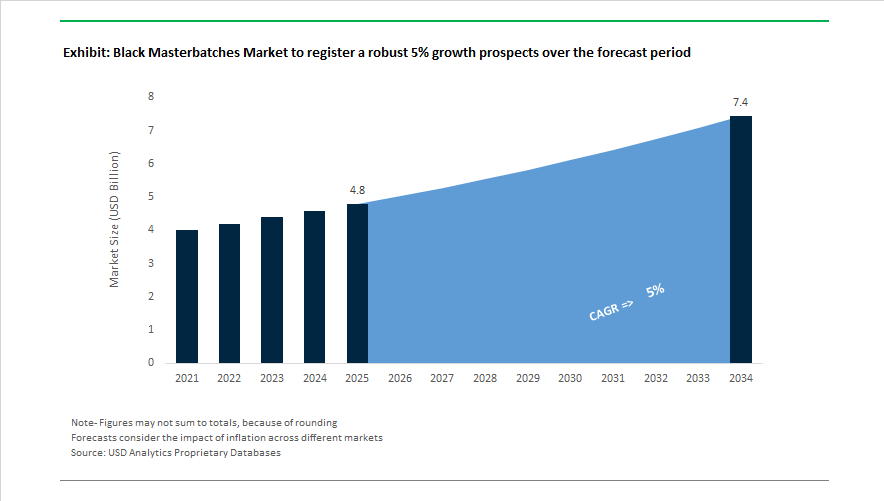

The black masterbatches market is projected to expand from USD 4.8 billion in 2025 to USD 7.4 billion by 2034, registering a CAGR of 5% supported by rising demand for recycled plastics, EV components, durable consumer goods, and high-performance polymer coloration. Sustainability-driven innovation accelerated in April 2024 when Avient Corporation presented its ColorForward 2025 design direction at Chinaplas, emphasizing matte and deep-gloss black finishes engineered with UV stability and heat dissipation for electric vehicle battery housings and high-voltage connectors. In May 2024, Cabot Corporation launched Replasblak universal circular black masterbatch using 45% ISCC PLUS mass-balance recycled polymers, enabling cross-resin compatibility for automotive compounders. July 2024 sustainability reporting from Cabot confirmed early achievement of greenhouse gas intensity reduction targets, reinforcing the shift toward low-emission carbon black production technologies.

Portfolio diversification and materials integration expanded through 2024 and 2025. In June 2024, Huber Engineered Materials completed acquisition of Active Minerals International, strengthening capabilities to develop hybrid black masterbatches combining pigments with functional fillers for automotive and construction polymers. In 2025, Ampacet introduced Natura Jet, a naturally pigmented black masterbatch compatible with PE, PP, PET, and PLA, targeting electronics and durable goods requiring deep jetness. During late 2025, Ampacet expanded into regulated sectors with ProVital+ LaserMark, enabling high-contrast laser marking on medical devices while meeting biocompatibility standards. AI-based carbon black dispersion monitoring systems adopted across Europe and Asia between late 2024 and 2025 reduced energy use and improved consistency in thin-film extrusion and geomembrane production.

Regional supply chain adjustments and circular material investments are shaping future growth. In early 2025, U.S. tariffs on carbon black feedstocks accelerated domestic masterbatch capacity expansion to offset import cost volatility. BASF strengthened regional presence in 2024 through partnerships with Indian masterbatch producers to supply durable black masterbatches for infrastructure-grade HDPE and PVC pipe systems. In January 2026, LyondellBasell reported strong performance of its Circulen circular masterbatch portfolio and raised investment targets for recycled plastic infrastructure. In February 2026, Avient launched Nymax REC formulations, incorporating high-jetness black masterbatch into recycled nylon systems for industrial applications. Circular feedstock scaling advanced toward 2026 as Michelin and Cabot progressed the Continua SCM recovered carbon black project in Trecate, aimed at supplying consistent high-volume recycled pigments.

Trends and Opportunities Transforming the Black Masterbatches Market

Shift Toward Low-PAH, High-Jetness Specialty Blacks

Automotive, consumer electronics, and high-touch product manufacturers are prioritizing black masterbatches with reduced Polycyclic Aromatic Hydrocarbon (PAH) content and enhanced aesthetic performance. The shift aligns with stricter environmental and human safety regulations, as well as demand for premium “piano-black” finishes in interior and exterior components. The implementation of Commission Regulation (EU) 2025/660 requires PAH content below 0.1 mg/kg for articles involving skin contact or indoor exposure, leading to wider adoption of advanced specialty carbon blacks. Technology upgrades such as AI-driven dispersion monitoring, now being deployed in commercial production, support consistent jetness, lower defects, and process efficiencies including reduced energy intensity.

Commercial Integration of Circular and Recovered Carbon Black

Sustainability objectives linked to Net Zero commitments are directing investments into recovered carbon black (rCB) utilization, especially in masterbatches for industrial and commodity uses. Market adoption is supported by innovations in mass-balance certification and standardized material qualification. The introduction of ISCC PLUS-certified circular black portfolios and ASTM D36 quality benchmarks addresses long-standing concerns such as ash content and structural variability. With improved traceability and reliability, rCB-based offerings are increasingly specified in applications such as construction films, non-pressure pipes, and molded packaging where sustainability credentials strengthen procurement preference.

Advanced Conductive Grades for 5G and EV Applications

Connectivity infrastructure expansion is accelerating demand for conductive black masterbatches engineered to deliver Electromagnetic Interference (EMI) shielding and Electrostatic Discharge (ESD) control. High-density data centers, compact IoT equipment, and 5G components require materials with stable electrical performance across demanding operating temperatures. The rapid scale-up of electric vehicle production adds another strategic growth layer, with conductive masterbatches becoming integral to battery trays, fluid-management components, and protective housings where safety and thermal management are critical design priorities.

UV-Resistant Masterbatches for Long-Life Geosynthetics

Infrastructure projects in waste management, water conservation, and mining reinforce the requirement for durable geomembranes and industrial films capable of sustaining multi-year UV exposure. Masterbatches combining high-structure carbon black with HALS-based stabilizer packages help manufacturers meet GRI specifications for oxidative resistance and long-term structural integrity. Product innovations in agricultural films and drip-irrigation systems demonstrate measurable extension of service life, particularly in regions with elevated solar radiation. These attributes contribute to lower lifecycle costs and greater sustainability value, making UV-stabilized masterbatches a priority for regulatory-driven infrastructure sectors.

Black Masterbatches Market Share and Segmentation Insights

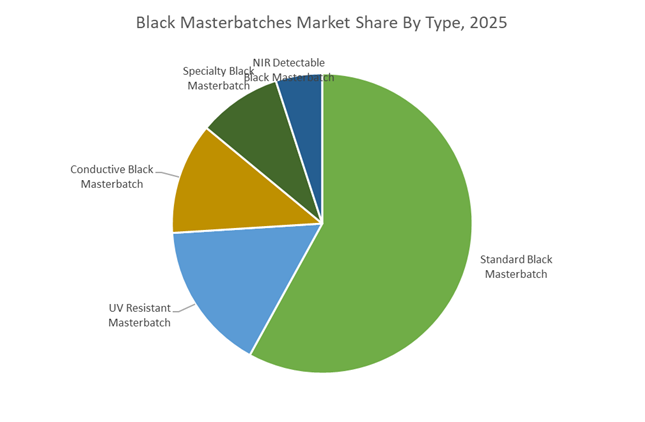

Market Share by Type: Standard Black Leads Volume While UV and NIR Grades Capture Value Growth

Standard black masterbatch accounts for 58% of global demand in 2025, anchoring the market through high-volume use in packaging, pipes, and general-purpose injection molding where pigmentation and basic UV protection are primary requirements. This segment remains margin-thin and closely correlated with GDP growth and industrial output. UV resistant masterbatch represents the second-largest and fastest-growing category, formulated with high-performance carbon black and stabilizers to extend outdoor service life in agricultural films, geomembranes, and exterior furniture, with tightening durability standards accelerating adoption. Conductive black masterbatch holds a meaningful share in electrical and electronics, delivering ESD protection for sensitive components, fuel systems, and cleanroom packaging as device miniaturization increases. Specialty black masterbatch, including food-grade and pharmaceutical-grade variants, commands premium pricing in regulated applications. NIR detectable black masterbatch remains the smallest but most innovative segment, enabling recyclability of black plastics under EU circular economy mandates and driving rapid uptake in sustainable packaging.

Market Share by End Use Industry: Packaging Dominance Supported by Electronics and EV Materials

Packaging leads black masterbatch consumption with a 44% share in 2025, spanning rigid containers and flexible films, with growing emphasis on recyclable mono-material structures and NIR-detectable solutions in Europe and North America. Automotive remains a core downstream sector, using black masterbatch in interior trim, exterior panels, and under-hood parts, while EV adoption is expanding demand for black-colored engineering plastics in battery housings and charging infrastructure. Building and construction utilizes black masterbatch in PVC pipes, roofing membranes, window profiles, and geomembranes, where UV stabilization is essential for long-term durability and infrastructure investment supports steady growth. Electrical and electronics is the fastest-growing end-use, driven by conductive grades for ESD trays, cable jacketing, and appliance housings, reinforced by 5G deployment and data center expansion. Agriculture forms a specialized segment, applying UV-stabilized black masterbatch in mulch films, greenhouse covers, and irrigation systems.

Competitive Landscape Analysis of the Black Masterbatches Market

The global black masterbatches market in 2026 is being reshaped by circular plastics adoption, ultra-thin film processing, EV electrification, and stringent recyclability mandates. Competition increasingly centers on captive carbon black supply, NIR-detectable blacks, PFAS-free formulations, graphene-enhanced conductivity, and low-dosage UV-stable systems. Leading producers are differentiating through Industry 4.0 dosing platforms, recycled-content compatibility, EMI-shielding compounds, and application-specific engineering for agriculture films, medical packaging, infrastructure pipes, and consumer electronics. Strategic priorities include ISCC PLUS certification, NIR sortability, high-speed extrusion performance, and turnkey polymer–masterbatch integration to support sustainable packaging and next-generation automotive and energy applications.

Cabot Corporation delivers circular, ultra-jet black masterbatches through captive carbon black integration

Cabot stands apart as the only vertically integrated black masterbatch leader producing its own carbon black, ensuring pigment consistency and supply security. Its REPLASBLAK Universal Circular series, scaled in 2026, delivers high-jetness blacks across polyolefins and engineering plastics with up to 45% mechanically recycled content under ISCC PLUS certification. Late 2025 expansion at Ville Platte strengthened output of circular reinforcing carbons for sustainable automotive trims. Through EVOLVE Sustainable Solutions, Cabot engineers particle size for ultra-fine dispersion, preventing pinholes in ultra-thin agricultural films. Its universal masterbatch technology, recognized with a CLEPA Innovation Award, simplifies material management across PE, PP, ABS, and PA.

Ampacet Corporation advances NIR-detectable and natural-pigment black masterbatches for recyclability

Ampacet leads functional black innovation with a strong focus on recyclability and high-speed processing. Natura Jet, introduced in late 2025 and early 2026, achieves deep blacks using naturally derived pigments for electronics and footwear. REC-NIR-Black enables near-infrared detection of black packaging, ensuring proper sorting and recycling of trays and films. At Plastindia 2026, Ampacet showcased its LIAD Smart Industry 4.0 platform for real-time dosing and color correction, cutting masterbatch waste significantly. The company also expanded healthcare offerings via ProVital+, delivering ISO 10993-compliant medical-grade blacks for pharmaceutical packaging and regulated applications.

Avient Corporation combines EMI shielding and recycled aesthetics in high-performance black systems

Avient, incorporating legacy Clariant masterbatch capabilities, specializes in high-performance aesthetics and multifunctional black formulations. In 2026, it prioritized PFAS-free internally lubricated blacks for automotive and industrial markets, replacing traditional processing aids. The company introduced conductive black masterbatches for 5G infrastructure and EV battery enclosures, delivering EMI shielding without compromising mechanical strength. Avient’s ReVive compatibilizers restore the appearance of recycled PE and PA blends, boosting gloss and reducing haze in black recycled plastics. It also dominates UV-blocking fiber applications, supplying durable black concentrates for outdoor textiles and automotive interiors requiring extreme light-fastness.

LyondellBasell integrates polymers and black masterbatches into turnkey infrastructure solutions

LyondellBasell leverages its position as a major polymer producer to deliver ready-to-use black compounds and masterbatches. Its full-portfolio approach combines Hyperzone PE and Catalloy technologies with tailored blacks for pipe and infrastructure markets. In January 2026, KARO 5.0 integration accelerated oriented film development for black barrier packaging. Medical-grade Asepthene MD and Purell resins are paired with low-odor black masterbatches for fluid delivery systems. Expansion across AfMEIT in early 2026 targets India’s natural-gas pipelines and e-commerce mailers, reinforcing LyondellBasell’s role in scalable, integrated polymer–masterbatch solutions.

Hubron International pioneers graphene-enhanced and high-loading precision black masterbatches

Hubron operates as a pure-play black masterbatch specialist, combining carbon black with advanced nanomaterials. Its partnership with Black Swan Graphene is commercializing graphene-enhanced blacks in 2026 for industrial tubing and construction, delivering superior thermal and electrical conductivity. Hubron is known for high-loading precision, achieving up to 50% carbon black with aggregates under 20 microns, ideal for high-speed extrusion. The company leads geosynthetics and irrigation with UV-stabilized blacks for mulch films and landfill liners. Its 2026 strategy emphasizes prescription masterbatches, drawing on a library of over 300 raw materials for niche electrical applications.

Tosaf Group optimizes low-dosage UV and matte black masterbatches for agriculture and packaging

Tosaf focuses on efficiency engineering, delivering low-dosage, high-impact black masterbatches for agriculture and flexible packaging. Its UV4120PE set a 2026 benchmark, achieving 80% UV-barrier performance at just 0.7 phr after 9,000 hours of field exposure. Matte-finish black masterbatches are gaining traction in consumer electronics and automotive interiors for premium tactile feel and glare reduction. Tosaf’s smart greenhouse blacks selectively block wavelengths to enhance crop growth while preventing soil overheating. Expansion of its Specialty Film division supports Europe’s automated packaging lines, with formulations designed to prevent plate-out during continuous production.

China Black Masterbatches Market: Energy Intensity Reduction and Scale-Driven Export Advantage

China’s black masterbatches industry is being reshaped by national energy targets, unmatched production scale, and a rapid pivot toward specialty formulations. Under the 2025 Carbon Peaking Action Plan, industrial producers are required to reduce energy consumption per unit of value added by 13.5% versus 2020 levels. This mandate is forcing masterbatch compounders to upgrade to energy-efficient twin-screw extrusion platforms and optimize dispersion efficiency, particularly in carbon-black-intensive grades. These investments are concentrated in Shandong and Jiangsu, where integrated plastics production involving masterbatches reached roughly 6.4 million metric tons during 2023 and 2024, reinforcing China’s role as the world’s largest manufacturing base.

Capacity and pricing dynamics further strengthen competitiveness. Cabot Corporation expanded its Tianjin footprint in 2024 by 25,000 metric tons to serve domestic automotive demand, especially high-jetness and UV-stable grades. In May 2025, regional oversupply pushed carbon black prices down to around USD 1,030 per metric ton, far below U.S. price peaks, enabling export arbitrage for Chinese compounders. At the same time, domestic producers are moving up the value chain. Conductive black masterbatches for electronic packaging are gaining traction, while graphene-enhanced formulations aligned with the Made in China 2025 framework are being adopted to improve impact resistance in lightweight EV structural components. This combination of cost leadership and specialty innovation positions China as both a volume supplier and a technology contender through 2026.

United States Black Masterbatches Market: Regulatory Pressure, Circular Grades, and Re-shored Electronics Supply

In the United States, the black masterbatches market is being driven by regulatory enforcement, recycled-content compliance, and strategic re-shoring. Packaging laws enacted in New Jersey and mirrored by other states impose daily civil penalties for failure to meet post-consumer recycled content thresholds. As a result, converters are rapidly shifting toward masterbatches engineered for compatibility with recycled polymers, without compromising gloss or jetness.

Innovation has followed regulation. In May 2025, Cabot Corporation introduced reUN5285 and reUN5290 universal circular black masterbatches, enabling high-gloss coloration across multiple polymer bases while incorporating recycled content. Cost pressures are also shaping sourcing strategies. Feedstock tariffs effective January 1, 2026 prompted suppliers such as Huber Advanced Materials to announce global price increases, reinforcing the need for value-added formulations. Infrastructure investments are moving in parallel. Avient Corporation and peers showcased fluoro-free polymer processing aids in 2025 to ensure compliance with upcoming PFAS-related bans. Federal incentives under the CHIPS and Science Act are further accelerating localization of electronic-grade masterbatches to secure cleanroom packaging for the domestic semiconductor supply chain.

India Black Masterbatches Market: Infrastructure Pull, Localization Incentives, and Export Momentum

India’s black masterbatches industry is benefiting from a rare convergence of infrastructure demand, industrial policy, and export competitiveness. Expansion of the National Infrastructure Pipeline across 2024 and 2025 has generated sustained demand for high-performance black masterbatches used in HDPE and PVC piping systems, where 50-year UV longevity is a non-negotiable requirement. These applications favor formulations with optimized carbon black dispersion and long-term weathering resistance.

Policy support is amplifying capacity build-out. Under the Production Linked Incentive scheme, which recorded roughly ₹2 lakh crore in realized investments by September 2025, chemical and automotive manufacturers have accelerated localization of specialty additive production. Downstream demand from electronics is also structural. A 28-fold increase in domestic mobile phone production between 2015 and 2025 has created large-scale requirements for anti-static and aesthetic black masterbatches for device housings. Export capability is strengthening as well. At PlastIndia 2026, the Ministry of Commerce highlighted India’s transition into a net exporter of polymer additives, with exports accounting for close to half of output in specialized segments. This positions India as both a consumption-driven and export-oriented hub for black masterbatches.

Germany and the European Union Black Masterbatches Market: Circular Sorting Mandates and Carbon Cost Equalization

Across Germany and the European Union, the black masterbatches market is increasingly defined by circular economy enforcement and carbon accounting. The European Commission is preparing a late-2026 legal framework to tighten controls on plastic imports, protecting domestic recyclers that lost capacity in 2025 due to energy price volatility. This policy backdrop is accelerating adoption of masterbatches that support mechanical recycling at scale.

A pivotal requirement is near-infrared detectability. To meet the EU’s 2025 packaging waste recovery target of 65 percent, converters are mandated to use NIR-detectable black masterbatches that allow automated sorting of carbon-black-colored plastics. Solutions such as Ampacet REC-O Black have become reference materials for compliance. Cost structures will further evolve with the full implementation of the Carbon Border Adjustment Mechanism from 2026, which is expected to neutralize the price advantage of high-carbon imports and favor German producers operating renewable-energy-powered plants. Despite regulatory support, Europe is forecast to lose around one million metric tons of recycling capacity by the end of 2025, prompting a strategic rebalancing of masterbatch supply toward North American and Asian hubs for certain applications.

Country-Level Strategic Snapshot: Black Masterbatches Industry

Black Masterbatches Market County Level Snapshot

|

Country / Region

|

Strategic Orientation

|

Key Developments

|

|

China

|

Energy efficiency and scale leadership

|

Carbon Peaking mandates, Tianjin capacity expansion, conductive and graphene-enhanced grades

|

|

United States

|

Circular compliance and re-shoring

|

PCR penalties, circular masterbatches, PFAS-free processing aids, CHIPS-driven localization

|

|

India

|

Infrastructure-led demand and exports

|

Pipe and electronics demand, PLI-driven localization, net exporter transition

|

|

Germany / EU

|

Circular sorting and carbon pricing

|

NIR-detectable mandates, CBAM implementation, recycling capacity realignment

|

Black Masterbatches Market Report Scope

Black Masterbatches Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2034)

|

$7.4 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Type (Standard Black Masterbatch, Specialty Black Masterbatch, Conductive Black Masterbatch, UV Resistant Masterbatch, NIR Detectable Black Masterbatch), By Carrier Resin (Polyethylene, Polypropylene, Polyvinyl Chloride, Polystyrene and ABS, Engineering Plastics), By Carbon Black Content (Low Concentration, Medium Concentration, High Concentration), By Application Method (Injection Molding, Blow Molding, Film Extrusion, Pipe and Profile Extrusion, Fiber Spinning), By End Use Industry (Packaging, Automotive, Building and Construction, Agriculture, Electrical and Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cabot Corporation, Ampacet Corporation, Avient Corporation, LyondellBasell Industries, Birla Carbon, Clariant, Huber Engineered Materials, Plastiblends, Orion Engineered Carbons, Tosaf Group, Penn Color, Plastika Kritis, RTP Company, Colloids, Sanyo Color Works

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Black Masterbatches Market Segmentation

By Type

- Standard Black Masterbatch

- Specialty Black Masterbatch

- Conductive Black Masterbatch

- UV Resistant Masterbatch

- NIR Detectable Black Masterbatch

By Carrier Resin

- Polyethylene

- Polypropylene

- Polyvinyl Chloride

- Polystyrene and ABS

- Engineering Plastics

By Carbon Black Content

- Low Concentration

- Medium Concentration

- High Concentration

By Application Method

- Injection Molding

- Blow Molding

- Film Extrusion

- Pipe and Profile Extrusion

- Fiber Spinning

By End Use Industry

- Packaging

- Automotive

- Building and Construction

- Agriculture

- Electrical and Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Black Masterbatches Industry

- Cabot Corporation

- Ampacet Corporation

- Avient Corporation

- LyondellBasell Industries

- Birla Carbon

- Clariant

- Huber Engineered Materials

- Plastiblends

- Orion Engineered Carbons

- Tosaf Group

- Penn Color

- Plastika Kritis

- RTP Company

- Colloids

- Sanyo Color Works

*- List not Exhaustive