Specialty Surfactants Market Valuation 2025–2034: $38.8 Billion to $62.8 Billion at 5.5% CAGR Anchored in Bio-Based Innovation and Portfolio Realignment

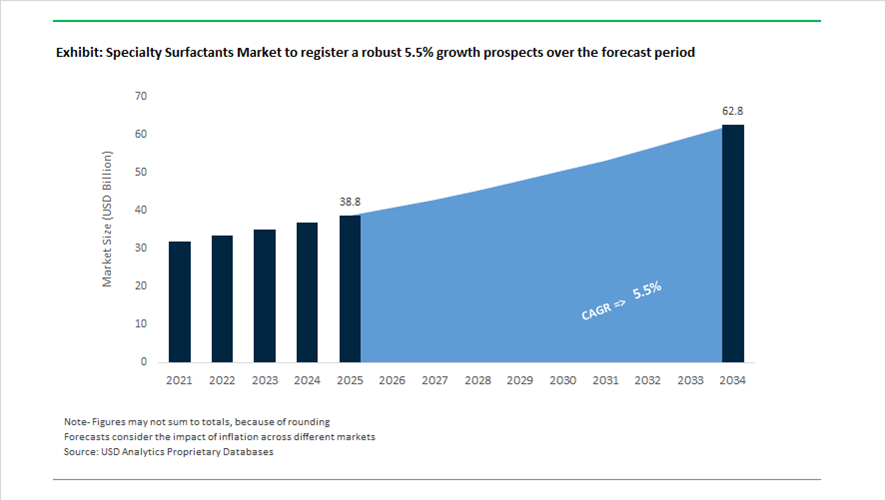

The global specialty surfactants market is valued at $38.8 billion in 2025 and is projected to reach $62.8 billion by 2034, expanding at a CAGR of 5.5%. Growth is driven by rising demand for high-performance emulsifiers, demulsifiers, quaternary ammonium compounds, ethoxylates, hydrotropes, and bio-based surfactants across personal care, home care, oil and gas, agrochemicals, pulp and paper, and industrial cleaning. The market is shifting toward renewable carbon surfactants, RSPO-certified feedstocks, low-foaming narrow-range ethoxylates, and solvent-free biodegradable chemistries as regulatory pressure intensifies around VOC emissions, PFAS restrictions, and wastewater discharge standards. Capacity expansions, strategic divestments, and targeted acquisitions are reshaping competitive positioning across North America, Europe, and Asia-Pacific.

Portfolio restructuring defined 2024. In early 2024, Kemira finalized the divestment of its oil and gas chemical business to Sterling Specialty Chemicals, including hydraulic fracturing surfactant lines, enabling greater focus on pulp and paper chemistry. Throughout 2024, Clariant completed the sale of its North American Land Oil and Quats businesses, reallocating capital toward its Care Chemicals and cosmetics portfolio. In November 2024, Indorama Ventures, through its Indovinya segment, acquired the KEMELIX and FLOWSOLVE brands, strengthening its specialty surfactant platform for energy extraction applications including demulsifiers and flow assurance agents. In the same month, Godrej Industries signed a business transfer agreement to acquire Savannah Surfactants’ Food Ester and Emulsifier business, expanding its footprint in food-grade emulsifiers and bio-based specialty surfactants. In late 2024, Stepan Company announced a $220 million global capacity expansion targeting natural alcohol derivatives, with full operational efficiency expected by early 2026.

Sustainable product innovation accelerated in 2025. In March 2025, Kemira announced a multi-million Euro expansion at its Wellgrow site in Thailand to scale specialty surfactants and functional agents serving Southeast Asia’s hygiene and packaging markets. In October 2025, Nouryon launched AG™ 6206, a 100% renewable carbon, solvent-free surfactant certified by RSPO for industrial and household cleaning formulations. During the same month, Croda introduced Natrineo™ CR8, a plant-derived specialty emulsifier recognized at the Pure Beauty Awards, reflecting the shift toward high-purity cosmetic stabilizers. In late 2025, Nouryon expanded its Ethylan™ X series with low-foaming narrow-range ethoxylates engineered to reduce water and energy consumption in hard-surface cleaning processes.

Operational optimization and decarbonization initiatives intensified entering 2026. In February 2026, Evonik Coating Additives announced a streamlined distribution network across the United States and Canada to enhance market responsiveness for specialty surfactants in coatings and inks. In the same month, BASF introduced AdBlue® GE manufactured using 100% renewable electricity, reinforcing the broader transition of specialty nitrogen intermediates and surfactant feedstocks toward low-carbon manufacturing. These acquisitions, divestitures, bio-based surfactant launches, ethoxylate innovations, and capacity investments are reshaping competitive dynamics in the specialty surfactants market through 2034.

Structural Trends and High-Value Opportunities in the Specialty Surfactants Market

CPG Strategic Pivot Toward Non-Ethoxylated and Bio-Based Surfactants

The Specialty Surfactants Market is undergoing a decisive structural shift as global Consumer Packaged Goods manufacturers accelerate the removal of Alcohol Ethoxylates and Alkylphenol Ethoxylates from product portfolios. This transition is not cosmetic but risk-driven, responding to rising consumer scrutiny of ingredient transparency and tightening regulatory oversight around 1,4-dioxane contamination. As a result, non-ethoxylated and bio-based surfactants are moving from niche alternatives to default formulation choices in premium home care and personal care categories.

Innovation recognition underscores the momentum behind this shift. In January 2024, Dow’s EcoSense 2470 surfactant received a BIG Innovation Award, highlighting industry validation of high-performance bio-based surfactants that match or exceed the cleaning efficacy of petrochemical incumbents. Alkyl Polyglucosides, derived from renewable sugars and fatty alcohols, are increasingly specified for mildness, biodegradability, and compatibility with sensitive-skin formulations.

Capacity investments confirm the long-term nature of this trend. BASF announced the doubling of its APG production capacity at its Jinshan site in China in 2024, directly addressing demand growth in Asia-Pacific and North America. This expansion positions bio-based surfactants as a scalable backbone for the fast-growing natural and clean-label product segments rather than as constrained specialty inputs.

Eco-Label Mandates Redefining Industrial and Institutional Cleaning Chemistry

In the Industrial and Institutional cleaning segment, sustainability requirements have evolved into enforceable procurement criteria. Programs such as the U.S. EPA Safer Choice initiative now function as gatekeepers for supplier qualification, particularly in healthcare, hospitality, and food service environments. As of July 2025, the EPA’s Safer Chemical Ingredients List expanded to 983 approved substances, providing a definitive framework for formulators seeking eco-certified status without compromising performance.

This regulatory clarity is reshaping product development roadmaps. Institutional buyers increasingly require documented low aquatic toxicity, biodegradability, and reduced occupational exposure risk, pushing specialty surfactants into the center of compliance strategies. Corporate sustainability integration is reinforcing this shift. In August 2024, Ecolab advanced its sustainability platform by deploying enzyme-based cleaning systems combined with specialty surfactants. These systems enable food and beverage operators to meet stringent hygiene standards while lowering chemical usage, water consumption, and environmental footprint, strengthening the value proposition of advanced surfactant technologies.

Low-Foam Surfactant Systems for High-Efficiency CIP Operations

The automation of manufacturing environments and the rise of Industry 4.0 have made low-foam performance a non-negotiable requirement in Clean-in-Place operations. High-speed pumps, sensors, and closed-loop cleaning systems demand surfactants that deliver strong wetting and soil removal under extreme pH conditions while generating virtually no foam. This has created a high-value opportunity for advanced non-ionic and modified alkoxylate systems engineered specifically for turbulent CIP cycles.

Innovation in this space is accelerating. In October 2025, Nouryon introduced eco-friendly low-foam cleaning technologies designed for industrial laundry and surface cleaning. These formulations provide rapid soil suspension without foam accumulation, enabling faster rinse cycles and improved equipment uptime. Performance data from late 2024 further indicates that low-foam surfactants are critical to reducing water and energy consumption in automated dishwashing and pharmaceutical cleaning systems, reinforcing their role as efficiency enablers rather than cost additives.

Multi-Functional Polymeric Surfactants for Waterborne and High-Solids Coatings

The global transition toward waterborne and high-solids coatings is creating demand for specialty surfactants that deliver multiple functions within a single additive package. Coating formulators increasingly seek polymeric surfactants that combine dispersion, wetting, and defoaming capabilities while remaining compliant with low-VOC and PFAS-free requirements.

This opportunity was highlighted at the European Coatings Show 2025, where Syensqo showcased Rhodoline HBR, a fluorosurfactant-free wetting agent offering enhanced stain resistance and hot-block performance in architectural coatings. Complementing this, Rhodoline 6100, containing 33% bio-based content, addresses pigment dispersion challenges in high-solids and alkyd systems while remaining APE-free. These developments illustrate how multi-functional specialty surfactants are becoming central to achieving durability, sustainability, and regulatory compliance simultaneously, positioning them as high-margin growth levers within the Specialty Surfactants Market.

Specialty Surfactants Market Share and Segmentation Insights

Non-Ionic Surfactants Lead the Specialty Surfactants Market Due to Versatile Formulation Performance

Non-ionic surfactants accounted for 34.8% of the specialty surfactants market in 2025, making them the most widely used surfactant type across multiple industrial and consumer formulations. These surfactants offer strong compatibility with other formulation ingredients, stability in hard water conditions, and adjustable hydrophilic-lipophilic balance, enabling tailored performance for diverse applications including personal care products, household detergents, and industrial cleaning formulations. Their versatility supports use in emulsification, wetting, and solubilization processes. A major 2025 market trend is the expansion of bio-based non-ionic surfactants, such as alkyl polyglycosides and bio-derived alcohol ethoxylates, which provide comparable performance to conventional surfactants while supporting renewable content claims and sustainability-focused product formulations.

Home Care and Detergents Drive Global Specialty Surfactant Consumption

Home care and detergents represent the largest application segment in the specialty surfactants market, accounting for 34.80% of global demand in 2025 due to the high consumption of surfactants in cleaning products. Applications include laundry detergents, dishwashing liquids, surface cleaners, and specialty household cleaning products, where surfactants provide critical functions such as soil removal, grease emulsification, foaming control, and surface wetting. The scale of global detergent production continues to drive demand for advanced surfactant technologies. A key 2025 industry trend is the shift toward concentrated detergent formulations and unit-dose cleaning systems, where specialty surfactants are optimized to deliver high cleaning performance, compatibility with water-soluble packaging films, and improved biodegradability.

Specialty Surfactants Market Competitive Landscape

The specialty surfactants market in 2026 is shaped by biotechnology-integrated formulations, PFAS-free chemistries, and precision agriculture adjuvants. Tier-1 players are prioritizing bio-based surfactants, digital formulation platforms, and regional manufacturing expansion to align with EU Zero-Pollution mandates and high-performance personal care and industrial applications.

Evonik Advances PFAS-Free Surfactants and Biotech-Driven Lipid Innovation for High-Performance Applications

Evonik is strengthening its specialty surfactants leadership through biotechnology-driven interface chemistry and sustainability-focused innovation. The company achieved €1.87 billion adjusted EBITDA in 2025 and projects €1.7–€2.0 billion for 2026, supported by Care Solutions growth. It launched Protectosil ECO-TRETE® ANTIGRAFFITI, a PFAS-free surface protection surfactant targeting coatings and construction applications. Its SPHINOX® Vively platform leverages advanced sphingolipid biotechnology to enhance skin barrier performance in premium personal care formulations. Through its "Tailor Made" program, Evonik is streamlining operations while investing in bio-based rhamnolipid production. The company’s integrated biosurfactant strategy positions it at the forefront of green specialty surfactants.

BASF Expands Non-Ionic Surfactant Capacity and Strengthens Bio-Based Portfolio Through Verbund Integration

BASF is leading the green transformation of specialty surfactants through large-scale integration and regional capacity expansion. The inauguration of its non-ionic surfactant facility in Seosan, Korea enhances supply for agrochemicals, home care, and personal care markets in Asia-Pacific. BASF implemented price increases of up to 30% in Europe to offset feedstock volatility and logistics pressures, reinforcing value-based pricing strategies. The company generated approximately €60 billion in sales in 2025 with €1.3 billion free cash flow, supporting reinvestment in high-margin surfactant platforms. Its "Winning Ways" program targets €2.3 billion in cost savings by 2026, optimizing Care Chemicals operations. BASF’s vertically integrated Verbund system ensures cost efficiency and supply chain resilience for specialty surfactants.

Croda Strengthens High-Purity Bio-Based Surfactants and Expands Biopharma Ingredient Capabilities

Croda is reinforcing its position as a sustainable specialty surfactants leader through renewable chemistry and high-purity ingredient innovation. The company reported £1.70 billion in 2025 sales, with Consumer Care and Life Sciences divisions delivering 8% growth. Its partnership with Amino GmbH and expansion of Super Refined™ facilities support pharmaceutical-grade surfactant production. Natrineo™ CR8, an award-winning natural emulsifier, highlights Croda’s leadership in clean-label cosmetic formulations. The company is reallocating R&D toward New & Protected Products, which grew 5% in 2025, targeting higher-margin specialty applications. Croda’s long-term framework aims for over 20% operating margins driven by innovation-led surfactant portfolios.

Stepan Optimizes Manufacturing Network and Expands Specialty Surfactants for Agriculture and Oilfield Applications

Stepan is restructuring its global operations to prioritize high-margin specialty surfactants and reduce reliance on commodity products. Through Project Catalyst, the company aims to deliver $100 million in pre-tax savings by mid-2026 by closing inefficient assets and optimizing production. Its Pasadena, Texas alkoxylation facility is scaling output of over 60 specialty surfactants, improving supply chain efficiency. Despite a temporary volume decline, the company achieved strong sales growth driven by agricultural adjuvants and oilfield chemicals. Stepan’s expertise in sulfonation and alkoxylation technologies supports advanced formulations for rigid foams and industrial cleaning. The company is focusing on performance-driven surfactants aligned with energy and agriculture demand.

Clariant Expands Bio-Based Surfactants and Agricultural Dispersants Through Asia-Centric Manufacturing Growth

Clariant is advancing specialty surfactants through bio-based innovation and regional manufacturing expansion. The CHF 80 million Daya Bay facility strengthens its presence in Asia for personal care and pharmaceutical surfactants. Dispersogen™ PSL 100 enhances stability in complex agricultural formulations, supporting biological crop protection trends. Plantasens™ Emulsifier HP 49 offers a 99% Renewable Carbon Index, aligning with clean beauty and sustainability standards. Integration of Lucas Meyer Cosmetics enables the development of neuro-cosmetic surfactants such as GlowCytocin™. Clariant’s dual focus on precision agriculture and skin science is driving high-margin specialty surfactant growth.

Syensqo Focuses on Bio-Circular Surfactants and Portfolio Optimization Following Strategic Spin-Off

Syensqo is positioning itself as a high-performance specialty surfactants and advanced materials leader following its spin-off from Solvay. The company reported €1.21 billion EBITDA in 2025 with strong free cash flow generation. It divested its Oil & Gas business in 2026 to focus on electrification and sustainable specialty chemicals. ISCC PLUS certification at its Moerdijk plant enables production of bio-circular surfactants using mass-balance feedstocks. Syensqo is leveraging its global R&D network to expand its ECHO portfolio of sustainable polymers and surfactants. The company targets 18% circular product sales by 2030 through innovation in green chemistry and advanced materials.

United States Specialty Surfactants Market Accelerated by Circular Carbon and Regulatory Signaling

The United States specialty surfactants industry is entering a structurally different growth phase, defined by circular feedstocks, regulatory labeling incentives, and application-specific innovation. In mid-2025, Dow, in collaboration with LanzaTech Global, scaled commercial production of the EcoSense 2470 surfactant, marking the first circular surfactant manufactured from recycled industrial carbon emissions for the North American home care market. This development reflects a broader shift toward carbon-utilization chemistry rather than incremental petrochemical optimization. Parallel to upstream innovation, Brenntag expanded its specialty distribution agreement with Kao Chemicals Europe in late 2025, reinforcing domestic supply resilience for high-performance surfactants used in premium beauty and personal care formulations.

Regulatory signaling has become a key demand catalyst. By early 2026, more than a quarter of newly registered U.S. surfactants had applied for the EPA Safer Choice label, with particular momentum in non-ionic grades offering accelerated biodegradability and reduced aquatic toxicity. State-level PFAS bans further reshaped the market, driving rapid commercialization of silicone-free and fluorine-free wetting agents for performance apparel and industrial textiles. On the innovation front, Stepan Company completed a $20 million R&D upgrade in 2025 focused on fermentation-derived surfactants for agriculture and oilfield applications, while Ashland introduced its Easy-Wet agricultural adjuvant line to improve pesticide efficacy while reducing runoff in large-scale farming systems.

European Union Specialty Surfactants Market Shaped by Digital Traceability and Biosurfactant Industrialization

Across Germany, France, and Belgium, the European Union specialty surfactants landscape is being structurally reshaped by regulation-driven transparency and accelerated biosurfactant scale-up. In December 2025, the EU Council approved a comprehensive update to the Detergents and Surfactants Regulation, introducing mandatory Digital Product Passports by 2027 and establishing the first formal safety framework for microbial cleaning products. This regulatory shift compels manufacturers to embed cradle-to-gate data traceability directly into specialty surfactant supply chains, increasing compliance costs while favoring technologically sophisticated producers.

Germany has emerged as the industrial anchor for biosurfactants. In early 2025, Evonik Industries operationalized its first industrial-scale rhamnolipid facility, producing Rewoferm RL 100 through proprietary fermentation. This asset positions biosurfactants as commercially viable inputs for ultra-premium household and institutional cleaning products. Complementing this, Sasol Chemicals and Holiferm entered a long-term supply agreement in 2025 for sophorolipids derived from wood-residue fermentation, targeting a 40% reduction in carbon intensity for European industrial detergents. Belgium’s role is increasingly defined by low-carbon manufacturing, with Nouryon completing Phase 2 of its renewable energy integration at Mons in August 2025, powering specialty chelants and surfactants using wind and solar electricity.

China Specialty Surfactants Market Driven by Green Certification and Localization

China’s specialty surfactants industry is rapidly realigning around sustainability mandates, localized formulation, and export compliance. In November 2025, Nouryon inaugurated a Specialty Chemicals Innovation Center in Shanghai, focused on localized application development for electronics-grade cleaning and high-performance textile surfactants. This aligns with MIIT’s late-2025 mandate requiring 85% of industrial cleaning agents in high-tech zones to be Green-Certified, triggering a large-scale shift toward bio-based and low-toxicity non-ionic surfactants.

Export dynamics are also reshaping production strategies. Following the implementation of carbon border mechanisms in Europe, Chinese producers began certifying specialty surfactants under the ISCC PLUS framework in late 2025 to preserve access to premium Western markets. At the same time, state-owned enterprises expanded investments in surfactant-polymer flooding systems for enhanced oil recovery, prioritizing high-temperature-stable sulfonates tailored for aging reservoirs. This dual focus on domestic green compliance and export-grade certification is redefining China’s competitive positioning in specialty surfactants.

India Specialty Surfactants Market Anchored in Certification and Import Substitution

India’s specialty surfactants sector is transitioning from volume-led production to certification-driven global participation. In 2025, Galaxy Surfactants achieved ISCC PLUS certification at its Taloja and Jhagadia facilities, enabling direct exports of sustainable specialty grades to regulated EU markets. This milestone reflects a broader national push toward internationally recognized sustainability frameworks.

Consolidation and policy support are accelerating scale. Godrej Industries strengthened its food-grade surfactant and emulsifier portfolio through the acquisition of Savannah Surfactants’ food additives business in early 2025, targeting regulated global food and beverage applications. Under the Production Linked Incentive scheme, India recorded peak specialty chemical investments of ₹1.76 lakh crore in 2025, with a substantial share directed toward domestic production of non-ionic specialty surfactants previously imported from East Asia. In parallel, the Department of Biotechnology launched targeted grants for waste-to-surfactant technologies, supporting microbial and fermentation-based routes using agricultural residues.

Comparative Snapshot: Specialty Surfactants Industry by Region

Specialty Surfactants Market County Level Snapshot

|

Region

|

Strategic Driver

|

Dominant Specialty Focus

|

Structural Direction

|

|

United States

|

Circular carbon and regulatory labeling

|

Non-ionic, PFAS-free, agricultural adjuvants

|

Carbon-utilization chemistry and Safer Choice alignment

|

|

European Union

|

Digital Product Passports and biosurfactants

|

Rhamnolipids, sophorolipids, chelants

|

Traceability-led compliance and fermentation scale-up

|

|

China

|

Green certification and localization

|

Bio-based non-ionics, oilfield sulfonates

|

MIIT-driven sustainability and export re-certification

|

|

India

|

Global certification and import substitution

|

Sustainable non-ionics, food-grade emulsifiers

|

ISCC PLUS adoption and PLI-backed capacity build-out

|

Specialty Surfactants Market Report Scope

Specialty Surfactants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$38.8 Billion

|

|

Market Size (2034)

|

$62.8 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Type (Anionic Surfactants, Non-Ionic Surfactants, Cationic Surfactants, Amphoteric Surfactants, Specialty and Bio-based Surfectants), By Origin (Synthetic Surfactants, Bio-based Surfactants, Biosurfactants), By Application (Personal Care and Cosmetics, Home Care and Detergents, Industrial and Institutional Cleaning, Agriculture, Oil and Gas, Textile and Leather, Food and Beverage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Stepan Company, Evonik Industries AG, Solvay SA, Dow Inc., Kao Corporation, Clariant AG, Nouryon, Croda International Plc, Galaxy Surfactants Ltd., Huntsman Corporation, Sasol Limited, Innospec Inc., Lion Specialty Chemicals Co., Ltd., Godrej Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Surfactants Market Segmentation

By Type

By Origin

- Synthetic Surfactants

- Bio-based Surfactants

- Biosurfactants

By Application

- Personal Care and Cosmetics

- Home Care and Detergents

- Industrial and Institutional Cleaning

- Agriculture

- Oil and Gas

- Textile and Leather

- Food and Beverage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Surfactants Industry

- BASF SE

- Stepan Company

- Evonik Industries AG

- Solvay SA

- Dow Inc.

- Kao Corporation

- Clariant AG

- Nouryon

- Croda International Plc

- Galaxy Surfactants Ltd.

- Huntsman Corporation

- Sasol Limited

- Innospec Inc.

- Lion Specialty Chemicals Co., Ltd.

- Godrej Industries Limited

*- List not Exhaustive