Naphthalene Sulfonate Market 2025–2034: Infrastructure-Led Demand, Formaldehyde-Free Innovation, and Regional Supply Realignment

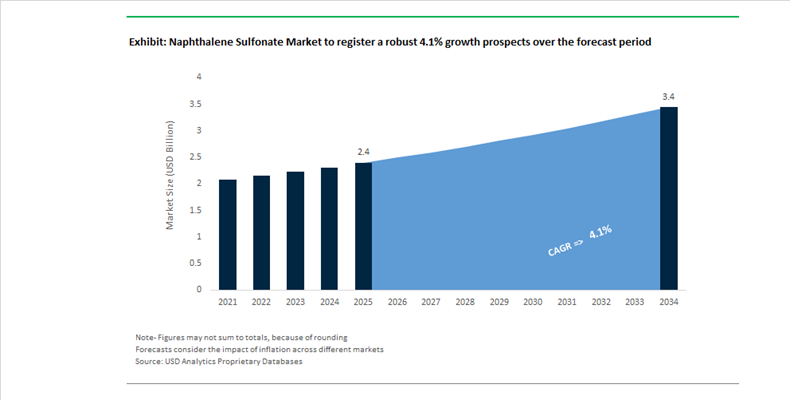

The Naphthalene Sulfonate Market is projected to expand from $2.4 billion in 2025 to $3.4 billion by 2034, reflecting a CAGR of 4.1%. Market growth is structurally linked to infrastructure expansion, urbanization-driven concrete consumption, and the ongoing need for cost-effective superplasticizers in emerging economies. Sulfonated naphthalene formaldehyde (SNF) dispersants remain widely used in ready-mix concrete, precast elements, tunnel linings, and large-scale transport projects due to their proven ability to reduce water-cement ratios while improving compressive strength and workability. Although polycarboxylate ether (PCE) technologies are gaining share in high-performance segments, naphthalene sulfonates continue to dominate price-sensitive bulk construction markets across Asia, Africa, and parts of Latin America.

Industry consolidation is reshaping the competitive structure. In February 2025, Saint-Gobain finalized its $1.025 billion acquisition of Fosroc, integrating Fosroc’s extensive naphthalene-based admixture portfolio into its global Construction Chemicals division. Combined with the earlier acquisition of GCP Applied Technologies, this move strengthens Saint-Gobain’s exposure to high-growth markets such as India, the Middle East, and Southeast Asia. The unified strategy, announced in December 2025, centers on “better concrete” objectives—optimizing water reduction, durability, and lifecycle performance in megaprojects including Saudi Arabia’s NEOM development. The integration of SNF and PCE technologies under one umbrella allows contractors to balance performance and cost efficiency across diverse climatic and structural requirements.

Regulatory pressure is accelerating formulation shifts. By early 2026, leading European and North American producers expanded formaldehyde-free naphthalene sulfonate offerings in response to tightening MSDS disclosures and eco-label requirements for public works. These next-generation variants reduce free formaldehyde residuals while maintaining dispersing efficiency, positioning SNF products as compliant alternatives in municipal and transportation tenders. Simultaneously, AI-driven process control systems—deployed in 2024 by major specialty chemical suppliers—have enabled real-time monitoring of sulfonation and condensation reactions, improving molecular weight consistency and lowering drying-stage energy intensity. This technological modernization is critical for producers facing feedstock volatility and carbon reporting obligations.

Regional supply dynamics are evolving. In January 2025, India’s ₹16,300 crore National Critical Minerals Mission indirectly stimulated domestic production of aromatic derivatives to reduce reliance on imported superplasticizers. MUHU (China) Construction Materials expanded its MENA headquarters to capture rising demand in Gulf and North African infrastructure corridors. Meanwhile, Adani Enterprises’ advancing Mundra petrochemical cluster is expected to secure upstream aromatic feedstock availability for India’s textile dye and concrete additive industries by 2026.

Trade disruptions also influenced pricing. New U.S. tariffs on petrochemical intermediates in early 2025 increased raw material costs for naphthalene sulfonate manufacturers, prompting diversification toward domestic aromatic sourcing and greater operational efficiency. Despite competitive pressure from advanced PCE admixtures, naphthalene sulfonates retain structural demand in mass concrete, road construction, and developing economies where cost-per-cubic-meter optimization remains paramount.

Naphthalene Sulfonate Market Trends and Opportunities

Trend: Strategic Backward Integration to Secure Naphthalene Sulfonate Supply Chains

The naphthalene sulfonate market is undergoing structural realignment as construction chemical manufacturers respond to sustained volatility in upstream feedstocks. Since 2022, prices of naphthalene and oleum have fluctuated by nearly 22 to 25% annually, exposing superplasticizer producers to margin instability and inconsistent quality from merchant suppliers. In response, leading players are pursuing backward integration strategies to establish captive production of sulphonated intermediates, ensuring both cost control and formulation consistency for high-performance concrete admixtures.

This trend is particularly pronounced in Asia-Pacific, where infrastructure-led demand remains robust. In late 2024, Rain Industries completed a 60,000 metric ton per year expansion at its Vizag facility, strengthening its integrated naphthalene derivatives value chain. Similarly, Himadri Speciality Chemical Ltd. commissioned a new 40,000 metric ton plant dedicated to high-purity naphthalene sulfonates to directly serve construction chemical formulators. These investments are not opportunistic capacity adds but strategic insulation moves against supply disruptions and quality drift.

India alone consumed more than 35,000 metric tons of naphthalene sulfonates in 2023, driven by expressway corridors, metro rail projects, and urban housing programs. Localized production allows manufacturers to bypass logistical bottlenecks and import duties while reducing the 15 to 20% premium typically paid for refined merchant-grade naphthalene. From a performance standpoint, integrated producers can tightly control sulfonation parameters, enabling Sulphonated Naphthalene Formaldehyde formulations that consistently reduce water-to-cement ratios by 20 to 30%. This combination of cost stability, performance reliability, and supply assurance is making backward integration a competitive necessity rather than a strategic option.

Trend: Regulatory-Driven Adoption in Agrochemical Dispersant Systems

Beyond construction, regulatory pressure is reshaping the role of naphthalene sulfonates in agrochemical formulations. As authorities in Europe and North America tighten restrictions on Alkylphenol Ethoxylates due to endocrine disruption risks, formulators are transitioning toward naphthalene sulfonate condensates as an environmentally acceptable dispersant benchmark. This shift is structural, as agrochemical producers must now balance regulatory compliance with high-load active ingredient delivery.

Alkyl naphthalene sulfonates are increasingly favored for their strong wetting and dispersing performance. Their ability to reduce surface tension from roughly 72 mN/m to around 30 mN/m significantly improves spray coverage and rainfastness, a critical requirement in a global agrochemical market exceeding 200 billion dollars in value. In Water-Dispersible Granule formulations, naphthalene sulfonates play a stabilizing role by preventing active ingredient aggregation, even under high-salinity and variable pH conditions. Recent patent activity underscores their effectiveness in maintaining dispersion stability in harsh field environments.

Toxicological expectations are also tightening. During 2024, more than 20 global manufacturers launched new naphthalene-based dispersants with ultra-low formaldehyde content below 0.1% to align with REACH and North American safety standards. This reformulation wave is reinforcing naphthalene sulfonates as a compliant, performance-proven solution for open-field agricultural use, positioning them as a long-term substitute rather than a transitional chemistry.

Opportunity: Low-Carbon Cement Grinding and Green Concrete Formulations

Decarbonization of cement and concrete is creating a high-growth opportunity for naphthalene sulfonates as multifunctional grinding aids and set-modifying dispersants. With the cement industry targeting a 10 to 15% reduction in CO2 emissions per tonne through clinker substitution, blended cements with fly ash and slag are becoming mainstream. However, these formulations often suffer from reduced early strength and poor workability.

Naphthalene sulfonates address this challenge by acting as powerful dispersants that expose more cement particle surface area to water. In low-clinker systems, this translates into Day 1 compressive strength improvements of 60 to 90% compared to untreated mixtures. At the production stage, optimized sulfonates reduce agglomeration during fine milling, lowering grinding energy consumption and aligning with the Global Cement and Concrete Association roadmap toward carbon neutrality.

While polycarboxylate-based admixtures offer superior water reduction, naphthalene sulfonates remain the most cost-effective solution for standard high-strength and precast concrete. This cost-performance balance is particularly attractive in emerging markets, where construction output is projected to grow sharply through 2030 and pricing sensitivity remains high.

Opportunity: High-Temperature Stability in Geothermal and Deep-Well Drilling

The expansion of Enhanced Geothermal Systems is opening a specialized but lucrative application window for naphthalene sulfonates in drilling fluids. Unlike many synthetic polymers that degrade above 160 degrees Celsius, naphthalene sulfonate-formaldehyde condensates retain rheological stability up to 300 degrees Celsius, making them suitable for ultra-high-temperature reservoirs.

Research published in 2025 demonstrates that optimized formulations maintain fluid-loss control after aging at 240 degrees Celsius, with successful field deployment in geothermal reservoirs in New Zealand and the United States. In fractured formations, these sulfonates are also used in foam drilling systems to stabilize foam membranes and prevent lost circulation in wells exceeding 3,000 meters in depth.

As geothermal energy transitions from pilot projects to commercial baseload power, demand for additives that combine thermal resilience, environmental acceptability, and cost efficiency is expected to rise. Naphthalene sulfonates, with decades of performance validation under extreme conditions, are well positioned to capture this niche growth trajectory.

Naphthalene Sulfonate Market Share and Segmentation Insights

Naphthalene Sulfonate Formaldehyde Leads as High-Performance Superplasticizer in Concrete Admixtures

Naphthalene sulfonate formaldehyde accounted for 58.60% of the Naphthalene Sulfonate Market by product type in 2025, driven by its widespread use as a high-performance superplasticizer in concrete admixtures. NSF condensates enable significant water reduction of 15 to 30% while maintaining concrete workability, making them essential for producing high-strength and durable concrete formulations. Their cost effectiveness and proven performance across ready-mix and precast concrete applications support strong global demand. These materials are widely used in infrastructure and large-scale construction projects requiring optimized concrete properties. In 2025, growing demand for high-range water reducers is reinforcing NSF consumption, particularly in projects requiring low water-cement ratios and enhanced structural performance.

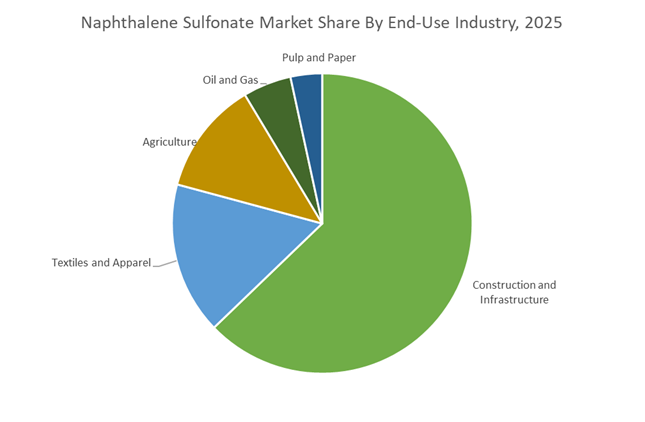

Construction and Infrastructure Sector Dominates Demand Driven by Global Urbanization and Concrete Consumption

Construction and infrastructure accounted for 62.80% of the Naphthalene Sulfonate Market by end-use industry in 2025, reflecting the dominant use of these chemicals in concrete production for buildings, roads, bridges, and urban infrastructure. The scale of global construction activity and rapid urbanization continues to drive high consumption of naphthalene sulfonate-based admixtures. These compounds play a critical role in improving concrete strength, durability, and workability across large projects. Infrastructure investments in emerging and developed economies further support consistent market demand. In 2025, sustainable construction practices are increasing adoption of advanced admixtures, with NSF-based superplasticizers enabling reduced cement usage and lower carbon footprint while maintaining required performance standards in modern construction.

Naphthalene Sulfonate Market Competitive Landscape

The naphthalene sulfonate market in 2026 is driven by high-performance SNF superplasticizers, precision sulfonation, and localized production strategies. Competitive differentiation centers on slump retention, low-bleeding formulations, and high-purity dispersants enabling 20–30% cement reduction in sustainable concrete and advanced industrial applications.

BASF expands localized SNF production and low-PCF dispersants for sustainable infrastructure growth

BASF SE is strengthening its leadership in naphthalene sulfonate-based superplasticizers through localized manufacturing and low-carbon innovation. The 2026 expansion at its Mangalore facility enhances supply of high-performance dispersions tailored for South Asia’s infrastructure boom. Its Basonal® PLUS portfolio delivers reduced product carbon footprint (PCF) solutions, aligning with green construction mandates. BASF’s Melnap® superplasticizers are optimized for high early strength and rapid curing in precast concrete applications. Leveraging Verbund integration, the company ensures cost-efficient production and consistent molecular weight distribution. Its focus on sustainable construction chemicals and regional supply chains reinforces its dominance in high-performance SNF formulations.

Kao drives high-purity dispersant innovation with MIGHTY® superplasticizers and bio-based R&D roadmap

Kao Corporation is a global leader in high-purity naphthalene sulfonate dispersants, targeting both construction and agrochemical sectors. Its MIGHTY® series enables superior workability and flowability in high-strength concrete, minimizing segregation in complex structures. Under its K27 strategy, Kao is advancing high-value SNF formulations with enhanced stability and performance consistency. Participation in NEDO-backed biomanufacturing projects signals a shift toward renewable surfactant alternatives. The company’s agile R&D framework accelerates customized dispersant development for pesticides and dyes. Strong ROIC performance supports reinvestment into next-generation high-purity sulfonation technologies.

Himadri scales integrated naphthalene chemistry to emerge as a global non-Chinese supply chain alternative

Himadri Speciality Chemical Ltd. is positioning itself as a strategic alternative supplier through vertically integrated naphthalene-based chemical production. Its 70,000 MTPA specialty carbon black expansion strengthens upstream feedstock security for sulfonate manufacturing. The company’s export of coal tar pitch enhances its global logistics network and ensures consistent raw material availability. A ₹220 crore investment program supports expansion into lithium-ion battery materials, leveraging synergies with its carbon chemistry expertise. Himadri’s EcoVadis Platinum rating places it among the top 1% of global chemical producers for ESG performance. Its cost-efficient production and global export capabilities make it a key player in diversified SNF supply chains.

MUHU advances high-concentration SNF superplasticizers with localized ASEAN manufacturing and chloride-free formulations

MUHU Construction Materials is a leading innovator in high-concentration sodium naphthalene sulfonate formaldehyde (SNF) superplasticizers. Its UNF-5 series delivers 15–20% cement reduction and significant slump improvement at low dosage, optimizing high-strength concrete performance. The company’s expansion into the Philippines through a joint production facility enables localized supply for Southeast Asia’s infrastructure growth. MUHU’s chloride-free and low-alkali formulations address corrosion challenges in coastal and high-rise construction. Offering both powder (≥92% solids) and liquid forms, MUHU enhances on-site flexibility and logistics efficiency. Its focus on process integration and regional manufacturing strengthens its competitive edge.

Enaspol targets high-purity industrial dispersants with continuous sulfonation and specialty application focus

Enaspol a.s. specializes in high-purity naphthalene sulfonate condensates for textile, leather, and specialty industrial applications. Its Spolostan 3L/4L series ensures uniform dye dispersion and color consistency in premium leather processing. The company’s continuous sulfonation technology guarantees stable active matter content (≥34%), critical for precision-driven industries. Enaspol is expanding into agriculture and paper sectors, supplying dispersants for pesticides and wettable powders. Its compliance with EU regulatory standards and recognition under Responsible Care® highlight its commitment to safe and sustainable production. This niche focus on high-purity, specialty applications differentiates Enaspol in the global market.

China: Regulatory Precision, Water-Based Reformulation, and Semiconductor Localization

China’s naphthalene sulfonate market is entering a compliance-driven reform cycle anchored in national standards and green manufacturing mandates. The most consequential trigger is the June 2026 implementation of GB 30981.1-2025 by the State Administration for Market Regulation, which imposes stricter limits on harmful substances in architectural coatings. This standard is forcing paint and coating formulators to migrate toward high-purity naphthalene sulfonate dispersants with materially lower residual formaldehyde. Parallel to coatings, China’s revised RoHS framework GB 26572-2025, effective late 2025, bans four major phthalates in electronic equipment, accelerating the adoption of SNF-based alternatives in plasticizer systems for electrical and electronic equipment housings.

Industrial execution is matching regulatory ambition. Throughout 2025, the Jiangbei New Material Technology Park advanced digital process controls across SNF production lines to achieve ultra-low VOC profiles aligned with the Green Manufacturing blueprint under the 14th Five-Year Plan, overseen by the Ministry of Industry and Information Technology. Shandong’s industrial zones are further subsidizing the shift from solvent-based to water-based coatings, where SNF functions as the primary dispersant for carbon black and inorganic pigments. Beyond construction and coatings, 2025 pilot work at Suzhou Industrial Park validated naphthalene sulfonate derivatives for CMP slurry formulations, supporting domestic self-sufficiency in 12-inch wafer processing. Logistics has also tightened, with GB 12268-2025 reclassifying liquid SNF transport from October 2025, standardizing packaging and increasing trans-provincial logistics costs for ready-mix concrete suppliers.

India: Infrastructure Push, Textile Demand, and Green Feedstock Pathways

India’s SNF demand profile is being shaped by public infrastructure spending and downstream industrial expansion. Under the Scheme for Special Assistance to States for Capital Investment for 2025–26, government priorities around highways and bridges are driving sustained uptake of SNF-based superplasticizers for standard-grade structural concrete, particularly across Tier-2 urban developments. Upstream stability has improved following the first major profit reported in Q2 2025 by the GACL–NALCO Alkalies & Chemicals joint venture, ensuring consistent chlorine and caustic soda availability for domestic sulfonation.

Demand diversification is equally pronounced. The Indian textile and apparel sector, valued above $100 billion in 2025, is increasing consumption of naphthalene sulfonate as a dye-leveling agent in high-temperature jet dyeing, notably across the Tiruppur cluster. Capacity additions are underway, with late-2025 brownfield expansions in Taloja adding 53,000 MTPA of naphthalene derivative capacity focused on plasticizer applications. Looking forward, early-2026 academic–industry breakthroughs demonstrated renewable naphthalene synthesis from furfural using zeolite catalysts, outlining a credible pathway for green SNF. Regulatory momentum will continue with the Pesticide Management Bill 2026, which mandates enhanced transparency on adjuvant safety and rain-fastness, raising technical documentation requirements for SNF suppliers serving agriculture.

Germany: Portfolio Consolidation, REACH Compliance, and Digitalized Admixtures

Germany’s SNF landscape is defined by consolidation, regulatory rigor, and digitally enabled formulation. A pivotal structural change occurred in February 2025 when Saint-Gobain completed the acquisition of Fosroc, consolidating a global portfolio of SNF and PCE admixtures under the Chryso and GCP brands. This integration strengthens bargaining power with construction majors while accelerating the transition toward low-impurity grades demanded by EU markets.

Regulation is intensifying this shift. Under 2026 REACH updates administered by the European Chemicals Agency, German SNF producers registering above the 10,000-tonne threshold must submit enhanced toxicity datasets, accelerating investment in cleaner sulfonation routes. Strategic initiatives are reinforcing competitiveness. Sika launched its Fast Forward program in November 2025, committing CHF 120–150 million to digitalization aimed at optimizing admixture supply chains and margin performance by 2026. Sustainability pilots at the Leuna Chemical Complex are integrating offshore wind electricity into sulfonation, cutting Scope 2 emissions by roughly 30%, while AI-driven co-creation platforms allow construction firms to tailor SNF water reducers to specific cement chemistries and site temperatures.

United States: Compliance Pressure, Infrastructure Resilience, and Process Efficiency

In the United States, regulatory oversight and infrastructure investment are jointly reshaping SNF production and use. Under TSCA Section 8(d), the Environmental Protection Agency has required the submission of unpublished health and safety studies for 16 chemicals used in sulfonation across 2025–2026. This scrutiny is pushing formulators toward NSF and ANSI-certified SNF grades, particularly for potable water-contact and public infrastructure applications. Concurrently, the Department of Energy expanded funding in late 2025 for amine-based carbon capture pilots, where SNF is being evaluated as a stabilizing additive in solvent regeneration cycles for post-combustion capture.

Market fundamentals remain supportive. Despite trade policy uncertainty, U.S. precast concrete demand stayed resilient through 2025, driven by data center construction and bridge rehabilitation projects under the Infrastructure Investment and Jobs Act. Operational efficiency is improving at the plant level. In September 2025, a major North American admixture facility installed a closed-loop chiller system, reducing water consumption by 40% in the energy-intensive naphthalene sulfonation process, reinforcing the industry’s pivot toward lower operating footprints and improved compliance economics.

Comparative Snapshot: Country Positioning in the Naphthalene Sulfonate Market

Naphthalene Sulfonate Market County Level Snapshot

|

Country

|

Primary Demand Drivers

|

Strategic Shift

|

Structural Outcome

|

|

China

|

Coatings, electronics, semiconductors

|

National standards and water-based reformulation

|

High-purity SNF and domestic substitution

|

|

India

|

Infrastructure, textiles, agrochemicals

|

Capacity expansion and renewable feedstocks

|

Volume growth with rising documentation rigor

|

|

Germany

|

Construction chemicals

|

Consolidation, REACH compliance, digitalization

|

Low-impurity, customized admixtures

|

|

United States

|

Precast concrete, carbon capture

|

TSCA compliance and process efficiency

|

Certified grades and closed-loop operations

|

Naphthalene Sulfonate Market Report Scope

Naphthalene Sulfonate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.4 Billion

|

|

Market Size (2034)

|

$3.4 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Product Type (Naphthalene Sulfonate Formaldehyde, Alkyl Naphthalene Sulfonates, Naphthalene Sulfonate Salts), By Form (Powder, Liquid), By Functionality (Dispersing Agents, Wetting Agents, Surfactants, Plasticizers and Water Reducers), By Application (Concrete Admixtures, Dyes and Pigments, Agrochemicals, Household and Industrial Detergents, Pharmaceuticals, Oil and Gas), By End-Use Industry (Construction and Infrastructure, Textiles and Apparel, Agriculture, Oil and Gas, Pulp and Paper)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Sika, Saint-Gobain, Kao, Mapei, Himadri Specialty Chemical, Rain Carbon, JFE Chemical, Koppers, MUHU Construction Materials, Shandong Wanshan Chemical, Guzman Polymers, Bisley, Hubei Aging Chemical, Gujarat Alkalies and Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Naphthalene Sulfonate Market Segmentation

By Product Type

- Naphthalene Sulfonate Formaldehyde

- Alkyl Naphthalene Sulfonates

- Naphthalene Sulfonate Salts

By Form

By Functionality

By Application

- Concrete Admixtures

- Dyes and Pigments

- Agrochemicals

- Household and Industrial Detergents

- Pharmaceuticals

- Oil and Gas

By End-Use Industry

- Construction and Infrastructure

- Textiles and Apparel

- Agriculture

- Oil and Gas

- Pulp and Paper

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Naphthalene Sulfonate Market

- BASF

- Sika

- Saint-Gobain

- Kao

- Mapei

- Himadri Specialty Chemical

- Rain Carbon

- JFE Chemical

- Koppers

- MUHU Construction Materials

- Shandong Wanshan Chemical

- Guzman Polymers

- Bisley

- Hubei Aging Chemical

- Gujarat Alkalies and Chemicals

*- List not Exhaustive