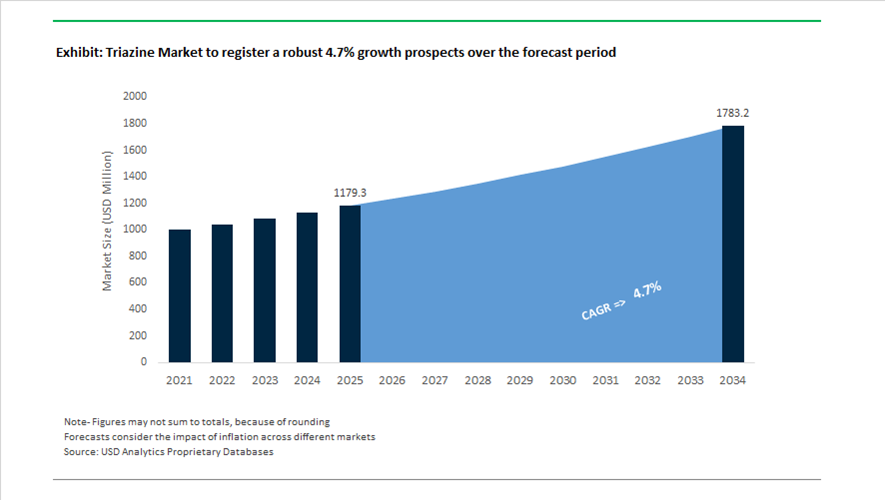

Triazine Market Overview 2025–2034: $1,179.3 Million to $1,783 Million at 4.7% CAGR Supported by H2S Scavengers, Water Treatment Chemistries, and Advanced Coatings Stabilizers

The global Triazine market is valued at $1,179.3 million in 2025 and is projected to reach $1,783 million by 2034, expanding at a CAGR of 4.7%. Triazines are nitrogen-rich heterocyclic compounds widely utilized in H2S scavengers, water treatment chemicals, herbicides, UV light stabilizers, melamine resins, biocides, and specialty polymer additives. Market growth is anchored in rising natural gas processing activity, tighter environmental compliance for water and agrochemical applications, and expanding use of triazine derivatives in high-performance coatings and plastics. The value chain spans upstream amine intermediates through to formulated oilfield scavengers and agricultural herbicide blends, with increasing emphasis on purity, environmental compliance, and performance optimization.

Oilfield and gas treatment applications remain a dominant growth engine. In March 2024, Evonik launched its Octamax catalyst line, engineered to enhance sulfur removal and octane retention in refining processes where triazine-based scavengers are routinely deployed for hydrogen sulfide control. In April 2024, CC Industries completed the acquisition of Foremark Performance Chemicals, a leading supplier of triazine-based H2S scavengers, strengthening its position in refinery and upstream oilfield chemical services. In February 2025, Baker Hughes was selected as a technology provider for the Argent LNG export facility in Louisiana, incorporating large-scale gas treatment systems that rely on triazine derivatives to ensure pipeline-grade natural gas purity. In August 2025, Kao Corporation operationalized its new world-scale tertiary amine and intermediates facility in Pasadena, Texas, expanding North American capacity for surfactant precursors and triazine-based sterilization agents targeting hygiene and energy markets. These developments reflect sustained demand for triazine chemistry in sour gas treatment, LNG infrastructure, and industrial sterilization systems.

Water treatment and agrochemical innovation are simultaneously reshaping regulatory positioning. In October 2024, LANXESS introduced a new portfolio of triazine-based water treatment formulations for industrial cooling towers and municipal systems, emphasizing enhanced microbial control and impurity removal efficiency. In early 2025, major agrochemical manufacturers including Syngenta and Adama launched chemistry-verified triazine herbicide formulations designed to reduce environmental leaching and comply with tightening 2026 regulatory standards. In December 2024, BASF inaugurated a Catalyst & Solids Processing Development Center in Ludwigshafen to optimize intermediates within the triazine value chain, including inputs for melamine resins and specialty herbicides. In February 2026, BASF showcased advanced triazine-derived light stabilizers at Plastindia, highlighting applications in agricultural plastic films where UV protection enhances crop yield durability. Late 2025 also saw the announcement of a proposed consolidation between AkzoNobel and Axalta, signaling procurement realignment for triazine-based UV absorbers and stabilizers used in high-performance automotive and industrial coatings.

Specialty materials and biocidal applications are expanding into adjacent high-value segments. In September 2025, Evonik launched its “Next Markets” strategic program, prioritizing specialty triazine additives for aerospace-grade foams and heat-resistant polymers. In January 2026, Lonza confirmed the successful integration of its Vacaville, California site, leveraging broader chemical platforms that include triazine-based biocides for industrial microbial control.

Triazine Market Trends and Opportunities: Regulatory Phase-Outs, Energy Sector Volatility, and High-Purity Specialty Applications

EU Regulatory Crackdown on Chlorinated Triazine Herbicides Reshaping Agrochemical Demand

The Triazine market is undergoing a structural contraction in Europe, driven by stringent environmental regulations targeting chlorinated triazine herbicides such as terbuthylazine. Under the EU’s “Farm to Fork” strategy and Zero Pollution framework, regulatory authorities are accelerating the phase-out of persistent agrochemicals linked to groundwater contamination and endocrine disruption, fundamentally reshaping demand dynamics across the agrochemical segment.

A key inflection point is the implementation of Commission Implementing Regulation (EU) 2024/989, which entered its active monitoring phase during 2025–2027. This framework enforces stricter Maximum Residue Levels (MRLs) for triazine-based compounds, effectively acting as a precursor to broader usage bans. Simultaneously, Regulation (EU) 2025/1163 has lowered permissible residue thresholds for nitrogen-based heterocycles, compelling manufacturers to transition toward low-persistence, next-generation crop protection chemistries.

Further regulatory tightening is evident in the REACH Programming Document 2026–2028, where ECHA has prioritized persistent and mobile substances. Triazines degrading into metabolites such as trifluoroacetic acid (TFA) face immediate non-renewal risks. This is accelerating the “cliff-edge” scenario for legacy herbicides, forcing agrochemical companies to divest chlorinated triazine portfolios and invest in environmentally compliant alternatives, thereby redefining the European triazine market landscape.

Oil Price Volatility and Green H2S Scavenger Innovation Transforming Energy Sector Demand

The demand profile for triazine-based chemicals in the oil and gas sector is being reshaped by crude oil price volatility and evolving environmental compliance standards, particularly in the application of hydrogen sulfide (H2S) scavengers. While triazines continue to dominate this segment with approximately 55% market share, increasing scrutiny over by-product formation and operational inefficiencies is driving the adoption of low-impact, “green” scavenger chemistries.

Market dynamics in late 2025 highlighted pricing distortions in MEA triazine, particularly in key hubs such as Houston, where oversupply and reduced refinery throughput exerted downward pressure. However, producers leveraging earlier low-cost inventory benefited from margin protection, signaling a shift toward strategic procurement cycles and inventory optimization as core operational strategies in the triazine supply chain.

Despite volatility, upstream investment remains robust. The International Energy Agency (IEA) reported $570 billion in global upstream investment in 2024, with a significant share directed toward high-sulfur (sour) reservoirs. In these environments, triazines remain indispensable due to their high reactivity at low concentrations, particularly in complex basins such as Brazil’s pre-salt and Saudi Arabia’s Jafurah shale. Concurrently, innovations such as Clariant’s SCAVINATOR™ platform are gaining traction by offering reduced solid by-product formation and lower scaling risks, aligning with the industry’s shift toward operational efficiency and environmental compliance.

High-Purity MMA Triazines Gaining Traction in Industrial Water Treatment and Closed-Loop Systems

The transition toward circular industrial water management systems is unlocking significant demand for high-purity triazine derivatives, particularly Monomethylamine (MMA) triazines, used as biocides to control microbial growth and prevent microbial-induced corrosion (MIC). These applications are critical in industries such as power generation, chemicals, and infrastructure, where closed-loop cooling systems require precise microbial control.

By 2026, increased investment in industrial water infrastructure and EU-backed sustainability projects is accelerating the adoption of eco-friendly triazine-based biocides. These formulations offer a balance between broad-spectrum antimicrobial performance and reduced environmental toxicity, positioning them as viable alternatives to conventional inhibitors in municipal and industrial water treatment systems.

Infrastructure expansion is further reinforcing demand. With the global construction sector driving a projected 7.8% CAGR for MMA triazines through 2026, these chemicals are increasingly integrated into concrete and building material treatment systems to prevent microbial degradation and enhance structural longevity. Additionally, the integration of IoT-enabled dosing systems, expected to grow by 10% in 2026, allows real-time monitoring of H2S and microbial levels, reducing overdosing risks and optimizing operational costs by 5% to 10% annually. This convergence of digitalization and specialty chemistry is positioning high-purity triazines as a critical component in next-generation industrial water management.

Non-Halogenated Triazine Flame Retardants Driving Growth in Advanced Polymers and Electronics

A high-growth opportunity in the Triazine market lies in the development of non-halogenated triazine-based flame retardants, which are increasingly replacing traditional brominated systems in response to strict REACH and RoHS regulations. These nitrogen-based additives are gaining traction across engineering thermoplastics, automotive interiors, and electronic components, where fire safety and environmental compliance are critical.

Collaborative innovation is accelerating commercialization. In 2025, BASF SE and THOR GmbH expanded their partnership to develop halogen-free triazine synergists, enabling manufacturers to meet evolving regulatory standards while maintaining high-performance material properties. These solutions are particularly relevant in applications requiring low smoke emission, reduced toxicity, and long-term stability.

Technological advancements are further enhancing product value. Triazine derivatives such as Flamestab® NOR™ 116 offer dual functionality as both flame retardants and UV stabilizers, delivering high thermal stability and low migration characteristics. This makes them ideal for polyolefin applications in automotive, textiles, and films, where durability and aesthetic performance are essential. The broader phosphorus-nitrogen flame retardant segment, growing at approximately 7.5% CAGR, is benefiting from the shift toward intumescent systems, which promote char formation and suppress flame propagation without releasing toxic gases. This positions triazine-based additives as a key enabler of safer, high-performance polymer systems in advanced manufacturing sectors.

Triazine Market Share and Segmentation Insights

Product Type Market Share: MEA Triazine Leads with High-Efficiency H₂S Scavenging in Oil and Gas Operations

MEA triazine holds a dominant 58.60% share in the triazine market in 2025, driven by its superior performance as a hydrogen sulfide scavenger across upstream, midstream, and downstream oil and gas operations. Its fast reaction kinetics, high scavenging capacity, and cost efficiency make it the preferred solution for treating sour gas, crude oil, and produced water streams. Other product types such as MMA triazine, high-purity triazine, bio-based triazine compounds, and asymmetric triazines serve niche or emerging applications. A key market driver is the rise in sour gas production, where increasing H₂S concentrations require higher triazine dosing rates and more advanced multi-stage treatment systems integrated with sulfur recovery processes.

End-Use Industry Market Share: Oil and Gas Sector Dominates with Continuous Chemical Injection Demand

Oil and gas accounts for 68.40% of the triazine market in 2025, reflecting the critical role of triazine-based chemistries in maintaining operational safety, corrosion control, and product quality across hydrocarbon production and processing systems. Continuous injection into pipelines, separators, and processing units drives sustained consumption volumes. Agriculture, water treatment, plastics and polymers, and pharmaceuticals represent secondary application areas with more limited demand. A major growth factor is the intensification of unconventional oil and gas production, where increased souring risks, higher water cuts, and complex reservoir conditions necessitate advanced triazine treatment programs, supporting higher chemical consumption across mature and shale assets.

Triazine Market Competitive Landscape

The triazine market in 2026 is shaped by regulatory-driven resilience and functional diversification, with strong demand for UV absorbers, H₂S scavengers, and low-impurity formulations. Manufacturers are advancing ACV-compliant chemistries, eliminating legacy contaminants, and aligning with EPA and ECHA mandates for sustainable, high-performance triazine applications.

BASF Expands Hydroxyphenyl-Triazine Portfolio with Premium UV Stabilizers and Verbund Integration

BASF leads the triazine market through its Verbund-integrated production of hydroxyphenyl-triazine UV absorbers and performance stabilizers. The launch of Tinuvin® NOR 211 AR enhances durability in agricultural films, extending service life by up to 25% under high UV exposure. The Zhanjiang Verbund ramp-up supports growth in Nutrition & Care and Chemicals, contributing to projected €6.2–€7.0 billion EBITDA in 2026. BASF maintains premium pricing for its low-migration, non-toxic Tinuvin® range, reflecting high R&D intensity. Net debt reduction to €18.3 billion and targeted €2.3 billion cost savings strengthen capital allocation for bio-based triazine intermediates. The company continues advancing high-performance stabilizers aligned with global regulatory standards.

Syngenta Transitions Toward Sustainable Triazine Herbicides and Precision AgTech Integration

Syngenta is reshaping triazine-based crop protection through a strategic pivot toward sustainable herbicides and integrated weed management systems. The planned cessation of Paraquat production by June 2026 marks a shift toward environmentally compliant triazine formulations. Its Cropwise™ platform enables AI-driven precision spraying, reducing atrazine usage by up to 30% while improving field efficiency. Breakthrough herbicide subclasses introduced in 2025 enhance resistance management when used alongside triazines. Strategic collaboration with SALIC supports the development of salt-tolerant crops using triazine-coated seed technologies. Syngenta’s innovation pipeline aligns with global demand for low-toxicity, high-efficacy agrochemicals.

Evonik Accelerates Low-VOC Triazine Crosslinkers for High-Performance Coatings and Electronics

Evonik positions its triazine derivatives as essential crosslinkers and additives for automotive coatings and electronics applications. The 2026 distribution expansion across North America enhances technical support for its high-performance curing agents. Through the "Evonik Tailor Made" restructuring, the company improved operational agility while reducing costs, supporting faster commercialization cycles. Its Custom Solutions segment is prioritizing low-VOC triazine additives for waterborne coatings, aligning with EU environmental regulations. With a projected EBITDA range of €1.7–€2.0 billion, Evonik maintains strong financial resilience. The company continues to innovate in triazine-based epoxy curing systems and advanced material applications.

Chemours Strengthens Specialty Triazine Surfactants with Advanced Performance Materials Focus

Chemours leverages its Advanced Performance Materials segment to scale triazine-based repellents and surfactants for industrial and textile applications. The Capstone™ range delivers compliant, short-chain chemistries with superior oil and water repellency across leather and construction materials. The $360 million Taiwan asset divestment enhances capital flexibility to invest in high-tech triazine intermediates. Chemours projects 2026 EBITDA between $800–$900 million, targeting over 25% free cash flow conversion. Strategic price increases implemented in late 2025 offset feedstock volatility in sulfur and nitrogen inputs. The company is expanding into semiconductor-grade initiators and specialty chemical formulations.

Lonza Advances Pharmaceutical-Grade Triazine Intermediates Through CDMO Expansion and Sustainability Targets

Lonza dominates the pharmaceutical-grade triazine segment, leveraging its CDMO model for high-value intermediates in antiviral and oncology drug development. The integration of its Vacaville site supports projected 11–12% sales growth and CORE EBITDA margins above 32% in 2026. Portfolio realignment, including the exit of its CHI business, sharpens focus on specialized modalities using triazine scaffolds. Lonza is implementing energy-efficient catalytic synthesis routes to reduce emissions, targeting a 42% reduction in Scope 1 and 2 GHG emissions by 2030. Its regional supply strategy enhances resilience against trade disruptions. The company continues to scale high-purity triazine production for advanced life science applications.

United States Triazine Market Anchored in Shale Optimization and Infrastructure Durability

The United States triazine market in 2025–2026 is being reshaped by shale-specific operational requirements and a renewed cycle of public infrastructure investment. Rising liquid fuel consumption has accelerated the adoption of modular, continuous-flow triazine production units across the Permian Basin, replacing solvent-intensive batch systems. These next-generation units deliver approximately 30% lower solvent consumption, directly improving operating economics for gas sweetening applications. At the same time, stricter EPA sulfur regulations have lowered permissible H₂S thresholds in selected pipelines to below 4 ppm, forcing operators to deploy triazine-doped glycols capable of simultaneously dehydrating and sweetening gas streams. This dual-functionality has become a decisive procurement criterion for upstream operators managing higher-sulfur shale output.

Beyond oil and gas, federal and state-level construction spending has materially expanded the non-energy demand base. Large-scale public infrastructure projects are driving consumption of triazine-based corrosion inhibitors and wood adhesives designed for long-term structural integrity under variable climatic exposure. Innovation is reinforcing this trend. Advanced triazine-type UV stabilizers introduced in 2025 are extending the service life of polyamide components used in automotive and heavy machinery. Parallel field trials in the Bakken shale demonstrated that nanoparticle-functionalized triazine scavengers outperform conventional MEA triazine by roughly 40% in longevity, highlighting a shift toward performance-engineered scavenging systems rather than volume-driven chemical dosing.

China Triazine Market Shaped by Self-Sufficiency and UV Absorber Scale

China’s triazine market is increasingly defined by self-reliance policies and scale-driven leadership in downstream applications. Escalating trade tensions during 2025 and retaliatory tariff increases on selected U.S. chemical imports have accelerated domestic investment in high-purity triazine intermediates. This push is particularly visible in agrochemicals and electronic materials, where uninterrupted access to triazine derivatives is now treated as a strategic priority. Refinery modernization under the MIIT 2026 blueprint has further strengthened domestic consumption, with AI-driven dosing systems in Zhejiang sour-gas processing hubs reducing chemical waste by approximately 15% while stabilizing H₂S removal efficiency.

Export controls have also influenced market direction. The designation of additional U.S. entities under China’s Export Control List in April 2025 constrained access to certain dual-use triazine precursors, prompting local suppliers to accelerate indigenous synthesis pathways. At the same time, China continues to dominate global production of monomeric triazine UV absorbers. Capacity expansions completed in 2025 are targeting agricultural films and flexible packaging, reinforcing China’s role as the primary global supplier for UV-stabilized polymer applications despite rising regulatory scrutiny in export markets.

Germany Triazine Market Driven by Sustainability and Precision Formulation

Germany’s triazine market reflects the intersection of sustainability mandates and advanced formulation science. In response to EU-wide environmental requirements introduced in 2025, German producers are transitioning toward bio-based aldehydes as feedstocks for next-generation “green triazine” variants. These formulations are engineered to deliver comparable scavenging and stabilization performance while exhibiting lower aquatic toxicity profiles, aligning with tightening environmental risk assessments across Europe.

Construction remains a key demand pillar. Germany continues to be the leading European market for triazine-based stabilizers used in external infrastructure, where long-term UV resistance is critical for façades, coatings, and composite materials. On the technology front, neural-network-driven process control has emerged as a competitive differentiator. Advanced digital platforms deployed in 2025 allow producers to tailor MEA triazine formulations to specific crude and gas compositions, minimizing over-dosing and reducing the formation of insoluble dithiazine deposits that can impair pipeline integrity.

India Triazine Market Supported by Refinery Upgrades and Agrochemical Exports

India’s triazine market is expanding on the back of refinery modernization and export-oriented agrochemical manufacturing. Large-scale refinery upgrades undertaken in 2025 to process higher-sulfur crude have driven an estimated 12% year-on-year increase in domestic procurement of MEA triazine scavengers. These chemicals are now central to meeting stricter sulfur specifications for fuels while maintaining throughput efficiency across upgraded distillation and hydrotreating units.

In parallel, India’s agrochemical sector is leveraging triazine chemistry to support export growth. Domestic producers have increased output of next-generation triazine herbicides positioned as safer alternatives to legacy atrazine and simazine, ensuring compliance with stringent international residue and toxicity standards introduced in 2025. This dual demand from energy and agriculture positions India as both a consumption and formulation hub within the global triazine value chain.

Saudi Arabia Triazine Market Enabled by Mega-Projects and Localization

Saudi Arabia’s triazine market is closely tied to upstream mega-projects and localization strategies. Large-scale developments in the Jafurah shale gas field and continued expansion at Ghawar have integrated triazine scavengers with sensor-based analytics for real-time H₂S removal. This digital integration improves operational safety while reducing chemical wastage, making triazine-based systems a core component of sour-gas management.

Trade realignments in 2025 have further enhanced the Kingdom’s attractiveness as a production base. Chemical manufacturers are increasingly shifting triazine synthesis to Saudi Arabia to bypass U.S.–China tariff volatility, leveraging competitively priced feedstocks such as formaldehyde. These localization initiatives support Saudi Arabia’s broader industrial diversification agenda while embedding triazine chemistry deeper into its energy and materials ecosystem.

Comparative Snapshot: Triazine Market by Country

Triazine Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Lever

|

Market Positioning

|

|

United States

|

Shale gas sweetening, infrastructure

|

Continuous-flow units, EPA sulfur limits

|

Performance-driven, innovation-led

|

|

China

|

Agrochemicals, UV absorbers

|

Self-sufficiency, AI dosing

|

Scale leadership with export focus

|

|

Germany

|

Construction, sustainable chemistry

|

Bio-based feedstocks, neural control

|

High-value, regulation-aligned

|

|

India

|

Refining upgrades, agro exports

|

Sulfur processing, safer herbicides

|

Dual energy–agro demand hub

|

|

Saudi Arabia

|

Sour gas mega-projects

|

Localization, sensor integration

|

Feedstock-advantaged growth market

|

Triazine Market Report Scope

Triazine Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1179.3 Million

|

|

Market Size (2034)

|

$1783 Million

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Product Type (MEA Triazine, MMA Triazine, High-Purity Triazine, Asymmetric Triazines, Bio-Based Triazine Compounds), By Form (Water-Soluble Triazine, Oil-Soluble Triazine, Gas-Phase Triazine), By Functionality (H2S Scavengers, UV Stabilizers, Biocides and Antimicrobials, Agrochemical Intermediates, Corrosion Inhibitors), By End-Use Industry (Oil and Gas, Agriculture, Plastics and Polymers, Water Treatment, Pharmaceuticals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hexion Inc., Eastman Chemical Company, BASF SE, Baker Hughes Company, Dow Inc., Sintez OKA, Evonik Industries AG, Ecolab Inc., Stepan Company, Lonza Group Ltd., Halliburton Company, Foremark Performance Chemicals, Ashland Inc., Haihang Industry Co. Ltd., Clariant AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Triazine Market Segmentation

By Product Type

- MEA Triazine

- MMA Triazine

- High-Purity Triazine

- Asymmetric Triazines

- Bio-Based Triazine Compounds

By Form

- Water-Soluble Triazine

- Oil-Soluble Triazine

- Gas-Phase Triazine

By Functionality

By End-Use Industry

- Oil and Gas

- Agriculture

- Plastics and Polymers

- Water Treatment

- Pharmaceuticals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Triazine Market

- Hexion Inc.

- Eastman Chemical Company

- BASF SE

- Baker Hughes Company

- Dow Inc.

- Sintez OKA

- Evonik Industries AG

- Ecolab Inc.

- Stepan Company

- Lonza Group Ltd.

- Halliburton Company

- Foremark Performance Chemicals

- Ashland Inc.

- Haihang Industry Co. Ltd.

- Clariant AG

*- List not Exhaustive