PVDC Coated Films Market Size, Barrier Packaging Demand, and Pharmaceutical Growth

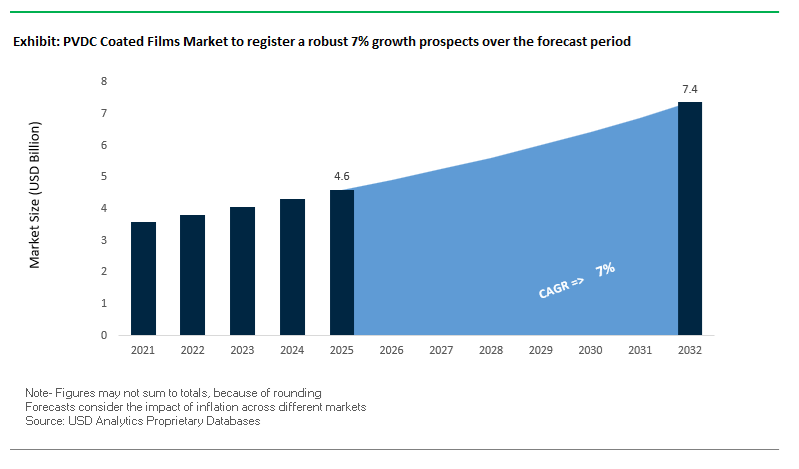

The global PVDC Coated Films Market was valued at $4.6 billion in 2025 and is projected to grow at a CAGR of 7.0% through 2032, reaching $7.4 billion by 2032. This growth is primarily driven by increasing demand for high-barrier packaging solutions across pharmaceuticals, food, and specialty industrial applications, where PVDC (polyvinylidene chloride) coatings deliver exceptional oxygen and moisture barrier performance.

PVDC-coated films are widely used in blister packaging, flexible food packaging, and laminated structures, particularly where extended shelf life and product stability are critical. Their ability to maintain low oxygen transmission rates (OTR) and resist permeability under high humidity conditions makes them indispensable for sensitive products such as medicines, processed foods, and nutraceuticals.

A key structural driver is the rapid expansion of the pharmaceutical packaging sector, especially in Asia-Pacific. The rising demand for unit-dose blister packs, sterile packaging, and temperature-sensitive drug protection is significantly increasing the consumption of PVDC-coated substrates. This is further supported by the growth of generic drug manufacturing and healthcare access in emerging economies.

In parallel, the food industry continues to adopt PVDC coatings for premium packaging applications, including snacks, dried fruits, and ready-to-eat products, where both visibility and barrier integrity are essential. However, the market is also undergoing a structural shift due to environmental concerns around chlorine-based polymers, leading to increased focus on recyclability, reduced halogen content, and hybrid barrier solutions.

Market Analysis: Pharma-Led Capacity Expansion, Low-Chlorine Formulations, and Sustainable Coating Technologies Driving Market Evolution

Recent developments in the PVDC Coated Films Market highlight a strong convergence of capacity expansion, sustainability-driven reformulation, and advanced coating technologies. In March 2026, Kureha Corporation expanded its PVDC resin capacity to over 100,000 metric tons annually, targeting the surge in pharmaceutical demand across Asia-Pacific, where blister packaging requirements increased significantly in the previous year.

Sustainability pressures are accelerating material innovation. Kureha’s 25% reduced-chlorine PVDC resin (December 2025) represents a critical step toward compliance with EU REACH regulations, enabling manufacturers to maintain high barrier performance while improving environmental compatibility. Similarly, SK Chemicals’ eco-friendly PVDC blends incorporate bio-derived content, improving recyclability of multilayer films by up to 40%, addressing one of the key limitations of traditional PVDC systems.

Application technology is also evolving. The shift toward PVDC latex (water-based coatings) in Europe, which saw a 14.2% year-on-year increase in adoption (2026), reflects the industry’s move toward low-VOC, solvent-free processing, aligning with stringent environmental standards.

Product innovation continues to enhance performance in high-value segments. UFlex’s BOPET-based PVDC film (September 2025) offers high clarity, flex-crack resistance, and stable barrier properties under humid conditions, targeting premium food packaging applications. Meanwhile, Bilcare’s strategic focus on unit-dose blister packaging (February 2026) highlights the growing importance of PVDC coatings in protecting sensitive pharmaceuticals in emerging markets.

Cost dynamics are influencing formulation strategies. The 14% increase in vinylidene chloride (VDC) monomer prices (2025) is driving manufacturers toward coating optimization, reducing PVDC layer thickness while combining it with complementary barrier materials to maintain performance at lower cost.

Regulatory developments remain a critical market force. The implementation of new EU REACH labeling requirements (January 2026) for chlorine-based polymers has triggered widespread R&D efforts focused on chlorine-free alternatives and hybrid PVDC systems, with more than 50 companies actively engaged in reformulation initiatives.

Market Trend: EU Regulatory Enforcement Accelerating Phase-Out of PVDC in Recyclable Packaging Structures

The PVDC coated films market is entering a critical transition phase as European regulatory frameworks intensify focus on recyclability and hazardous substance management. The convergence of the Packaging and Packaging Waste Regulation and updated CLP classification rules is shifting PVDC from a performance-driven material to a regulatory liability in flexible packaging applications.

The enforcement of Design for Recycling criteria under the EU framework, becoming strictly applicable from August 2026, requires that all packaging formats be recyclable at scale by 2030. PVDC coatings, widely used for their superior oxygen and moisture barrier properties, are increasingly categorized as recycling disruptors in polyolefin and PET streams. This classification is materially impacting packaging design decisions across food, pharmaceutical, and consumer goods sectors.

A critical compliance milestone is the November 1, 2026 deadline for updated hazard classification under CLP regulations. Coating manufacturers must ensure that all PVDC-based formulations comply with revised substance classifications or face immediate exclusion from the EU market. This is accelerating reformulation efforts and driving investment in alternative barrier technologies.

Recyclability grading criteria introduced in 2026 further intensify the pressure. Flexible packaging structures containing more than 1% chlorinated polymers by weight are now likely to be classified as non-recyclable under Grade D or Grade E categories. This classification triggers higher eco-modulation fees, directly impacting cost structures for brand owners and converters.

In addition, the regulatory nexus with PFAS is creating further complexity. Since PVDC coatings often rely on PFAS-based processing aids, the October 2026 requirement for industrial PFAS management plans is forcing manufacturers to conduct comprehensive chemical audits and identify substitute processing technologies. These combined regulatory pressures are accelerating the phase-out of PVDC in single-use packaging across Europe.

Market Trend: Japanese Circular Economy Standards Driving Transition Toward Monomaterial Packaging Solutions

Japan’s transition from voluntary recycling guidelines to enforceable design standards under the Plastic Resource Circulation Promotion Act is significantly impacting the PVDC coated films market. The introduction of stricter recyclability certification requirements in 2026 is reshaping material selection strategies among packaging manufacturers and brand owners.

The enforcement of “Easily Separable” design criteria, effective January 24, 2026, is particularly disruptive for multilayer packaging structures incorporating PVDC coatings. PVDC layers are difficult to separate from PET and polypropylene substrates during recycling, leading to their exclusion from A-grade recyclability certifications. This is reducing their viability in high-volume consumer packaging applications, especially in food and confectionery sectors.

As a result, major Japanese packaging users are accelerating the transition toward monomaterial solutions that are compatible with established recycling streams. Industry benchmarks indicate that leading confectionery companies are targeting up to 85% conversion to monomaterial packaging formats by the end of fiscal year 2026. This shift is driving demand for alternative high-barrier coatings such as water-based and inorganic barrier technologies.

The regulatory push is not only influencing domestic markets but also shaping export strategies, as Japanese manufacturers align with global recyclability standards. The emphasis on circular packaging design is expected to significantly reduce the role of PVDC in conventional flexible packaging, while creating opportunities for next-generation barrier materials that balance performance with recyclability.

Market Opportunity: SiOx Coating Technologies Enabling PVDC Replacement in High-Barrier Food Packaging Applications

The shift away from PVDC in North America is creating a strong opportunity for silicon oxide coating technologies as a drop-in replacement for high-barrier food packaging applications. SiOx-coated PET films are gaining traction among meat and cheese packaging manufacturers seeking to maintain product shelf life while meeting recyclability and regulatory requirements.

Barrier performance is a key advantage. SiOx-coated films are achieving oxygen transmission rates below 0.5 cc per square meter per day, effectively matching the performance of conventional PVDC coatings. At the same time, these films remain fully compatible with existing PET recycling streams, addressing one of the primary regulatory challenges associated with PVDC.

Optical clarity is another differentiating factor. SiOx coatings offer a 20% to 30% improvement in transparency compared to aged PVDC films, resulting in lower haze and improved product visibility. This is particularly important in retail packaging for fresh meat and dairy products, where visual appeal directly influences consumer purchasing behavior.

Operational efficiency benefits further strengthen the case for SiOx adoption. Unlike metallized films, SiOx coatings are microwave-transparent and do not interfere with in-line metal detection systems. This reduces false rejects and improves throughput efficiency, with processing facilities reporting up to a 12% reduction in waste-to-line ratios. These combined advantages position SiOx coatings as a leading alternative in the transition toward recyclable high-barrier packaging.

Market Opportunity: Modified PVDC Coatings Expanding into Durable Reusable Transit Packaging Applications

While single-use PVDC applications are facing regulatory headwinds, a niche growth opportunity is emerging in modified PVDC coatings for reusable transit packaging in industrial sectors such as automotive and aerospace. In these applications, performance requirements are centered on chemical resistance, durability, and lifecycle cost optimization rather than recyclability.

Modified PVDC coatings are demonstrating superior resistance to aggressive chemicals, including hydraulic fluids such as Skydrol, with performance improvements of approximately 40% compared to conventional epoxy and polyurethane coatings. This makes them well-suited for protecting sensitive components during transport and storage in harsh industrial environments.

Durability is a key value driver in reusable packaging systems. PVDC-modified liners used in automotive work-in-progress transit packaging have shown the ability to withstand up to 50 industrial wash cycles at temperatures of 70°C without delamination. This significantly reduces cost-per-use and supports circular logistics models adopted by Tier-1 automotive suppliers.

In addition, advancements in surface energy control are enabling new applications in aerospace tooling. Modified PVDC coatings can create low-surface-energy interfaces that reduce the need for external release agents by approximately 15% per production cycle. This improves process efficiency and reduces consumable usage in high-precision manufacturing environments.

These developments indicate that while PVDC is declining in traditional packaging markets, it retains strong potential in specialized, high-performance applications where durability and chemical resistance outweigh recyclability constraints.

PVDC Coated Films Market Share and Segmentation Insights: Double-Side Coating Dominance and Direct Supply Chain Optimization

By Coating Configuration: Double-Side Coated PVDC Films Lead with Superior Barrier Performance

The double-side coated PVDC films segment dominated the market with a 66.3% share in 2025, driven by its exceptional oxygen barrier and moisture barrier properties critical for high-performance packaging applications. These films provide hermetic sealing capabilities, making them essential for preserving oxygen-sensitive and high-moisture food products such as meat, cheese, coffee, and snack items, extending shelf life to 12+ months. The dual coating enhances barrier uniformity and product protection, positioning PVDC-coated films as a premium solution in the flexible packaging market. Additionally, double-side coated configurations offer heat seal compatibility on both surfaces, enabling greater flexibility in packaging design and processing without orientation limitations, unlike single-side coated alternatives. This versatility supports widespread adoption across food packaging, pharmaceutical packaging, and medical applications, reinforcing the segment’s leadership through enhanced shelf-life performance, sealing efficiency, and packaging reliability.

By Sales Channel: Direct Sales Channel Dominates with Customization and Supply Chain Reliability

The direct sales segment accounted for a leading 53.6% share of the PVDC coated films market in 2025, reflecting the increasing need for custom-engineered barrier film solutions and reliable supply partnerships. Large-scale food packaging companies and medical device manufacturers collaborate directly with film producers to develop tailored PVDC coating specifications, including precise coating weights, film thickness, and seal initiation temperatures to meet stringent performance and regulatory requirements. This direct engagement ensures optimal functionality in high-barrier packaging applications. Furthermore, long-term supply agreements enable consistent barrier performance, full lot traceability, and priority allocation during PVDC resin supply constraints, which is critical given the sensitivity of PVDC copolymer supply chains. By offering technical collaboration, quality assurance, and supply security, the direct sales channel continues to strengthen its dominance in the global PVDC coated films market.

Competitive Landscape of the PVDC Coated Films Market

Jindal Films Leads High-Barrier Innovation with Recyclable Mono-Material PVDC Solutions

Jindal Films is a global leader in the PVDC coated films market, leveraging its expertise in BOPP and BOPE technologies to deliver high-barrier, recyclable packaging solutions. Its Bicor™ range combines water-based PVDC coatings with Very Low-Temperature Seal (VLTS) technology, achieving oxygen barrier levels below 0.5 cm³/m²/day for high-speed packaging lines. The company has invested significantly in expanding its European production capabilities, targeting replacement of non-recyclable aluminum laminates. In 2026, Jindal achieved “Made for Recycling” certification for its PVDC-coated films, demonstrating strong alignment with circular economy goals while reducing material usage by up to 30%.

Mondi Drives Circular Packaging Innovation with Mono-Material PVDC Technologies

Mondi Group is a major player in the PVDC coated films market, focusing on sustainable flexible packaging solutions. Its MAP2030 initiative emphasizes replace, reduce, and recycle strategies, with mono-material PVDC films extending shelf life of fresh food by up to five times. The company has received multiple global awards for its packaging innovations and is actively replacing traditional multi-layer laminates with recyclable alternatives. Its partnerships, such as with Werner & Mertz, highlight its leadership in incorporating post-consumer recycled materials into high-barrier packaging systems.

Cosmo First Expands Specialty Film Portfolio with High-Barrier PVDC and Healthcare Applications

Cosmo First Limited, through its Cosmo Films division, is a key innovator in the PVDC coated films market, particularly in FMCG and pharmaceutical packaging. The company has expanded its specialty chemicals and packaging portfolio, introducing PVC-free and high-barrier PVDC-coated PET films for retort and lidding applications. Its strong vertical integration allows in-house development of PVDC coatings, ensuring precise control over barrier properties and sealing performance. Cosmo is also targeting the growing pharmaceutical packaging segment, focusing on moisture-sensitive drug protection through advanced blister films.

UFlex Strengthens Integrated Packaging Solutions with Sustainable PVDC Coating Technologies

UFlex Limited is a leading multinational in the PVDC coated films market, offering end-to-end packaging solutions. The company has introduced mono-material PET films and water-based heat-seal coatings, integrating them with PVDC layers to create fully aqueous, high-barrier structures. UFlex’s vertical integration—spanning chemicals, printing machinery, and packaging—ensures efficient large-scale production. Its patented waterborne coating technologies enhance sustainability while maintaining performance, positioning it strongly in premium and eco-friendly packaging segments.

Kureha Secures Raw Material Leadership with Global PVDC Resin Production

Kureha Corporation is the backbone supplier in the PVDC coated films market, leading global production of PVDC resin under its Krehalon® brand. The company is investing heavily in capacity expansion to ensure stable supply for high-barrier packaging applications. Its films are widely used in meat and cheese packaging, offering exceptional oxygen barrier properties that preserve freshness and reduce food waste. Kureha is also expanding downstream capabilities to move closer to end-use markets, particularly in medical and high-performance packaging applications.

Innovia Films Advances Sustainable Packaging with Down-Gauged and Recyclable PVDC Films

Innovia Films, part of CCL Industries, is a major player in the PVDC coated films market, focusing on high-performance BOPP and cellulose films. Its Encore range includes PVDC-coated films designed for easy mechanical recycling, supporting sustainability goals. The company has successfully reduced film thickness by 15%, enabling material savings while maintaining long shelf-life performance. Innovia is particularly strong in tobacco overwrap, labeling, and pharmaceutical blister packaging, where optical clarity and barrier performance are critical.

China PVDC Coated Films Market: Export Leadership and Smart Manufacturing

China remains the global leader in the PVDC coated films market, maintaining the highest export volume with 1,132 shipments in the 2024–2025 period, far exceeding competitors. The country is transitioning toward smart manufacturing, leveraging AI-driven digital twin coating lines that optimize oxygen transmission rates (OTR) to extremely low levels (<5 cc/m²/day), while reducing resin consumption by around 12%.

Government support under the 14th Five-Year Plan is accelerating the shift from solvent-based coatings to aqueous PVDC dispersions, aligning with environmental goals. China’s dominance extends into advanced applications, particularly in EV battery packaging and high-precision electronics wraps, where moisture barrier performance is critical. Additionally, industrial hubs in Zhejiang and Shandong are expanding clean production capacity to meet rising demand from processed food packaging, while innovations in metal-like aesthetic PVDC films are opening premium confectionery applications.

India PVDC Coated Films Market: Pharmaceutical Packaging Powerhouse

India is emerging as a global hub for pharmaceutical PVDC blister packaging, supported by strong domestic demand and export growth. The country ranked second globally with 648 shipments (2024–2025), driven by expanding pharmaceutical production expected to reach $65 billion by 2025.

Technological advancements include ultra-high barrier PVDC coatings for hygroscopic drugs and the development of heat-reflective PVDC films for agricultural packaging in tropical climates. Government initiatives such as the PLI scheme are promoting local production of BOPP/PVDC laminates, reducing import dependency.

Companies like Cosmo Films and Uflex are investing in high-speed coating lines with wider web capacity, improving scalability. Regulatory measures under the Quality Control Order (QCO) are also enforcing strict OTR and WVTR standards, ensuring quality and performance in both domestic and export markets.

United States PVDC Coated Films Market: PFAS-Free Transition and Reshoring Growth

The U.S. PVDC coated films market is undergoing a structural shift due to PFAS-free regulatory mandates (2025–2026) and increasing reshoring of manufacturing. This has triggered significant R&D efforts to develop alternative PVDC formulations that maintain barrier properties without restricted chemicals.

Infrastructure investments are indirectly boosting demand for PVDC films in ready-meal packaging, while the healthcare sector is expanding usage in sterilized medical device packaging, with steady long-term growth projections. Innovations such as UV-curable PVDC coatings are enabling instant curing on heat-sensitive substrates, improving efficiency.

Sustainability trends are also influencing the market, with growing adoption of bio-attributed resins and aqueous coating technologies to reduce VOC emissions and meet ESG targets.

Germany PVDC Coated Films Market: Sustainable Barriers and Digital Traceability

Germany leads Europe in sustainable PVDC coated film innovation, focusing on recyclability and circular economy integration. Key developments include recyclable PVDC-coated polyethylene structures that can be processed within standard PE recycling streams without contamination.

Regulatory alignment with the EU Packaging and Packaging Waste Regulation (PPWR) is accelerating adoption of mono-material laminates, while digitalization initiatives such as blockchain-based material passports are enabling full traceability of film composition.

Technological advancements include low-temperature curing PVDC resins (<80°C), reducing energy consumption by up to 20%, and research into graphene-enhanced ultra-thin barrier layers. The market is also driven by demand for anti-fog, high-gloss films in premium food packaging applications across Europe.

Vietnam PVDC Coated Films Market: Emerging Manufacturing Hub

Vietnam is rapidly becoming a strategic “China+1” destination in the PVDC coated films market, supported by strong FDI inflows and expanding packaging demand. The country ranks third globally in exports with 212 shipments (2024–2025).

Infrastructure development in cities like Ho Chi Minh City and Hanoi is supporting integrated coating and lamination clusters. Government incentives such as tax benefits for clean production are encouraging adoption of energy-efficient infrared curing technologies.

Key applications include marine-grade food packaging for seafood exports, where high-barrier PVDC films are critical. Additionally, the adoption of automated color-matching technologies is enabling Vietnam to serve fast-moving consumer electronics packaging markets.

Japan PVDC Coated Films Market: High-Precision and Smart Packaging Innovation

Japan focuses on ultra-high barrier PVDC film technologies, particularly for pharmaceutical and specialty packaging. Innovations include oxygen-scavenging PVDC coatings, which not only block oxygen but actively absorb it, extending shelf life for sensitive products.

The country excels in multi-layer co-extrusion, enabling triple-barrier protection (oxygen, moisture, and UV) in ultra-thin films (~15 microns). Key applications include retortable pouches for elderly nutrition, which require high-temperature resistance without compromising barrier performance.

Sustainability efforts include the use of recycled PVDC resin in secondary layers, while investments in cleanroom coating facilities are supporting next-generation “smart pharma” packaging with NFC integration. Strict regulatory compliance ensures high safety standards in food and healthcare applications.

Brazil PVDC Coated Films Market: Agribusiness Demand and Domestic Protection

Brazil’s PVDC coated films market is driven by its strong agribusiness sector and increasing focus on domestic production. Regulatory measures such as import monitoring policies (2025) are supporting local film converters and strengthening supply chain resilience.

The country is a leader in high-barrier PVDC shrink films for meat exports, enabling extended shelf life for long-distance shipments. Investments in new coating lines are also supporting applications in electronics and industrial packaging.

Technological advancements include ZAM-compatible protective film coatings for mining and heavy-duty applications, while innovations in antimicrobial PVDC films with silver-ion technology are expanding usage in healthcare. Additionally, infrastructure growth is driving demand for protective packaging solutions in high-humidity construction environments.

PVDC Coated Films Market Report Scope

PVDC Coated Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.6 Billion

|

|

Market Size (2032)

|

$7.4 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Substrate Material (BOPP, BOPET, PVC, PE, BOPA, Specialty Substrates), By Coating Configuration (Single-Side Coated, Double-Side Coated), By Film Appearance (Transparent, Metallized, Pearlized, White), By End-Use Industry (Food and Beverage, Pharmaceuticals and Healthcare, Cosmetics and Personal Care, Industrial and Electronics, Chemicals and Agrochemicals), By Coating Thickness (Thin Films, Medium Films, Thick), By Sales Channel (Direct Sales, Specialty Film Distributors, E-commerce and Digital B2B Platforms)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kureha Corporation, Asahi Kasei Corporation, Jindal Poly Films Limited, Cosmo Films Limited, Mondi Group, Klöckner Pentaplast, CCL Industries Inc., SKC Co., Ltd., Unitika Ltd., Bilcare Limited, CPH Chemie + Papier Holding AG, UFlex Limited, Glenroy, Inc., Juhua Group Corporation, Vibac Group S.p.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PVDC Coated Films Market Segmentation

By Substrate Material

- BOPP

- BOPET

- PVC

- PE

- BOPA

- Specialty Substrates

By Coating Configuration

- Single-Side Coated

- Double-Side Coated

By Film Appearance

- Transparent

- Metallized

- Pearlized

- White

By End-Use Industry

- Food and Beverage

- Pharmaceuticals and Healthcare

- Cosmetics and Personal Care

- Industrial and Electronics

- Chemicals and Agrochemicals

By Coating Thickness

- Thin Films

- Medium Films

- Thick

By Sales Channel

- Direct Sales

- Specialty Film Distributors

- E-commerce and Digital B2B Platforms

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in PVDC Coated Films Industry

- Kureha Corporation

- Asahi Kasei Corporation

- Jindal Poly Films Limited

- Cosmo Films Limited

- Mondi Group

- Klöckner Pentaplast

- CCL Industries Inc.

- SKC Co., Ltd.

- Unitika Ltd.

- Bilcare Limited

- CPH Chemie & Papier Holding AG

- Uflex Limited

- Glenroy, Inc.

- Juhua Group Corporation

- Vibac Group S.p.A.

*- List not Exhaustive