UV Absorbers Market Overview 2025–2034: $2.6 Billion to $4.2 Billion at 5.6% CAGR Driven by High-Performance Light Stabilizers, Food-Contact Compliance, and Semiconductor UV Technologies

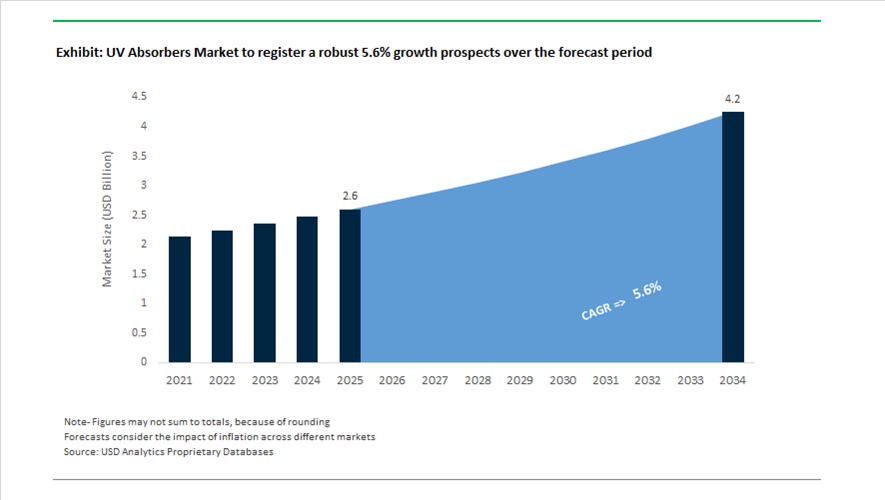

The global UV Absorbers market is valued at $2.6 billion in 2025 and is projected to reach $4.2 billion by 2034, expanding at a CAGR of 5.6%. Growth is being fueled by rising demand for light stabilizers, UV absorbers for plastics, HALS stabilizers, benzotriazole UV absorbers, triazine UV absorbers, UV protection additives for coatings, and weather-resistant polymer formulations. Increasing outdoor exposure requirements in construction membranes, electric vehicle components, food-contact packaging, semiconductor lithography materials, and renewable energy infrastructure are reshaping formulation standards. The market is transitioning toward high thermal stability, acid-resistant NOR-HALS systems, non-benzotriazole chemistries, antimony-free catalysts, and regulatory-compliant additives as environmental scrutiny intensifies.

Product innovation between 2024 and 2026 reflects a shift toward advanced polymer durability. In May 2024, SONGWON introduced SONGSORB® 1164, a triazine-based UV absorber engineered for food-contact polyolefins and engineering plastics exposed to outdoor weathering. In September 2024, Everlight Chemical received recognition for its Eversorb® AQ series, solvent-free liquid light stabilizers designed for aqueous coatings and adhesives without compromising optical clarity. In March 2025, SABIC showcased LNP™ ELCRES™ polycarbonate copolymers optimized for fiber optic closures and data center housings requiring extreme UV and heat resistance. In October 2025 at K 2025, BASF launched Tinuvin® NOR® 600, a next-generation NOR-HALS stabilizer delivering superior acid resistance and thermal stability for roofing membranes, PVC structures, and artificial turf systems. During the same period, Clariant introduced antimony-free AddWorks™ titanium-based catalyst solutions to simplify PET recycling while enhancing UV durability. ADEKA announced in October 2025 the construction of a 3.2 billion yen plant dedicated to organometallic compounds for High-NA EUV lithography, strengthening UV absorption control in advanced semiconductor patterning. In February 2026 at Plastindia, Milliken presented RESIST™ XTR colorants engineered for high-voltage EV connectors, combining extreme temperature tolerance with long-term UV weather resistance.

Sustainability and regulatory compliance are restructuring the competitive landscape. In September 2025, ADEKA’s TRANSPAREX™ clarifier received global recognition for polypropylene transparency performance while maintaining UV stability, reinforcing the convergence of optical clarity and photoprotection in packaging and consumer goods. In fiscal 2025, Sakai Chemical announced its exit from pigment-grade titanium dioxide to pivot toward high-purity dielectric materials and cosmetic-grade ultrafine zinc oxide, aligning with demand for transparent UV-blocking solutions in personal care. Throughout 2025 and into 2026, BASF integrated its Tinuvin® and Irgastab® stabilizers into the VALERAS® sustainability platform, demonstrating extended service life for solar pontoons exceeding 30 years and enhanced durability of agricultural mulch films. In December 2025, the European Chemicals Agency migrated chemical safety data to the ECHA CHEM platform, increasing transparency for benzotriazole-based UV absorbers facing bioaccumulation scrutiny. These regulatory adjustments are accelerating the industry shift toward triazine chemistries, HALS-NOR systems, zinc oxide nanomaterials, and recyclable polymer-compatible stabilizers, positioning UV absorbers as critical enablers of long-life plastics, EV infrastructure resilience, semiconductor fabrication reliability, and circular packaging solutions.

Trends and Opportunities Shaping the UV Absorbers Market

OEM-Mandated UV Resilience for 800V EV Architectures and Premium Finishes

Automotive OEM specifications are rapidly tightening as electric vehicles transition to 800V and higher architectures, placing unprecedented stress on exterior coatings and polymer components. Elevated thermal radiation from high-density battery packs, coupled with the rising adoption of deep, high-chroma pigments, is accelerating the specification of advanced UV absorber systems. In March 2025, global coating suppliers such as PPG and BASF expanded the rollout of next-generation waterborne clearcoats tailored for EV production hubs in China and Southeast Asia. These systems integrate triazine-based UV absorbers with Hindered Amine Light Stabilizers to deliver long-term gloss retention and resistance to chalking, even under persistent tropical UV exposure.

From a formulation standpoint, UV absorbers are now required to survive higher bake temperatures in automated spray lines, typically between 140°C and 160°C, without volatilization or loss of activity. Data from 2024–2025 qualification cycles indicates that hybrid absorber packages can reduce basecoat fading by up to 35% in high-voltage EV models, where darker aesthetic colors amplify photothermal stress. This is transforming UV absorbers from optional additives into OEM-mandated performance enablers within the EV coatings value chain.

Global Phase-Out of Legacy UV-328 and Benzophenones in Food-Contact Applications

Regulatory enforcement has entered a decisive phase for low-molecular-weight UV absorbers in food-contact plastics, triggering a structural reformulation wave across PET bottles, polyolefin films, and rigid containers. As of January 2025, the Stockholm Convention finalized guidance placing UV-328 under Annex A, effectively mandating global substitution unless narrow exemptions are granted. This action has immediate implications for multinational brand owners operating across more than 180 signatory countries, where inventory tracking and reporting requirements now extend deep into the additive supply chain.

In parallel, food safety regulators are converging on stricter migration controls. The U.S. Food and Drug Administration has intensified post-market surveillance of migrating additives, while the Ministry of Health, Labour and Welfare implemented its Positive List System for food-contact materials in June 2025. These changes are accelerating demand for high-molecular-weight, low-volatility UV absorbers that meet specific migration limits under both FDA and Japanese frameworks. As a result, non-migrating absorbers with strong compatibility in high-clarity polymers are becoming the new baseline for compliant food packaging.

High-Refractive-Index UV Absorbers for AR/VR Optics and Advanced Sensors

The commercialization of AR and VR devices is opening a premium niche for UV absorbers engineered for high-refractive-index optical resins, where even minor yellowing or haze is unacceptable. In January 2025, Sanyo Chemical Industries introduced HILUCIS, a nanoimprint resin platform with a refractive index approaching 1.9. This development highlights a broader opportunity for UV absorber suppliers: conventional stabilizers often compromise optical clarity or depress refractive index in near-UV wavelengths, limiting their use in waveguides and micro-lenses.

As optical components in smartphones, facial recognition systems, and AR smart glasses continue to miniaturize, resin systems with refractive indices above 1.6 are becoming standard. UV absorber manufacturers that can deliver liquid-phase stabilizers fully soluble in high-RI monomers, without inducing micro-cracking or discoloration, are positioned to capture high-margin demand from next-generation optics and sensing platforms.

Photoselective UV Management in Agrivoltaics and Greenhouse Films

Agrivoltaics and controlled-environment agriculture are creating a distinct growth pathway for UV absorbers that combine polymer protection with crop-performance optimization. In early 2025, specialty suppliers including 3V Sigma published data demonstrating how modern greenhouse films rely on UV absorbers to block destructive UV-B radiation while transmitting photosynthetically active radiation. This selective filtering prevents photo-oxidative degradation of polyolefin films, significantly extending service life and reducing replacement frequency.

Beyond durability, photoselective UV absorbers are emerging as functional tools in sustainable farming. By filtering UV wavelengths used by certain pests for navigation, these additives can lower pest pressure in greenhouse and agrivoltaic systems by up to 20%, supporting reduced pesticide usage in line with EU Farm to Fork objectives. This dual role positions UV absorbers as strategic inputs not only for material longevity but also for precision agriculture outcomes, expanding their relevance well beyond traditional plastics stabilization.

UV Absorbers Market Share and Segmentation Insights

Chemical Class Market Share: Benzotriazoles Lead with Superior UV Stability and Polymer Compatibility

Benzotriazoles dominate the UV absorbers market with a 42.80% share in 2025, driven by their high UV absorption efficiency, thermal stability, and compatibility across a wide range of polymers and coating systems. These UV stabilizers provide broad-spectrum protection while maintaining clarity and color stability, making them essential in plastics and coatings. Other chemical classes such as triazines, benzophenones, salicylates, and oxalanilides serve specialized applications with varying performance characteristics. A key trend is the increasing demand for high-performance coatings, where enhanced photostability and resistance to extraction are critical for long-term durability in automotive, industrial, and architectural environments.

Application Market Share: Plastics Segment Leads with Outdoor Durability and UV Protection Requirements

Plastics account for 42.80% of the UV absorbers market in 2025, reflecting the critical role of UV stabilizers in preventing photodegradation in polymer materials. Applications include automotive components, construction materials, packaging, and consumer goods exposed to sunlight and environmental conditions. Coatings, personal care, adhesives and sealants, renewable energy, and textiles contribute additional demand across diverse sectors. A key growth driver is the increasing use of plastics in outdoor applications, where long-term durability, resistance to discoloration, and retention of mechanical properties are essential, driving the adoption of advanced UV absorber systems tailored to specific polymer formulations and performance requirements.

UV Absorbers Market Competitive Landscape

The UV Absorbers market in 2026 is defined by material resilience engineering, low-VOC and SVOC-free formulations, and non-migratory stabilizers designed for floating solar, automotive coatings, and outdoor infrastructure, ensuring extended durability under extreme UV exposure and strict indoor air quality regulations.

BASF SE Expands UV Stabilizer Innovation for Floating Solar and Circular Plastics

BASF SE is reinforcing its leadership in the UV Absorbers market through advanced light stabilizers integrated with digital formulation tools and sustainability-driven innovation. The company implemented up to 20% global price increases in March 2026 to offset raw material inflation and fund green chemistry R&D. Its collaboration with Xfloat Ltd. enhances UV durability in floating photovoltaic systems, a fast-growing segment in renewable energy infrastructure. BASF is integrating UV absorbers into loopamid® recycled polyamide streams to maintain UV resistance in circular textile applications. Expansion of its additives and dispersions line in Mangalore strengthens its footprint in South Asia’s architectural coatings market. This combination of renewable energy alignment and circular economy integration enhances BASF’s competitive positioning.

SONGWON Strengthens Regional Supply and Recycling-Focused UV Stabilizer Portfolio

SONGWON Industrial Co., Ltd. is advancing its position in the UV Absorbers market through localized production and regulatory leadership. The establishment of a One Pack Systems facility in Saudi Arabia enables regional blending of UV absorbers and antioxidants for the Middle East polyolefin industry. Its leadership role in ELiSANA strengthens influence over global REACH compliance and chemical stewardship frameworks. SONGWON is commercializing recycling-specific stabilizers such as XP2121 and SONGNOX® PQ to enhance the performance of recycled polypropylene and polyethylene films. The SONGSORB® 5710 benzotriazole remains a key product for high-transparency plastics like polycarbonate and PMMA used in electronics. This dual focus on sustainability and regional supply chain optimization supports long-term growth.

Syensqo Accelerates Low-VOC Automotive UV Stabilizers and AI-Driven Material Discovery

Syensqo is positioning itself as a leader in high-performance UV absorbers by focusing on advanced material applications in automotive and agriculture. Its CYASORB CYNERGY SOLUTIONS® V703 meets strict 2026 requirements for low VOC emissions and low fogging in automotive interior components. The CYASORB THT® 6460 stabilizer delivers multi-year durability for greenhouse films, resisting degradation from pesticides and fumigants. The company is leveraging Syensqo.AI to accelerate molecular discovery, targeting a 50% reduction in HALS loading while maintaining performance. Its decarbonization roadmap includes transitioning UV stabilizer production sites to clean energy. This integration of AI-driven R&D and regulatory compliance strengthens Syensqo’s position in premium stabilization solutions.

Adeka Corporation Integrates Green UV Absorbers into High-Purity Electronics Supply Chains

Adeka Corporation is strengthening its presence in the UV Absorbers market through high-purity additive systems and renewable plastic integration. The company established a global supply chain for incorporating green UV absorbers into recycled resins used by leading electronics OEMs. Its new organometallic facility supports ultra-pure chemical production for EUV lithography, reinforcing its expertise in precision materials. Adeka’s TRANSPAREX™ technology enhances clarity while working synergistically with UV absorbers for premium packaging applications. The company is also advancing weight-saving automotive solutions using UV-stabilized HALS, enabling thinner plastic components with long-term weather resistance. Its focus on environment-friendly additives aligns with evolving global regulatory standards.

Everlight Chemical Leads Waterborne UV Stabilizer Innovation for Eco-Friendly Coatings

Everlight Chemical is emerging as a leader in eco-friendly UV absorbers through its waterborne and solvent-free stabilizer technologies. The Eversorb® AQ series, recognized with the Taiwan Excellence Award, offers up to 90% active content and supports sustainable coatings formulations. Its Eversorb® HP series replaces powdered stabilizers in sealants and adhesives, improving process efficiency and preventing discoloration in architectural applications. The non-toxic Eversorb® HP5 grade meets stringent EU and North American safety standards without hazard labeling requirements. Strengthened distribution partnerships in Europe enhance supply for epoxy and polyurethane markets. This focus on water-based, high-performance stabilizers positions Everlight at the forefront of green coating technologies.

China UV Absorbers Market Accelerated by Regulatory Tightening and Advanced Materials Integration

China represents the most policy-driven and structurally coordinated UV absorbers market globally, with regulatory reform directly reshaping product design, capacity placement, and end-use demand. In 2025, the State Administration for Market Regulation introduced mandatory standards GB 30981.1-2025 and GB 30981.2-2025, effective June 1, 2026, which impose significantly tighter limits on harmful substances in architectural and industrial coatings. These standards are accelerating the replacement of conventional benzotriazole UV absorbers with low-VOC, high-molecular-weight alternatives, particularly in infrastructure coatings, metal protection systems, and exterior plastics. Compliance pressure is strongest in Tier-1 cities, where enforcement intensity and green procurement mandates are highest.

Parallel regulatory momentum is emerging from China’s recycled plastics framework. Effective February 1, 2026, nine new national standards for recycled plastics will mandate enhanced traceability and performance consistency. This shift is increasing demand for recycling-friendly UV stabilizers that maintain performance through secondary and tertiary processing without generating degradation by-products. Under the Plastic Pollution Control Action Plan, domestic producers such as Suqian Unitechem are expanding production of high-molecular-weight UV absorbers positioned as green functional materials. Industrial policy alignment further extends into electronics. High-purity UV absorbers are now incorporated into the Ministry of Industry and Information Technology 2026 Electronic Chemicals Blueprint, supporting photoresists and optical cleaning agents for the domestic 7 nm semiconductor ecosystem. Investment discipline is also tightening, with new UV absorber capacity in 2025 being directed exclusively into certified Resource Recycling Bases to centralize waste management under the 14th Five-Year Plan. Demand is additionally reinforced by rapid deployment of outdoor 5.5G infrastructure in Shenzhen and Shanghai, where triazine-based UV absorbers are specified for telecom enclosures requiring service lifetimes exceeding ten years.

Germany UV Absorbers Market Defined by POP Phase-Outs and Circular Additive Innovation

Germany’s UV absorbers market is shaped by regulatory leadership and downstream specification rigor, particularly within automotive, construction, and advanced polymer applications. In alignment with the Stockholm Convention, German automotive manufacturers coordinated through the European Automobile Manufacturers’ Association have confirmed that UV-328 will be fully eliminated from all new vehicle components by January 2026 following its classification as a Persistent Organic Pollutant. This phase-out is triggering accelerated adoption of alternative benzotriazole-free and NOR-based UV absorber systems across interior trims, exterior plastics, and under-the-hood components.

Innovation-led substitution is reinforcing this transition. In October 2025, BASF launched Tinuvin NOR 600 at the K2025 trade fair, positioning it as a next-generation NOR-HALS and UV absorber hybrid engineered for high acid resistance in demanding outdoor PVC roofing membranes and artificial turf systems. BASF’s Valeras sustainability platform further underpins market evolution, with its UV absorber portfolio undergoing mass-balance certification audits to enable traceability of bio-attributed carbon content. In parallel, specialty construction demand is expanding. Clariant and Omya showcased AddWorks IBC 760 at the European Coatings Show 2025, demonstrating up to 50% service-life extension in silane-modified polymer sealants exposed to severe weathering. Collectively, Germany functions as a regulatory bellwether and technical benchmark for UV absorber performance in Europe.

South Korea UV Absorbers Market Anchored in Carbon Reduction and Upstream Control

South Korea’s UV absorbers market is increasingly differentiated by sustainability execution and supply-chain self-sufficiency. SONGWON Industrial announced that by 2026 its Ulsan facility will operate using externally supplied zero-emission steam, reducing emissions by an estimated 25,900 tCO2-equivalent annually. This transition materially lowers the product carbon footprint of the SONGSORB UV absorber portfolio, strengthening competitiveness with global brand owners that have embedded carbon intensity thresholds into procurement criteria.

Product innovation is closely tied to circular plastics. At K 2025, Songwon introduced XP2121, an experimental stabilizer developed to enhance UV resistance in low-grade recycled polypropylene. The formulation is designed to enable closed-loop plastic systems without sacrificing outdoor durability. South Korea’s regulatory influence also extends beyond its borders. In 2025, Songwon technology leaders were appointed to chair the European Light Stabilizer and Antioxidant Association, positioning Korean expertise at the center of EU chemical stewardship discussions. Upstream independence further reinforces market resilience, with Songwon completing major investments in di-alkylphenol production in late 2025, securing domestic access to critical intermediates for UV absorber synthesis and insulating operations from global supply volatility.

United States UV Absorbers Market Driven by Construction Demand and Sustainable Polymer Funding

The United States UV absorbers market is increasingly shaped by federal funding initiatives and robust downstream demand from construction, automotive refinish, and personal care applications. In late 2024 and early 2025, the Economic Development Administration recommended $51 million in funding for a Sustainable Polymers Tech Hub in Ohio. The initiative focuses on lifecycle management, advanced recycling, and bio-based UV stabilizers, signaling long-term institutional support for next-generation additive technologies.

Capacity expansion is responding to near-term market pull. BASF and Songwon both announced production increases at their U.S. facilities in Cincinnati and Houston to support rising demand for liquid stabilizers and alkyl polyglucoside-based systems through 2026. The automotive sector remains a key demand anchor. As light trucks gained an additional 3.4% share of U.S. vehicle sales by late 2025, demand has risen for high-solids UV absorber packages in clear-coat systems designed to withstand intense solar exposure in southern and southwestern states. This trend reinforces the importance of high-performance UV absorbers with enhanced weathering resistance and compatibility with low-solvent formulations.

Thailand UV Absorbers Market Positioned as a Southeast Asian Formulation Hub

Thailand is emerging as a strategic formulation and supply hub for UV absorbers serving Southeast Asia’s personal care and home care sectors. In November 2025, BASF inaugurated a major expansion of its surfactant and UV filter operations in Bangpakong, strengthening its regional alkyl polyglucoside and UV stabilizer footprint. The facility is designed to support rising demand for sun care, skin protection, and household formulations across ASEAN markets, where climatic exposure and consumer awareness of UV protection continue to intensify.

The Bangpakong expansion is structurally differentiated by feedstock strategy. The site emphasizes biodegradable surfactants and UV-stabilizing systems derived entirely from renewable raw materials, aligning with tightening environmental standards and multinational brand sustainability targets. This positioning enables Thailand to function as a formulation-centric export base for natural and low-toxicity UV absorber systems, particularly in premium personal care and hygiene applications.

Summary of Country-Level UV Absorbers Market Characteristics

UV Absorbers Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Key Application Focus

|

Strategic Role

|

|

China

|

Coatings regulation and recycled plastics standards

|

Infrastructure coatings, electronics, telecom hardware

|

Policy-driven scale and industrial integration

|

|

Germany

|

POP phase-outs and circular additive certification

|

Automotive, construction polymers, sealants

|

Regulatory and technical benchmark

|

|

South Korea

|

Carbon footprint reduction and upstream control

|

Recycled plastics, high-performance polymers

|

Sustainability-led innovation hub

|

|

United States

|

Federal funding and construction demand

|

Automotive refinish, building materials, personal care

|

Downstream demand and capacity expansion

|

|

Thailand

|

Regional formulation investment

|

Sun care and home care products

|

Southeast Asian production and export hub

|

UV Absorbers Market Report Scope

UV Absorbers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$4.2 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Chemical Class (Benzotriazoles, Triazines, Benzophenones, Oxalanilides, Salicylates), By Application (Plastics, Coatings, Adhesives and Sealants, Personal Care, Renewable Energy, Textiles), By Form (Liquid UV Absorbers, Powder and Crystal Forms, Granules, Masterbatches)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Songwon Industrial Co. Ltd., Clariant AG, SABIC, Solvay SA, Adeka Corporation, Everlight Chemical Industrial Corp., Eastman Chemical Company, Huntsman Corporation, Mitsubishi Chemical Group Corporation, Suqian Unitechem Group, Valtris Specialty Chemicals, Evonik Industries AG, Mayzo Inc., SABO S.p.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

UV Absorbers Market Segmentation

By Chemical Class

- Benzotriazoles

- Triazines

- Benzophenones

- Oxalanilides

- Salicylates

By Application

- Plastics

- Coatings

- Adhesives and Sealants

- Personal Care

- Renewable Energy

- Textiles

By Form

- Liquid UV Absorbers

- Powder and Crystal Forms

- Granules

- Masterbatches

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the UV Absorbers Market

- BASF SE

- Songwon Industrial Co. Ltd.

- Clariant AG

- SABIC

- Solvay SA

- Adeka Corporation

- Everlight Chemical Industrial Corp.

- Eastman Chemical Company

- Huntsman Corporation

- Mitsubishi Chemical Group Corporation

- Suqian Unitechem Group

- Valtris Specialty Chemicals

- Evonik Industries AG

- Mayzo Inc.

- SABO S.p.A.

*- List not Exhaustive