Market Overview: Sudarshan–Heubach Consolidation, REACH-Driven Reformulation, and Eco-Compliant Chemistries Reshape Azo Pigments Market

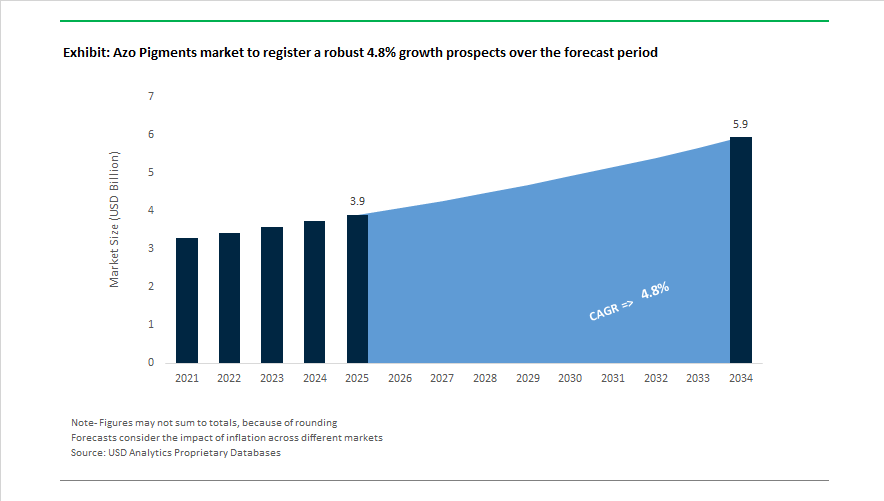

The Azo pigments market is valued at $3.9 billion in 2025 and is forecast to reach $5.9 billion by 2034, expanding at a 4.8% CAGR. Growth is anchored in demand for high-performance organic pigments, Azo reds and yellows, low-VOC colorants, heavy-metal-free pigments, water-dispersible Azo systems, automotive coating pigments, industrial paint colorants, and plastic masterbatch pigments. Structural change began in April 2024, when Heubach GmbH filed for insolvency, disrupting supply of high-durability Azo grades used in automotive and coatings sectors. This event accelerated consolidation, culminating in October 2024–March 2025 with Sudarshan Chemical Industries acquiring the global pigment business of Heubach Group, elevating Sudarshan to the second-largest global pigment supplier and strengthening its portfolio of specialty Azo chemistries.

Pricing power and sustainability compliance defined the next phase. Sun Chemical, part of DIC Corporation, implemented global pigment price increases in January 2025, citing higher raw material costs and capital investments needed for evolving environmental standards. In parallel, BASF introduced eco-compliant Azo pigment ranges during 2024, engineered to minimize heavy metal content and align with low-VOC architectural and industrial coating requirements. Clariant enhanced Asia-Pacific production capabilities in 2024 for high-durability colorants and lightfastness stabilizers, while initiating its CHF 80 million savings program during 2024–2025, including production line rationalization. Leadership transition at Clariant occurred in April 2025 with the appointment of Ben van Beurden as Chairman, reinforcing emphasis on energy-efficient chemical operations. Operational optimization extended to digitalization, as major producers such as BASF deployed AI-driven production control in 2024 to improve batch consistency and color strength uniformity in Azo pigment manufacturing.

Market direction through 2025 emphasized regulatory adaptation and portfolio rationalization. REACH updates across Europe and North America in 2025 accelerated adoption of water-dispersible Azo pigments in decorative paints, replacing solvent-based systems to meet green building standards. DIC Corporation and Sun Chemical showcased high-chroma innovations at CHINACOAT in November 2025, demonstrating premium orange and complementary shades aligned with modern automotive styling. Cost discipline also emerged as a theme, with Orion S.A. initiating workforce reductions in late 2024–2025 to stabilize margins amid feedstock volatility. Post-merger restructuring continued when Sudarshan completed the liquidation of Heubach Colorants Scandinavia in December 2025, streamlining its global entity structure.

Trends and Opportunities Reshaping Growth Strategy in the Azo Pigments Market

Market Trend: Regulatory Pressure Forcing Reformulation Toward Low-Amine and Fully-Disclosed Azo Pigments

The Azo Pigments Market is entering a compliance-driven reformulation cycle, where pigment suppliers must certify ultra-low aromatic amine release under thermal stress and ensure transparency along the supply chain. The EU Ecolabel v3.0 (February 2025) now requires a "low-amine" certification for pigments used in architectural paints, with stricter trace limits targeting residual aromatic amines in Pigment Red 170 and Pigment Yellow 83.

In North America, California Proposition 65 amendments (January 2025) require short-form warnings that specify at least one chemical of concern, forcing pigment users in toys and textiles to publicly disclose azo-related impurities. As a result, R&D inquiries for “amine-free” pigment solutions increased an estimated 24% in 2025, significantly shifting procurement strategies among major coating formulators.

Market implications are accelerating in Scandinavia. The December 2025 Danish EPA restriction on select blue azo pigments with a 30 ppm amine limit has triggered nearly universal batch-testing requirements for imported pigment lots sold into European textile supply chains. This trend is pushing global players toward tightly controlled production, digital traceability, and standardized impurity disclosures — transforming azo pigments from bulk commodities into specification-controlled materials.

Market Trend: Capital Reallocation Toward High-Performance Non-Azo Alternatives

Producers are defending revenue sustainability by diversifying color portfolios away from regulatory-exposed azo lines into High-Performance Pigments (HPPs) such as Diketopyrrolopyrrole (DPP) and Quinacridones. These chemistries are rapidly gaining share in automotive OEM coatings and industrial paint systems, where heat and UV endurance remain non-negotiable.

During its December 2025 briefing, BASF confirmed activation of its loopamid® chemical-recycling facility to strip pigments and dyes from nylon, positioning itself for an ESG-aligned non-azo portfolio. Simultaneously, BASF expanded distribution with OQEMA for specialty organic pigments that comply with 2026 construction-sector regulations.

Performance benchmarking from a September 2025 automotive pigment guide classified Quinacridone and Perylene reds as new standards capable of passing SAE J2527 xenon-arc testing, outperforming traditional azo reds in metallic and pearlescent finishes.

A differentiating technology path is emerging: bio-based pigments. In 2025, Clariant and Heubach (post-consolidation) began leveraging algae and agricultural waste feedstocks to decouple pigment production from petrochemical precursors, enhancing investor ESG scoring and securing long-horizon procurement contracts.

Market Opportunity: Ultra-Fine Azo Pigments for Digital Textile Printing Growth

Digital textile printing is transforming the colorants demand curve, creating a premium niche for ultra-fine, nano-grade azo pigment dispersions optimized for high-speed inkjet performance.

The Digital Textile Printing Ink segment reached $1.98 billion in 2025, and pigment inks are projected to grow at a double-digit CAGR through 2029. Adoption is accelerating as brands like DuPont expand the Artistri® P1600 platform, which relies on pigment dispersions engineered to avoid clogging and maintain storage stability.

Commercial specifications are shifting toward nano-pigments (<200 nm), delivering 20–30% higher color strength and enabling formulators to reduce ink load while achieving richer reds and deeper blacks. For digital presses, "ultra-low salt" impurities are becoming a supply-side differentiator, as 2025 industrial trials confirmed that reducing ionic contaminants by 15% can extend printhead uptime by up to 4,000 operating hours.

Market Opportunity: IR-Reflective Azo Chemistries for Cooling-Oriented Coatings

Urban sustainability policies are opening a new high-value segment: IR-reflective azo pigments engineered for thermal efficiency in buildings, automotive panels, and infrastructure.

A 2025 Ohio Academy of Science study showed that coatings formulated with next-generation NIR-reflective azo pigments can lower interior temperatures by 3–5°C when applied at only 10% pigment loading, positioning them as viable alternatives to traditional HEUCODUR Blacks.

Under the European Green Deal (2024–2025), municipal procurement codes increasingly mandate high-albedo roofing and facade coatings. IR-reflective Azo Yellows and Oranges are gaining traction because they deliver desired aesthetics without the heat-capture profile of conventional organic pigments.

Automotive cabin cooling is another growth vector. In Q3 2025, pigment manufacturers—including Fineland Chem—demonstrated IR-reflective pigments that reduce EV interior heat by up to 10°C, enabling downsizing of HVAC systems and improving battery range economics.

Azo Pigments Market Share and Segmentation Insights

Product Type Market Share: Monoazo Leads Volumes While Benzimidazolone Drives Premium Growth

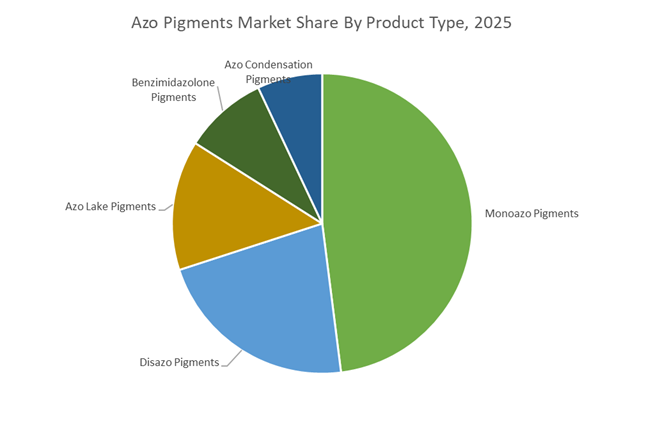

In 2025, monoazo pigments hold 48% of global azo pigments market share, retaining volume leadership as cost-effective yellow, orange, and red colorants for mass-market inks, plastics, and coatings. However, this segment faces margin compression from Chinese overcapacity and ongoing substitution by high-performance alternatives in premium applications. Disazo pigments provide improved heat and solvent resistance and are widely specified in plastics and automotive coatings where mid-tier durability is required. Benzimidazolone pigments represent the fastest-growing sub-segment, delivering superior lightfastness and weatherability while increasingly competing with phthalocyanine and quinacridone pigments in high-end coatings. Azo lake pigments remain under regulatory pressure, with calcium and barium lakes restricted under EU REACH and US CPSIA, particularly in toys and food packaging. Azo condensation pigments occupy a specialized niche, offering exceptional durability but limited adoption due to high molecular weight synthesis costs.

End-Use Industry Market Share: Printing Inks Dominate as Plastics and Coatings Shift to High-Performance Grades

By end-use, printing inks account for 42% of azo pigment consumption in 2025, driven by strong demand for high tinting strength in flexographic and gravure packaging inks, especially across Asia’s flexible food packaging sector. While digital printing poses a structural threat, conventional ink volumes remain resilient. Paints and coatings are steadily migrating toward benzimidazolone and azo condensation pigments, as industrial and architectural formulators replace cadmium and lead chromates with heavy-metal-free organic alternatives. Plastics and rubber favor disazo and benzimidazolone grades, capable of withstanding higher processing temperatures in polypropylene and engineering plastics where monoazo pigments fall short. Textiles continue a long-term decline, pressured by reactive and disperse dye substitution and EU Annex XVII restrictions on arylamine-based azo dyes. Food and stationery applications remain highly regulated, relying on non-migratory, non-toxic pigments, delivering stability but modest growth.

Azo Pigments Market Competitive Landscape

The global azo pigments market in 2026 is defined by sustainability-led reformulation, digital color management, and rapid capacity expansion across Asia and Europe. Leading manufacturers are investing heavily in NIR-detectable pigments, fiber-grade textile colors, and low-migration formulations for packaging, toys, and food-contact applications. Strategic priorities include Product Carbon Footprint transparency, REACH compliance, AI-driven molecular design, and vertically integrated precursor supply. Automotive coatings, textile spinning, printing inks, and agricultural seed treatments remain core demand engines, while regulatory pressure is accelerating the shift toward PFAS-free, low-SVOC, and circular pigment chemistries.

Digital color ecosystems and NIR-ready azo pigments from DIC Corporation / Sun Chemical

DIC Group, via Sun Chemical, leads the azo pigments market through its Color & Display platform and advanced digital workflow. At PlastIndia 2026, Sun Chemical unveiled Spectrasense™ Black K 0089 FK, a non-carbon black pigment engineered for NIR detectability in recycling streams and solar heat control. Its Heliogen® and Fastogen® ranges now emphasize fiber-grade pigments like Fastogen® Pink K 4430 FP, certified with OEKO-TEX® ECO PASSPORT for sustainable textile spinning. Integration capabilities include the Pigment Viewer App for HDPE color simulation and the Pigment Finder platform, providing instant PCF data and regulatory documentation to support fully digitalized customer workflows.

Responsible color leadership and global scale by Sudarshan Chemical Industries Ltd.

Sudarshan Chemical has emerged as a global azo pigment powerhouse following the full integration of the Heubach Group by early 2026, creating one of the world’s most comprehensive organic pigment portfolios. Its Sudaperm™ and Sudafast™ lines deliver extreme durability, offering over 2,000 hours of xenon-arc weather resistance for outdoor engineering polymers. At PlastIndia 2026, Sudarshan showcased its “Make in India, For the World” strategy, highlighting expanded capacity for HPP and CICP pigments for automotive applications. Regulatory leadership remains central, with halogen-free, FDA-compliant, and low-migration azo formulations tailored for toys and food-contact packaging.

AI-designed automotive azo effects and low-SVOC dispersions from BASF SE

BASF continues to shape high-end azo pigment innovation for coatings and automotive markets through its integrated Verbund value chain. In early 2026, BASF launched Near-Zero SVOC dispersion technology to reduce indoor air emissions in architectural coatings. The company also opened a Global Digital Hub in Hyderabad to accelerate AI-driven molecular modeling for next-generation light-stable azo reds and yellows. Its 2025 to 2026 automotive color collection focuses on interference pigments and azo synergists that create depth and “visual void” effects. Internal precursor production provides resilience against petrochemical volatility while supporting consistent global pigment supply.

Sustainability-conscious azo chemistry from Clariant AG

Clariant is repositioning itself as a pure-play specialty chemicals leader, prioritizing bio-based feedstocks and circularity in azo pigment production. Under its Greater Chemistry strategy, the company targets a 46.9% reduction in Scope 1 and 2 emissions by 2030, with 2026 focused on scaling PFAS-free technologies. Its Graphtol™ and PV Fast™ ranges serve high-margin care chemicals and industrial applications requiring low-toxicity, high-chroma yellows. Clariant also introduced a Formulator Toolbox for agriculture, including Dispersogen® PSL 100 to stabilize azo dispersions in seed coatings, while divesting legacy pigment units to sharpen its specialty focus.

Export-grade azo pigments and REACH compliance from Trust Chem Co., Ltd.

Trust Chem is China’s largest independent organic pigment producer, bridging Asian manufacturing scale with Western regulatory standards. The company is the primary Chinese supplier to achieve full REACH compliance across its azo portfolio, enabling strong penetration into Europe’s value-segment printing ink market. Trust Chem specializes in high-volume Pigment Yellow 12 and Pigment Red 57:1 for packaging and textiles, delivering consistent tinting strength. In late 2025, it expanded its Hangzhou technical service center to provide rapid color matching for e-commerce packaging brands. Investments in closed-loop wastewater systems ensure uninterrupted operations under China’s Blue Sky environmental mandates.

Vertically integrated azo reds and seed treatment pigments from Meghmani Organics Ltd.

Meghmani Organics has rapidly scaled into a top-tier global pigment supplier through deep vertical integration, spanning CP Crude to finished azo and phthalocyanine pigments. In late 2025, the company commissioned a new multipurpose facility in Gujarat, shifting production toward high-performance azo reds for paints and coatings. Its 2026 strategy emphasizes agricultural-pigment synergy, developing seed treatment pigments that provide UV protection and high visual contrast. Meghmani reported record export growth in Q1 2026, driven by new contracts with European automotive refinish brands seeking cost-effective yellow pigment alternatives backed by stable, integrated supply.

India Azo Pigments Market: Global Consolidation Hub and Sustainable Pigment Manufacturing Base

India has emerged as a strategic anchor for global azo pigment consolidation, driven by decisive corporate actions and supportive industrial policy. In early 2025, Sudarshan Chemical Industries Limited completed the acquisition of the Heubach Group, creating the unified platform “ONE Sudarshan.” This integration brought together 17 manufacturing sites and more than 695 pigment products, repositioning India as a central node in global organic pigment supply chains rather than a regional exporter. The consolidation has strengthened India’s leverage in printing inks, plastics, and coatings where consistency of shade and dispersion is critical.

Product-led innovation continues to reinforce this position. In December 2025, Sudarshan introduced Sudafast Red 313D, a high-performance red azo pigment optimized for global ink formulators seeking batch-to-batch reliability and improved dispersion. Government backing is reinforcing these trends. Under the NITI Aayog 2025 Global Value Chains framework and initiatives such as Aroma Mission 2.0 and the rollout of eight high-potential chemical clusters, India is channeling R&D funding toward non-toxic organic pigments and eco-friendly azo alternatives. At the manufacturing level, companies like Aksharchem India are lowering carbon intensity through captive solar power installations, while strict enforcement of bans on 112 hazardous azo dyes ensures alignment with export market requirements.

China Azo Pigments Market: Scale, Environmental Coding, and Reformulation Pressure

China remains the largest-volume producer of azo pigments and intermediates, but its industry structure is shifting rapidly under regulatory and environmental pressure. BASF’s Zhanjiang Verbund expansion, scheduled to reach a major milestone by early 2026, will add world-scale citral and downstream intermediates that influence the global availability of precursors for yellow and orange azo pigments. This reinforces China’s upstream dominance while also embedding higher process integration.

At the same time, regulatory tightening is reshaping formulation strategies. The Draft Ecological and Environmental Code released in 2025 mandates full disclosure of hazardous properties for all pigments, accelerating consolidation into state-monitored Green Chemical Zones. In parallel, the GB 30981.1-2025 standard, effective from June 2026, imposes stricter limits on harmful aromatic compounds in coatings. These measures are forcing domestic formulators to reformulate away from legacy azo chemistries. Sustainability-linked innovation is also emerging, highlighted by BASF’s loopamid® facility in Shanghai, which chemically removes dyes and additives from textile waste, linking pigment chemistry to circular polymer streams.

Germany Azo Pigments Market: Regulatory Substitution and Automotive Color Leadership

Germany’s role in the azo pigments industry is defined less by volume and more by regulatory leadership and high-value applications. German producers are at the forefront of substituting legacy pigments such as Pigment Yellow 12 and 13 with safer, large-molecule disazo alternatives to comply with updated EU food-contact and packaging directives under REACH. This substitution-driven demand is reshaping pigment portfolios across Europe.

Innovation in automotive coatings further underscores Germany’s influence. BASF Coatings’ 2025–2026 Automotive Color Trends showcased advanced shades such as Tesseract Blue, combining interference effects with azo-hybrid technologies to deliver depth and color travel demanded by premium OEMs. Meanwhile, DIC and its subsidiary Sun Chemical expanded capacity in Ludwigshafen in late 2025, integrating lower-carbon manufacturing processes to serve Europe’s growing appetite for high-performance organic pigments. Germany thus functions as a technology and compliance benchmark rather than a cost-driven producer.

Japan Azo Pigments Market: Transparency, Electronics Integration, and Functional Diversification

Japan’s azo pigment industry is increasingly defined by carbon transparency and cross-sector innovation. In November 2025, DIC Corporation achieved third-party certification for its Product Carbon Footprint methodology, setting a regional precedent for measurable sustainability claims in pigments. This transparency is becoming critical for electronics and automotive customers with stringent disclosure requirements.

Japanese producers are also extending azo chemistry into advanced applications. At SEMICON Japan 2025, DIC showcased specialized azo-based color filters and photoresist pigments tailored for next-generation displays and sensors. Beyond coloration, the company leveraged pigment know-how to develop GELRAMIC™ endothermic materials to mitigate thermal runaway in EV batteries, signaling a strategic pivot from decorative pigments toward functional materials with safety and performance attributes.

Indonesia Azo Pigments Market: Food-Contact Compliance and Southeast Asian Expansion

Indonesia is emerging as a strategic manufacturing base for food-contact compliant azo pigments. In August 2025, DIC Group commissioned a new sustainable production facility dedicated to coatings for direct food-contact materials. The move addresses rising regional demand for safer azo-based colorants in packaging, particularly for multinational FMCG brands operating across Southeast Asia. Indonesia’s role is therefore less about innovation leadership and more about cost-effective, regulation-aligned capacity expansion close to fast-growing consumer markets.

Strategic Positioning of the Azo Pigments Industry by Country

Azo Pigments market County Level Snapshot

|

Country

|

Strategic Focus

|

Implication for Azo Pigments

|

|

India

|

Global consolidation and green manufacturing

|

India positioned as a primary global supply hub

|

|

China

|

Scale with regulatory reformulation

|

Shift toward compliant, reformulated azo systems

|

|

Germany

|

REACH substitution and automotive innovation

|

Demand for high-value, safer disazo pigments

|

|

Japan

|

Carbon transparency and functional expansion

|

Azo chemistry moving into electronics and EV safety

|

|

Indonesia

|

Food-contact compliant capacity

|

Regional hub for safe packaging pigments

|

Azo Pigments Market Report Scope

Azo Pigments market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.9 Billion

|

|

Market Size (2034)

|

$5.9 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Monoazo Pigments, Disazo Pigments, Azo Condensation Pigments, Benzimidazolone Pigments, Azo Lake Pigments), By Color Shade (Red Pigments, Yellow Pigments, Orange Pigments), By Solubility (Water Soluble Azo Dyes, Insoluble Azo Pigments), By End Use Industry (Printing Inks, Paints and Coatings, Plastics and Rubber, Textiles, Food and Stationery)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DIC Corporation, Sudarshan Chemical Industries Limited, BASF SE, Clariant AG, Heubach Group, Trust Chem Co Ltd, Lily Group Co Ltd, Dainichiseika Color and Chemicals, Meghmani Organics Limited, Atul Limited, Lanxess AG, Toyo Ink SC Holdings, Shandong Sunshine Pigment, Asahi Songwon Colors Limited, Anshan Hifichem

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Azo Pigments Market Segmentation

By Product Type

- Monoazo Pigments

- Disazo Pigments

- Azo Condensation Pigments

- Benzimidazolone Pigments

- Azo Lake Pigments

By Color Shade

- Red Pigments

- Yellow Pigments

- Orange Pigments

By Solubility

- Water Soluble Azo Dyes

- Insoluble Azo Pigments

By End Use Industry

- Printing Inks

- Paints and Coatings

- Plastics and Rubber

- Textiles

- Food and Stationery

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Azo Pigments Industry

- DIC Corporation

- Sudarshan Chemical Industries Limited

- BASF SE

- Clariant AG

- Heubach Group

- Trust Chem Co Ltd

- Lily Group Co Ltd

- Dainichiseika Color and Chemicals

- Meghmani Organics Limited

- Atul Limited

- Lanxess AG

- Toyo Ink SC Holdings

- Shandong Sunshine Pigment

- Asahi Songwon Colors Limited

- Anshan Hifichem

*- List not Exhaustive