Pigments Market Size 2025–2034: $31.6 Billion to $54.3 Billion at 6.2% CAGR Driven by Automotive Coatings, Sustainable Iron Oxides, and Industry Consolidation

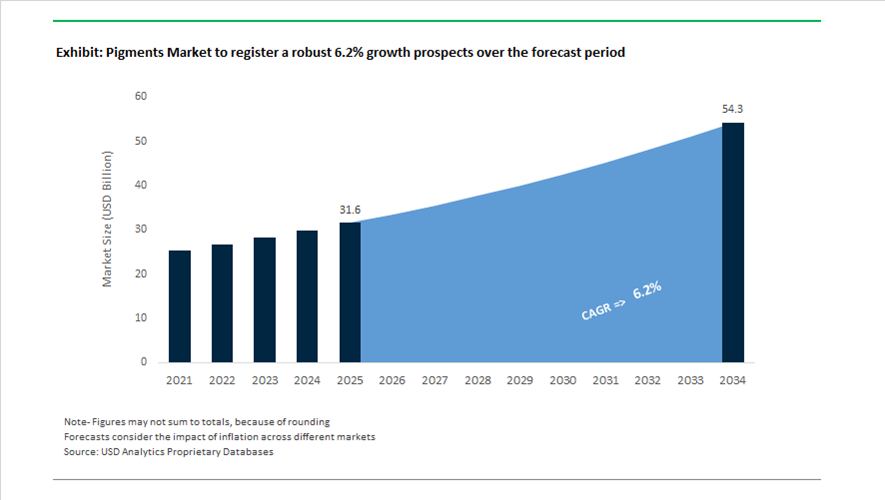

The global pigments market is projected to expand from $31.6 billion in 2025 to $54.3 billion by 2034, registering a CAGR of 6.2%. Demand for inorganic pigments (titanium dioxide, iron oxides), organic pigments, effect pigments, and specialty colorants is accelerating across automotive coatings, construction materials, plastics, packaging, and printing inks. Rising EV production, premium architectural finishes, and sensor-compatible automotive coatings are increasing requirements for high-durability, weather-resistant, and interference-based pigment technologies. At the same time, tightening environmental standards and carbon footprint transparency requirements are reshaping sourcing strategies and manufacturing investments in the global pigments industry.

A defining structural shift occurred in March 2025 when Sudarshan Chemical Industries Limited completed acquisition of Germany-based Heubach Group through its subsidiary Sudarshan Europe B.V. The transaction created a diversified global pigment leader spanning 19 manufacturing sites. The integration combines Heubach’s two-century technological legacy with Sudarshan’s operational scale, addressing Heubach’s 2024 insolvency challenges and reinforcing the high-performance organic and specialty pigment portfolio. In early 2026, Sudarshan inaugurated a Global Capability Center in partnership with Genpact, forming the operational backbone of its “New Sudarshan” strategy focused on AI-enabled global integration and responsible color innovation.

Portfolio realignment continues to reshape the competitive landscape. Following its earlier divestment of pigments to the Heubach platform, Clariant confirmed in its 2024 Integrated Report (released March 2025) its full pivot toward additives and care chemicals, formally exiting direct pigment manufacturing. Meanwhile, in January 2026, International Chemical Investors Group (ICIG) signed an agreement to acquire Venator Germany GmbH’s Duisburg site as part of Venator’s broader European restructuring. Earlier, in July 2024, Kronos Worldwide acquired full ownership of Louisiana Pigment Company, consolidating its titanium dioxide production in North America, though it subsequently reported inventory cost pressures entering 2025.

Capacity rationalization is also evident in Asia. In January 2026, Tronox announced the permanent closure of its 46,000 metric ton per year titanium dioxide facility in Fuzhou, citing weak domestic demand and unsustainable pricing dynamics caused by overcapacity. This move reflects broader supply-demand balancing efforts within the TiO₂ segment, which remains highly sensitive to sulfur costs and Chinese production cycles.

Innovation in automotive and effect pigments remains a major growth catalyst. In October 2025, BASF Coatings launched its 2025–2026 Automotive Color Trends collection, highlighting advanced interference pigments engineered for visual depth and compatibility with autonomous driving sensors. At CHINACOAT 2025, Sun Chemical introduced Glacier Exterior Ceramic White S1303M, a synthetic mica pearl pigment delivering intense purity and enhanced weather resistance for automotive and industrial applications. Earlier, in January 2024, Altana strengthened its ECKART division through acquisition of Silberline, expanding aluminum-based effect pigment capabilities across North America and Asia.

Sustainability-driven differentiation is intensifying. In March 2025, Lanxess launched Scopeblue iron oxide pigments with approximately 35% lower product carbon footprint through renewable energy integration and optimized raw material selection. However, rising compliance costs and regulatory pressures have influenced pricing. Effective January 1, 2025, Sun Chemical implemented global pigment price increases, citing inflation, raw material volatility, and expanded sustainability reporting obligations.

Trends and Opportunities in the Global Pigments Market

Strategic Friend-Shoring and Regionalization of High-Performance Pigments Supply Chains

The global pigments market is undergoing a pronounced structural realignment as manufacturers respond to energy volatility, geopolitical risk, and customer demands for supply security. During 2024–2025, Europe experienced sustained energy cost inflation of approximately 8–12% for energy-intensive pigment synthesis, materially compressing margins for producers of high-performance pigments (HPP). As a result, pigment suppliers are re-architecting their manufacturing footprints through “friend-shoring” strategies, prioritizing politically aligned, cost-competitive regions such as India and North America while retaining Europe as a specialty and innovation hub.

A defining transaction in this shift was the late-2024 acquisition of the global Heubach Group operations by Sudarshan Chemical Industries Limited (SCIL). The strategic rationale extended beyond scale. SCIL is consolidating European assets into specialty-only manufacturing centers while migrating intermediates and selected production lines to India to hedge against German energy price volatility and regulatory overhead. This model allows continuity for automotive, aerospace, and industrial coatings customers that require uninterrupted access to high-chroma, high-durability organic pigments.

Parallel capacity investments reinforce this trend. In November 2025, Sun Chemical announced a 200-metric-ton expansion of perylene pigment capacity at its Ludwigshafen site, targeting premium automotive and luxury coatings that demand exceptional weatherfastness and color purity. At the same time, India has emerged as a strategic absorber of global pigment capacity. Under the Make in India framework, ECKART, part of the Altana Group, partnered with Runaya in 2025 to establish a sustainable aluminum powder facility producing spherical atomized granules for aerospace and high-value effect pigments. These investments collectively signal a bifurcation of the pigments value chain, with Europe focused on innovation-led specialty output and Asia assuming a larger share of resilient, scalable production.

Reformulation Pressure Driven by NIR Detectability and Circular Economy Regulation

Regulatory enforcement of the EU Packaging and Packaging Waste Regulation in 2025 has accelerated reformulation across the pigments market, particularly for black and dark shades. Conventional carbon black absorbs near-infrared light, rendering black plastics undetectable to automated recycling systems. This regulatory bottleneck has become a commercial urgency for packaging, consumer goods, and automotive OEMs seeking compliance with recyclability mandates.

A major technological breakthrough occurred in December 2025 with the launch of UPM Circular Renewable Black™, the world’s first bio-based, carbon-negative, NIR-detectable black pigment. Produced from renewable lignin at UPM’s €1.3 billion Leuna biorefinery, the pigment enables black packaging to be correctly sorted using existing NIR infrastructure, unlocking recyclability for premium black consumer packaging. This innovation materially shifts the economics of sustainable packaging and establishes a new benchmark for pigment performance aligned with circular economy objectives.

Similar decarbonization efforts are evident in effect pigments. In March 2025, ECKART introduced its AL-II portfolio based on secondary aluminum feedstocks, delivering metallic brilliance with the lowest reported product carbon footprint in the category. These products allow coatings manufacturers to address Scope 3 emissions reduction targets without compromising visual performance. Sustainability credentials are increasingly gatekeepers for market access, as evidenced by Sun Chemical’s Paliogen Red perylene pigments receiving OEKO-TEX ECO PASSPORT certification in 2025, enabling broader adoption in sustainable textiles and high-end automotive interiors.

Functional Pigments for Energy-Efficient and “Cool Surface” Applications

Urban heat island mitigation, energy efficiency mandates, and green building standards are transforming pigments into functional materials rather than purely aesthetic components. Infrared-reflective pigments represent one of the fastest-growing opportunity segments as municipalities and commercial developers mandate cool roofs, reflective façades, and thermally optimized infrastructure.

In 2025, Sun Chemical highlighted its Spectrasense functional black perylene pigments, which deliver deep black coloration while remaining NIR-reflective. Field data indicates that surfaces formulated with these pigments can remain up to 5°C cooler under direct solar exposure, translating into measurable reductions in HVAC energy consumption for buildings and improved thermal comfort in automotive interiors. This performance aligns with increasingly stringent Solar Reflectance Index requirements embedded in municipal building codes across North America and Europe.

Functional pigment demand is also expanding into mobility and autonomy. At the European Coatings Show 2025, ECKART launched radar-transparent effect pigments engineered to allow uninterrupted transmission of ADAS signals through metallic-looking automotive bumpers. These materials address a critical integration challenge for LiDAR- and radar-equipped vehicles, positioning functional pigments as enablers of next-generation autonomous driving architectures rather than passive design elements.

High-Stability Pigment Dispersions for Industrial Digital Textile and Packaging Printing

The global shift toward on-demand production, mass customization, and localized micro-factories is accelerating the replacement of analog dyeing with digital pigment inkjet printing across textiles and flexible packaging. In 2025, pigment-based inks continued to displace reactive and acid dyes due to their substrate versatility, lower water consumption, and compatibility with polyester-rich and blended fabrics without chemical pre-treatment.

Market data indicates that pigment-based inks now dominate new installations for Direct-to-Garment and Direct-to-Fabric systems, supported by aggressive portfolio expansion from equipment and materials leaders such as Kornit Digital, DuPont, and Sun Chemical. The digital textile printer market, valued at approximately $2.9 billion in 2025, is increasingly defined by high-speed single-pass systems. These platforms require ultra-fine, highly stable pigment dispersions with zero agglomeration to prevent nozzle failure in industrial printheads operating at multi-million-dollar utilization rates.

Innovation is also extending into digital packaging. In September 2025, Sun Chemical launched its first HP Indigo-approved primer for label applications, creating a chemical bridge that improves pigment adhesion and color gamut on challenging flexible substrates. This development accelerates the displacement of flexographic printing in short-run and high-SKU packaging, reinforcing pigment dispersions as a core growth engine within digital manufacturing ecosystems.

Pigments Market Share and Segmentation Insights

Inorganic Pigments Lead Global Pigment Consumption with Titanium Dioxide Dominating Volume Demand

Inorganic pigments accounted for 52.80% of the Pigments Market by type in 2025, reflecting their widespread use in coatings, plastics, and construction materials that require high opacity, durability, and thermal stability. Major inorganic pigments include titanium dioxide, iron oxides, chromium oxides, and other mineral-based pigments used in industrial and decorative applications. Titanium dioxide remains the most widely used pigment globally due to its ability to provide exceptional whiteness and hiding power in paints, plastics, and paper products. In 2025, optimization of titanium dioxide usage through improved dispersion technologies and particle engineering is shaping pigment formulation strategies as manufacturers balance cost volatility and sustainability concerns associated with TiO₂ production.

Paints and Coatings Segment Drives Pigment Demand Across Architectural and Industrial Coating Production

Paints and coatings represented 48.60% of the Pigments Market by application in 2025, making it the largest end-use segment for color pigments worldwide. Architectural coatings, automotive finishes, and industrial protective coatings require pigments to deliver color development, opacity, and long-term weather resistance. Global construction growth and industrial manufacturing activity continue to sustain large-scale pigment consumption in coating formulations. In 2025, the industry shift toward waterborne and high-solids coating technologies with reduced VOC emissions is influencing pigment selection, with coating manufacturers prioritizing pigments that maintain color strength, stability, and dispersion efficiency in environmentally compliant coating systems.

Pigments Market Competitive Landscape

The global pigments market is undergoing consolidation and sustainability-driven transformation, with organic pigment integration and TiO₂ portfolio optimization reshaping competition. Key players are prioritizing Product Carbon Footprint tracking, PFAS-free chemistries, and high-performance pigments for automotive, electronics, and energy transition applications.

Sudarshan-Heubach Merger Creates Diversified Global Pigment Platform with Digital Supply Chain Integration

Sudarshan Chemical Industries, following its March 2025 acquisition of Heubach Group, has established a global pigment platform spanning 19 international sites. The “ONE Sudarshan” integration strategy combines European technical expertise with India-based cost-efficient manufacturing to enhance competitiveness. The company introduced lead-free alternative pigment dispersions at PlastIndia 2026 under its “Responsible Color Innovation” initiative targeting construction and automotive applications. A Global Capability Center developed with Genpact in late 2025 supports digital supply chain optimization and operational agility. The expanded portfolio includes organic, inorganic, and anti-corrosive pigments aimed at revitalizing Heubach’s legacy revenue base. Strategic focus centers on integration efficiency, sustainable pigment chemistry, and global market expansion.

DIC Strengthens Functional Pigment Leadership with High-Chroma Innovations and PCF Transparency

DIC Corporation, through Sun Chemical, maintains global leadership in pigment manufacturing with strong emphasis on functional pigments for new energy and automotive sectors. A $10 million investment in Newport, Delaware expands quinacridone pigment capacity for high-chroma red and violet applications. The launch of Paliocrom® Brilliant Ruby L 3558 introduces a high-intensity aluminum effect pigment suitable for both solvent-borne and water-borne NEV coatings. Expansion of perylene pigment capacity in Ludwigshafen by 200 metric tons supports demand for transparent pigments in digital packaging. The Pigment Finder platform now includes Product Carbon Footprint (PCF) data, enhancing ESG transparency for customers. Product strategy integrates high-performance pigments with digital sustainability tracking and advanced application performance.

BASF Refocuses Pigment Portfolio on High-Margin Industrial Solutions and Biomass-Balanced Innovation

BASF SE is restructuring its pigments and dispersions business under the “Winning Ways” strategy to prioritize high-margin specialty segments. The divestiture of its decorative paints business in October 2025 enables focus on automotive and electronics OEM pigment applications. The company reported €59.7 billion in sales in 2025, with EBITDA of €6.6 billion reflecting ongoing portfolio optimization. Expansion at the Zhanjiang Verbund site increases production of high-purity intermediates used in advanced pigment synthesis. Development of biomass-balanced dispersants supports reduction of fossil feedstock usage without altering formulation performance. Strategic direction emphasizes green transformation, high-purity pigment chemistry, and regulatory-aligned innovation.

Chemours Optimizes TiO₂ Portfolio with Pricing Discipline and Digital Customer Platforms

The Chemours Company is managing its Titanium Technologies segment through pricing strategies and asset optimization in a volatile TiO₂ market. The December 2025 Ti-Pure™ price increase addresses rising energy and ore costs while protecting margins. The sale of its Taiwan Titanium Technologies site for approximately $360 million supports debt reduction from a $4.2 billion position as of Q3 2025. A strategic agreement with SRF Limited enhances localized supply chain resilience in India through “friend-shoring.” Digital platforms such as Ti-Pure™ Flex and Ti-Pure™ Connect provide real-time inventory and formulation optimization tools for customers. Operational focus includes cost control, digital engagement, and high-performance TiO₂ product lines.

Tronox Strengthens Vertical Integration While Diversifying into Rare Earth Processing

Tronox Holdings plc leverages its vertically integrated mining and pigment production model to manage feedstock volatility in the TiO₂ market. The closure of its 46,000 metric ton Fuzhou plant in January 2026 reflects strategic retrenchment in response to pricing pressures and rising production costs. The company reported a 13% increase in TiO₂ sales volumes in Q4 2025, driven by market share gains in India. Expansion into rare earth element processing includes evaluation of a cracking and leaching facility in Australia for monazite tailings. Despite a net loss in 2025, Tronox generated $53 million in free cash flow in Q4, indicating improving financial stability. Strategy focuses on cost optimization, vertical integration, and diversification into critical minerals.

Venator Streamlines Pigment Portfolio with Divestitures and Focus on High-Purity Specialty Segments

Venator Materials PLC is executing a portfolio simplification strategy focused on stabilizing its specialty pigment business. The company completed divestitures of its French and German pigment units in early 2026, following prior restructuring initiatives. An EcoVadis Gold rating for three consecutive years highlights strong performance in environmental and ethical standards. The sale of its UK TiO₂ operations to LB Group reflects a shift away from lower-margin assets toward higher-value European production sites. The company maintains a strong position in ultramarine blue and high-purity iron oxide pigments for cosmetics and pharmaceutical applications. Strategic direction emphasizes specialty pigments, ESG performance, and margin-focused portfolio optimization.

India – Acquisition-Led Global Scale with Policy-Backed Cost Realignment

India’s pigments industry entered a structurally new phase in 2025 following the completion of the Heubach Group acquisition by Sudarshan Chemical Industries Limited. This transaction positions the combined entity as the world’s second-largest pigment producer, with 19 manufacturing sites across Europe, the Americas, and APAC. The strategic logic is not volume-driven expansion but portfolio rebalancing. Commodity pigment production is being progressively shifted to Indian low-cost manufacturing hubs, while Frankfurt is retained as a global center for specialty pigment R&D and customer-specific formulation support. The announced ₹1,180 crore upfront integration investment underscores a clear focus on margin optimization, backward integration, and supply-chain rationalization rather than capacity-led growth.

This corporate consolidation is being reinforced by policy-level interventions. The 2025–2026 Union Budget allocation of ₹1,61,965 crore to the Ministry of Chemicals has created targeted incentives for high-value specialty pigments and intermediates. Trade policy relief, particularly the June 2025 extension of Export Obligation timelines from 6 to 18 months for QCO-covered products, has eased working-capital pressure for pigment exporters navigating logistics volatility. In parallel, the NITI Aayog Chemical Industry Report 2025 has formalized a roadmap toward shared infrastructure via dedicated Chemical Funds, supporting scale efficiencies across pigment clusters. Demand-side visibility is improving through the expanded National Technical Textiles Mission, which now explicitly includes advanced pigments for UV-protective, functional, and performance-wear textiles.

China – Regulation-Led Reformulation with Electronics-Grade Prioritization

China’s pigment industry is undergoing a compliance-driven reset shaped by stricter toxicological thresholds and a pivot toward electronics-grade materials. The release of mandatory standards GB 30981.1-2025 and GB 30981.2-2025 by the State Administration for Market Regulation introduces tighter limits on heavy metals and aromatic compounds, with enforcement starting June 2026. These standards are forcing accelerated reformulation across organic pigment portfolios, particularly impacting legacy azo and solvent-heavy systems. Compliance costs are rising, but the regulatory clarity is favoring large, vertically integrated producers capable of rapid portfolio migration.

At the same time, China is pushing up the value curve. The 2025 Work Plan for Stabilizing Growth explicitly prioritizes Grade G5 ultra-high-purity pigments for electronics, color filters, and display applications, aiming to displace premium imports from Japan. This strategic intent was visible at CHINACOAT 2025, where Sun Chemical and DIC Corporation introduced advanced aluminum-effect pigments for automotive OEM finishes, signaling China’s ambition in effect pigments as well. On the production side, BASF confirmed that its Zhanjiang Verbund site remains on track for a 2025 startup, powered by renewable electricity, anchoring China’s role as a global demand center for high-performance organic pigments.

Germany – Portfolio Carve-Outs and Technology-Led Differentiation

Germany’s pigment landscape in 2025 is characterized by strategic divestments paired with deep technology specialization. The October 2025 agreement between BASF and Carlyle, alongside QIA, to carve out BASF’s coatings and automotive pigment-related business at an enterprise valuation of €7.7 billion reflects a deliberate capital reallocation. Rather than retreating from pigments, Germany is narrowing its focus toward high-technology niches where regulatory complexity and application engineering create defensible margins.

Innovation remains the anchor. ECKART has advanced radar-transparent metallic pigments designed to allow ADAS sensors to function through coated EV bumpers, positioning pigments as functional enablers rather than decorative inputs. Concurrently, BASF’s €16 billion green transformation capex program between 2025 and 2028 is reshaping pigment value chains through low-carbon feedstocks and energy optimization. Circular economy innovation is also accelerating, with German firms scaling Loopamid technologies that chemically recycle pigmented textiles into virgin-quality fibers without color loss, directly addressing one of the hardest challenges in pigment sustainability.

United States – Ownership Shifts and Regulatory-Driven Innovation

The US pigments industry is being reshaped by ownership realignment and regulatory tightening rather than capacity expansion. The acquisition of Merck KGaA’s Surface Solutions business by Global New Material International for $725 million has materially shifted control of US-based pearlescent pigment assets, signaling increased foreign participation in specialty effect pigments. This transition is occurring alongside strong downstream demand from digital printing and advanced coatings.

Operational investments are aligned with application shifts. Cabot Corporation expanded its Massachusetts facility to double capacity for aqueous inkjet dispersions, supporting the rapid migration from analog to digital printing platforms. Regulatory pressure is a central driver of innovation. The updated EPA Sustainable Chemistry framework for 2026 has tightened scrutiny of PFAS-containing surfactants in pigment dispersions, triggering a measurable increase in domestic R&D focused on PFAS-free alternatives. This regulatory trajectory is elevating compliance-led differentiation as a core competitive parameter in the US pigment market.

Comparative Snapshot – Pigments Industry by Country

Pigments Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

2025–2026 Inflection Point

|

Competitive Positioning

|

|

India

|

Global consolidation and cost arbitrage

|

Heubach integration, QCO relief

|

Scaled global producer

|

|

China

|

Regulatory tightening and purity upgrade

|

GB 30981 enforcement, G5 focus

|

High-volume adaptive market

|

|

Germany

|

Portfolio rationalization and tech depth

|

BASF carve-out, radar pigments

|

Premium innovation hub

|

|

United States

|

Ownership shifts and compliance innovation

|

PFAS restrictions, inkjet growth

|

Application-led specialty market

|

Pigments Market Report Scope

Pigments Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$31.6 Billion

|

|

Market Size (2034)

|

$54.3 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Type (Organic Pigments, Inorganic Pigments, Specialty & Effect Pigments), By Formulation (Powder, Liquid & Paste Dispersions, Masterbatches, Water-Borne Systems), By Application (Paints & Coatings, Printing Inks, Plastics, Cosmetics & Personal Care, Textiles & Leather)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sudarshan Chemical Industries Limited, DIC Corporation, BASF SE, Global New Material International, Altana AG, Clariant AG, Venator Materials PLC, KRONOS Worldwide Inc., The Shepherd Color Company, Lanxess AG, Toyo Ink SC Holdings Co. Ltd., Cabot Corporation, Evonik Industries AG, Tronox Holdings plc, Ferro Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pigments Market Segmentation

By Type

- Organic Pigments

- Azo Pigments

- Phthalocyanine Pigments

- Quinacridone Pigments

- High-Performance Pigments

- Inorganic Pigments

- Titanium Dioxide

- Iron Oxide

- Carbon Black

- Mixed Metal Oxides

- Specialty & Effect Pigments

By Formulation

- Powder

- Liquid & Paste Dispersions

- Masterbatches

- Water-Borne Systems

By Application

- Paints & Coatings

- Printing Inks

- Plastics

- Cosmetics & Personal Care

- Textiles & Leather

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Pigments Industry

- Sudarshan Chemical Industries Limited

- DIC Corporation

- BASF SE

- Global New Material International

- Altana AG

- Clariant AG

- Venator Materials PLC

- KRONOS Worldwide Inc.

- The Shepherd Color Company

- Lanxess AG

- Toyo Ink SC Holdings Co. Ltd.

- Cabot Corporation

- Evonik Industries AG

- Tronox Holdings plc

- Ferro Corporation

*- List not Exhaustive