Market Overview: Anionic Surfactant Market to Reach $35.6 Billion by 2034 as Bio-Based Inputs, Regulatory Reformulation, and Regional Capacity Expansion Accelerate

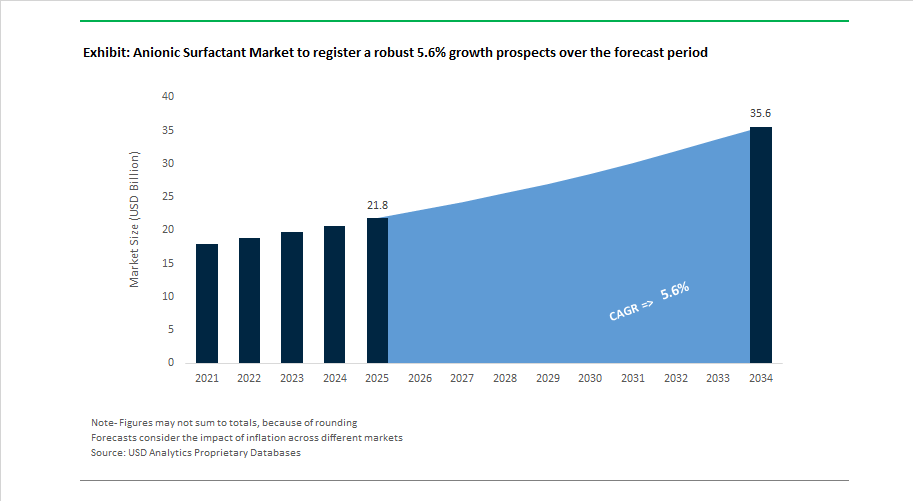

The global anionic surfactant market is projected to grow from $21.8 billion in 2025 to $35.6 billion by 2034, registering a 5.6% CAGR supported by strong demand in laundry detergents, dishwashing liquids, industrial cleaners, agrochemical adjuvants, and personal care formulations. Anionic surfactants such as linear alkylbenzene sulfonate, alcohol sulfates, methyl ester sulfonates, taurates, and glutamates remain essential for high detergency, foaming, and soil removal. Market evolution is increasingly defined by the transition toward bio-based anionics, sulfate-free chemistries, low 1,4-dioxane formulations, and circular carbon feedstocks. Regulatory reform in Europe and North America is pushing manufacturers to reduce ethoxylation by-products and improve biodegradability profiles, prompting accelerated adoption of renewable raw materials and greener processing technologies.

Portfolio diversification and supply stabilization began in April 2024 when Clariant completed integration of Lucas Meyer Cosmetics, enabling bundling of surfactant systems with high-end actives. Circular innovation progressed the same month as Kaffe Bueno introduced KLEANSTANT from up-cycled coffee feedstocks. Carbon-derived surfactant technology advanced in late 2024 as Dow and LanzaTech expanded the EcoSense portfolio using captured industrial emissions. Production stability improved in early 2025 when Stepan Company restored full capacity at its Millsdale plant, reinforcing North American supply of linear alkylbenzene sulfonate. Biosurfactant scale-up accelerated in March 2025 through capacity expansions by Dispersa and AGAE Technologies. EU regulatory changes throughout 2025 drove reformulation away from ethoxylated sulfates toward taurates and glutamates.

Regional capacity expansion strengthened in November 2025 when BASF inaugurated a bio-based surfactant facility in Thailand, followed by Nouryon’s AG 6206 Natural hydrotrope launch in October 2025. Profitability improved in October 2025 as Clariant reported margin gains tied to specialty anionic growth. Industry momentum carried into January 2026 with BASF confirming its Cincinnati start-up schedule, while February 2026 saw Nouryon introduce the first fully bio-based CMC anti-redeposition polymer and Stepan report surfactant revenue growth driven by agricultural and oilfield demand.

Trends and Opportunities Reshaping the Anionic Surfactant Market

Global Phase-Out of PFAS-Based Anionic Surfactants Drives Forced Substitution

The most disruptive structural shift in the anionic surfactant market is the regulatory-driven elimination of PFAS-based chemistries across industrial, municipal, and consumer applications. This transformation is not a long-term directional signal but a legally enforced compliance milestone that directly influences formulation pipelines, capital allocation, and raw material sourcing. Commission Regulation (EU) 2025/1988, enacted on October 2, 2025, imposes a <1 mg/L PFAS limit in firefighting foams by 2030, with accelerated 2026 deadlines for portable extinguishers and training foams. In real commercial terms, this mandates immediate substitution planning for fire safety OEMs, petrochemical operators, airport authorities, and municipal water bodies.

France has escalated the urgency further. Law No. 2025-188, effective January 1, 2026, bans PFAS-containing cosmetics and waterproofing agents, pushing textile and personal-care manufacturers to adopt PFAS-free surfactants like Sodium Lauryl Sulfoacetate and Alpha Olefin Sulfonates (AOS). Bio-based replacements are already demonstrating technical parity. In semiconductor wet-etching studies (2024–2025), hydrocarbon-based anionic blends and APGs achieved equivalent contact angles to PFAS chemistries, proving feasibility at scale. This means PFAS regulatory pressure is no longer only environmental—it is now a market access gatekeeper determining who can legally sell into Europe and North America.

Linear Alkylbenzene Sulfonate (LAS) Moves to a Renewable-Carbon Model

The market is also undergoing a supply-side pivot toward renewable feedstock LAS, transitioning away from petroleum-based paraffins to mass-balance and bio-derived carbon. Based on early-2025 disclosures, 61% of global LAB plants have begun incorporating renewable feedstocks due to the EU’s 2024 non-biodegradable surfactant ban and detergent brand commitments. This trend is not only regulatory but economic. 47% of sector-wide R&D spend in sulfonates is now being deployed on bio-paraffins and circular feedstocks, targeting a 15–20% lifecycle carbon reduction for mass-market detergents.

A landmark enabling milestone is BASF’s November 2025 expansion of its Thailand site, which creates Asia-centric capacity and reduces intercontinental freight emissions. The investment strategy is synchronized with BASF’s sites in Germany, China, and the US, forming a regionalized production grid designed to serve home-care giants demanding traceable, renewable-carbon anionic bases.

Market Opportunities for Value Chain Expansion

Ultra-Pure Anionic Sulfonates Unlock High-Node Semiconductor Fabrication

As semiconductor design migrates from 5 nm toward 3 nm and 2 nm nodes, chemical inputs must move from commodity to specialty-grade. Fabrication plants now require Electronics-Grade or MOS-Grade sulfonates, where metallic impurities (Fe, Cu, Na) must remain at ppb or ppt levels to avoid surface defects. These ultra-pure anionic surfactants are essential in Post-CMP wafer cleaning, where preventing particle re-adhesion directly affects chip yield.

Beyond cleaning, fluorinated anionic additives are entering EUV (Extreme Ultraviolet) lithography as Top Anti-Reflective Coatings (TARCs), modulating solubility and enabling higher-fidelity patterning. Capital is flowing into this niche: in April 2025, startup ChEmpower secured $18.7 million (Intel Capital-led) to scale abrasive-free planarization chemicals, signaling commercial transition from pilot-scale to industrial supply. The takeaway is clear—the semiconductor material segment is becoming a pricing-power zone where anionic chemistry is monetized at premium margins.

High-Solid-Content Battery Dispersants Become an Industrial-Scale Demand Driver

Electric-vehicle manufacturing is establishing a second major strategic avenue. The global race for higher-density EV batteries is increasing the relevance of anionic polymeric dispersants that stabilize water-based electrode slurries, replacing PVDF/NMP solvent systems. Data from 2025 trials demonstrates that naphthalene sulfonates and lignosulfonates can deliver over 25% improvement in capacity retention after 400 cycles for LFP cells by maintaining slurry homogeneity during thick-film coating.

This adoption is evolving into a structural market. With EV sales projected to hit 45 million units annually by 2030, dispersant demand is shifting from R&D to global industrial procurement. Domestic pilots in Indonesia and Brazil (2025) reveal early localization strategies, with electrode-slurry dispersant manufacturing being co-built alongside cathode plants to secure supply chains and reduce reliance on imported chemistry.

Anionic Surfactant Market Share and Segmentation Insights

Market Share by Product Type: LAS Anchors Volume While Amino Acid Anionics Deliver High-Growth Premiumization

Linear Alkylbenzene Sulfonates (LAS) command approximately 41% of the global anionic surfactant market in 2025, remaining the backbone of laundry detergents and dishwashing liquids due to superior detergency, soil suspension, and unmatched cost-performance, with incremental growth concentrated in Asia-Pacific, Africa, and Latin America. Alkyl Ether Sulfates (AES), led by SLES, rank second and expand at +6% YoY, driven by shampoos, body washes, and hand dishwashing liquids where foam quality and viscosity control matter. Alkyl Sulfates (SLS/AS) are declining in premium personal care but persist in toothpaste and price-sensitive cleaners. Lignosulfonates provide stable, bio-based volumes for concrete admixtures and agro dispersants. Alpha Olefin Sulfonates grow steadily in premium detergents with hard-water tolerance. Phosphate esters serve high-margin specialty niches. Amino acid based anionic surfactants are the fastest-growing, propelled by sulfate-free, ultra-mild personal care and clean beauty positioning.

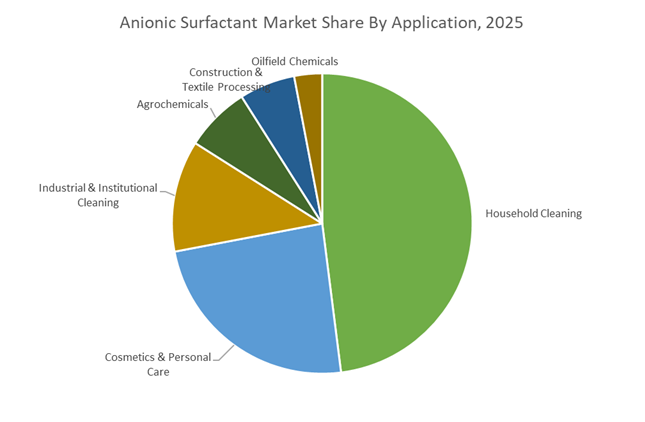

Market Share by Application: Household Cleaning Dominates as Personal Care Drives Margin Expansion

Household cleaning represents roughly 48% of anionic surfactant consumption in 2025, spanning laundry formats (powder, liquid, pods), hand dishwashing, automatic dishwashers, and hard-surface cleaners, with LAS and AES dominating volume. While formulation concentration reduces product weight, surfactant intensity per dose is rising, keeping demand resilient and population-linked. Cosmetics & personal care rank second and deliver the highest margins, covering shampoos, body washes, facial cleansers, and toothpaste, where AES remains central, SLS is being phased down, and amino acid anionics are gaining share under sulfate-free reformulation, supporting 5–7% growth in developed markets and higher in Asia. Industrial & institutional cleaning is stable and specification-driven, led by LAS and phosphate esters. Agrochemicals rely on lignosulfonates and phosphate esters for emulsification and dispersion. Construction & textiles remain mature, while oilfield chemicals form the smallest but high-value segment, with AOS preferred for high-salinity reservoirs amid cyclical recovery.

Anionic Surfactant Market Competitive Landscape

The global anionic surfactant market is undergoing a structural transformation driven by cold-water washing technologies, sulfate-free personal care reformulations, bio-based feedstocks, and circular chemistry. Leading producers are competing on mass-balance certification, fermentation-derived actives, regionalized manufacturing, and formulation agility to serve fast-growing FMCG, agrochemical, semiconductor, and industrial cleaning sectors. Capacity expansions across Europe, Asia, and the Middle East, combined with microbiome-friendly hygiene innovation and ESG-aligned production, are redefining supplier selection criteria. Market leadership is increasingly anchored in vertical integration into ethylene oxide and fatty alcohols, sustainable Alpha Olefin Sulfonates (AOS), and next-generation amino-acid-based anionic surfactants that balance performance, mildness, and carbon footprint reduction.

Verbund-scale integration enables BASF SE to lead low-carbon anionic surfactants

BASF remains the world’s most integrated anionic surfactant producer, leveraging its Verbund system to stabilize pricing while decoupling production from fossil fuels through mass-balance certification. In late 2025, BASF implemented a “Regional Sovereignty” strategy by expanding hubs in Antwerp and Bangpakong, reducing tariff exposure and logistics-related CO2 emissions. The 2025 scale-up of AuraPure™ introduced cold-water washing down to 15°C, significantly lowering household energy consumption. BASF is also pivoting toward “Microbiome-Friendly Hygiene,” aligning Care Chemicals R&D with medical-grade skincare requirements. Deep backward integration into ethylene oxide and fatty alcohols provides long-term supply security for global detergent and personal care manufacturers.

Formulation agility defines Stepan Company’s North American leadership

Stepan anchors the North American anionic surfactant market through high-performance AOS, SLES, and mild cleansing systems for agriculture, oilfield, and FMCG applications. Its expanded Pasadena, Texas alkoxylation facility came online in 2025, boosting Alpha Olefin Sulfonate capacity for domestic laundry and industrial cleaning. Mid-2025 ISCC PLUS certification across European sites now enables Stepan to supply fully traceable, sustainable anionic surfactants aligned with EU Green Deal standards. The STEOL® and STEPAN-MILD® portfolios remain benchmarks for low-irritation mass-market formulations. Stepan’s “Formulation-as-a-Service” model supports over 2,500 customers with pre-validated blends, accelerating regulatory-compliant product launches.

Bio-waste innovation positions Kao Corporation as a cold-water surfactant pioneer

Kao leads in Advanced Interface Science, commercializing Bio-IOS technology during 2025–2026, an anionic surfactant derived from discarded palm fruit solids with superior solubility in cold and hard water versus traditional LAS. Under its K27 mid-term plan, Kao is integrating consumer and chemical operations across Asia, targeting 150% growth in high-value surfactant sales in Thailand and Vietnam by 2027. Internal brands serve as real-world validation platforms for new chemistries before merchant release. A 2025 pivot to light-asset operations in China refocused investment toward R&D for drone-based agricultural adjuvants and specialty anionic systems.

Fermentation-based chemistry powers Evonik Industries AG’s biosurfactant transition

Evonik has repositioned itself as a biosurfactant powerhouse, commissioning the world’s first industrial-scale rhamnolipid facility in Slovakia during 2024–2025. This delivers a 100% bio-based, biodegradable anionic surfactant with strong foaming and ultra-low toxicity. Evonik specializes in semiconductor wafer cleaning and wastewater disinfection, where purity and performance are mission-critical. The company is divesting traditional Performance Materials to concentrate on Next-Generation Solutions centered on circularity and climate protection. With deep expertise in specialty amines and lipid chemistry, Evonik engineers designer anionic surfactants capable of operating under extreme pH and temperature conditions, including deep-sea drilling environments.

Emerging-market scale strengthens Galaxy Surfactants Ltd.’s global footprint

Galaxy Surfactants dominates mild anionic surfactant supply across the Global South, serving leading CPG brands with sulfate-free alternatives. Production expansions in Jhagadia (India) and Egypt during 2025 addressed surging hygiene demand in Africa and the Middle East. The Galsoft® glutamate and sarcosinate portfolio is rapidly replacing SLES in premium shampoos, while Galseer® Tresscon enables high-performance solid beauty formats, cutting plastic packaging by up to 90%. Galaxy achieved Water Positive status in 2025, reinforcing its ESG leadership. Strong oleochemical backward integration ensures stable Cocamidopropyl and amino-acid surfactant supply despite palm oil volatility.

Affordable bio-based disruption defines Sino Lion’s anionic strategy

Sino Lion is reshaping the anionic surfactant landscape through amino-acid-based innovation and commodity-scale green manufacturing. In 2025, it launched a Global Green Surfactant Engineering Research Center with Nanjing University, accelerating synthesis from fermented agricultural waste. Its Eversoft™ Sodium Cocoyl Glycinate and Glutamate powders are widely adopted by indie beauty brands for waterless concentrates. A patented zero-waste glycinate process introduced in 2026 eliminated salt by-products, enabling clear formulations previously unattainable with amino surfactants. By industrializing bio-based production, Sino Lion has made 100% renewable anionic surfactants cost-competitive with petroleum-derived alternatives.

United States Anionic Surfactant Market: Sulfonation Scale-Up and Low-Contaminant Manufacturing Leadership

The United States remains a core innovation and capacity hub for anionic surfactants, particularly alpha olefin sulfonates and ether sulfates. In June 2025, Stepan Company announced a 25% increase in AOS production capacity across its Millsdale, Anaheim, and Winder sites, directly responding to surging demand for sulfate-free personal care formulations. This expansion reinforces the country’s role in supplying high-purity anionics for shampoos, facial cleansers, and sensitive-skin products.

Upstream and specialty intermediate investments are also accelerating. Planet Chemical Company expanded its Middletown, Ohio operations in early 2025, targeting a doubling of AOS output by 2027 for the household and institutional cleaning segment. Sustainability is shaping operational strategy, with BASF implementing 100% renewable electricity credits at its Geismar site to reduce the carbon footprint of its anionic portfolio. Meanwhile, regulatory pressure on 1,4-dioxane contamination has driven more than $40 million in U.S. investments in vacuum stripping technologies, ensuring compliance with sub-1 ppm thresholds. Companies such as Pilot Chemical are also hedging petrochemical volatility by integrating bio-based fatty alcohols into anionic feedstock streams.

Slovakia Anionic Surfactant Market: Fermentation-Based Anionics Set a New Global Benchmark

Slovakia has emerged as a strategic global hub for next-generation anionic biosurfactants. In May 2024, Evonik inaugurated the world’s first industrial-scale rhamnolipid biosurfactant plant in Slovenská Ľupča. This triple-digit million-euro facility utilizes fermentation and renewable corn feedstocks to produce high-performance, non-toxic anionic alternatives compatible with mild and sustainable formulations.

The site functions as the global launch platform for Evonik’s REWOFERM® series, protected by proprietary biotechnology that delivers strong detergency even in cold-water laundry applications. By late 2025, Evonik expanded on-site R&D with a dedicated biotech scale-up laboratory to develop specialized anionic biosurfactant variants for pharmaceutical processing and oilfield chemistry. Slovakia’s role is therefore shifting from contract manufacturing to high-value innovation within the anionic surfactant ecosystem.

India Anionic Surfactant Market: BioE3 Policy Drives Export-Ready Green Anionics

India’s anionic surfactant industry is advancing rapidly under policy-driven green chemistry initiatives. The BioE3 Policy, announced in late 2024, explicitly prioritizes bio-based chemicals and enzyme-enabled synthesis, providing tax incentives and infrastructure support for domestic producers. Within this framework, Galaxy Surfactants launched Galseer® DermaGreen, a biodegradable anionic blend designed for ultra-mild beauty care applications.

Export-oriented capacity expansion has become a defining theme. In 2025, Galaxy expanded its Jhagadia facility in Gujarat to increase production of GalEcosafe, a high-purity anionic surfactant engineered for international markets across Africa, the Middle East, and Turkey. Sustainability metrics are improving in parallel. By March 2025, leading Indian producers achieved 20% process water recycling and reported 77% waste circularity rates, reflecting deep integration of zero liquid discharge systems and circular economy practices within anionic manufacturing.

China Anionic Surfactant Market: Verbund Integration and Premium Home Care Demand

China’s anionic surfactant industry is being reshaped by large-scale integrated investments and premiumization of household cleaning. BASF is preparing to commission its Zhanjiang Verbund site in late 2025, part of a €10 billion investment that integrates surfactant precursors and ensures localized supply for South China. This Verbund approach significantly reduces logistics emissions while enhancing supply security for alkyl ether sulfates and sulfonates.

Circular economy initiatives are gaining momentum. In early 2025, BASF commenced commercial production of loopamid at its Caojing site, signaling broader adoption of recycled feedstocks across the surfactant value chain. Policy reforms also favor exporters, as streamlined registration for anionic-based pesticide adjuvants reduced compliance burdens for overseas markets. Renewable energy integration further strengthens China’s decarbonization agenda, with offshore wind farms supplying 100% renewable electricity to key BASF sites. On the demand side, rapid urbanization and premium detergent formats drove a notable increase in the use of AES in concentrated laundry pods during 2025.

Germany Anionic Surfactant Market: Carbon-Derived Anionics and Supply Chain Accountability

Germany remains at the forefront of sustainable anionic surfactant innovation. In 2025, the Flue2Chem project, supported by BASF and Unilever, demonstrated the commercial feasibility of synthesizing anionic surfactants from captured industrial CO2, achieving performance parity with fossil-derived counterparts. This breakthrough positions Germany as a leader in carbon-capture-based surfactant chemistry.

Recognition for sustainability leadership followed. Clariant received the 2025 Schneider Electric Outstanding Supplier Award for halogen-free, low-toxicity anionic additives aligned with GreenScreen-certified standards. Product innovation continues in industrial applications, with Clariant’s Hostagliss LS enabling water-based metalworking systems to replace mineral oil emulsifiers. Simultaneously, enforcement of the Supply Chain Due Diligence Act has pushed German producers toward full adoption of RSPO-certified palm oil, elevating traceability and ethical sourcing as core competitive differentiators.

Strategic Positioning by Country in the Anionic Surfactant Industry

Anionic Surfactant Market County Level Snapshot

|

Country

|

Strategic Emphasis

|

Industry Implication

|

|

United States

|

Sulfonation scale-up and dioxane control

|

Leadership in high-purity, sulfate-free anionics

|

|

Slovakia

|

Fermentation-derived biosurfactants

|

Global innovation hub for non-toxic anionic alternatives

|

|

India

|

BioE3-driven green chemistry and exports

|

Rising supplier of sustainable, export-grade anionics

|

|

China

|

Verbund integration and premium detergents

|

Scale efficiency with growing circularity

|

|

Germany

|

Carbon-capture surfactants and due diligence

|

Benchmark for low-carbon, traceable anionic systems

|

Anionic Surfactant Market Report Scope

Anionic Surfactant Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.8 Billion

|

|

Market Size (2034)

|

$35.6 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Type (Linear Alkylbenzene Sulfonates, Alpha Olefin Sulfonates, Alkyl Ether Sulfates, Alkyl Sulfates, Lignosulfonates, Phosphate Esters, Amino Acid Based Anionic Surfactants), By Form (Liquid and Slurry, Powder and Granules, Paste and Gel), By Application (Household Cleaning, Cosmetics and Personal Care, Agrochemicals, Oilfield Chemicals, Construction and Textile Processing, Industrial and Institutional Cleaning)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Stepan Company, Evonik Industries AG, Galaxy Surfactants Limited, Clariant AG, Nouryon, Solvay SA, Huntsman Corporation, Sasol Limited, Kao Corporation, Pilot Chemical Company, Innospec Inc, Zschimmer and Schwarz, Sino Lion, Tinci Materials Technology

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anionic Surfactant Market Segmentation

By Product Type

- Linear Alkylbenzene Sulfonates

- Alpha Olefin Sulfonates

- Alkyl Ether Sulfates

- Alkyl Sulfates

- Lignosulfonates

- Phosphate Esters

- Amino Acid Based Anionic Surfactants

By Form

- Liquid and Slurry

- Powder and Granules

- Paste and Gel

By Application

- Household Cleaning

- Cosmetics and Personal Care

- Agrochemicals

- Oilfield Chemicals

- Construction and Textile Processing

- Industrial and Institutional Cleaning

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Anionic Surfactant Industry

- BASF SE

- Stepan Company

- Evonik Industries AG

- Galaxy Surfactants Limited

- Clariant AG

- Nouryon

- Solvay SA

- Huntsman Corporation

- Sasol Limited

- Kao Corporation

- Pilot Chemical Company

- Innospec Inc

- Zschimmer and Schwarz

- Sino Lion

- Tinci Materials Technology

*- List not Exhaustive