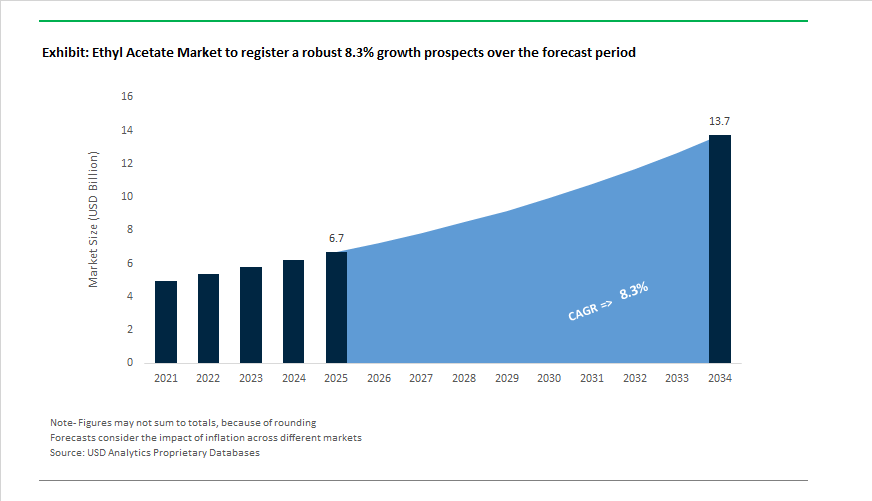

Ethyl Acetate Market to Reach $13.7 Billion by 2034 as Bio-Based Capacity and Acetyl Chain Integration Accelerate

The Ethyl Acetate Market is projected to grow from $6.7 billion in 2025 to $13.7 billion by 2034, reflecting a robust CAGR of 8.3%. Growth is being driven by expanding demand from paints and coatings, flexible packaging inks, pharmaceuticals, and specialty adhesives, alongside a structural shift toward renewable ethanol-based production. As a fast-evaporating, low-toxicity solvent with strong solvency for resins and polymers, ethyl acetate remains central to industrial and pharmaceutical processing, particularly in regions undergoing packaging and infrastructure expansion.

A defining development in the market is the transition toward bio-based production pathways. Viridis Chemical relocated its renewable ethyl acetate plant to Peoria, Illinois in January 2025, co-locating with BioUrja Renewables’ high-purity alcohol facility to enhance feedstock integration and logistics efficiency. The facility, expected to reach full operational capacity by late 2025, converts corn-derived ethanol into sustainable ethyl acetate using a proprietary low-energy process. The company’s technology previously earned recognition from the U.S. Environmental Protection Agency through the 2024 Green Chemistry Challenge Award, highlighting the increasing policy support for green solvent chemistry in North America.

In Europe, CropEnergies AG broke ground in April 2024 on a €130 million renewable ethyl acetate facility in Zeitz, Germany. Positioned as the first dedicated green ethyl acetate plant in Europe, the project leverages sustainable ethanol feedstock to reduce lifecycle carbon emissions compared to fossil-based imports. This investment responds directly to EU decarbonization targets and the packaging sector’s demand for low-carbon solvents compatible with recyclable flexible films.

India is simultaneously emerging as a competitive export hub. Godavari Biorefineries Limited committed ₹130 crore toward a 200 KLPD dual-feedstock distillery in late 2024, ensuring ethanol security through both sugarcane and grain routes. This flexibility mitigates climate-linked agricultural volatility and strengthens downstream ethyl acetate production stability. In parallel, Jubilant Ingrevia announced 18 new product launches targeting high-purity solvent grades for CDMO pharmaceutical applications, where ethyl acetate is widely used in extraction and crystallization processes.

China continues to consolidate upstream dominance. By the end of 2025, nearly 10 million tons of additional ethylene capacity were commissioned domestically, stabilizing acetic acid and ethanol intermediate supply. State-backed integration strategies from Sinopec aim to shift refinery yields toward higher-value aromatics and olefins through 2027, reinforcing China’s position as the lowest-cost global exporter of commodity ethyl acetate.

Meanwhile, European manufacturers face structural headwinds. Celanese Corporation announced the planned closure of its Lanaken, Belgium facility by H2 2026 as part of broader acetyl chain optimization. Rising energy costs and regulatory burdens are accelerating the migration of solvent capacity toward North America and Asia. At the same time, Wacker Chemie AG reported stable 2025 chemical earnings but implemented price increases in January 2026 to offset persistent logistics and raw material inflation.

Regulatory compliance remains central to export competitiveness. IOL Chemicals and Pharmaceuticals secured EU REACH approval in October 2024, allowing expanded access to the European coatings and pharmaceutical markets amid tightening quality standards.

Trends and Opportunities in the Ethyl Acetate Market

Rapid Scale-Up of Bio-Based Production and Feedstock Transition

- The most defining trend in the ethyl acetate market is the accelerated shift away from fossil-derived ethylene toward bio-ethanol and bio-acetic acid feedstocks. This transition is directly linked to Scope 3 emission reduction targets set by coatings, packaging, and specialty chemicals manufacturers, which increasingly require solvents with verifiable renewable carbon content.

- In May 2024, CropEnergies AG announced an investment of approximately USD 130–140 million to build a renewable ethyl acetate facility at the Zeitz Chemical and Industrial Park in Germany. Scheduled for commissioning by the end of 2025, this plant is designed to supply fossil-free ethyl acetate to European paints, coatings, and printing ink producers, significantly lowering the cradle-to-gate carbon footprint of finished formulations.

- Bio-integrated producers in Asia are also strengthening feedstock resilience. Godavari Biorefineries Ltd. reported in its FY 2024–25 sustainability disclosures that its 570 KLPD ethanol capacity underpins a globally competitive bio-ethyl acetate portfolio. In December 2024, the company further diversified feedstock sourcing by expanding grain-based ethanol inputs, reducing exposure to sugarcane supply volatility and ensuring uninterrupted renewable solvent output.

- In Europe, decarbonization efforts are extending beyond feedstock to site energy systems. INEOS Acetyls completed a GBP 30 million hydrogen conversion project at its Hull facility in December 2025. By replacing natural gas with clean-burning hydrogen, the site achieved a 75% reduction in CO₂ emissions, establishing a benchmark for low-carbon ethyl acetate manufacturing at industrial scale.

Displacement of N-Methyl-2-Pyrrolidone in Precision Manufacturing

- A parallel demand shift is unfolding as ethyl acetate increasingly replaces N-methyl-2-pyrrolidone in battery, electronics, and pharmaceutical manufacturing. Regulatory pressure under EU REACH Annex XVII and updated U.S. TSCA risk management rules has made NMP a high-liability solvent due to its reproductive toxicity classification and tightening workplace exposure limits.

- By late 2025, high-purity ethyl acetate had gained traction in lithium-ion battery electrode processing, particularly in PVDF binder systems. Compared with NMP, ethyl acetate offers a lower boiling point and faster solvent removal, reducing drying energy requirements in gigafactory coating lines by an estimated 15 to 20%. These efficiency gains translate directly into lower operating costs and improved throughput at scale.

- Ethyl acetate’s favorable toxicological profile is also reinforcing its adoption. Sekab, recipient of the Environmental Strategy Award 2025, has positioned its ISCC+ certified bio-ethyl acetate as a non-toxic, fossil-free alternative for pharmaceutical and electronics manufacturers seeking to eliminate high-concern solvents from procurement frameworks. This shift reflects a broader market reality where solvent choice is now scrutinized as closely as active material performance.

High-Performance, Low-VOC Adhesives for Flexible Packaging

- Flexible packaging remains one of the most resilient demand pillars for ethyl acetate, particularly as brand owners push for low-VOC, food-safe, and high-speed adhesive systems. Ethyl acetate continues to be favored in solvent-based and hybrid adhesive formulations due to its excellent solvency for polyurethane resins and rapid evaporation characteristics.

- As of November 2025, food packaging and medical laminates represent a major share of ethyl acetate consumption in adhesives. Its acceptance under multiple global eco-labeling schemes enables converters to achieve low-VOC certification without compromising bond strength or line speed. Modern lamination lines increasingly operate at 400 to 600 meters per minute, and ethyl acetate’s fast flash-off profile is critical to maintaining this throughput in high-volume FMCG supply chains.

- Regionally, Asia-Pacific remains the largest volume market, supported by strong packaging demand in China and India. However, North America is emerging as the fastest-growing region for high-performance adhesive solvents through 2030, driven by the replacement of ketones and other hazardous air pollutants in response to stricter air quality regulations.

Circular Lignin-First Biorefining and Decentralized Production Models

- Ethyl acetate is also gaining strategic importance within circular bio-economy frameworks, particularly in lignin valorization and decentralized biorefining. Recent 2024–2025 academic and industrial studies have identified ethyl acetate as an effective solvent for depolymerizing technical lignin into high-value phenolic compounds such as vanillin and guaiacol. These lignin-first approaches allow agricultural and forestry residues to be converted into sustainable chemical intermediates rather than burned or discarded.

- Because ethyl acetate can be synthesized directly from fermentation-derived ethanol and acetic acid, it supports decentralized production models where biorefineries generate both the solvent and the extracted bio-actives on site. This closed-loop approach significantly reduces logistics-related emissions and improves supply security for rural processing hubs.

- Demand is also rising in the extraction of essential oils and pharmaceutical intermediates, where bio-ethyl acetate enables 100% natural-origin declarations. Its selective solvency preserves aromatic integrity while eliminating petrochemical residue concerns, making it particularly attractive for high-value botanical and nutraceutical applications.

Ethyl Acetate Market Share and Segmentation Insights

Synthetic Ethyl Acetate Dominates Supply as Bio-Based Alternatives Gain Momentum

Synthetic ethyl acetate represents 88% of total market share in 2025, reflecting its cost efficiency, consistent quality, and mature global supply chains based on acetic acid–ethanol esterification and acetaldehyde routes. This dominance supports large-volume demand from coatings, printing inks, adhesives, and chemical processing industries requiring reliable solvent performance. Bio-based ethyl acetate, produced from fermentation-derived ethanol, remains a smaller but rapidly expanding segment as sustainability commitments accelerate across packaging, cosmetics, and food-contact applications. Although commanding premium pricing, renewable ethyl acetate benefits from lower carbon footprints and growing regulatory preference for green solvents. Brand owners increasingly specify bio-based grades for environmentally conscious formulations, positioning this segment as a strategic growth lever within the broader ethyl acetate market despite lower overall volumes.

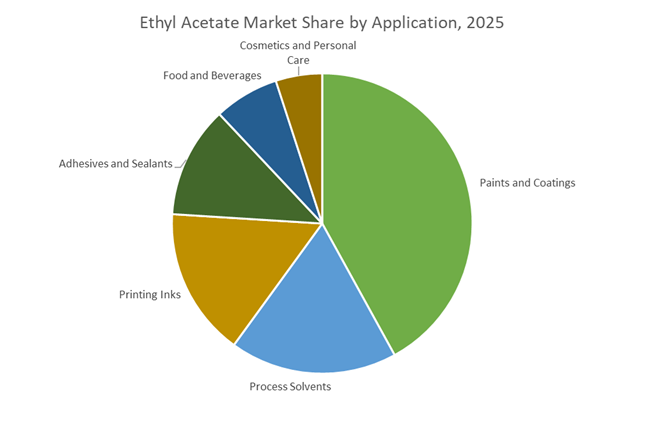

Paints and Coatings Lead Solvent Consumption Across Industrial and Packaging Applications

Paints and coatings account for 42% of ethyl acetate demand in 2025, making this the largest application segment. Ethyl acetate’s fast evaporation rate and strong solvency for nitrocellulose and film-forming resins enable quick-drying finishes in automotive refinish, industrial coatings, and wood treatments. Process solvents form a major secondary market, using ethyl acetate in pharmaceutical extraction, chemical synthesis, and specialty manufacturing where low toxicity and volatility are valued. Printing inks represent a significant share, particularly in gravure and flexographic printing for flexible packaging and labels, supporting high-speed production with sharp image quality. Adhesives and sealants maintain steady uptake in footwear, packaging, and construction. Food and beverages utilize ethyl acetate for flavoring and decaffeination, while cosmetics and personal care represent a fast-growing segment for nail products, fragrances, and makeup removers driven by consumer preference for mild, efficient solvents.

Competitive Landscape of the Ethyl Acetate Market

The global ethyl acetate market in 2026 is defined by deep feedstock integration, rapid decarbonization initiatives, and strong demand from pharmaceuticals, flexible packaging, paints & coatings, and electronics, with leading producers leveraging AI, bio-based pathways, and CCU to defend margins in a volatile acetyls value chain.

Celanese accelerates low-carbon ethyl acetate through acetyls dominance and CCU integration

Celanese Corporation anchors the global ethyl acetate market through its leadership in acetyl intermediates and its position as the world’s largest acetic acid producer. The company supplies high-purity ethyl acetate for high-performance paints & coatings and flexible packaging. Following the full integration of DuPont’s Mobility & Materials business by 2026, Celanese strengthened downstream ester utilization across its engineering materials portfolio. During 2025–2026, AI-driven reactor optimization improved yields and reduced carbon intensity by an estimated 3%–5%. Its Carbon Capture & Utilization strategy converts captured CO2 into methanol feeding the acetyls chain, positioning Celanese as a pioneer of lower-carbon ethyl acetate supported by a tightly optimized global supply network spanning North America, Europe, and Asia.

INEOS Acetyls scales sustainable ethyl acetate via Texas City expansion and bio-attributed solvents

INEOS Acetyls has rapidly emerged as a top-tier ethyl acetate producer after completing the $490 million acquisition of Eastman’s Texas City operations, significantly expanding 2026 capacity. Leveraging competitive U.S. feedstocks, INEOS now dominates the North American merchant solvent market while supplying pharmaceutical-grade ethyl acetate for API extraction and purification. In Europe, the company launched a sustainable ethyl acetate line using mass-balance bio-attributed feedstocks, targeting cosmetics and personal care brands seeking lower carbon footprints. Backed by extreme vertical integration into ethylene and ethane, INEOS maintains cost leadership across acetyl derivatives, reinforcing its role as a strategic supplier to pharma, coatings, and specialty solvent customers.

Jubilant Ingrevia advances bio-ethyl acetate to capture specialty chemicals growth

Jubilant Ingrevia Limited ranks as the world’s seventh-largest ethyl acetate manufacturer and a standout in bio-ethyl acetate derived from agricultural ethanol. Its REACH-registered product portfolio carries Halal, Kosher, and FSSC/ISO-22000 certifications, appealing strongly to Western FMCG and packaging players seeking de-fossilized solvents. In early 2026, Jubilant executed a major capability reset, expanding scientific talent by 50% and establishing a tech-transfer organization to scale its CDMO platform. While ethyl acetate remains a core intermediate, the company is pivoting toward higher-margin specialty chemicals and nutrition, projecting a 22% EBITDA CAGR through FY26–28, driven by monetized capital investments and strong green credentials.

Jiangsu Sopo strengthens Asia-Pacific supply with high-purity ethyl acetate and APC upgrades

Jiangsu Sopo Chemical Co., Ltd. leads China’s ethyl acetate production in the world’s largest exporting and consuming region. In 2025–2026, Sopo successfully scaled ≥99.9% high-purity ethyl acetate, targeting electronics and photoresist solvent applications. The company operates the Asia-Pacific region’s largest ethanol-derivative capacity, providing critical supply-chain stability. Late-2025 upgrades introduced Advanced Process Control in distillation columns, significantly cutting energy consumption for high-purity separation. With massive in-house glacial acetic acid production, Jiangsu Sopo maintains some of the most competitive bulk pricing globally, reinforcing its dominance in merchant ethyl acetate for coatings, inks, and electronics-grade solvent markets.

Laxmi Organic expands Indian ethyl acetate capacity to drive import substitution

Laxmi Organic Industries Ltd. plays a pivotal role in South Asia’s specialty intermediates landscape, serving fast-growing pharmaceutical, printing ink, and flexible packaging sectors. In 2024–2025, the company approved approximately $22 million (₹182 crore) to build a new 70 KTA ethyl acetate plant in Lote, Maharashtra, directly supporting India’s “Make in India” and import substitution objectives. Laxmi Organic dominates food-safe packaging solvents in the region and is integrating recent acquisitions to offer broader acetyl alternatives to cosmetics and fragrance formulators. Its 2026 strategy centers on strengthening domestic supply chains while expanding value-added solvent portfolios for pharma and coatings customers.

India: Ethanol Policy Shock and Competitive Rebalancing

India’s ethyl acetate market in 2025–2026 is being structurally reshaped by national fuel policy rather than downstream solvent demand. In October 2025, the Government of India removed quantitative restrictions on ethanol production for the supply year beginning November 1, 2025, accelerating the path toward a 20% ethanol-to-gasoline blending target by end-2026. While this policy strengthens energy security, it has materially tightened the availability of bio-ethanol feedstock for domestic ethyl acetate producers, forcing acetyl manufacturers to optimize sourcing strategies and production efficiency. As ethanol diversion toward fuels intensifies, ethyl acetate producers are prioritizing yield optimization, batch rationalization, and cost discipline to protect margins in pharmaceutical and agrochemical solvent applications.

Despite feedstock pressure, leading producers such as Jubilant Ingrevia reported resilient operational performance. In the quarter ending September 30, 2025, the company posted a 6% year-on-year increase in its Chemical Intermediates segment, driven by record ethyl acetate and acetic anhydride volumes. Jubilant’s ongoing Multi-Purpose Plant expansion at Gajraula, scheduled for completion by late 2026, is designed to address sustained demand from regulated end-use sectors. In parallel, Indian producers have transitioned nearly 28% of their power consumption to renewable energy as of late 2025, lowering fuel costs by roughly 16%. Combined with internal lean savings programs, these measures enabled Indian exporters to recover lost volume share in Q3 2025 despite rising ethanol input costs.

China: Policy-Backed Self-Sufficiency and Digital Solvent Manufacturing

China’s ethyl acetate market is advancing under a coordinated industrial policy framework that emphasizes specialty solvent self-reliance and digitalized production. In October 2025, seven ministries including the Ministry of Industry and Information Technology issued a Steady Growth Plan targeting more than 5% average annual growth for the chemical industry through 2026. Within this agenda, ethyl acetate is categorized as a priority specialty solvent, particularly for electronics, coatings, and high-purity applications.

Regulatory mandates are accelerating digital transformation. The 2026 roadmap for chemical clusters requires AI-driven process optimization and blockchain-based traceability for solvent supply chains, directly affecting high-purity ethyl acetate lines serving electronics manufacturing. At the structural level, Beijing’s self-sufficiency initiative aims to lift domestic coverage of critical intermediates beyond 90% by 2026, reducing reliance on imported acetyls from the United States and Southeast Asia. This objective is reinforced by the final commissioning phase of the SINOPEC–BASF Zhanjiang Verbund site, where world-scale ethylene and downstream ester units are expected to reach full throughput by mid-2026, strengthening China’s integrated acetyl platform.

Germany: Energy Economics Forcing Structural Reset

Germany’s ethyl acetate market illustrates the pressure that energy economics are exerting on Europe’s solvent value chain. In October 2025, INEOS Inovyn announced the closure of its electrochemical and allylics operations at Rheinberg, citing unsustainable energy costs and the absence of protective trade mechanisms. This decision reflects a broader rationalization trend across European solvent production, where high fixed energy inputs have undermined regional competitiveness.

Counterbalancing these exits, bio-based solvent infrastructure is emerging as a strategic response. CropEnergies AG is commissioning a renewable ethyl acetate plant at the Zeitz Chemical and Industrial Park with a €130–140 million investment, scheduled for late 2025 startup. The facility leverages sustainable ethanol feedstock to supply low-carbon solvents aligned with EU climate objectives. Regulatory pressure is also increasing. The European Chemicals Agency updated its Key Areas of Regulatory Challenge in June 2025, pushing ethyl acetate producers toward New Approach Methodologies for safety evaluation. Despite these structural shifts, market conditions stabilized by Q4 2025, with balanced inventories and routine imports supporting pricing equilibrium across the region.

Belgium: Asset Exit and Portfolio Consolidation

Belgium’s role in the ethyl acetate value chain is transitioning from production to supply chain coordination. In October 2025, Celanese announced the planned closure of its Lanaken acetate tow facility by the second half of 2026. The decision was driven by declining demand and the site’s high energy intensity, reinforcing the trend toward consolidation away from legacy European assets.

Importantly, this exit does not signal withdrawal from the regional market. Celanese has reaffirmed its European commitments by reallocating supply responsibilities to higher-efficiency global sites, ensuring continuity for long-term customer contracts through 2026. For buyers, this shift underscores a growing reliance on globalized sourcing rather than local European production, with implications for logistics planning and risk management.

United States: Pricing Discipline and Demand Stability

The U.S. ethyl acetate market entered 2026 with relative stability compared to other regions. Gulf Coast producers announced price increases for oxo-derivatives and esters effective January 1, 2026, led by Eastman Chemical, citing the need to finance decarbonization and carbon-capture infrastructure. These adjustments reflect long-term capital requirements rather than immediate supply constraints.

Demand fundamentals remained balanced through late 2025. In October, FOB Gulf Coast ethyl acetate pricing held steady, supported by consistent consumption from automotive refinish coatings and flexible packaging applications. Unlike Europe, energy costs have been more predictable, allowing U.S. producers to maintain operational continuity while gradually embedding sustainability investments into their cost structures.

Strategic Snapshot: Ethyl Acetate Market by Country (2025–2026)

Ethyl Acetate Market County Level Snapshot

|

Country / Region

|

Primary Pressure Point

|

Strategic Response

|

Market Direction

|

|

India

|

Ethanol diversion to fuels

|

Lean savings, renewables, capacity expansion

|

Export volume recovery

|

|

China

|

Self-sufficiency mandate

|

Digitalized, integrated Verbund assets

|

Import substitution

|

|

Germany

|

Energy cost inflation

|

Asset rationalization, bio-based solvents

|

Structural contraction

|

|

Belgium

|

Legacy asset inefficiency

|

Portfolio consolidation

|

Supply chain realignment

|

|

United States

|

Decarbonization capex

|

Price indexation, stable demand

|

Gradual normalization

|

Ethyl Acetate Market Report Scope

Ethyl Acetate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.7 Billion

|

|

Market Size (2034)

|

$13.7 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Product Type (Synthetic Ethyl Acetate, Bio-Based Ethyl Acetate), By Purity Grade (Industrial Grade, Food and Pharmaceutical Grade, Electronic Grade), By Application (Paints and Coatings, Adhesives and Sealants, Process Solvents, Printing Inks, Food and Beverages, Cosmetics and Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Celanese Corporation, BASF SE, Eastman Chemical Company, INEOS Group, China Petroleum & Chemical Corporation, Jubilant Ingrevia Limited, Daicel Corporation, Sekisui Chemical Co., Ltd., Laxmi Organic Industries Limited, Resonac Corporation, Guangdong Jiangmen Shiny Chemical Co., Ltd., Jiangsu Sopo Group Co., Ltd., Godavari Biorefineries Limited, Yip’s Chemical Holdings Limited, Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethyl Acetate Market Segmentation

By Product Type

- Synthetic Ethyl Acetate

- Bio-Based Ethyl Acetate

By Purity Grade

- Industrial Grade

- Food and Pharmaceutical Grade

- Electronic Grade

By Application

- Paints and Coatings

- Adhesives and Sealants

- Process Solvents

- Printing Inks

- Food and Beverages

- Cosmetics and Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethyl Acetate Industry

- Celanese Corporation

- BASF SE

- Eastman Chemical Company

- INEOS Group

- China Petroleum & Chemical Corporation

- Jubilant Ingrevia Limited

- Daicel Corporation

- Sekisui Chemical Co., Ltd.

- Laxmi Organic Industries Limited

- Resonac Corporation

- Guangdong Jiangmen Shiny Chemical Co., Ltd.

- Jiangsu Sopo Group Co., Ltd.

- Godavari Biorefineries Limited

- Yip’s Chemical Holdings Limited

- Wacker Chemie AG

*- List not Exhaustive