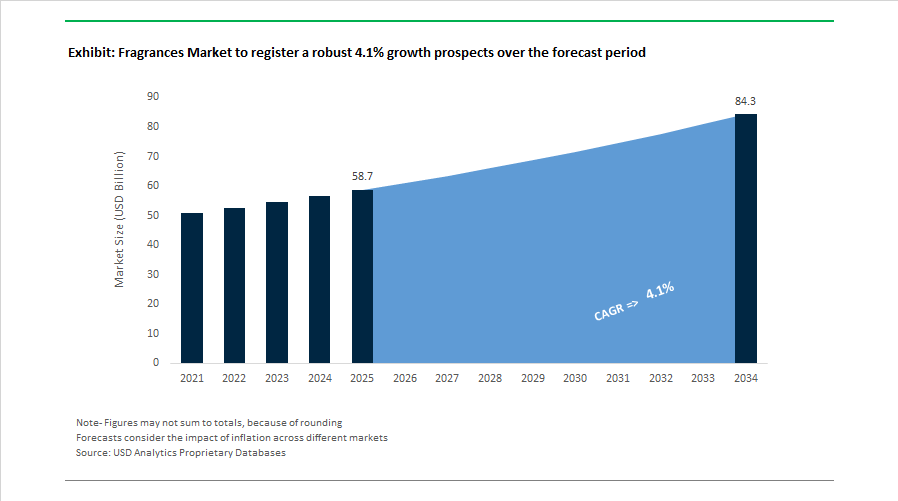

Fragrances Market Size 2025–2034: $58.7 Billion to $84.3 Billion at 4.1% CAGR Led by Luxury Consolidation and Portfolio Optimization

The Fragrances Market is projected to expand from $58.7 billion in 2025 to $84.3 billion by 2034, registering a CAGR of 4.1%. Market growth is being shaped by consolidation among luxury houses, expansion of prestige fragrance portfolios, omnichannel retail acceleration, and biotechnology-driven ingredient innovation. Fine fragrances, prestige perfumes, niche artisanal brands, and high-margin designer licenses remain primary growth drivers. Capital reallocation toward scent-focused divisions and divestment of non-core assets are redefining competitive positioning across multinational beauty conglomerates.

In early 2026, LVMH promoted Véronique Courtois to CEO of its Beauty Division, strengthening oversight of prestige fragrance brands including Christian Dior, Guerlain, and Maison Francis Kurkdjian after an 8% operating profit increase in perfumes and cosmetics during 2025. In January 2026, Coty launched its “Coty. Curated” strategic overhaul following new leadership appointment, refocusing on prestige fragrance houses such as Burberry and Marc Jacobs while evaluating divestment of mass-market brands to enhance margin profile. In February 2026, International Flavors & Fragrances confirmed continuation of its Food Ingredients divestment process after accelerating portfolio optimization through 2025, reinforcing capital concentration on its Scent and Health & Biosciences divisions.

Luxury consolidation intensified in late 2025. L’Oréal finalized acquisition of Kering Beauté, including the historic House of Creed, and secured 50-year exclusive fragrance licenses for Gucci, Bottega Veneta, and Balenciaga, marking a structural shift in the global luxury fragrance licensing landscape. In September 2025, Givaudan completed acquisitions of Belle Aire Creations in the United States and a majority stake in Vollmens Fragrances in Brazil, strengthening regional creative and supply capabilities across North America and Latin America. In October 2025, The Estée Lauder Companies opened a dedicated Fragrance Atelier in Paris to accelerate luxury scent development for Le Labo, Tom Ford, and Kilian Paris, all of which posted double-digit growth during 2025. In December 2025, dsm-firmenich launched its “Cloud Dancer” fragrance collection, integrating neuroscientific mapping and color psychology to align scent creation with emotional consumer data. Sephora, owned by LVMH, recorded record performance in 2025 driven by exclusive launches such as the Rhode brand, reinforcing the role of curated retail ecosystems in accelerating indie-prestige fragrance adoption.

Earlier structural repositioning began during 2024 and early 2025. Symrise debuted a green chemistry production process for L-Carvone in 2024 using renewable feedstocks and scaled the initiative in 2025, reducing wastewater and chemical waste by more than 30%. Throughout 2025, Coty completed divestment of its remaining 25.8% stake in Wella to KKR for $750 million, strengthening its balance sheet and reinforcing focus on fragrance innovation. International Flavors & Fragrances executed divestments of its Pharma and Nitrocellulose units during 2025 as part of a broader strategy to streamline operations around high-growth scent portfolios.

Trends and Opportunities Shaping the Global Fragrances Market

Strategic Pivot to Scent as a Service and Experiential Retail Platforms

Luxury fragrance houses are systematically shifting from single-point sales to recurring and service-oriented revenue models. By late 2025, subscription-based fragrance platforms such as Scentbird and ScentBox had transformed the discovery funnel by standardizing the try-before-you-buy model. These platforms expanded their libraries by hundreds of designer and niche scents during 2025 alone, reinforcing the rise of the “fragrance wardrobe” consumer who rotates scents by mood, season, and occasion.

Parallel to digital subscriptions, leading brands are reinvesting in physical experiential spaces. In October 2025, Estée Lauder inaugurated its Global Fragrance Atelier in Paris, positioning it as a high-touch innovation and artistry hub. These immersive labs allow consumers to interact directly with perfumers, raw materials, and formulation processes, creating a premium sensory experience that strengthens brand equity and justifies higher price points.

Commercial real estate and hospitality have become major adopters of scent-based engagement. According to 2025 disclosures from CBRE, a majority of hospitality investors are increasing capital allocation to luxury properties where olfactory branding is now embedded into guest experience design. Automated ambient scenting systems are being deployed as part of hyper-personalized environments to improve dwell time, guest satisfaction, and repeat visitation, positioning fragrance as a service layer rather than a consumable.

Data-Driven Perfumery and AI-Enabled Consumer Co-Creation

Artificial intelligence is now embedded across fragrance ideation, testing, and commercialization, fundamentally compressing development timelines. In February 2025, International Flavors & Fragrances launched ScentChat™, an AI-enabled interface that uses natural language processing to translate real-time consumer feedback into formulation insights. This allows perfumers to fine-tune accords during early development rather than post-launch, improving success rates and reducing reformulation costs.

AI-driven generation tools are also gaining commercial traction. In November 2024, NotCo introduced an AI fragrance formulator built on its proprietary databases, enabling rapid molecular simulation and sensory optimization. These systems replace traditional trial-and-error approaches with predictive modeling, allowing brands to respond faster to trend shifts and regional preferences.

At the consumer level, mass-premium personalization is expanding rapidly. Brands such as Maison 21G and EveryHuman now allow users to design bespoke perfumes digitally. By 2025, these platforms increasingly integrate social media behavior and contextual data to anticipate scent preferences, transforming fragrance into a data-informed lifestyle accessory rather than a static product.

Functional and Skin-Beneficial Fragrances Driving the Skin-Scent Convergence

The expansion of the global wellness economy is creating sustained demand for fragrances that deliver functional and skin-safe benefits. By 2024–2025, the functional fragrance segment reached a key inflection point as aromachology moved from niche to mainstream. Consumers are actively seeking fragrances formulated with bioactive components, such as linalool-rich fractions, that are supported by clinical evidence for stress reduction, sleep support, or mood enhancement.

This shift is opening high-margin opportunities in active skincare and spa-grade applications. Fragrance developers are increasingly focused on creating active-safe scent systems that remain stable in high-potency formulations containing retinoids, vitamin C, or exfoliating acids. The rise of medical-grade wellness tourism and therapeutic spa environments has further elevated fragrance from a masking ingredient to a core sensory intervention.

Haircare represents another underpenetrated growth avenue. By 2025, essential oils such as rosemary and lemongrass are being incorporated into fragrance profiles not only for scent appeal but also to support scalp health and hair vitality claims. This convergence of perfumery and trichology enables brands to command premium pricing while aligning with clean beauty and efficacy-driven narratives.

Olfactory Branding for Digital and Virtual Environments

One of the most disruptive opportunities lies at the intersection of fragrance and immersive technology. In December 2025, Scentient unveiled Escents, a wearable scent delivery device designed for VR and AR ecosystems. The system synchronizes scent release with digital content, enhancing realism for gaming, training simulations, and therapeutic environments.

E-commerce is another major beneficiary of digital scent innovation. In late 2024, Osmo demonstrated scent teleportation technology capable of capturing and transmitting odor signatures for digital analysis. This enables consumers to experience scent cues remotely before purchase, a capability expected to materially reduce return rates in online beauty and personal care retail.

By 2025, the digital scent technology space had become a focal investment area for North American tech hubs, with applications spanning entertainment, medical diagnostics, and virtual commerce. The convergence of electronic noses, scent synthesizers, and wearable delivery systems marks the emergence of a multi-billion-dollar adjacency, offering fragrance ingredient suppliers and brand owners a new frontier for long-term growth and differentiation.

Fragrances Market Share and Segmentation Insights

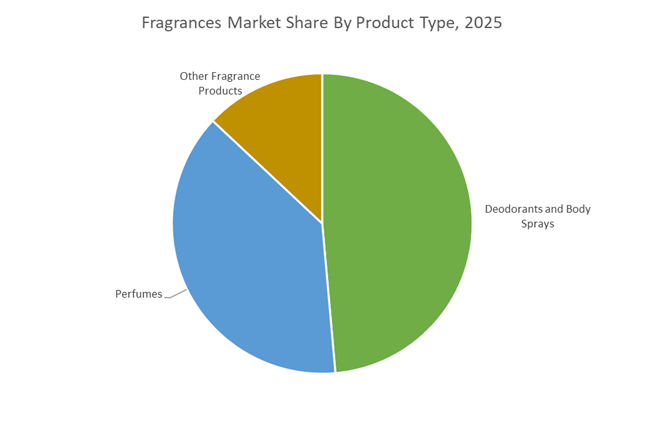

Deodorants and Body Sprays Lead the Global Fragrances Market Through High-Frequency Consumer Usage

Deodorants and Body Sprays accounted for 48.60% of the Fragrances Market share in 2025, making them the largest product category within the global fragrance industry. Their leadership stems from their role as daily-use personal grooming essentials, purchased frequently by consumers across all age groups and demographics. Compared with traditional perfumes, deodorants and body sprays are typically positioned at accessible price points, allowing mass-market penetration in both developed and emerging markets. These products combine odor protection, freshness, and fragrance appeal, making them an integral part of daily hygiene routines. In 2025, the segment is undergoing notable premiumization driven by evolving consumer expectations around skin health and sensory experience. Many brands are introducing next-generation deodorant formulations featuring fine-fragrance quality scent compositions, aluminum-free active systems, botanical ingredients, and dermatologically tested formulations. These products aim to provide both functional performance and a luxury fragrance experience typically associated with higher-end perfumes. As consumers increasingly trade up from traditional mass-market deodorants to premium personal care fragrances, the deodorants and body sprays category continues to generate strong volume and value growth within the global fragrances market.

Personal Care Products Drive the Largest Demand for Fragrance Across Consumer Product Categories

Personal Care represented 48.70% of the Fragrances Market share in 2025, establishing it as the largest application segment for fragrance ingredients and fragrance formulations. Personal care products—including shower gels, body lotions, deodorants, shampoos, conditioners, and skincare products—are used daily by billions of consumers, creating consistent global demand for fragrances that enhance the sensory appeal of these products. Fragrance is an essential element in personal care formulation, not only improving consumer experience and product differentiation, but also helping mask the base odors of active ingredients used in cosmetic and hygiene formulations. In 2025, a major behavioral trend influencing fragrance consumption is the rise of “scent layering” within personal care routines. Consumers increasingly combine multiple fragranced products—such as body wash, body lotion, deodorant, and hair care products—to create customized fragrance experiences that evolve throughout the day. This trend has encouraged brands to design coordinated fragrance collections across multiple personal care products, enabling consumers to build signature scent profiles through layering.

Competitive Landscape in Fragrances Market

Givaudan Maintains Global Leadership Through Fine Fragrance Surge and Regional Expansion

Givaudan S.A. remains the undisputed global leader in the fragrances market. For full-year 2025, the company reported CHF 7.5 billion in sales, reflecting 5.1% growth, with Fragrance & Beauty contributing CHF 3.83 billion. Fine Fragrance recorded an exceptional 18.3% surge, reinforcing premiumization trends across Europe, the Middle East, and Asia. In early 2026, Givaudan announced a $110 million investment in a new manufacturing hub in Mexico to serve high-growth Latin American demand under its regionalized production model. The company has transitioned to its 2030 Strategy, anchored by Campus 52, a CHF 55 million Swiss investment integrating production and innovation for natural fragrance development. In 2025, Givaudan achieved 100% renewable electricity across global operations, strengthening its ESG leadership while supporting scalable fragrance ingredient production.

dsm-firmenich Refocuses on Consumer Fragrance and Portfolio Simplification

dsm-firmenich, formed through the DSM and Firmenich merger, reported €9.03 billion in 2025 sales for continuing operations. While overall revenue growth remained flat, its Fine Fragrance division delivered high single-digit organic growth, signaling strength in premium scent categories. In February 2026, the company agreed to divest its Animal Nutrition & Health business for €2.2 billion, positioning itself as a pure-play leader in fragrance, taste, and beauty. Capital discipline was reinforced through a €500 million share repurchase program launched in Q1 2026 following portfolio simplification. Innovation efforts remain central, highlighted by the 2026 Scent of the Year, Frosted Star Anise, developed using proprietary Freezestorm cooling technology. This restructuring sharpens focus on high-margin fragrance compounds, biotech-derived ingredients, and consumer-centric olfactive design.

IFF Advances Operational Turnaround and High-Value Scent Innovation

International Flavors & Fragrances reported 2025 net sales of $10.89 billion, with the Scent segment contributing $2.48 billion, supported by double-digit growth in Fine Fragrance. For 2026, IFF forecasts revenue between $10.5 billion and $10.8 billion, with capital expenditure projected at approximately 6% of sales to support R&D expansion. The company completed the sale of its Pharma Solutions business in 2025 and expects closure of the Soy Crush and Lecithin divestiture by March 2026 to streamline its portfolio. As of early 2026, IFF holds 849 granted U.S. patents, underscoring its technological depth, particularly in LMR Naturals, which focuses on traceable and sustainable natural extracts. This innovation intensity, combined with portfolio optimization, reinforces IFF’s competitiveness in premium fragrance creation and specialty aroma ingredients.

Symrise Strengthens Margin Discipline and Diversified Fragrance Platforms

Symrise AG reported approximately €4.9 billion in revenue in 2025 and maintains an EBITDA margin near 21.5%, supported by the ONE SYM transformation program. The initiative aims to deliver €40 million in recurring cost savings by the end of 2026 through supply chain optimization and operational efficiency. In late 2025, Symrise issued an €800 million Eurobond to refinance debt and fund expansion into adjacent growth segments such as probiotics and functional scents. The company differentiates itself through its Beauty+ strategy, which integrates fragrance with cosmetic active ingredients. This cross-functional model enhances value capture in premium personal care and skincare formulations.

Takasago Expands Asian Footprint with Multicultural and AI-Driven Innovation

Takasago International Corporation recorded net sales of JPY 229.2 billion for the fiscal year ending March 2025, with fragrance sales expanding by 18.8%. The company inaugurated a Taste & Scent Innovation Centre in Bengaluru in May 2025 and is finalizing a pharmaceutical intermediates facility in Japan, strengthening its advanced synthesis capabilities. Its Global Pulse TrendSeeds 2026 forecast identifies Inner Balance and Technovation as primary consumer drivers, reflecting demand for emotionally resonant and AI-assisted scent discovery. Takasago has aligned corporate sustainability targets with a 1.5°C pathway, committing to net-zero greenhouse gas emissions across its value chain by 2050. With strong asymmetric synthesis expertise and deep multicultural consumer insight, Takasago remains the leading Asian fragrance house within the global fragrances market.

France: Regulatory Leadership Forcing Structural Reformulation and Data Overhaul

France remains the global rule-setter for the fragrances market, with regulatory enforcement directly reshaping formulation strategies, product architecture, and go-to-market execution. French fragrance houses are at the forefront of compliance with Regulation (EU) 2023/1545, which mandates individual labeling of 56 additional fragrance allergens by July 31, 2026, increasing the total to 80 declarable substances. This requirement is triggering a fundamental overhaul of SKU databases, packaging workflows, and supply chain traceability, particularly for multi-variant fine fragrance portfolios where label real estate is limited. As a result, reformulation toward lower-allergen fragrance bases and simplified accords is accelerating across both prestige and masstige segments.

Sustainability regulation is compounding this shift. France’s national ban on per- and polyfluoroalkyl substances in cosmetics and fragrances, effective January 1, 2026, is forcing a rapid exit from fluorinated fixatives and film-formers previously used for longevity and diffusion control. This has materially increased demand for biodegradable musks and bio-sourced fixative systems. In response, dsm-firmenich scaled its Castets facilities to full capacity in 2025, focusing on biotechnological synthesis of Habanolide and pine-based ingredients aligned with Green Beauty standards. Parallel innovation is underway at Mane, which expanded Grasse-based R&D following its 2025 U.S. asset acquisition to scale sclareolide production as a sustainable alternative to ambergris-derived notes in fine fragrances.

United States: Transparency Mandates and Generative Innovation Reshaping Brand Strategy

The United States fragrances market is entering a new compliance and innovation cycle driven by federal disclosure mandates and AI-led molecule design. Under the Modernization of Cosmetics Regulation Act, the U.S. Food and Drug Administration is finalizing its May 2026 rulemaking for mandatory fragrance allergen disclosure. This aligns U.S. transparency requirements more closely with European standards and is forcing domestic perfume brands to reassess ingredient sourcing, fragrance briefs, and long-term reformulation pipelines well ahead of enforcement.

On the supply side, portfolio restructuring is strengthening access to compliant specialty inputs. In October 2025, Honeywell completed the spin-off of its specialty chemicals division as Solstice Advanced Materials, sharpening focus on low-GWP aerosol propellants and high-purity solvents used in premium fragrance delivery systems. Innovation dynamics are also shifting upstream, with Osmo integrating AI-designed fragrance molecules such as Glossine, Fractaline, and Quasarine into commercial pilots across 2024–2025. At the brand level, The Estée Lauder Companies’ minority investment in Mexico-based luxury house XINÚ in November 2025 signals a strategic pivot toward narrative-driven niche fragrances aimed at high-growth, culturally anchored consumer segments.

Mexico: Botanical Luxury and Design-Led Fragrance Manufacturing

Mexico is rapidly emerging as a differentiated hub within the global fragrances market, driven by foreign direct investment, indigenous ingredient sourcing, and design-centric brand building. By late 2025, Mexico had attracted significant investment from U.S. fragrance conglomerates seeking access to locally inspired olfactory narratives rooted in botanical materials such as Mexican tuberose and copal. This positioning aligns Mexico with the growing global demand for authentic, origin-driven luxury fragrances.

Domestic niche players are scaling with international ambition. Brands such as XINÚ have expanded olfactory production and industrial design capabilities, combining artisanal fragrance development with avant-garde packaging engineered to meet European and North American luxury standards. This evolution is transforming Mexico from a sourcing destination into a full-spectrum fragrance innovation ecosystem capable of competing in the global prestige segment.

China: Regulatory Acceleration and Digital Transparency Enabling Faster Market Entry

China’s fragrances market is entering a structurally faster launch cycle following comprehensive regulatory streamlining. On November 17, 2025, the National Medical Products Administration introduced 24 reform measures that removed overseas sales record requirements for many imported fragrance categories. This change is significantly reducing regulatory lead times and enabling international prestige brands to synchronize China launches with global rollouts in 2026.

Digital infrastructure is reinforcing this acceleration. From February 1, 2026, the Shanghai Municipal government will pilot QR-code based electronic labeling, allowing fragrance brands to disclose full ingredient and allergen information digitally rather than on constrained physical packaging. On the supply side, the Prigiv joint venture between Givaudan and Privi Speciality Chemicals reached full operational capacity by 2025, ensuring localized access to high-volume aroma chemicals and reducing import dependency for China’s expanding personal care and home fragrance sectors.

India: Biomanufacturing Policy and Feedstock Security Supporting Export Growth

India’s fragrances market is being structurally strengthened by biotechnology policy support and upstream feedstock stabilization. In 2025, India’s BioE3 Policy began funding biomanufacturing hubs focused on bio-based aroma chemicals and enzymatic synthesis, enabling a gradual shift away from petroleum-derived intermediates. These initiatives are particularly relevant for natural perfumes, attars, and wellness-aligned fragrance formats where sustainability credentials are increasingly decisive in export markets.

Feedstock security is also improving. The Ministry of Petroleum and Natural Gas extended the OALP-X licensing round to February 18, 2026, offering nearly 200,000 square kilometers of acreage to support domestic petrochemical production critical for synthetic fragrance manufacturing. Complementing this, GST revisions implemented in September 2025 streamlined taxation on essential oil services, reducing friction across farm-to-fragrance logistics. Together, these measures are enhancing India’s competitiveness as a scalable supplier of both natural and synthetic fragrances for global brands.

Summary of Country-Level Strategic Drivers in the Fragrances Market

Fragrances Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Implications for the Fragrances Market

|

|

France

|

Allergen labeling and PFAS ban

|

Accelerated reformulation and bio-sourced fragrance systems

|

|

United States

|

MoCRA disclosure and AI innovation

|

Shift toward transparent, generative fragrance design

|

|

Mexico

|

Botanical luxury and FDI

|

Emergence as a niche fragrance innovation hub

|

|

China

|

Regulatory streamlining and digital labeling

|

Faster global launches and ingredient transparency

|

|

India

|

Biomanufacturing policy and feedstock access

|

Expansion of sustainable and export-oriented fragrances

|

Fragrances Market Report Scope

Fragrances Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$58.7 Billion

|

|

Market Size (2034)

|

$84.3 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Product Type (Perfumes, Deodorants and Body Sprays, Other Fragrance Products), By Price Category (Premium and Luxury, Mass Market and Mid-Range), By Ingredient Origin (Natural, Synthetic), By Consumer Demographic (Women, Men, Unisex), By Application (Fine Fragrances, Personal Care, Home Care), By Distribution Channel (Offline Retail, Online Retail)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Givaudan SA, DSM-Firmenich AG, The Estée Lauder Companies Inc., L’Oréal S.A., International Flavors & Fragrances Inc., Symrise AG, Coty Inc., LVMH Moët Hennessy Louis Vuitton, Chanel S.A., Puig, Shiseido Company, Limited, Inter Parfums, Inc., Takasago International Corporation, Mane SA, Hermès International

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fragrances Market Segmentation

By Product Type

- Perfumes

- Deodorants and Body Sprays

- Other Fragrance Products

By Price Category

- Premium and Luxury

- Mass Market and Mid-Range

By Ingredient Origin

By Consumer Demographic

By Application

- Fine Fragrances

- Personal Care

- Home Care

By Distribution Channel

- Offline Retail

- Online Retail

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fragrances Industry

- Givaudan SA

- DSM-Firmenich AG

- The Estée Lauder Companies Inc.

- L’Oréal S.A.

- International Flavors & Fragrances Inc.

- Symrise AG

- Coty Inc.

- LVMH Moët Hennessy Louis Vuitton

- Chanel S.A.

- Puig

- Shiseido Company, Limited

- Inter Parfums, Inc.

- Takasago International Corporation

- Mane SA

- Hermès International

*- List not Exhaustive