Linear Alkylbenzene Sulfonate Market 2025–2034: Low-Carbon LAB, Capacity Expansion, and Surfactant Value Chain Integration Driving $37.5 Billion Outlook at 8.7% CAGR

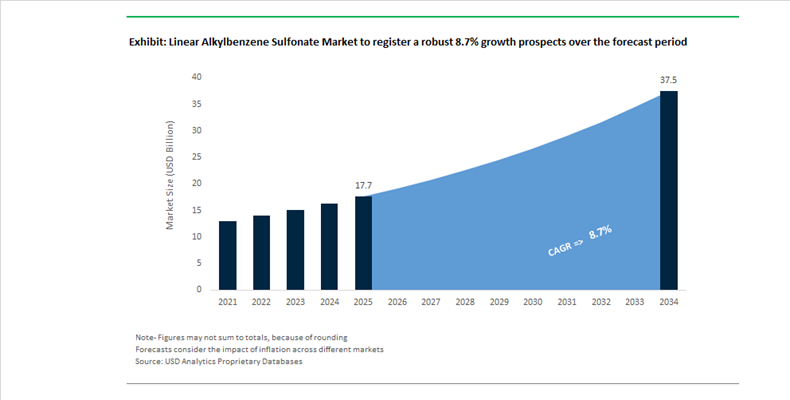

The Linear Alkylbenzene Sulfonate (LAS) Market is projected to expand from $17.7 billion in 2025 to $37.5 billion by 2034, registering a strong CAGR of 8.7%. Growth is being fueled by rising demand for anionic surfactants in household detergents, industrial cleaners, institutional sanitation, and personal care formulations. LAS remains the dominant workhorse surfactant due to its high detergency, biodegradability profile, and cost-performance balance compared to alternative surfactant chemistries. Increasing urbanization, higher per capita detergent consumption in emerging economies, and expanding industrial cleaning standards are strengthening long-term consumption of LAB and downstream sulfonated derivatives.

In early 2024, Farabi Petrochemicals unveiled a $950 million LAB plant in Yanbu, Saudi Arabia, significantly increasing global supply of linear alkylbenzene, the primary precursor for LAS production, targeting export markets across Africa and Europe. In April 2024, Tamilnadu Petroproducts Limited partnered with EY-Parthenon to establish a carbon-neutral roadmap focused on decarbonizing sulfonation processes. In September 2024, TPL announced a ₹405 Crore investment to expand LAB and caustic soda capacities, with commissioning expected by 2026 to address surging domestic detergent demand. Throughout 2024, India imposed anti-dumping duties on LAB imports, strengthening domestic production economics and prompting higher capacity utilization by integrated players such as Reliance Industries and Indian Oil Corporation. These regulatory and capital investments reinforce regional self-sufficiency in LAB-to-LAS conversion.

Decarbonization and technology optimization are reshaping the surfactant manufacturing landscape. In late 2024 and 2025, Cepsa Química expanded production of NextLab-R Low Carbon at its Puente Mayorga facility, introducing the first LAB with a cradle-to-gate negative carbon footprint derived from renewable energy and waste-based feedstocks. In 2025, Moeve and Honeywell expanded their alliance to scale renewable LAB production using Ecofining technology, targeting bio-based LAS for eco-label detergent brands. In mid-2025, Stepan Company commissioned a new alkoxylation facility in Pasadena, Texas, enhancing blending flexibility for high-performance cleaning formulations incorporating LAS. In October 2025, BASF divested its Brazilian decorative paints business to refocus on integrated chemical value chains, including surfactant intermediates. In late December 2025, Sasol restarted its Louisiana cracker, ensuring ethylene stability within the paraffin-to-LAB chain despite soft global chemical conditions. In January 2026, Desmet Ballestra marked 80 years of engineering leadership, continuing global deployment of advanced falling film sulfonation reactors that enable high-purity LAS production with minimal byproducts, particularly across Southeast Asia and South America.

Strategic Trends and High-Impact Opportunities Shaping the Linear Alkylbenzene Sulfonate Market

Trend: Vertical Integration into Bio-Based Linear Alkylbenzene Feedstocks

The linear alkylbenzene sulfonate market is entering a decisive transition phase as producers pursue vertical integration into renewable feedstocks to address Scope 3 emissions and long-term carbon risk. Traditional petrochemical routes based on crude-oil-derived paraffins are increasingly viewed as structurally misaligned with brand-level climate commitments and regulatory expectations. As a result, leading manufacturers are investing in captive production of renewable linear alkylbenzene that can be used as a direct input for LAS without altering downstream sulfonation assets.

A landmark development occurred in November 2025 when Moeve and Honeywell UOP expanded their collaboration to industrialize NextLab-R, the first LAB produced entirely from renewable raw materials. This technology enables a drop-in substitution in existing LAS plants, allowing detergent brands to reduce lifecycle emissions without operational disruption. Parallel to this, suppliers such as Indorama Ventures and Sasol are scaling ISCC+ mass-balance certification to transition portfolios toward bio-based and recycled carbon inputs. Indorama’s high placement in ChemScore 2025 reflects accelerated phase-out of hazardous legacy chemistries in favor of sustainable surfactant feedstocks. Upstream diversification is also extending into biotechnology. Unilever has committed capital from its Climate and Nature Fund into biomass initiatives, including partnerships with Nufarm to develop energy cane as a sustainable carbon source for surfactant production.

Trend: Reformulation Focused on Cold-Water Performance and Energy Compliance

Energy efficiency has become a primary performance metric for LAS-based detergents as regulators and appliance manufacturers target reductions in household energy use. Heating water accounts for a majority of washing machine energy consumption, making cold-water efficacy a central requirement for next-generation surfactant systems. This is reshaping LAS formulation strategies toward improved soil removal, lipid solubilization, and enzyme compatibility at temperatures as low as 20 degrees Celsius.

Regulatory momentum is reinforcing this shift. The EU Detergents Regulation adopted in late 2025 introduces stricter biodegradability thresholds and mandates digital product passports for traceability, accelerating the transition toward high-performance LAS blends optimized for eco-modes. Industry leaders are already demonstrating commercial impact. Procter & Gamble reported in 2025 that more than half of wash loads in North America are now run in cold water, supported by optimized LAS and enzyme systems that reduce energy use by approximately 90% per load. Product innovation is extending into fabric-specific performance. In February 2025, Henkel introduced Persil Activewear Clean, highlighting how advanced LAS chemistry can effectively remove body oils and odors from synthetic textiles at low temperatures where conventional surfactants underperform.

Opportunity: Ultra-Concentrated LAS Formulations for E-Commerce and Direct-to-Consumer Channels

The rapid expansion of e-commerce and subscription-based detergent models is creating a high-margin opportunity for ultra-concentrated LAS formulations. Direct-to-consumer logistics favor low-volume, lightweight products that deliver equivalent cleaning power at three to four times traditional concentration levels. This places a premium on LAS grades with low viscosity, high solubility, and long-term stability in compact liquid and pod formats.

Manufacturers are actively responding. In 2025, Henkel upgraded formulations across its All and Persil liquid detergents, increasing concentration by 16% while incorporating recycled plastic packaging. These changes are estimated to save millions of gallons of water and several thousand tonnes of carbon dioxide annually through reduced packaging and transport. E-commerce readiness is also influencing process design. High-speed automated filling lines require LAS systems that resist gel formation and ensure consistent flow. At the same time, subscription-based sheet and pod formats are leveraging LAS cost efficiency and cleaning strength to minimize shipping weights and warehouse footprints, reinforcing concentrated LAS as a core enabler of digital detergent business models.

Opportunity: Engineered LAS for Automated Laundry-as-a-Service Systems

The growth of commercial and shared laundry infrastructure is opening a specialized opportunity for engineered LAS tailored to automated dosing environments. Laundry-as-a-service models are expanding rapidly across Asia-Pacific, the Middle East, and Africa, driven by urbanization and demand for cost-efficient fabric care in multi-housing developments. These systems require surfactants with predictable flow behavior, rapid dissolution, and consistent performance under continuous operation.

Technology convergence is accelerating adoption. At CES 2025, Henkel showcased its Smartwash Technology, an AI-enabled cartridge dosing platform that adjusts surfactant delivery based on load size and soil level. Such systems require LAS formulations engineered for micro-dosing accuracy to avoid clogging and under- or over-dosing. Commercial laundry growth in regions such as Lagos, Nairobi, and Mumbai is further increasing demand for high bulk-density LAS powders suited for high-throughput machines. Appliance manufacturers are increasingly co-developing smart dispensing systems with chemical suppliers, ensuring that LAS-based detergents are precisely calibrated to machine algorithms. This machine-chemical interdependence positions engineered LAS as a critical component of the next generation of automated fabric care ecosystems.

Linear Alkylbenzene Sulfonate Market Share and Segmentation Insights

Sodium Linear Alkylbenzene Sulfonate Leads the Market Through High-Performance Detergency in Cleaning Formulations

Sodium Linear Alkylbenzene Sulfonate (Sodium LAS) accounted for 68.40% of the Linear Alkylbenzene Sulfonate Market share in 2025, making it the dominant product form used in global detergent manufacturing. Sodium LAS is the neutralized form of linear alkylbenzene sulfonic acid, widely used as a high-performance anionic surfactant in household and institutional cleaning formulations. It provides strong detergency, foaming capability, grease removal efficiency, and tolerance to hard water conditions, which are essential characteristics for laundry detergents, dishwashing liquids, and multi-purpose cleaning agents. Sodium LAS is also valued for its cost effectiveness, formulation stability, and compatibility with builders, enzymes, and other detergent additives, enabling manufacturers to develop versatile cleaning products for mass-market use. In 2025, the continued shift toward concentrated liquid detergents and single-dose detergent pods has encouraged surfactant suppliers to optimize sodium LAS formulations with higher active concentrations and improved stability, ensuring consistent cleaning performance in compact detergent formats.

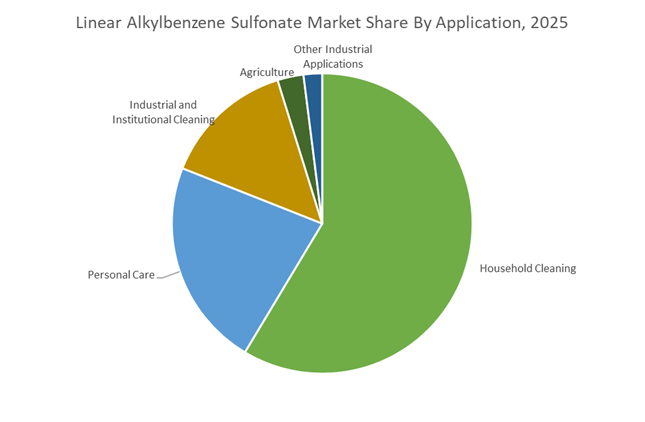

Household Cleaning Sector Drives the Largest Demand for Linear Alkylbenzene Sulfonate

Household cleaning accounted for 58.60% of the Linear Alkylbenzene Sulfonate Market share in 2025, establishing it as the largest application segment for LAS surfactants. Linear alkylbenzene sulfonate remains the primary anionic surfactant used in laundry detergents, dishwashing liquids, and surface cleaners, due to its excellent ability to remove oils, dirt, and particulate soils from fabrics and surfaces. The global scale of detergent consumption ensures sustained demand for LAS across household laundry care, kitchen cleaning, and general home sanitation products. Manufacturers rely on LAS because it delivers consistent cleaning performance across a wide range of water hardness levels and washing conditions, while maintaining cost efficiency in high-volume detergent production. In 2025, evolving consumer habits and sustainability initiatives have accelerated the shift toward cold water washing practices, aimed at reducing household energy consumption. Detergent producers have therefore optimized LAS-based formulations for improved solubility and cleaning efficiency at lower washing temperatures, enabling effective stain removal while supporting energy-efficient laundry practices.

Linear Alkylbenzene Sulfonate Market Competitive Landscape

The Linear Alkylbenzene Sulfonate (LAS) market in 2026 is defined by low-carbon LAB production, ZDHC-compliant surfactants, and circular feedstock integration. Competition is intensifying around renewable-based intermediates, Scope 1 and 2 emission reduction, and high-performance formulations for liquid detergents and unit-dose applications across global FMCG supply chains.

CEPSA drives low-carbon LAB innovation with renewable feedstocks and Detal Plus technology

CEPSA Química (Moeve) leads the LAS value chain through its dominance in Linear Alkylbenzene (LAB) production, accounting for ~18% of global capacity. Its NextLab-R Low Carbon portfolio introduces “beyond zero” carbon LAB using renewable heat and feedstocks, enabling detergent manufacturers to adopt drop-in sustainable surfactants without reformulation. Implementation of Detal Plus technology reduces water consumption by 40% and eliminates hydrofluoric acid catalysts, strengthening environmental compliance. Recognition from Henkel underscores CEPSA’s strategic importance in enabling low-carbon detergent supply chains aligned with ZDHC and FMCG sustainability mandates.

Stepan optimizes high-purity LAS production for advanced detergent formulations

Stepan Company is strengthening its position in anionic surfactants by focusing on high-active LAS grades tailored for liquid and unit-dose detergents. Its “smart-capacity” expansion strategy targets emerging markets, enabling localized production aligned with rising FMCG demand. The company emphasizes biodegradability and low aquatic toxicity, positioning LAS as a safe and effective surfactant under tightening regulatory frameworks. Strong formulation expertise allows Stepan to integrate LAS with secondary surfactants, delivering enhanced detergency, foam stability, and cold-water washing performance critical for next-generation laundry and dishwashing products.

BASF expands LAS-based home care solutions with regional manufacturing and green transformation strategy

BASF SE integrates LAS into its Home Care and Industrial & Institutional (I&I) portfolio, focusing on region-specific innovation and sustainability-driven manufacturing. Expansion of its Mangalore facility enhances supply for Asia-Pacific markets, particularly for high-performance cleaning chemicals. Its Lutensit® and Plurafac® portfolios leverage LAS as a core surfactant base for industrial degreasing and institutional cleaning. Through its “Winning Ways” strategy and Innovation Campus Mumbai, BASF is developing LAS formulations optimized for hard water conditions, while advancing low-carbon production and aligning with global detergent manufacturers’ sustainability transitions.

Sasol secures feedstock advantage with n-paraffin integration and renewable energy investments

Sasol Limited leverages its coal-to-liquids and gas-to-liquids technologies to ensure a stable supply of high-quality n-paraffins, a critical feedstock for LAB and LAS production. Improved Secunda Operations output and destoning technology enhance feedstock consistency, strengthening downstream surfactant production. The company’s investment in over 1,200 MW of renewable energy capacity supports lower-carbon chemical intermediates, aligning with global decarbonization targets. Its International Chemicals reset strategy focuses on cost optimization and margin improvement, reinforcing its competitive position in the global LAS supply chain.

Reliance dominates regional LAB and LAS supply through integrated petrochemical scale

Reliance Industries Limited (RIL) is a key supplier in the Asia-Pacific LAS market, leveraging its fully integrated refining and petrochemical ecosystem to achieve cost leadership and supply reliability. Its focus on high-purity LAB grades (LAB 26 and LAB 28) supports advanced detergent formats such as liquid capsules, ensuring consistent surfactant performance. Dominance in LABSA supply within India positions RIL at the center of domestic and multinational FMCG value chains. Ongoing exploration of recycled feedstock integration reflects its strategic shift toward circular petrochemicals and sustainable surfactant intermediates.

Clariant enhances LAS performance with specialty additives and ESG-compliant formulations

Clariant is differentiating in the specialty segment by enhancing LAS-based formulations with performance additives that improve efficiency, mildness, and sustainability. Its focus on ESRS compliance enables customers to meet stringent environmental reporting and lifecycle transparency requirements. Portfolio optimization toward high-margin specialty chemicals has driven EBITDA margins to 17.8%, supporting continued innovation. Developments in concentrated liquid detergents and skin-mild surfactant systems highlight Clariant’s role in advancing eco-conscious, high-performance LAS applications across home care and personal care markets.

United States: Performance-Led Reformulation and Industrial Diversification of LAS

The United States Linear Alkylbenzene Sulfonate market is being reshaped by a dual focus on performance-led detergent reformulation and expansion into higher-value industrial applications. In 2025, Stepan Company reported a 10% increase in surfactant net sales during Q1, driven primarily by double-digit demand from agricultural adjuvants and oilfield chemicals. This demand profile highlights a structural shift away from purely commodity household detergents toward application-specific LAS grades that offer controlled foaming, emulsification stability, and compatibility with complex formulations. At the same time, Stepan disclosed negative free cash flow linked to higher working capital deployment, a deliberate move to secure raw materials and inventory buffers ahead of potential 2025–2026 trade tariff volatility.

From a formulation standpoint, U.S. detergent majors such as Henkel are accelerating the transition toward concentrated liquid laundry systems. This evolution is pushing LAS chemistry toward higher solubility, improved cold-water detergency, and better rinse performance to align with Department of Energy 2026 energy efficiency standards. Beyond consumer cleaning, North American manufacturers are scaling LAS usage in emulsion polymerization, industrial lubricants, and metalworking fluids, where LAS is increasingly deployed as a coupling agent to replace less biodegradable branched surfactants. This diversification is reinforcing the role of LAS as a multi-sector surfactant platform rather than a single-use detergent ingredient.

China: Self-Sufficiency Mandates and Catalyst-Driven Yield Optimization

China’s LAS market is being actively restructured under industrial policy that prioritizes self-sufficiency, efficiency, and environmental compliance. In September 2025, the Ministry of Industry and Information Technology released a petrochemical stabilization work plan targeting over 5% annual growth in sectoral added value. Within this framework, traditional surfactants such as LAS are being repositioned as integrated chemical solutions, tightly linked with upstream LAB production and downstream formulation services. A central objective is the increase of domestic LAB self-sufficiency from roughly 85% to above 90% by late 2026, reducing exposure to imported intermediates.

Technological upgrading is a key enabler of this transition. In December 2025, Clariant showcased progress in catalyst systems developed in partnership with Chinese national programs, aimed at improving linear alkyl chain selectivity and yield. These advancements directly enhance the purity and biodegradability of finished LAS. Parallel regulatory pressure is intensifying. New 2026 chemical park rules require LAS producers to deploy AI-driven process optimization to cut VOC emissions and waste energy by approximately 12%. As a result, Chinese LAS producers are investing simultaneously in digital process control and greener sulfonation technologies to remain compliant while maintaining scale.

India: Refinery Integration and Standards-Led Market Formalization

India’s LAS market is benefiting from expanding petrochemical infrastructure and a sharper regulatory focus on quality and standards enforcement. In April 2025 alone, national petrochemical output reached 1,763 thousand metric tonnes, supported by substantial Union Budget allocations to the Ministry of Chemicals and Fertilizers. A pivotal structural development is the Rajasthan Refinery Limited project, scheduled for commercial operation by March 31, 2026, which is expected to materially strengthen the regional supply of kerosene and related feedstocks essential for LAB and LAS manufacturing.

On the corporate side, Reliance Industries Limited continues to anchor domestic LAS production with approximately 135 KTPA of LAB capacity across its Patalganga and Vadodara facilities. The use of UOP HF-alkylation technology supports high linearity and biodegradability, aligning Indian LAS output with international detergent specifications. Regulatory tightening is reinforcing this quality orientation. From February 2025, Quality Control Orders covering more than 150 chemical products mandate strict purity and performance benchmarks for surfactants used in household appliances, limiting the entry of sub-standard imports and formalizing demand for compliant LAS grades.

Thailand and Southeast Asia: Sustainability Capital Recycling and Bio-Based Innovation

Southeast Asia, led by Thailand, is positioning itself as a sustainability and innovation hub for LAS formulations. Indorama Ventures is executing its IVL 2.0 transformation strategy through 2025, emphasizing asset rationalization and reinvestment into higher-growth specialty chemicals. The company expects to unlock more than $200 million in 2026 from divesting non-core assets, capital that is being redirected toward surfactant innovation and sustainability upgrades.

At the Sustainability Expo 2025, Indorama Ventures highlighted a $33 million R&D commitment and the development of hundreds of new products, including bio-based surfactants designed to lower the carbon footprint of conventional LAS systems. This strategic direction is reinforced by external validation. In December 2025, IVL ranked first globally in the ChemScore 2025 index, underscoring best-in-class performance in chemicals management and environmental safety. For LAS, this translates into formulations that retain cost competitiveness while improving lifecycle metrics, particularly for export-oriented detergent manufacturers.

South Korea: Performance Optimization and Export-Oriented Purity

South Korea’s LAS market is carving out a niche based on formulation performance and export quality. In October 2025, ISU Chemical announced a technical breakthrough that significantly improves LAS dissolution speed in water. This advancement directly targets the fast-growing quick-wash detergent segment, where shorter cycles and lower water usage demand rapid surfactant activation and minimal residue.

From a trade perspective, South Korean producers are actively leveraging the China plus one sourcing strategies adopted by global buyers. By supplying LAS grades with purity levels above 98%, manufacturers are expanding exports to Europe and North America, particularly for premium personal care and specialty cleaning formulations. This export orientation is reinforcing South Korea’s role as a supplier of high-specification LAS rather than bulk commodity volumes.

Linear Alkylbenzene Sulfonate Market: Country-Level Strategic Snapshot

Linear Alkylbenzene Sulfonate Market County Level Snapshot

|

Country / Region

|

Primary Strategic Focus

|

Key LAS Differentiator

|

Market Implication

|

|

United States

|

Reformulation and industrial diversification

|

Cold-water solubility and coupling performance

|

Shift toward multi-sector, high-function LAS

|

|

China

|

Self-sufficiency and digital efficiency

|

Catalyst-driven purity and AI-enabled compliance

|

Integrated, policy-aligned LAS supply chains

|

|

India

|

Refinery integration and standards enforcement

|

High-linearity, QCO-compliant LAS

|

Formalized domestic market with export readiness

|

|

Thailand & Southeast Asia

|

Sustainability reinvestment

|

Bio-based and low-carbon LAS

|

ESG-led differentiation for global brands

|

|

South Korea

|

Performance and export purity

|

Fast-dissolving, high-purity LAS

|

Premium positioning in global detergent markets

|

Linear Alkylbenzene Sulfonate Market Report Scope

Linear Alkylbenzene Sulfonate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.7 Billion

|

|

Market Size (2034)

|

$37.5 Billion

|

|

Market Growth Rate

|

8.7%

|

|

Segments

|

By Type (Linear Alkylbenzene Sulfonic Acid, Sodium Linear Alkylbenzene Sulfonate, Calcium Linear Alkylbenzene Sulfonate), By Purity Level (Standard Purity, High Purity, Ultra-High Purity), By Formulation (Liquid or Slurry, Powder or Granules, Paste), By Application (Household Cleaning, Personal Care, Industrial and Institutional Cleaning, Agriculture, Other Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Stepan Company, Clariant AG, Indorama Ventures Public Company Limited, Reliance Industries Limited, Sasol Limited, BASF SE, China Petroleum and Chemical Corporation, ISU Chemical, PetroChina Company Limited, Kao Corporation, Indian Oil Corporation Limited, Moeve, Nirma Limited, Unggul Indah Cahaya, Farabi Petrochemicals Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Linear Alkylbenzene Sulfonate Market Segmentation

By Type

- Linear Alkylbenzene Sulfonic Acid

- Sodium Linear Alkylbenzene Sulfonate

- Calcium Linear Alkylbenzene Sulfonate

By Purity Level

- Standard Purity

- High Purity

- Ultra-High Purity

By Formulation

- Liquid or Slurry

- Powder or Granules

- Paste

By Application

- Household Cleaning

- Personal Care

- Industrial and Institutional Cleaning

- Agriculture

- Other Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Linear Alkylbenzene Sulfonate Market

- Stepan Company

- Clariant AG

- Indorama Ventures Public Company Limited

- Reliance Industries Limited

- Sasol Limited

- BASF SE

- China Petroleum and Chemical Corporation

- ISU Chemical

- PetroChina Company Limited

- Kao Corporation

- Indian Oil Corporation Limited

- Moeve

- Nirma Limited

- Unggul Indah Cahaya

- Farabi Petrochemicals Company

*- List not Exhaustive