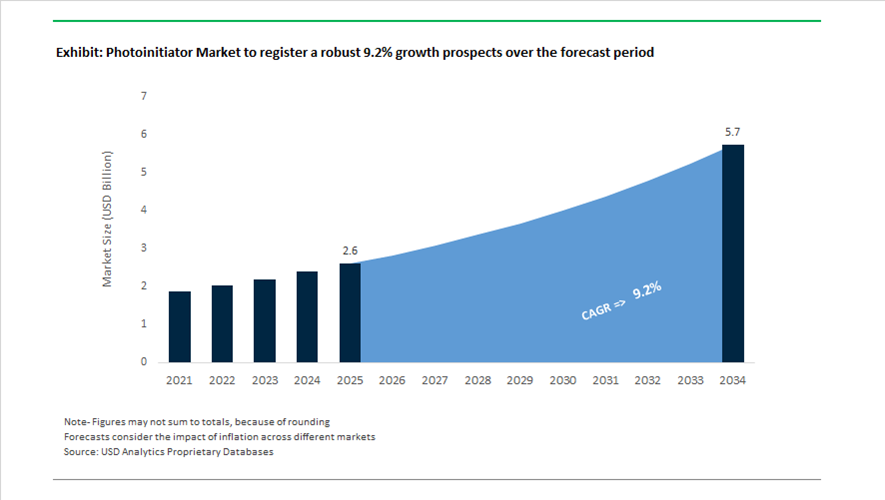

Photoinitiator Market Size 2025–2034: $2.6 Billion to $5.7 Billion at 9.2% CAGR Fueled by UV-LED Curing, EUV Lithography, and TPO-Free Reformulations

The global photoinitiator market is projected to grow from $2.6 billion in 2025 to $5.7 billion by 2034, registering a strong CAGR of 9.2%. Market expansion is driven by accelerating adoption of UV/EB curing technologies in printing inks, industrial coatings, 3D printing resins, adhesives, and advanced semiconductor photoresists. Photoinitiators, including radical and cationic systems such as phosphine oxides, benzophenone derivatives, and onium salts, remain indispensable in energy-curing formulations that deliver rapid polymerization, low VOC emissions, and high surface durability. Increasing regulatory scrutiny, intellectual property enforcement, and transition toward UV-LED curing systems are redefining product portfolios across global suppliers.

Regulatory changes in 2025 significantly reshaped product development strategies in the photoinitiator industry. In September 2025, the EU reclassification of TPO (Trimethylbenzoyl Diphenylphosphine Oxide) under Regulation 2024/197 became effective, moving it to Reprotoxic Category 1B. This stricter classification triggered immediate reformulation across European inks, adhesives, and coatings markets. Major manufacturers launched TPO-free photoinitiator alternatives to maintain compliance in food packaging, industrial printing, and medical device coatings. This regulatory shift accelerated R&D investment in safer phosphine oxide derivatives and alternative radical photoinitiator chemistries.

Intellectual property protection and distribution realignment further intensified competitive positioning. In January 2024, iGM Resins initiated patent enforcement actions to protect Omnirad 819 technology in radical polymerization systems, highlighting the high strategic value of patented photoinitiators for automotive coatings and industrial applications. In December 2025, iGM Resins formed an exclusive distribution alliance with IDCC Global Chem for the Indian subcontinent, effective January 1, 2026, covering Omnirad®, Esacure®, and Omnipol® brands. This move strengthens market penetration in South Asia’s fast-growing UV-curable printing inks and packaging coatings segment.

Semiconductor innovation is emerging as a high-value demand catalyst. In late 2025, advanced EUV photoinitiators and photoresists were validated by leading material providers for High-NA EUV lithography systems deployed in early 2nm logic node production. These chemistries support next-generation chip manufacturing requiring ultra-precise photopolymerization at nanoscale dimensions. The transition toward advanced lithography nodes significantly increases demand for ultra-high-purity, high-sensitivity photoinitiator molecules compatible with ASML’s TWINSCAN EXE:5000 platforms.

Sustainability and circular raw materials are shaping procurement decisions. In July 2025, ICL Group showcased industrial-scale application of its Puraloop® recycled phosphorus platform, creating a circular feedstock stream for phosphorus-based precursors used in radical photoinitiators such as phosphine oxides. In 2025, Rahn AG achieved EcoVadis Gold Medal status, expanding Product Carbon Footprint coverage to 70% of its EnergyCuring portfolio. This reflects broader demand for low-carbon UV-curing materials across packaging and automotive supply chains.

Technological transition toward UV-LED systems is accelerating. By February 2026, industry reports confirmed widespread migration to photoinitiators optimized for 395nm and 405nm wavelengths, replacing mercury-vapor lamps in printing, 3D printing, and electronics assembly. These UV-LED-specific photoinitiators deliver deeper cure, improved energy efficiency, and lower thermal stress, supporting sustainability targets and process cost reduction. Meanwhile, artience Group expanded into near-infrared fluorescent materials and advanced photo-curable resins in late 2024, broadening photoinitiator applications in security printing and medical diagnostics.

Corporate portfolio restructuring also influenced market focus. In October 2025, BASF divested its decorative paints operations to sharpen focus on high-value industrial solutions, including advanced photoinitiators for automotive multi-coat UV systems. Concurrently, BASF Coatings unveiled 2025–2026 automotive color technologies requiring next-generation UV-curing systems to achieve enhanced scratch resistance and metallic depth. In January 2026, Tatva Chintan confirmed progress on its Jolva facility, expanding quaternary ammonium precursor production critical for cationic photoinitiator systems in electronics.

Technology-Led Trends and Monetizable Opportunities in the Photoinitiator Market

Accelerated Shift to Low-Migration and Bio-Attributed Photoinitiator Systems

The global photoinitiator market is undergoing a structural reset as regulatory scrutiny around food-contact materials, packaging safety, and chemical migration moves from guidance to enforcement. In Europe, updated Swiss Ordinance limits and downstream brand owner specifications such as the Nestlé Guidance Note have effectively redefined “low-migration” from a premium feature to a baseline compliance requirement. As a result, manufacturers are rapidly moving away from small-molecule photoinitiators such as benzophenone and ITX, which are prone to diffusion and extractables, toward polymeric and macromolecular systems that are physically incapable of migrating through packaging substrates.

This transition is already reflected in commercial product development. In December 2025, IGM Resins expanded its glyoxylate-based portfolio with Omnipol® BL 582, a polymeric photoinitiator engineered specifically for high-speed, low-migration ink systems used in flexible food packaging. The product addresses stringent brand owner compliance thresholds while maintaining the fast cure response required for industrial printing lines operating at scale. Such developments illustrate how performance and compliance are now being optimized simultaneously rather than treated as trade-offs.

Parallel to migration control, carbon intensity has become a second strategic filter in photoinitiator selection. In mid-2025, Arkema (via its Sartomer business) secured ISCC PLUS certification across its U.S. and Malaysia production sites, enabling the commercial rollout of bio-attributed photoinitiators and acrylate systems under a mass-balance framework. This approach allows converters and brand owners to claim 30–40% carbon footprint reductions at the formulation level without sacrificing cure speed, surface hardness, or chemical resistance.

At the frontier of this trend, the industry is also exploring initiator-free curing concepts. A landmark collaboration between BASF and IST Metz, showcased across the 2024–2025 Drupa cycle, introduced FreeCure technology. By combining high-dose UV-C irradiation with tailored aqueous varnishes, the system enables full cross-linking without conventional photoinitiators. For food-safe packaging, this represents a disruptive pathway that eliminates extractable risk entirely and redefines the competitive ceiling for low-migration performance.

Formulation-Specific Photoinitiators for Industrial-Scale Additive Manufacturing

A second major trend reshaping the photoinitiator market is the industrialization of additive manufacturing. As 3D printing transitions from prototyping to serial production, photoinitiators are no longer selected for generic reactivity but for formulation-specific performance under thick layers, high filler loading, and continuous production cycles.

Industry data for 2025 shows that consumption of cationic photoinitiators in additive manufacturing applications has increased by approximately 60% compared to prior cycles. This surge is driven by their inherent advantages in stereolithography and digital light processing systems, including reduced volumetric shrinkage, superior adhesion, and reliable curing through thick sections. These properties are increasingly critical as printed components move into functional automotive, aerospace, and industrial tooling applications.

At the same time, the standardization of 405 nm LED light engines across industrial printers has triggered a focused R&D push to replace traditional acylphosphine oxide initiators such as TPO and TPO-L. While effective, these materials are associated with yellowing and long-term color instability in thick sections. In response, new Type I and Type II initiator blends are being developed with optimized absorption profiles that align precisely with 365 nm and 395 nm LED outputs, ensuring deep cure without aesthetic compromise.

The scale of this transition is already visible in downstream adoption. By 2024–2025, automotive OEMs had shifted roughly 40% of rapid prototyping and tooling workflows toward high-performance UV-curable resins. This volume expansion is driving demand for photoinitiators with higher thermal stability to withstand the intense exothermic heat generated during high-speed continuous liquid interface production, reinforcing the move toward application-engineered initiator systems.

Photoinitiators for Thin-Film Encapsulation in Foldable and Flexible Displays

One of the most attractive margin opportunities in the photoinitiator market lies in advanced display technologies. The rapid commercialization of foldable smartphones and rollable OLED panels has elevated thin-film encapsulation from a niche process to a core manufacturing step. These architectures rely on ultra-thin UV-cured barrier coatings that must deliver moisture and oxygen protection without introducing thermal stress or optical distortion.

During 2024–2025, leading display manufacturers integrated nanoscale UV-cured encapsulation layers adding less than 0.1 mm to total device thickness while maintaining scratch resistance and environmental durability. Achieving this requires ultra-high-purity photoinitiators that cure cleanly, leave no residual odor, and preserve more than 99% optical clarity. Any trace by-products can compromise display uniformity or long-term reliability, making initiator purity a decisive qualification criterion.

Research published in 2025 underscores why UV-curable systems have become the industry standard for encapsulation. Their low shrinkage and rapid cure prevent stress cracking in flexible substrates, but performance is highly sensitive to initiator chemistry. The next growth wave is centered on liquid-phase photoinitiators that bond reliably to polyimide and other low-surface-energy films used in foldable displays. In parallel, demand is rising for dual-cure systems combining UV and thermal activation, enabling full polymerization along curved edges and shadowed geometries where light exposure is limited.

Expansion of UV-LED Photoinitiators for Digital and Sustainable Packaging

The final major opportunity lies in the acceleration of energy-curing digital printing for packaging. As converters replace analog flexographic and gravure processes with on-demand digital systems, UV-LED inkjet technologies are becoming the preferred solution for short runs, variable data, and rapid changeovers. This shift has direct implications for photoinitiator selection.

In February 2025, new photoinitiator selection strategies were introduced to resolve wavelength mismatch challenges in high-speed digital presses. By aligning initiator absorption peaks precisely with 365 nm and 395 nm LED outputs, printers can reduce energy consumption by up to 50% compared to mercury lamp systems while maintaining cure integrity on non-porous substrates.

The circular economy adds another layer of complexity. As packaging increasingly incorporates recycled PET and HDPE, surface energy variability creates adhesion challenges for UV inks. This has opened a high-growth niche for amine-modified acrylate co-initiators that enhance wetting and reactivity under oxygen-inhibited conditions, particularly on low-energy recycled plastics.

Market adoption is already advanced. By 2025, approximately 45% of new commercial digital printing installations were based on UV-LED curing platforms. To support this transition, Arkema launched dedicated Graphic Arts Centers of Excellence in the UK, focused on optimizing photocurable formulations for labels and packaging at industrial scale. This infrastructure investment signals long-term confidence in UV-LED photoinitiator demand as digital printing becomes the dominant growth engine in sustainable packaging.

Photoinitiator Market Share and Segmentation Insights

Free Radical Photoinitiators Lead UV-Curable Chemistry Adoption in Industrial Coatings and Printing Systems

Free radical photoinitiators accounted for 52.80% of the Photoinitiator Market by type in 2025, reflecting their dominant role in UV-curable coatings, inks, and adhesive formulations. These photoinitiators initiate polymerization in acrylate-based systems widely used in wood coatings, overprint varnishes, and graphic arts applications due to their fast curing speed and efficient through-cure performance. Their cost effectiveness and compatibility with large-scale UV curing processes continue to drive strong industrial adoption. In 2025, low-migration free radical photoinitiator development for food packaging applications is gaining importance, with manufacturers designing polymeric and high-molecular-weight photoinitiators that remain immobilized in cured films, supporting regulatory compliance in food contact packaging materials.

Paints and Coatings Segment Drives Photoinitiator Demand in UV and LED-UV Curing Technologies

Paints and coatings represented 42.80% of the Photoinitiator Market by application in 2025, reflecting widespread use of UV-curable coatings in furniture finishing, flooring systems, packaging coatings, and industrial surface protection. UV curing technology enables rapid polymerization, high production throughput, and reduced volatile organic compound emissions compared with conventional thermal curing methods. Industries such as wood processing, packaging printing, and metal finishing continue to expand adoption of UV-curable coating systems. In 2025, the transition toward LED-UV curing systems operating in the 365–405 nm wavelength range is influencing photoinitiator chemistry development, with new initiator molecules optimized for LED absorption spectra enabling efficient curing without traditional mercury arc lamp systems.

Photoinitiator Market Competitive Landscape

The global photoinitiator market is transitioning toward UV-LED curing systems, replacing mercury-lamp technologies and accelerating demand for high-purity, low-migration, and polymeric photoinitiators. Competitive dynamics are shaped by resin-photoinitiator integration, regulatory compliance for food contact materials, and advanced applications in 3D printing, electronics, and sustainable packaging.

IGM Resins Expands Polymeric Photoinitiator Portfolio with Strong IP Protection and India Market Entry

IGM Resins operates as a pure-play leader in energy-curing raw materials with a comprehensive portfolio including Omnirad®, Esacure®, and Omnipol® photoinitiators. The December 2025 partnership with IDCC Global Chem strengthens distribution across India, targeting inks and coatings demand growth. Omnipol® BL 582, a polymeric glyoxylate photoinitiator, addresses food contact material requirements with ultra-low migration performance. The company enforces its BAPO intellectual property, supported by a legal win protecting Omnirad 819 manufacturing processes used in deep-curing pigmented systems. Investment in a cryogenic nitrogen plant at Mortara (August 2025) supports lower-emission chemical synthesis. Product strategy centers on high-purity, polymeric photoinitiators aligned with regulatory compliance and advanced curing performance.

Arkema Integrates Photoinitiators with Specialty Resins for UV-LED and 3D Printing Applications

Arkema, through its Sartomer® platform, delivers integrated UV/LED/EB curing solutions combining photoinitiators with specialty acrylate resins. The Wetherby Center of Excellence (February 2025) focuses on low-migration formulations for digital printing and circular packaging. Collaboration with Axtra3D (November 2025) enables qualification of N3xtDimension® resins for high-speed SLA 3D printing, embedding photoinitiator functionality into additive manufacturing systems. The Speedcure range includes cationic photoinitiators for epoxy systems with low shrinkage and high chemical resistance in electronics encapsulation. Development of smart-tagged formulations enables real-time monitoring of curing depth in thick coatings and complex geometries. Portfolio strategy emphasizes turnkey curing systems and application-specific performance.

BASF Focuses on High-Purity Specialty Photoinitiators within Integrated Dispersions and Resin Systems

BASF SE concentrates on high-value photoinitiators integrated into its broader dispersions and resin portfolio following divestment of standard product lines. R&D spending of approximately €2 billion in 2024 supports development of non-migratory photoactive building blocks for flexible electronics and apparel applications. Sustainability-driven innovation accounts for 45% of new patents, targeting green photoinitiator chemistry. The March 2026 price increase across acrylate intermediates reflects rising precursor costs for high-grade photoinitiator production. Expansion of dispersions capacity in Mangalore (February 2026) supports regional demand for UV-curable construction and architectural coatings. Technology focus aligns with high-purity, low-migration photoinitiators and integrated material systems.

Rahn Develops Advanced Photoinitiator Blends for UV-LED, Visible Light, and Excimer Applications

Rahn AG supplies high-performance photoinitiators under the GENOCURE® portfolio with strong emphasis on formulation expertise. GENOCURE® LRT, introduced in 2025, replaces traditional TPO with low-yellowing properties and improved curing in white pigmented UV/LED inks. The GENOCURE® BAPO series supports high-thickness curing requirements in aerospace and automotive composite materials. GENOCURE® CQ enables visible-light curing, widely used in medical and dental applications requiring precise light activation. Strategic focus on excimer lamp technologies supports ultra-matte and scratch-resistant coatings for wood and plastics. Product development addresses specialized curing environments and high-performance industrial applications.

Zhejiang Yangfan Strengthens Cost Leadership with Large-Scale Photoinitiator Production and Backward Integration

Zhejiang Yangfan New Materials operates as a large-scale producer of commodity photoinitiators with strong cost efficiency and global supply capability. The company maintains annual production capacity exceeding 3,000 tons for Photoinitiator 907, serving high-volume UV-inkjet and PCB manufacturing markets. Backward integration into benzophenone and phosphorus-based intermediates reduces raw material volatility and enhances supply chain control. Portfolio diversification toward Photoinitiator 707 and ECHA-compliant alternatives supports continued access to European markets under tightening regulatory frameworks. The company supplies ultra-pure photoinitiators for PCB and display manufacturing in South Korea and China, where low ionic contamination is critical for yield performance. Manufacturing strategy focuses on scale, compliance, and high-volume industrial applications.

China – Semiconductor Self-Sufficiency and Solar-Driven Volume Expansion

China’s photoinitiator industry is being reshaped by state-backed self-sufficiency mandates and large downstream pull from semiconductors and photovoltaics. Under the MIIT Work Plan for Chemical Growth (2025–2026), high-purity photoinitiators are classified as strategic reagents, particularly sulfonium salts used in advanced integrated circuit manufacturing. This policy focus is explicitly aimed at reducing reliance on Japanese and European electronic-grade precursors, accelerating domestic R&D and capacity build-out. Environmental enforcement has added another layer of structural change. From July 2025, stricter discharge limits for TPO production compelled manufacturers such as Tianjin Jiuri New Materials to implement closed-loop solvent recovery, increasing compliance costs but materially improving process sustainability and export readiness.

Demand-side momentum is equally significant. As China targets 270–300 GW of solar installations in 2025, photoinitiators used in UV-curable solar cell encapsulates have moved into a strategic supply category. The MIIT-led August 2025 symposium on quality standards reflects official concern over supply stability and the prevention of below-cost sales in this critical input market. On the manufacturing front, the commissioning of iGM Resins’ Anqing greenfield site in late 2025, with capacity exceeding 10,000 metric tons and backward integration into key starting materials, marks a shift toward scale plus security. By year-end 2025, China had reportedly achieved 70% self-sufficiency in core basic materials under the Made in China 2025 framework, with photoinitiators firmly embedded in this milestone.

India – Distribution-Led Market Penetration and Medical-Grade Upgrading

India’s photoinitiator landscape is transitioning from import dependence to a hybrid model combining global distribution alliances and localized specialty production. The December 2025 exclusive distribution agreement between iGM Resins and IDCC Global Chem, effective January 2026, is strategically targeted at Mumbai and Gujarat, where energy-curing inks and adhesives are seeing accelerated adoption. This partnership significantly improves market access for advanced LED-curing photoinitiators while reducing technical service gaps for local converters.

Macroeconomic tailwinds are reinforcing this shift. The Economic Survey 2024–2025 highlighted 9.5% industrial growth, triggering new investments in UV-curable infrastructure across packaging, labels, and electronics assembly. Domestic producers such as Rahul Photoinitiators are scaling output to meet a reported 55% rise in regional demand. Parallel to volume growth, India is moving up the value chain in regulated applications. Driven by the BioE3 Policy (2025), manufacturers are expanding production of biocompatible photoinitiators for medical devices and dental resins. This segment, supported by domestic healthcare manufacturing and export ambitions, is expected to be a key differentiator for India through 2026.

United Kingdom – Regulatory Navigation and Sustainable Formulation Leadership

The United Kingdom has positioned itself as a formulation and regulatory competence hub within the global photoinitiator ecosystem. Arkema’s inauguration of the Graphic Arts Center of Excellence in Wetherby in February 2025 anchors this role. The center is dedicated to UV, LED, and EB curable solutions for digital printing and sustainable packaging, reflecting the industry’s pivot away from high-VOC systems toward low-migration alternatives. Beyond formulation, Wetherby has been designated as a global compliance hub, supporting molecule development under both UK REACH and EU regulatory regimes, a critical capability in the post-Brexit environment.

Sustainability-driven R&D is a core pillar of UK activity. Arkema’s ongoing pilots of bio-attributed photoinitiators using a mass-balance approach signal a move toward lower-carbon industrial printing solutions by late 2026. This combination of regulatory fluency and sustainable chemistry positions the UK less as a volume producer and more as an innovation and validation center for next-generation photoinitiator systems.

Germany – Regulatory Shock and Rapid Transition to Polymer-Based Systems

Germany sits at the epicenter of regulatory-driven transformation in the European photoinitiator market. The enforcement of Commission Regulation (EU) 2025/877, banning TPO from the EU market as of September 1, 2025, has forced a rapid pivot toward sustainable TPO alternatives and polymeric photoinitiators. This shift has been compounded by REACH Annex XVII updates in June 2025, which restrict solvents such as DMAC and NEP in photoinitiator manufacturing and impose new DNEL compliance deadlines by December 2026.

Despite regulatory pressure, Germany remains a focal point for innovation. At RadTech Europe 2025, German players showcased advanced photoinitiator systems for UV-curing composites used in lightweight automotive structures. BASF SE’s 2025 expansion of its compliant Luvipur and Irgacure ranges underscores the industry’s move toward polymeric photoinitiators designed to minimize migration risk in food-contact and sensitive packaging applications. These developments position Germany as the EU’s primary transition hub from legacy photoinitiators to next-generation, regulation-aligned systems.

Japan – High-Precision Electronic Materials and Specialty Portfolio Reorientation

Japan’s photoinitiator industry is tightly coupled with its electronic materials ecosystem, emphasizing purity, precision, and reliability over volume. In 2025, Tokyo Ohka Kogyo and JSR Corporation scaled production of I-Line and G-Line photoresists, which rely on tightly controlled photoinitiator chemistries for mature lithography nodes used in consumer electronics and automotive AI chips. While not cutting-edge by node size, these applications are critical for volume electronics and remain highly margin-accretive.

At the frontier, Japanese firms are leading in chemically amplified resists that utilize high-precision photoinitiators to enable sub-7nm patterning, reinforcing Japan’s role in advanced lithography R&D. Structurally, May 2025 portfolio restructuring announcements by major chemical groups, including Mitsui Chemicals, highlight a deliberate shift away from commodity chemicals toward high-margin specialty photoinitiators for OLED displays and advanced electronics. This strategic isolation of commodity assets is strengthening Japan’s positioning as a premium supplier of photoinitiators for mission-critical applications.

Comparative Snapshot – Photoinitiator Industry by Country

Photoinitiator Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key 2025–2026 Catalyst

|

Industry Positioning

|

|

China

|

Self-sufficiency and scale

|

Semiconductors and solar PV expansion

|

High-volume, integrated producer

|

|

India

|

Market access and specialty upgrading

|

Distribution alliances and medical applications

|

Emerging specialty hub

|

|

United Kingdom

|

Regulatory and sustainability leadership

|

UK REACH alignment and bio-attributed R&D

|

Innovation and compliance center

|

|

Germany

|

Regulation-driven transformation

|

TPO ban and REACH solvent restrictions

|

EU transition and reformulation hub

|

|

Japan

|

Precision electronics focus

|

Advanced lithography and OLED materials

|

Premium, high-purity supplier

|

Photoinitiator Market Report Scope

Photoinitiator Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$5.7 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Type (Free Radical Photoinitiators, Cationic Photoinitiators, Polymeric Photoinitiators, Visible Light & LED Curable Photoinitiators, Water-Borne Photoinitiators), By Application (Paints & Coatings, Inks, Adhesives & Sealants, Electronics & Lithography, Additive Manufacturing), By End-Use Industry (Packaging & Graphic Arts, Consumer Electronics, Automotive & Transportation, Healthcare & Medical Devices, Construction & Infrastructure)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

IGM Resins, Arkema SA, BASF SE, Lambson Ltd., Tianjin Jiuri New Materials Co. Ltd., Tronly New Electronic Materials Co. Ltd., Adeka Corporation, JSR Corporation, Tokyo Ohka Kogyo Co. Ltd., Evonik Industries AG, Double Bond Chemical Industrial Co. Ltd., Eutec Chemical Co. Ltd., Zhejiang Yangfan New Materials Co. Ltd., Rahn AG, Miwon Specialty Chemical Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Photoinitiator Market Segmentation

By Type

- Free Radical Photoinitiators

- Cationic Photoinitiators

- Polymeric Photoinitiators

- Visible Light & LED Curable Photoinitiators

- Water-Borne Photoinitiators

By Application

- Paints & Coatings

- Inks

- Adhesives & Sealants

- Electronics & Lithography

- Additive Manufacturing

By End-Use Industry

- Packaging & Graphic Arts

- Consumer Electronics

- Automotive & Transportation

- Healthcare & Medical Devices

- Construction & Infrastructure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Photoinitiator Industry

- IGM Resins

- Arkema SA

- BASF SE

- Lambson Ltd.

- Tianjin Jiuri New Materials Co. Ltd.

- Tronly New Electronic Materials Co. Ltd.

- Adeka Corporation

- JSR Corporation

- Tokyo Ohka Kogyo Co. Ltd.

- Evonik Industries AG

- Double Bond Chemical Industrial Co. Ltd.

- Eutec Chemical Co. Ltd.

- Zhejiang Yangfan New Materials Co. Ltd.

- Rahn AG

- Miwon Specialty Chemical Co. Ltd.

*- List not Exhaustive