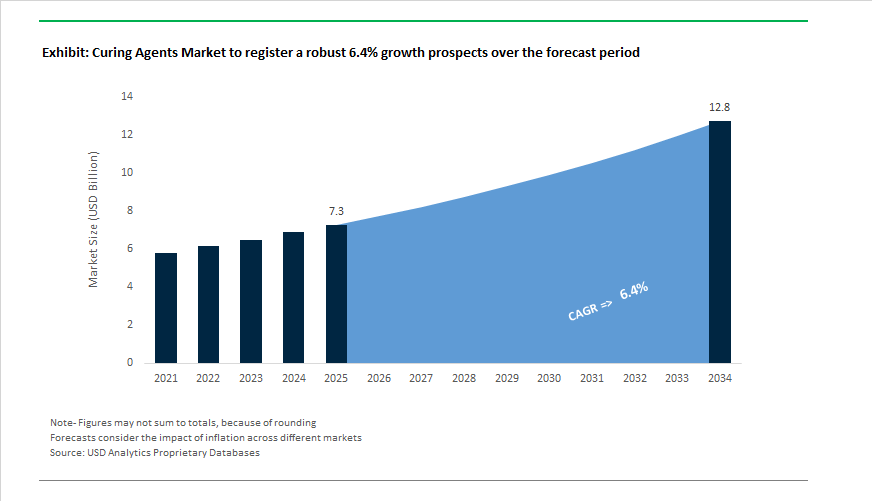

Curing Agents Market to Reach $12.8 Billion by 2034 at 6.4% CAGR Driven by Sustainable Epoxy and Polyurethane Hardener Innovation

The Curing Agents Market is projected to expand from $7.3 billion in 2025 to $12.8 billion by 2034, registering a CAGR of 6.4%. Growth is anchored in accelerating demand for high-performance epoxy curing agents, polyurethane hardeners, phenalkamide curing systems, and peroxide crosslinkers across automotive lightweighting, wind energy composites, construction chemicals, electronics encapsulation, and marine protective coatings. Sustainability mandates, carbon footprint transparency, and recyclability requirements are reshaping R&D investment priorities across global producers.

A structural shift in competitive dynamics emerged in November 2024, when Evonik broke ground on a major specialty amines expansion in Nanjing, China, aimed at strengthening the Asia-Pacific supply of epoxy curing agents used in wind turbine blades and infrastructure adhesives. In October 2024, Atul Ltd. added 50,000 tons per annum to its epoxy resin and curing agent capacity in India, targeting domestic growth in civil engineering and industrial coatings. Innovation in performance chemistry accelerated in April 2024, when Evonik introduced Ancamine® 2844, an ultra-fast epoxy hardener engineered for plural-component spray systems, reducing return-to-service times in aggressive environments. The same year, Cardolite launched LITE 3070, a bio-based phenalkamide curing agent derived from cashew nut shell liquid, offering fast cure combined with extended pot life for marine and heavy-duty coatings.

Bio-circular and recyclable composite technologies gained visibility in March 2025, when Westlake Epoxy introduced its EpoVIVE™ portfolio at JEC World 2025, including the EPIKURE™ 6874-WZ-50 curing agent formulated with bio-circular feedstocks to reduce product carbon footprint in aerospace and automotive composites. Westlake further showcased recyclable rotor blade technology the same month, utilizing a specialized curing system that enables fiber-matrix separation at end-of-life, addressing wind energy blade disposal challenges. Sustainability transformation intensified in July 2025, when Evonik confirmed that its epoxy curing agent plants transitioned to 100% renewable electricity, directly lowering Scope 1 and 2 emissions for its Crosslinkers business line. Regulatory-driven process innovation was evident in October 2025, when Arkema unveiled Luperox® NeatCure® at K 2025, a dust-free organic peroxide granule improving worker safety and curing efficiency in elastomer processing. Corporate portfolio realignment continued in December 2025, as BASF signed an agreement to divest its optical brightening agent business to Catexel, sharpening focus on advanced chemical intermediates and curing technologies, with closure expected in Q1 2026.

Industry consolidation and cost volatility are redefining capital allocation strategies. In January 2026, ADNOC’s XRG finalized regulatory approval for the acquisition of Covestro, including a €1.17 billion capital increase to accelerate polyurethane and epoxy curing agent R&D aligned with circular economy objectives. This transaction reinforces long-term investment into advanced crosslinkers for mobility and electronics through 2026 and beyond. In February 2026, Wacker Chemie announced price increases of up to 25% for addition-curing silicone systems and crosslinkers, citing platinum catalyst price escalation after an 18-month surge in precious metal markets. Meanwhile, Olin Corporation intensified restructuring across 2025–2026, prioritizing Electrochemical Unit margins and optimizing its Blue Cube Operations epoxy segment toward high-value vertical integration following legal and market pressures. These developments reflect a curing agents market increasingly defined by renewable feedstocks, recyclable composite systems, platinum-driven cost dynamics, regional capacity expansion in Asia, and consolidation-led R&D acceleration across epoxy hardeners, amine curing agents, silicone crosslinkers, and peroxide-based curing chemistries.

Emerging Trends and High-Growth Opportunities Reshaping the Curing Agents Market

Wind Energy Expansion and Offshore Installations Accelerating Demand for High-Performance Epoxy Curing Agents

The global wind energy expansion is emerging as a primary structural growth driver for the curing agents market, particularly in epoxy-based composite systems used in turbine blades. According to the International Energy Agency Renewables 2025 report, global wind power capacity is projected to nearly double to over 2,000 GW by 2030, creating sustained demand for high-performance amine and anhydride curing agents that ensure structural integrity, fatigue resistance, and long service life. Rotor blade manufacturing alone currently consumes approximately 24,162 tonnes of epoxy resin systems annually, underscoring the scale of opportunity for advanced thermoset curing technologies. In September 2025, Vestas announced commercial scaling of a breakthrough chemical recycling process developed with Olin and Aarhus University, enabling recovery of epoxy resin components from decommissioned blades without redesigning blade architecture, thereby introducing circularity into thermoset composite supply chains.

Offshore wind development is further intensifying technical requirements for specialty curing agents. The IEA projects annual offshore wind additions to quadruple to 37 GW per year by 2030, shifting deployment toward harsh marine environments characterized by high humidity, salt exposure, and sub-10°C staging conditions. This has accelerated adoption of phenalkamine curing agents known for superior corrosion resistance, rapid cure in damp conditions, and enhanced adhesion performance in offshore blade and coating applications. As renewable energy investments scale globally, epoxy curing agents tailored for offshore composites, corrosion protection, and long-term durability are expected to represent a high-value growth segment within the global curing agents market.

Regulatory Restrictions on Formaldehyde, Hazardous Amines, and BPA Driving the Transition to Low-VOC and Safer Hardener Systems

Regulatory pressure from global chemical agencies is triggering a fundamental reformulation cycle across the curing agents industry. Under REACH Regulation EU 2023/1464, the European Chemicals Agency released updated guidance in April 2025 restricting formaldehyde emissions, mandating that from August 6, 2026, articles placed on the EU market must not exceed emission limits of 0.062 mg/m³ for furniture and 0.080 mg/m³ for other products. These thresholds directly affect formaldehyde-based curing agents used in wood composites, construction panels, and interior coatings. Entry 77 of REACH further tightens limits for vehicle interiors effective August 2027, requiring OEM components to meet the 0.062 mg/m³ standard, accelerating the automotive sector’s transition toward low-VOC waterborne curing agents and formaldehyde-free amine hardener systems.

Parallel to emission controls, public health scrutiny surrounding Bisphenol A is reshaping epoxy curing agent portfolios. BPA-free epoxy systems are projected to increase market share by 25% by late 2026, driven by regulatory compliance and consumer safety initiatives. Leading manufacturers such as Evonik and Huntsman are commercializing modified polyetheramines that replicate the mechanical strength and chemical resistance of traditional systems while mitigating endocrine-disruption risks. This regulatory-driven shift toward safer, low-emission, and BPA-free curing agents is redefining competitive positioning across automotive, construction, and industrial coatings segments.

Bio-Based and Renewable Curing Agents Unlocking Sustainable Growth Pathways

The transition from fossil-based raw materials to renewable feedstocks is evolving from pilot-scale experimentation to industrial-scale implementation within the curing agents market. In July 2025, Evonik announced that all its global epoxy curing agent production sites across Germany, the United States, and Singapore now operate on 100% renewable electricity, a move projected to reduce Scope 1 and 2 emissions of its curing agent portfolio by 30% annually. Such decarbonization strategies directly align with corporate net-zero targets and increase demand for low-carbon epoxy hardener systems across infrastructure and marine applications.

Bio-based chemistries are gaining measurable commercial traction. Cardolite Corporation has expanded production of phenalkamines derived from Cashew Nut Shell Liquid, a non-food chain byproduct, offering 60 to 80% bio-content while delivering superior damp-surface adhesion in heavy-duty marine coatings. Simultaneously, major chemical producers are targeting a 25 to 40% reduction in product-related carbon footprints by 2030, catalyzing growth in dimer acid-based polyamide curing agents derived from plant-based fatty acids. These renewable hardener systems are increasingly adopted in flexible, high-impact resistant coatings and corrosion protection applications, positioning bio-based curing agents as a structurally expanding segment within the global curing agents market.

Low-Temperature and Fast-Cure Technologies Enabling Energy Efficiency and High-Speed Manufacturing

Energy efficiency and industrial productivity imperatives are driving rapid adoption of low-temperature and snap-cure curing agent technologies. In late 2024, Hexcel introduced its HexPly M77 snap-cure system, achieving full composite cure in just two minutes at 150°C, enabling automotive OEMs to synchronize carbon-fiber reinforced EV chassis production with high-speed assembly line takt times. Such fast-cure epoxy systems significantly enhance throughput while reducing thermal cycle duration, a critical advantage for mass production of lightweight electric vehicle components.

Shifting from conventional 180°C high-heat ovens to ambient or sub-100°C curing systems can reduce facility energy consumption by up to 40%, directly supporting industrial Net Zero targets. In response, Huntsman International LLC launched new latent accelerators in 2025 that initiate rapid cross-linking at lower thermal thresholds without compromising resin shelf life. Additionally, as the semiconductor packaging market is projected to exceed $26 billion in 2025, demand for low-temperature amine-adduct curing agents capable of operating below 150°C is rising to protect thermally sensitive electronics during potting and encapsulation. These energy-efficient, high-productivity curing technologies are poised to capture significant share across automotive composites, electronics encapsulation, and industrial coatings applications.

Curing Agents Market Share and Segmentation Insights

Curing Mechanism Segmentation: Ambient Temperature Systems Lead Adoption as UV Technologies Accelerate Processing

Ambient temperature curing agents account for 42% of market share in 2025, driven by widespread use of amines, polyamides, and mercaptans in field-applied coatings, construction adhesives, marine maintenance, and civil engineering projects. Their ability to cure without external heat delivers major energy savings and operational flexibility, making them indispensable for on-site applications. Elevated temperature curing agents form a high-performance segment, dominated by anhydrides, phenolic resins, and dicyandiamide, enabling superior thermal stability and chemical resistance in automotive OEM coatings, powder coatings, aerospace composites, and electrical laminates where oven curing is standard. UV curing systems represent one of the fastest-growing categories, utilizing photoinitiators to achieve instant cure in electronics, optical fiber coatings, 3D printing, and high-speed printing lines. Moisture curing agents, including isocyanate prepolymers and silane-modified polymers, support one-component adhesives and sealants, valued for simplicity despite limitations in deep-section curing.

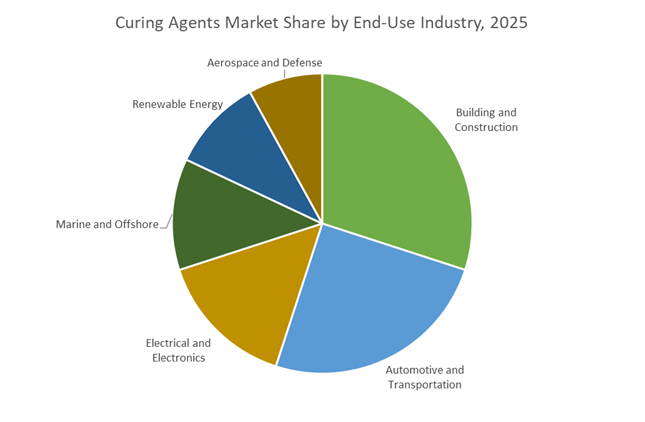

End-Use Industry Distribution: Construction Anchors Volume While Electronics and Renewables Drive Performance Demand

Building and construction leads curing agent consumption with 30% market share, fueled by demand for concrete repair materials, industrial flooring, structural adhesives, and protective coatings, where ambient-curing chemistries enable efficient on-site application. Automotive and transportation represent a significant segment, combining elevated-temperature curing for OEM production with ambient systems for refinish and repair operations. Electrical and electronics applications require ultra-high-purity curing agents for printed circuit boards, encapsulation compounds, and conductive adhesives, favoring thermal and UV curing for precision and void-free performance. Marine and offshore rely heavily on ambient-curing epoxy systems for corrosion protection in saltwater environments. Renewable energy is expanding rapidly, driven by epoxy composites in wind turbine blades and encapsulation materials for solar modules. Aerospace and defense demand elevated-temperature curing under strict quality control for carbon fiber composites and flight-critical structural components.

Competitive Landscape of the Curing Agents Market

The Curing Agents Market is highly competitive, driven by regulatory reformulation, bio-based chemistry adoption, and surging demand from protective coatings, composites, EV batteries, and electronics, with leading players competing on specialty amines, vertical integration, and regional manufacturing scale.

Evonik leads specialty amine curing agents with regulatory-ready innovation

Evonik Industries AG commands a strong global position through its Ancamine® and Ancamide® portfolios, serving industrial flooring, marine coatings, and protective applications. In 2024–2025, Evonik introduced Ancamine® 2880 and bio-based Ancamide® 2853/2865 as nonylphenol-free, low-VOC alternatives tailored for Europe and the Americas. Its strategic focus on “Regulatory Leadership” is accelerating the transition toward SVHC-free and CMR-free amine curing agents ahead of 2027 compliance deadlines. A major differentiator is Evonik’s global technical service network, which now offers digital Formulation Toolkits to simulate cure profiles. High-moisture-tolerance amidoamines further reinforce its dominance in marine and industrial coating systems.

Huntsman strengthens aerospace and EV composites with Aradur® curing systems

Huntsman Corporation remains a powerhouse in high-performance epoxy curing through its Aradur® ecosystem, with growing traction in aerospace, defense, and automotive lightweighting. In early 2026, the company intensified its focus on structural composites, where curing agents play a critical role in extending component life while reducing weight. Huntsman is also integrating its 2025 polyurethane elastomer upgrades to deliver hybrid curing solutions that blend polyurethane toughness with epoxy chemical resistance. A major strategic milestone came in 2026 with multi-year supply agreements with EV OEMs for low-viscosity encapsulants used in battery management systems. Deep vertical integration across epoxy and MDI-based foams supports holistic building and construction material solutions.

Westlake Epoxy advances sustainable curing with EpoVIVE™ and digital logistics

Westlake Epoxy has repositioned itself around sustainable, surplus-value curing technologies following its separation from Hexion. Its EpoVIVE™ portfolio, launched during 2025–2026, delivers lower environmental impact while preserving the performance of the established EPIKURE™ range. The company controls iconic EPON™, EPIKOTE™, and EPIKURE™ brands, which remain benchmarks in civil engineering and wind energy. In February 2026, Westlake expanded its Brenntag distribution partnership into India, targeting South Asia’s 6.5% CAGR infrastructure growth. Strategically, Westlake is deploying AI-driven inventory systems to stabilize specialty amine supply chains, reducing exposure to feedstock volatility such as benzylamine.

Olin anchors epoxy curing with unmatched backward integration

Olin Corporation plays a pivotal role in the curing agents ecosystem through unrivaled backward integration, producing both epichlorohydrin and caustic soda required for epoxy resin systems. This structural advantage insulates its curing agent portfolio from upstream price shocks. In late 2025, Olin advanced its Strategic Plan Implementation, prioritizing high-purity cycloaliphatic amines for electronics applications. By 2026, Olin ranked among the top three anchors in the $1.4 billion US epoxy curing agent market, with strong exposure to infrastructure repair and seismic retrofitting. Its “Essential Solutions” strategy positions Olin hardeners as foundational materials for large-scale bridge rehabilitation and roadway protection programs.

Cardolite accelerates bio-based curing chemistry with CNSL technology

Cardolite Corporation leads the global transition toward sustainable curing agents through its proprietary CNSL-based Phenalkamines and Phenalkamides. These inherently bio-based materials deliver unique wet-surface curing, ideal for corrosion protection and zinc-rich primers. During 2025–2026, Cardolite introduced the Ultra LITE series, enabling light-colored, aesthetic coatings using renewable chemistry for the first time. Its NX-series waterborne curing agents are co-solvent-free and optimized for zero-VOC applications. Strategically branded as “Chemistry for Tomorrow,” Cardolite is capitalizing on the rapid adoption of lignin- and CNSL-derived hardeners, a trend projected to add approximately 0.7% to overall curing agents market CAGR through sustainability-driven demand.

Kukdo dominates Asia-Pacific composites and electronics encapsulation

Kukdo Chemical is a major force in Asia-Pacific, a region accounting for 44.7% of global curing agent revenue in 2026. The company’s manufacturing efficiency and scale make it a primary supplier to the global wind energy sector, particularly for turbine blade composites in China and Europe. Kukdo also leads PCB encapsulation, delivering ultra-low-viscosity hardeners capable of filling microscopic voids in high-density electronics. Expanded operations across Southeast Asia in 2025 strengthened support for regional automotive and consumer electronics growth. Its strategic emphasis on high-performance composites includes developing next-generation thermal-management curing agents tailored for 5G infrastructure and advanced electronics hubs.

China: Policy-Orchestrated Shift Toward High-End, Self-Sufficient Curing Chemistries

China’s curing agents industry is being reshaped by a tightly coordinated industrial policy framework that prioritizes quality, self-sufficiency, and intelligent manufacturing. The Petrochemical Steady Growth Plan (2025–2026), jointly released by the Ministry of Industry and Information Technology and six central agencies in September 2025, sets a clear trajectory of achieving more than 5% annual growth in sectoral added value while structurally upgrading the product mix. Within this roadmap, specialty curing agents and crosslinkers are explicitly highlighted as strategic materials. The objective is to lift domestic self-sufficiency in high-end curing systems such as electronic-grade amines, carbodiimides, and aziridines beyond 90 %, reducing exposure to imported formulations used in semiconductors, aerospace composites, and renewable energy systems.

Execution is increasingly technology-led. Under the 2025 AI + Petrochemicals initiative, curing agent producers are integrating AI-driven process controls, automated hazard detection, and blockchain-enabled traceability for isocyanate and amine value chains. These systems directly support China’s dual-carbon goals by lowering incident risk, improving batch consistency, and enabling auditable low-emission production. Demand-side pull is strongest from the New Energy Vehicle ecosystem. Throughout 2025, capital flowed into low-viscosity, fast-curing modified amines and thermally conductive curing systems for EV battery modules, potting compounds, and structural adhesives. At the September 2025 Adhesive and Sealant Expo in Shanghai, domestic suppliers showcased SVHC-free curing agents designed for wind energy, aerospace, and advanced electronics, signaling a clear pivot toward green manufacturing credentials. Complementing this shift, Q4 2025 capacity controls on traditional refining effectively redirected investment toward high-value curing chemistries rather than volume-driven commodity output.

United States: Defense, Sustainability, and Regulatory-Driven Reformulation

The U.S. curing agents landscape in 2025 is defined by defense-linked demand, sustainability-led portfolio repositioning, and regulatory pressure on legacy chemistries. A notable demand catalyst emerged in February 2025 when Olin Corporation broke ground on a new 6.8 mm ammunition facility at the Lake City Army Ammunition Plant. This investment has driven specialized requirements for military-grade epoxy curing systems that deliver high thermal stability, controlled crosslink density, and long-term durability under extreme service conditions.

On the sustainability front, U.S. producers are accelerating bio-circular and low-toxicity transitions. Westlake Epoxy introduced its EpoVIVE™ portfolio in early 2025, leveraging ISCC PLUS mass-balance raw materials to reduce Scope 3 emissions while maintaining performance parity with fossil-based curing agents. In parallel, Huntsman Corporation rolled out a reformulated ARALDITE® range across the U.S. and Europe in September 2025, eliminating intentionally added BPA and CMR-classified substances. Regulatory dynamics reinforce this direction. Updated FDA food-contact standards and evolving state-level Clean Air Act requirements have accelerated adoption of low-VOC, waterborne epoxy dispersions, while the EPA’s continued TSCA risk evaluation of legacy amine hardeners is pushing formulators toward salicylic-acid-free and future-proof EHS profiles.

India: Localization, Infrastructure Demand, and Low-Emission Adoption

India’s curing agents industry is progressing along a localization and infrastructure-led growth path. The realization of PLI Scheme 2.0 investments exceeding ₹4,763 crore by September 2025 has materially strengthened domestic production of key starting materials and intermediates used in amine synthesis. According to the Ministry of Chemicals and Fertilizers, India reduced reliance on imports by domestically manufacturing 191 new APIs and intermediates by December 2025, several of which feed directly into specialized curing catalyst and hardener systems.

Demand expansion is closely tied to grid and construction modernization. Budget allocations for 2025–2026 have accelerated deployment of silane-grafted XLPE and epoxy-based potting compounds in high-voltage transmission equipment, substations, and renewable integration projects. At the same time, sustainability considerations are shaping formulation choices. Large-scale industrial flooring and infrastructure projects in 2025 began adopting low-emission amine building blocks, including Baxxodur® EC 151, which delivers up to 90% lower VOC emissions while maintaining rapid cure performance. This combination of domestic chemical self-sufficiency, power infrastructure build-out, and environmental performance requirements is positioning India as a fast-evolving market for modern curing agents rather than a volume-driven importer.

Germany: Bio-Based Acceleration and Regulatory-Led Portfolio Focus

Germany remains at the forefront of curing agent innovation, driven by bio-based chemistry, regulatory rigor, and portfolio optimization. In March 2025, BASF SE and Sika jointly commercialized Baxxodur® EC 151, a next-generation amine building block that reduces epoxy curing time by two-thirds at low temperatures of 5 to 10°C. This innovation directly addresses European construction and infrastructure needs where cold-weather application performance is critical.

Structural restructuring is also shaping the competitive landscape. LANXESS is executing its FORWARD! program through 2025–2026, targeting €150 million in permanent annual savings and refocusing on high-purity uretdione crosslinkers and aqueous curing agents for automotive OEMs. Regulatory pressure reinforces this specialization. The January 2025 SVHC update issued by the European Chemicals Agency tightened documentation and compliance requirements for amine derivatives, accelerating market adoption of improved EHS-profile products such as the Ancamine® series. Collectively, Germany’s curing agents industry is consolidating around high-performance, compliant, and bio-attributed solutions aligned with EU sustainability and safety frameworks.

Snapshot Summary: Strategic Direction by Country

Curing Agents Market County Level Snapshot

|

Country

|

Core Strategic Driver

|

Priority Curing Agent Focus

|

Structural Direction

|

|

China

|

Industrial policy and self-sufficiency

|

Specialty amines, carbodiimides, EV adhesives

|

Shift from bulk output to high-end derivatives

|

|

United States

|

Defense demand and EHS reformulation

|

Military-grade epoxies, bio-circular hardeners

|

Sustainability-led portfolio transition

|

|

India

|

Localization and grid expansion

|

Low-VOC amines, XLPE curing systems

|

Import substitution with infrastructure pull

|

|

Germany

|

Bio-based innovation and REACH pressure

|

Fast-cure amines, uretdione crosslinkers

|

High-purity, compliant specialization

|

Curing Agents Market Report Scope

Curing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.3 Billion

|

|

Market Size (2034)

|

$12.8 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Type (Amine-Based, Anhydride-Based, Isocyanate-Based, Others), By Curing Mechanism (Ambient Temperature Curing, Elevated Temperature Curing, UV Curing, Moisture Curing), By Application (Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, Civil Engineering), By End-Use Industry (Automotive and Transportation, Building and Construction, Marine and Offshore, Aerospace and Defense, Electrical and Electronics, Renewable Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries AG, Olin Corporation, Huntsman Corporation, Westlake Corporation, BASF SE, Kukdo Chemical Co., Ltd., Wanhua Chemical Group Co., Ltd., Mitsubishi Chemical Group Corporation, Aditya Birla Chemicals, Atul Ltd., Gabriel Performance Products, Nippon Carbide Industries Co., Inc., Arkema S.A., Covestro AG, Hexion Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Curing Agents Market Segmentation

By Type

- Amine-Based

- Aliphatic Amines

- Cycloaliphatic Amines

- Aromatic Amines

- Anhydride-Based

- Isocyanate-Based

- Others

By Curing Mechanism

- Ambient Temperature Curing

- Elevated Temperature Curing

- UV Curing

- Moisture Curing

By Application

- Coatings

- Adhesives and Sealants

- Composites

- Electrical and Electronics

- Civil Engineering

By End-Use Industry

- Automotive and Transportation

- Building and Construction

- Marine and Offshore

- Aerospace and Defense

- Electrical and Electronics

- Renewable Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Curing Agents Industry

- Evonik Industries AG

- Olin Corporation

- Huntsman Corporation

- Westlake Corporation

- BASF SE

- Kukdo Chemical Co., Ltd.

- Wanhua Chemical Group Co., Ltd.

- Mitsubishi Chemical Group Corporation

- Aditya Birla Chemicals

- Atul Ltd.

- Gabriel Performance Products

- Nippon Carbide Industries Co., Inc.

- Arkema S.A.

- Covestro AG

- Hexion Inc.

*- List not Exhaustive