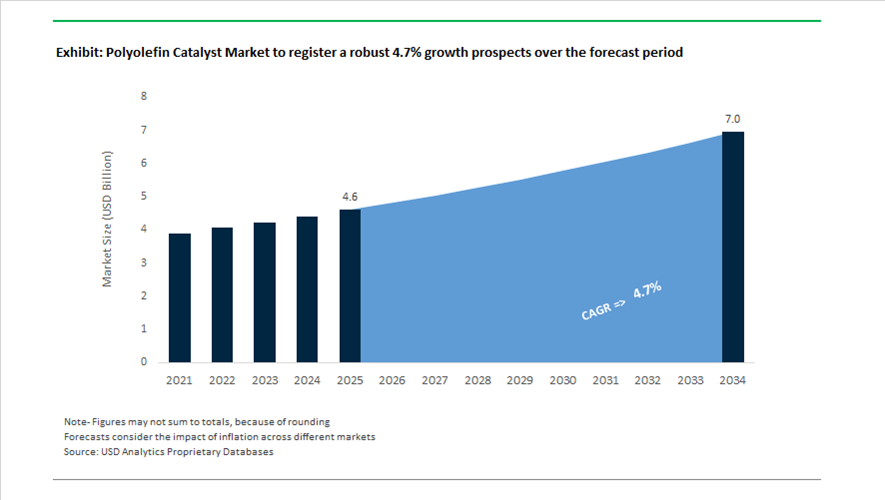

Polyolefin Catalyst Market Valued at $4.6 Billion in 2025, Projected to Reach $7 Billion by 2034 at 4.7% CAGR

The global polyolefin catalyst market is valued at $4.6 billion in 2025 and is projected to reach $7 billion by 2034, expanding at a CAGR of 4.7%. Growth is driven by rising capacity additions in polyethylene (PE), polypropylene (PP), linear low-density polyethylene (LLDPE), polyolefin elastomers (POE), and specialty polyolefins, particularly across China, the Middle East, and Southeast Asia. Increasing demand for metallocene catalysts, Ziegler–Natta systems, chromium-free catalysts, non-phthalate catalyst technologies, and aluminum alkyl co-catalysts such as TEAL and MMAO is reshaping the catalyst supply chain. Regulatory pressure on hazardous substances and carbon-intensive hydrogen production is accelerating adoption of cleaner catalytic chemistries and advanced process technologies.

In February 2024, W.R. Grace signed an agreement to double the licensed capacity of China Coal Shaanxi’s UNIPOL® PP reactor line in Yulin, incorporating Grace’s CONSISTA® catalyst systems. The expansion, commissioned in 2025, reinforces China’s ongoing investment in domestic polypropylene production. At NPE 2024, Clariant introduced PFAS-free AddWorks PPA polymer processing aids, enabling polyolefin film extruders to maintain processing efficiency without fluorinated additives. This shift reflects increasing compliance requirements across North America and Europe, particularly regarding PFAS elimination in polyolefin processing environments.

Strategic realignments intensified in 2025. In January 2025, Grupa Azoty and Orlen entered formal discussions regarding potential consolidation of polyolefin assets to stabilize the regional polyethylene supply chain and associated catalytic inputs. In May 2025, Honeywell reached an agreement to acquire Johnson Matthey’s Catalyst Technologies business for approximately $2.3 billion, with closure expected by mid-2026. The transaction integrates Johnson Matthey’s advanced catalyst manufacturing and licensing capabilities into Honeywell’s UOP portfolio, significantly expanding its footprint in polyolefin and refining catalysts. In June 2025, SHCCIG Yulin Chemical selected LyondellBasell’s fifth-generation Spheripol and Hostalen ACP technologies for a major petrochemical complex in China, deploying advanced non-phthalate catalysts to produce high-performance and durable polyolefin grades.

Domestic catalyst innovation gained momentum in July 2025 when China Coal Shaanxi Energy & Chemical announced industrial implementation of its first custom-designed catalyst, co-developed with Liaoning Dingjide. Tailored for Unipol PP units, the system demonstrated a 5% increase in activity retention, reducing reliance on imported catalyst platforms. In October 2025, Nouryon doubled triethylaluminum (TEAL) capacity at its Jiaxing facility in China, strengthening supply of this critical aluminum alkyl co-catalyst used in virtually all modern polyethylene and polypropylene production. Nouryon also confirmed plans to commence Modified Methylaluminoxane (MMAO) production in China by 2027, supporting metallocene catalysts for polyolefin elastomers widely used in solar panel encapsulants and high-performance films.

In December 2025, Mitsui Chemicals, Idemitsu Kosan, and Sumitomo Chemical signed a definitive agreement to integrate Sumitomo’s Japanese polypropylene and LLDPE businesses into Prime Polymer, effective 2026. This consolidation aims to optimize catalyst R&D efficiency in a contracting domestic market while strengthening export competitiveness. Clariant’s HySat™ chromium-free catalyst platform received recognition in 2025 for eliminating hexavalent chromium in hydrogenation processes linked to polyolefin value chains, ensuring compliance with REACH regulations. In September 2025, Clariant entered a supply agreement with SYPOX to manufacture catalysts for a large-scale electric steam methane reformer scheduled for 2026 operation, facilitating lower-carbon hydrogen feedstock for downstream polymerization.

The polyolefin catalyst market is increasingly shaped by non-phthalate catalyst systems, chromium-free hydrogenation catalysts, PFAS-free processing aids, TEAL and MMAO capacity expansions, domestic catalyst substitution in China, and mega-scale polypropylene licensing agreements. Consolidation among Japanese and European producers, large-scale investments in China, and integration of refining and polyolefin catalyst portfolios are redefining competitive positioning across global polyethylene and polypropylene production networks.

Key Trends and High-Growth Opportunities in the Polyolefin Catalyst Market

Strategic Capacity Expansion for Single-Site Catalysts Driven by Premium Product Demand

The polyolefin catalyst market is undergoing a decisive shift from volume-driven Ziegler-Natta systems toward metallocene and single-site catalyst (SSC) platforms that enable premium-grade polyolefins. This transition is being driven by end markets such as medical packaging, automotive lightweighting, and consumer electronics, where narrow molecular weight distribution, uniform comonomer incorporation, and optical clarity translate directly into pricing power and long-term supply contracts.

Licensing activity has accelerated accordingly. In June 2024, W. R. Grace & Co. expanded its UNIPOL® PP process licensing agreement with Bharat Petroleum Corporation Limited, adding approximately 950 kilotons of polypropylene capacity across Indian facilities. The deployment of non-phthalate CONSISTA® catalyst systems allows BPCL to manufacture high-impact and high-clarity copolymers tailored for medical disposables and premium consumer goods, segments that are structurally insulated from commodity price cycles.

Upstream integration is emerging as a parallel strategy to secure catalyst performance. In March 2025, LyondellBasell approved the expansion of its Channelview Complex to include a new metathesis unit that converts ethylene into propylene. This investment ensures a stable supply of high-purity propylene feedstock for Avant catalyst-driven specialty polypropylene and propylene oxide production, reducing exposure to propylene market volatility while improving polymer consistency.

The Middle East is also repositioning toward performance-driven output. Alujain National Industrial Company selected advanced Spherizone reactor technology and specialized catalysts to produce 500 KTA of high-value polypropylene in Saudi Arabia, with capacity scaling through 2025. This move targets import substitution of high-end automotive and textile grades across the GCC, signaling a broader regional pivot from commodity exports to differentiated polyolefin solutions.

Accelerated Development of Catalysts for Circular and Alternative Feedstocks

The transition toward circular plastics is redefining catalyst design requirements. Conventional Ziegler-Natta catalysts are highly sensitive to oxygenates, nitrogen compounds, and sulfur residues commonly found in chemically recycled or bio-based feedstocks. As a result, catalyst developers are prioritizing poison-tolerant systems capable of maintaining activity, stereocontrol, and molecular weight consistency under variable feedstock purity.

A notable inflection point occurred in March 2025, when India’s Ministry of Science & Technology formalized an agreement with APChemi to commercialize purified pyrolysis oil. This initiative aims to enable domestic production of circular polyolefins, but it simultaneously elevates the importance of advanced catalyst systems that can tolerate trace impurities without sacrificing reactor productivity or polymer quality.

Mass-balance circular feedstocks are already scaling at industrial levels. By 2025, producers such as SABIC and ExxonMobil had integrated ISCC PLUS-certified circular streams into commercial polyolefin production. These drop-in solutions rely on catalyst platforms engineered to stabilize molecular weight distribution even when recycled feedstock blending ratios fluctuate, ensuring that downstream converters receive consistent resin performance.

Looking further upstream, BASF’s 2024 announcement of commercial-scale Metal-Organic Framework (MOF) production marks an early step toward carbon-to-polymer pathways. With several hundred tons per year of MOF capacity now available, these materials are being evaluated as catalyst supports and selective adsorbents for CO₂-derived feedstocks, positioning advanced catalyst chemistry at the center of long-term decarbonization strategies.

Enabling Polyolefin Elastomers and Plastomers for EV Lightweighting and Solar Growth

Polyolefin Elastomers and Plastomers represent one of the fastest-growing catalyst-driven segments, underpinned by electric vehicle electrification and photovoltaic expansion. These materials require precise comonomer distribution, achievable only through single-site catalyst systems, to deliver the flexibility, dielectric strength, and durability demanded by next-generation applications.

China has emerged as the epicenter of POE capacity expansion. By late 2025, domestic POE capacity was doubling, led by large-scale investments from Wanhua Chemical and Sinopec Maoming. Wanhua alone is expected to reach 600,000 tons per year of POE capacity by year-end 2025, primarily serving EV wire and cable insulation as well as solar encapsulant films. According to December 2025 ICIS assessments, total Chinese POE capacity reached approximately 640,000 tonnes per year by Q4, significantly reducing reliance on imported high-octene copolymers.

The photovoltaic sector provides additional tailwinds. China’s cumulative solar capacity additions reached around 240 GW by September 2025, driving sustained demand for POE encapsulants with superior UV resistance and moisture barrier properties. Catalyst systems that enable consistent comonomer incorporation are critical to achieving the 25-year service life now expected of modern solar modules, creating long-duration demand visibility for POE catalyst suppliers.

Supply of Catalysts for High-Melt-Strength Polypropylene Applications

High-Melt-Strength Polypropylene is transitioning from a niche material into a mainstream solution for lightweight foams, thin-wall packaging, and industrial molding. Unlike conventional PP, HMS-PP requires catalysts capable of inducing long-chain branching directly in the reactor, eliminating the need for post-reactor modification.

In May 2025, Borealis announced an investment exceeding €100 million to triple capacity for its Daploy™ HMS-PP at the Burghausen site, with the new line scheduled to come online by 2026. This expansion targets fully recyclable foam solutions for automotive interiors, HVAC insulation, and construction materials, sectors under mounting pressure to reduce weight and improve circularity.

Catalyst innovation is increasingly focused on enhancing the strain-hardening index of polypropylene. Co-developed systems from major producers are enabling up to 15% weight reduction in automotive trim and HVAC ducting through advanced foaming techniques, without compromising impact resistance or dimensional stability. These performance gains are directly linked to catalyst-controlled molecular architecture rather than downstream processing alone.

Regulatory dynamics are reinforcing this opportunity. The EU Packaging and Packaging Waste Regulation 2025/351 is accelerating the phase-out of phthalate-based donor systems, particularly in applications with migration and traceability requirements. This creates a clear opening for non-phthalate HMS-PP catalyst platforms that combine regulatory compliance with the melt strength required for recyclable protective packaging and e-commerce logistics.

Polyolefin Catalyst Market Share and Segmentation Insights

Ziegler-Natta Catalysts Lead Global Polyolefin Catalyst Consumption in Polyethylene and Polypropylene Production

Ziegler-Natta catalysts accounted for 52.80% of the Polyolefin Catalyst Market by catalyst type in 2025, reflecting their critical role in large-scale polyethylene and polypropylene manufacturing. These catalysts remain the industry standard due to their cost efficiency, operational reliability, and compatibility with gas phase, slurry phase, solution phase, and bulk polymerization technologies used across polyolefin production facilities. Continuous catalyst optimization has enabled manufacturers to tailor polymer properties such as molecular weight distribution, stereoregularity, and particle morphology for specific industrial applications. In 2025, fourth generation Ziegler-Natta catalyst systems are improving polypropylene performance, enabling production of advanced grades with enhanced stiffness impact balance and optical clarity that compete with metallocene based polymers while maintaining economic advantages in high volume polyolefin production.

Packaging Industry Drives Polyolefin Catalyst Demand Through High-Volume Polyethylene and Polypropylene Applications

Packaging represented 48.60% of the Polyolefin Catalyst Market by end-use industry in 2025, supported by the extensive use of polyethylene and polypropylene in flexible films, rigid containers, protective packaging, and food packaging materials. Polyolefin catalysts enable the precise polymer architecture required to achieve film clarity, sealing performance, mechanical strength, and barrier properties demanded by modern packaging applications. The global expansion of e-commerce and consumer packaged goods continues to increase polyolefin packaging production worldwide. In 2025, catalyst innovation supporting recyclable mono-material packaging structures is gaining importance, with new catalyst technologies enabling polyethylene and polypropylene grades that replace multilayer packaging while improving compatibility with recycled content streams.

Polyolefin Catalyst Market Competitive Landscape

The global polyolefin catalyst market is transitioning toward metallocene catalysts, circular feedstock processing, and ultra-high-purity polymer production. Competitive dynamics are shaped by catalyst-process integration, sustainability mandates, and demand from EV, photovoltaic, and medical-grade polymer applications requiring precise molecular weight control.

LyondellBasell Expands Metallocene Leadership with Avant™ Catalysts and Global Licensing Dominance

LyondellBasell Industries remains the dominant force in polyolefin catalysts, leveraging its Avant™ catalyst portfolio and unmatched licensing ecosystem. The company is restructuring its European asset base in 2026 to prioritize high-growth catalyst technologies and its MoReTec chemical recycling platform. Its large-scale licensing agreement with SHCCIG Yulin integrates Spheripol, Spherizone, Hostalen ACP, and Lupotech T technologies to produce advanced PP and EVA for solar and EV applications. Despite margin compression in 2025, LYB exceeded its cost-saving targets and increased its 2026 financial optimization goal to $1.3 billion. Its Metocene PP technology enables production of high-clarity, high-strength polypropylene for medical and electronics markets. Strategy centers on licensing scale, circular polymerization, and precision metallocene catalyst systems.

W. R. Grace Strengthens Custom Catalyst Leadership with ActivCat® and Silica-Based Technologies

W. R. Grace & Co. leads the independent polyolefin catalyst segment through advanced customization and silica-based catalyst carriers. Its ActivCat® technology enhances metallocene catalyst efficiency, supporting production of PE-RT pipe resins with superior durability and chemical resistance. Grace’s mLLDPE catalyst systems are widely adopted in high-performance flexible packaging, delivering enhanced toughness and sealability. The expansion of CONSISTA® and HYAMPP® catalyst lines ensures compliance with non-phthalate requirements in food-contact and medical-grade polymers. Its SYLOID® and LUDOX® platforms underpin nearly half of global polyolefin catalyst production. Strategy focuses on catalyst customization, regulatory alignment, and high-performance polymer applications.

Clariant Advances Circular Catalyst Technologies with HDMax™ and Titanium-Based Solutions

Clariant AG is positioning itself as a sustainability-driven innovator in polyolefin catalysts, focusing on circular economy integration. Its HDMax™ catalyst technology enables single-step conversion of pyrolysis oil into cracker-grade feedstock, bridging mechanical and chemical recycling. The company’s titanium-based catalysts provide a high-performance, antimony-free alternative for PET production, aligning with global regulatory shifts. Clariant achieved a 17.8% EBITDA margin in 2025, supported by strong catalyst demand and operational efficiency improvements. Its catalyst business continues to benefit from energy-efficient ethylene and syngas technologies. Strategy emphasizes low-carbon catalysis, recycling integration, and regulatory-compliant innovation.

Mitsui Chemicals Accelerates Specialty Transition with Metallocene Catalysts and Vertical Integration

Mitsui Chemicals is transitioning toward high-value specialty catalysts, supported by strategic consolidation and vertical integration. The integration of Sumitomo Chemical’s PP and LLDPE businesses into Prime Polymer enhances Japan’s global competitiveness in polyolefins. The acquisition of Nippon Aluminum Alkyls secures critical co-catalyst supply, strengthening Mitsui’s catalyst production chain. Its Diffrar™ optical polymer wafer demonstrates advanced applications enabled by metallocene catalyst precision in AR technologies. The Biomass Evolue™ LLDPE platform highlights the company’s capability to process renewable feedstocks using advanced catalysts. Strategy centers on specialty materials, supply chain integration, and sustainable polyolefin innovation.

INEOS Enhances Process-Catalyst Synergy with INcat™ Portfolio and High-Throughput R&D

INEOS is leveraging its integrated polyolefin production expertise to develop operator-focused catalyst systems under the INcat™ brand. Its P-series non-phthalate catalysts and M-series metallocene catalysts enable efficient production of advanced polyethylene and polypropylene grades. The company utilizes high-throughput experimentation across global R&D centers to accelerate catalyst discovery and commercialization. INEOS catalysts are optimized for direct reactor injection, eliminating pre-polymerization steps and reducing operational costs. Its Innovene™ process integration ensures seamless catalyst performance for licensees. Strategy focuses on process synergy, operational efficiency, and advanced metallocene catalyst deployment.

Evonik Targets High-Margin Catalyst Segments with Circular Polymer and Advanced Materials Focus

Evonik Industries is focusing on specialty polyolefin catalysts aligned with circular polymerization and advanced material applications. Following the spin-off of SYNEQT in 2026, the company is concentrating resources on high-margin additives and catalyst innovation. Evonik reported €1.87 billion EBITDA in 2025 and is targeting up to €2.0 billion in 2026, driven by its Advanced Technologies segment. Its catalysts support high-performance plastics used in 3D printing, membranes, and EV-related applications requiring superior mechanical stability. The company is reinvesting free cash flow into hydrogen economy and circular polymer initiatives. Strategy emphasizes specialty catalyst development, sustainability, and next-generation polymer applications.

China: Policy-Driven Self-Sufficiency and Scale Expansion in High-End Polyolefin Catalysts

China remains the most structurally influential market in the global polyolefin catalyst industry, with 2025 marking a decisive acceleration toward catalyst self-sufficiency and large-scale deployment of licensed technologies. In September 2025, the Ministry of Industry and Information Technology released a dedicated petrochemical work plan for 2025 to 2026, explicitly prioritizing domestic capability in high-end polyolefin catalysts as part of a broader target to achieve 5% annual growth in chemical added value. This policy signal has translated into aggressive capacity build-outs and technology selection favoring advanced catalyst systems. In June 2025, SHCCIG Yulin Chemical selected technology packages from LyondellBasell, including Spheripol and Hostalen ACP processes, to support 1,100 KTA of combined polypropylene and polyethylene capacity using Avant catalyst systems optimized for grade consistency and reactor efficiency.

Operational scale-up continued across state-linked producers. China Coal Shaanxi Company doubled polypropylene output to 600 KTA at its Yulin facility during 2025, deploying W.R. Grace CONSISTA® non-phthalate catalysts integrated with UNIPOL® process control software. Beyond commodity polymers, China’s renewable energy strategy is reshaping catalyst demand profiles. Domestic producers are rapidly adopting Lupotech T catalyst technology licensed from LyondellBasell to manufacture EVA copolymers for photovoltaic encapsulants, a critical material class under China’s 2026 solar deployment targets. Simultaneously, domestic catalyst-focused enterprises such as Dongguan Grand Resource commissioned new polypropylene reactor lines totaling 1,200 KTA in 2025, relying on high-performance CONSISTA® catalyst architectures. Collectively, these developments reflect measurable progress toward the Made in China 2025 benchmark of achieving 70% domestic content in core chemical materials, including metallocene and chromium-based polyolefin catalysts.

India: Refinery-to-Petrochemical Integration and Localization of Ziegler-Natta Systems

India’s polyolefin catalyst market in 2025 is being reshaped by refinery-to-petrochemical integration and policy-backed localization of catalyst R&D. In November 2025, Nayara Energy commissioned its 450 KTA polypropylene plant at Vadinar, Gujarat, utilizing UNIPOL® PP technology from W.R. Grace combined with non-phthalate catalyst systems. The facility is strategically oriented toward medical, hygiene, and specialty packaging applications, segments that require tighter molecular weight distribution and consistent catalyst performance. Downstream investment momentum remains strong. HMEL announced a ₹2,600 crore investment in 2025 to expand polypropylene downstream units and fine chemical projects, directly increasing demand for localized catalytic processing and reactor optimization expertise.

At the policy level, India’s Atmanirbhar agenda continues to influence catalyst development pathways. The Production Linked Incentive scheme for chemicals has accelerated domestic research into Ziegler-Natta catalyst variants tailored for India’s upcoming polyethylene and polypropylene capacity additions planned for 2026. Complementing this, the Office of the Principal Scientific Adviser to the Government of India confirmed plans in late 2025 to expand national Science and Technology clusters from eight to twenty-five, with a defined focus on advanced materials and performance additives. Digitalization is also gaining traction. Indian polyolefin producers integrated UNIPOL UNIPPAC® digital process control platforms during 2025 to improve catalyst mileage, stabilize polymer grades, and reduce unplanned reactor downtime in high-output plants. These factors collectively position India as a fast-evolving catalyst consumption market anchored in localization, digital optimization, and downstream diversification.

Germany: Energy-Aware Innovation and Circular Catalyst Design Leadership

Germany’s polyolefin catalyst industry in 2025 is characterized by energy cost mitigation strategies, advanced catalyst engineering, and early leadership in circular polymer systems. In July 2025, the European Commission introduced its Competitiveness Action Plan for the Chemicals Industry, a framework designed to protect German catalyst producers from sustained high gas prices while reinforcing innovation capacity. Within this environment, BASF finalized the commercial rollout of its X3D catalyst technology, leveraging 3D printing to produce complex catalyst geometries that enhance reactor throughput and energy efficiency.

Circularity-driven innovation is gaining strategic prominence. In September 2025, Evonik launched its Next Markets Program, targeting catalyst solutions for pyrolysis-based chemical recycling of mixed polyolefin waste streams. At the K 2025 trade fair in Düsseldorf, German producers showcased switchable catalyst systems that enable rapid grade transitions within a single reactor, significantly reducing off-spec polymer volumes and production losses. Financial alignment with climate objectives is also strengthening. German chemical clusters adopted the updated Transition Finance Roadmap in 2025, securing funding for electrified catalyst production assets aligned with 2030 emissions targets. Germany’s market profile thus reflects a blend of cost-aware policy support, frontier catalyst design, and circular polymer enablement.

United States: Capacity Expansion and Performance-Driven Catalyst Demand

The United States polyolefin catalyst market in 2025 is increasingly shaped by long-term capacity expansion plans and application-specific performance requirements. ExxonMobil confirmed plans to add approximately 3 million tons of new polyethylene capacity by 2031, a trajectory that implies sustained demand for advanced metallocene catalyst supply agreements over the next decade. Regulatory navigation remains a parallel priority, with U.S. producers channeling R&D resources into PFAS-free catalyst processing aids to stay ahead of tightening state-level and federal environmental mandates.

High-purity polymer applications are exerting additional influence. In October 2025, LyondellBasell expanded its Purell medical-grade polymer portfolio across North America, relying on catalyst systems capable of meeting upcoming USP and EU Pharmacopeia standards effective in 2026. Infrastructure-led demand is also notable. The rapid expansion of data centers and electric vehicle infrastructure in 2025 has increased consumption of durable conduits and cable jacketing materials, produced using specialized high-stress-crack-resistant catalyst systems. These dynamics position the U.S. as a market where capacity scale, regulatory foresight, and high-performance end-use requirements collectively drive catalyst selection.

South Korea: Export-Oriented Capacity and Sustainable Catalyst Inputs

South Korea’s role in the polyolefin catalyst ecosystem is closely linked to export-oriented polymer production and sustainability-led process upgrades. In December 2025, Kumho Mitsui Chemicals approved a 100,000-ton MDI expansion, integrating recycling infrastructure into the catalytic process to reduce greenhouse gas intensity per unit of output. The Yeosu industrial hub reached full operation of a prior 200,000-ton capacity increase during the 2024 to 2025 period, reinforcing South Korea’s position as a major exporter of high-performance polyolefin intermediates.

Feedstock and catalyst sustainability are emerging priorities. Regional producers initiated a strategic shift toward greener alkoxide catalysts in 2025, supported by world-scale alkoxide production facilities in Singapore that supply the broader Asian market. This transition reflects rising customer expectations for lower lifecycle emissions across polymer value chains and positions South Korea as a technologically adaptive catalyst consumer and exporter.

Qatar: Feedstock Advantage and Export-Centric Catalyst Utilization

Qatar’s polyolefin catalyst demand in 2025 is anchored in large-scale integrated petrochemical projects and export dominance. In early 2025, QatarEnergy and Chevron Phillips Chemical advanced the Ras Laffan integrated complex, a $6 billion mega-project that will host the largest ethane cracker in the Middle East alongside two world-scale HDPE units. The project relies on advanced catalyst technologies to maximize yield and grade flexibility from low-cost ethane feedstocks.

Qatar reinforced its export leadership in 2025 by leveraging its feedstock advantage and access to state-of-the-art polyolefin catalyst systems to serve high-growth markets in India and China. As a result, Qatar’s catalyst consumption profile is characterized less by domestic diversification and more by scale-driven optimization for export-oriented polyethylene production.

Comparative Overview of Country-Level Dynamics in the Polyolefin Catalyst Industry

Polyolefin Catalyst Market County Level Snapshot

|

Country / Region

|

Core 2025 Focus Areas

|

Implications for Polyolefin Catalyst Demand

|

|

China

|

Self-sufficiency, licensed technologies, photovoltaic EVA

|

High-volume demand for metallocene and advanced ZN systems

|

|

India

|

Refinery integration, digital optimization, localization

|

Rising consumption of non-phthalate and customized ZN catalysts

|

|

Germany

|

Energy efficiency, circular polymers, 3D-printed catalysts

|

Demand for high-efficiency and switchable catalyst systems

|

|

United States

|

Capacity expansion, regulatory compliance, infrastructure

|

Long-term contracts for high-performance metallocene catalysts

|

|

South Korea

|

Export growth, sustainable alkoxides, MDI expansion

|

Increased use of low-emission and recyclable catalyst inputs

|

|

Qatar

|

Mega-scale ethane cracking, export orientation

|

Large-scale utilization of advanced HDPE catalyst technologies

|

Polyolefin Catalyst Market Report Scope

Polyolefin Catalyst Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.6 Billion

|

|

Market Size (2034)

|

$7 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Catalyst Type (Ziegler-Natta Catalysts, Metallocene Catalysts, Chromium Catalysts, Post-Metallocene & Specialty Catalysts), By Process Technology (Gas Phase Technology, Slurry Phase Technology, Solution Phase Technology, Bulk Phase Technology), By Polyolefin Product Type (Polyethylene, Polypropylene, Specialty Polyolefins), By End-Use Industry (Packaging, Automotive, Building & Construction, Medical & Healthcare, Energy & Electrical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

W. R. Grace & Co., LyondellBasell Industries N.V., BASF SE, Mitsui Chemicals Inc., INEOS Group, Chevron Phillips Chemical Company, Evonik Industries AG, Clariant AG, Albemarle Corporation, Univation Technologies LLC, Sinopec Group, Idemitsu Kosan Co. Ltd., Toho Titanium Co. Ltd., Johnson Matthey PLC, SABIC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polyolefin Catalyst Market Segmentation

By Catalyst Type

- Ziegler-Natta Catalysts

- Metallocene Catalysts

- Chromium Catalysts

- Post-Metallocene & Specialty Catalysts

By Process Technology

- Gas Phase Technology

- Slurry Phase Technology

- Solution Phase Technology

- Bulk Phase Technology

By Polyolefin Product Type

- Polyethylene

- Polypropylene

- Specialty Polyolefins

By End-Use Industry

- Packaging

- Automotive

- Building & Construction

- Medical & Healthcare

- Energy & Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polyolefin Catalyst Industry

- W. R. Grace & Co.

- LyondellBasell Industries N.V.

- BASF SE

- Mitsui Chemicals Inc.

- INEOS Group

- Chevron Phillips Chemical Company

- Evonik Industries AG

- Clariant AG

- Albemarle Corporation

- Univation Technologies LLC

- Sinopec Group

- Idemitsu Kosan Co. Ltd.

- Toho Titanium Co. Ltd.

- Johnson Matthey PLC

- SABIC

*- List not Exhaustive