Metal Packaging Coatings Market Size, BPA-NI Innovation, and Sustainable Can Coatings Outlook

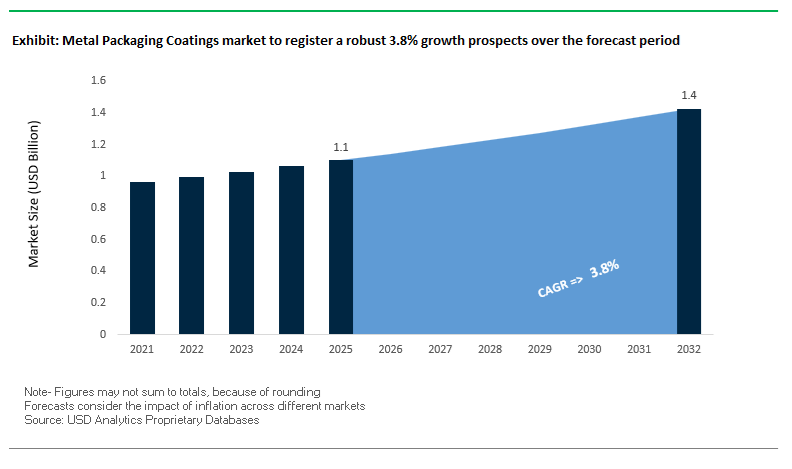

The global metal packaging coatings market was valued at $1.1 billion in 2025 and is projected to reach $1.4 billion by 2032, growing at a CAGR of 3.8%. Market expansion is being driven by rising demand for BPA-NI (Bisphenol A Non-Intent) coatings, PFAS-free coatings, water-based can coatings, UV-curable coatings, and food-safe packaging coatings across beverage cans, food containers, aerosol packaging, and specialty metal packaging applications. As global food safety regulations tighten and consumer awareness around chemical migration and packaging safety increases, manufacturers are rapidly transitioning toward non-toxic, compliant coating systems.

A key growth driver is the increasing demand for sustainable and regulatory-compliant packaging solutions, particularly in the beverage and ready-to-eat food sectors. Coatings must deliver high corrosion resistance, flexibility, adhesion, and chemical inertness while ensuring no interaction with packaged contents. Additionally, the rise of aluminum beverage cans and recyclable metal packaging is boosting the need for advanced coating technologies that support high-speed production lines and extended shelf life.

The market is also benefiting from innovation in energy-efficient curing technologies, bio-based resins, and advanced polymer systems, enabling reduced carbon footprint and operational costs. The shift toward UV/LED curing systems, waterborne formulations, and solvent-free coatings is accelerating, particularly in Europe and North America, where sustainability mandates are stringent. Asia-Pacific remains a key growth region due to expanding food and beverage manufacturing capacity and urban consumption patterns.

Market Analysis: UV-Curable Technologies, BPA-Free Innovation, and Strategic Consolidation Driving Market Evolution

The metal packaging coatings industry is undergoing a structural shift driven by regulatory compliance, sustainability innovation, and digital transformation in coating processes. In April 2026, ACTEGA showcased UV and UV/LED curable coatings under the ACTNext brand at METPACK, eliminating the need for gas-powered drying ovens and significantly reducing CO₂ emissions and energy consumption in metal decorating lines. This represents a major advancement in energy-efficient coating technologies.

Product innovation is increasingly focused on food safety and performance optimization. In March 2026, Henkel Adhesive Technologies introduced Darex WBC 4020, a water-based sealant for beverage cans, designed to enhance application efficiency and line speeds while maintaining stringent food-contact safety standards. Similarly, Nippon Paint’s May 2025 launch of hybrid polyester-silicone coatings targets retortable food cans, ensuring durability under high-pressure sterilization conditions without compromising adhesion or aesthetics.

Strategic consolidation is reshaping competitive dynamics. The February 2026 merger between AkzoNobel and Axalta is particularly significant for the packaging segment, combining AkzoNobel’s BPA-NI technology leadership with Axalta’s global industrial footprint. This merger is expected to influence global R&D direction and specification standards for metal packaging coatings.

Sustainability remains a central theme across product development. PPG Industries has been at the forefront with its INNOVEL® and INNOVEL® PRO coating systems, which are PFAS-free and BPA-NI compliant, gaining widespread adoption in the beverage sector. In July 2025, PPG expanded this range to include easy-open end (EOE) coatings, addressing evolving packaging design requirements. The company’s sustainability leadership was further recognized with a 2024 SEAL Sustainable Product Award, reinforcing the role of coatings in enabling safe and recyclable packaging systems.

Operational efficiency and digitalization are also transforming the industry. Sherwin-Williams’ January 2026 AI-driven pilot plant significantly reduces coating development and prototyping cycles, accelerating time-to-market for new packaging solutions. Meanwhile, Metlac’s March 2025 capacity expansion in Europe reflects strong demand for BPA-NI internal lacquers, particularly in craft beverages and personal care packaging.

Innovations in packaging design and materials are further expanding the role of coatings. ACTEGA’s Signite technology, highlighted in January 2025, replaces traditional plastic labels with functional coating layers, reducing material usage and enhancing recyclability. Additionally, PPG’s December 2025 sustainability milestone, with over 40% of sales from sustainably advantaged products, underscores the rapid shift toward eco-friendly coating solutions.

Market Trend: BPA-NI Epoxy Hybrid Coatings Becoming the Global Standard for Food-Contact Metal Packaging

The metal packaging coatings industry is undergoing a structural transformation as Bisphenol A Non-Intent (BPA-NI) systems transition from optional alternatives to mandatory solutions. This shift is primarily driven by Regulation (EU) 2024/3190, which enforces a comprehensive ban on BPA in food-contact materials. The regulation establishes a clear compliance deadline of July 20, 2026, after which traditional BPA-based epoxy coatings will no longer be permitted for internal can linings across the European Union.

This regulatory pressure is accelerating large-scale reformulation across the value chain, with coating manufacturers rapidly advancing BPA-NI epoxy hybrid systems to achieve full performance equivalence. Recent pack-test data confirms that modern BPA-NI coatings deliver over 98% success rates in long-term stability testing for aggressive food matrices such as acidic vegetables and fermented products. These results effectively close the historical performance gap between BPA-free alternatives and legacy bisphenol-based systems, particularly in corrosion resistance and flavor preservation over 24-month shelf life cycles.

Adoption is particularly advanced in the beverage segment, where scalability and regulatory exposure are highest. By early 2026, approximately 85% of newly installed aluminum beverage can lines in North America and Europe have transitioned to BPA-NI internal coatings. This reflects a proactive strategy by global brands to mitigate regulatory risk and align with evolving consumer safety expectations. The convergence of regulatory enforcement, technological maturity, and brand-driven sustainability commitments is firmly establishing BPA-NI coatings as the baseline standard in modern metal packaging.

Market Trend: Ultra-Thin Powder Coatings Driving Efficiency and Zero-VOC Manufacturing in Easy-Open Ends (EOE)

The Easy-Open End (EOE) segment is experiencing a rapid shift toward ultra-thin powder coating systems as manufacturers seek to optimize material efficiency, reduce emissions, and maintain high-speed production capabilities. Traditional liquid lacquer systems are increasingly being replaced by powder coatings that offer superior uniformity and environmental performance without compromising throughput.

Ultra-thin powder systems are capable of achieving consistent, pinhole-free coatings at dry film thicknesses of 20 to 30 microns. This represents a 20% to 30% reduction in coating weight compared to conventional liquid applications, directly lowering raw material consumption and associated costs. The ability to maintain coating integrity at reduced thickness is particularly valuable in high-volume can manufacturing, where marginal material savings scale significantly across production volumes.

Environmental performance is a major driver of this transition. Powder coatings enable zero-VOC processing by eliminating solvent carriers, resulting in more than 95% reduction in hazardous air pollutant emissions. This allows manufacturers to bypass capital-intensive emission control systems such as regenerative thermal oxidizers, significantly improving plant economics and regulatory compliance.

In terms of production efficiency, electrostatic powder application systems have reached line speeds exceeding 2,000 ends per minute, matching or exceeding traditional liquid coating processes. Additionally, powder systems eliminate edge-pull defects commonly associated with liquid coatings, ensuring uniform coverage across complex geometries. These combined advantages are positioning ultra-thin powder coatings as a next-generation solution for high-speed, sustainable metal packaging production.

Market Opportunity: Proposition 65 BPS Listing Creating Demand for Bisphenol-Free (BP-Total Free) Coating Chemistries

The addition of Bisphenol S (BPS) to California’s Proposition 65 list is creating a significant disruption in the metal packaging coatings market, particularly for manufacturers that previously transitioned from BPA to BPS-based alternatives. Effective December 2025, the classification of BPS as a reproductive and developmental toxicant introduces a 12-month compliance window, requiring product labeling or reformulation by December 2026.

This regulatory development is exposing a “regrettable substitution” gap, where coatings marketed as BPA-free are now subject to renewed scrutiny due to their reliance on structurally similar bisphenol compounds. As a result, there is a growing demand for Bisphenol-Total (BP-Total) free coating systems that eliminate the entire class of bisphenol chemistries. This shift is creating opportunities for alternative resin platforms, including acrylic, polyester, and polyolefin-based dispersions, which offer safer chemical profiles while maintaining performance requirements for food-contact applications.

The reformulation wave is expected to impact a substantial portion of the existing BPA-NI market, particularly in regions with strict chemical disclosure and labeling requirements. Coating suppliers that have already invested in non-bisphenol chemistries are positioned to gain a competitive advantage, as brand owners seek to future-proof packaging against evolving regulatory risks. This transition is accelerating innovation in next-generation food-safe coatings and reshaping competitive dynamics within the industry.

Market Opportunity: EU PPWR Regulation Driving Demand for Recyclability-Compatible and High-Purity Coating Systems

The introduction of the European Union’s Packaging and Packaging Waste Regulation (EU) 2025/40 is creating a new dimension of demand in the metal packaging coatings market, centered on recyclability performance and material purity. The regulation establishes mandatory recyclability grading for packaging starting in August 2026, with classifications ranging from A to E based on compatibility with recycling processes.

Coatings are emerging as a critical factor influencing recyclability outcomes. Systems that interfere with metal recovery, such as those generating excessive dross or slag during remelting, can negatively impact recyclability ratings, potentially downgrading packaging to lower categories. This has direct financial implications, as lower recyclability grades are associated with higher Extended Producer Responsibility fees for brand owners.

As a result, there is increasing demand for coating technologies that minimize contamination during recycling. This includes “wash-off” external coatings that can be easily removed during pre-treatment processes, as well as high-purity internal linings that do not introduce harmful substances into the recycled metal stream. The regulation also strengthens restrictions on substances of concern, further emphasizing the need for clean, compliant chemistries.

These requirements are driving innovation in coating formulations that balance performance with recyclability, creating opportunities for suppliers capable of delivering environmentally compatible solutions. As circular economy principles become embedded in packaging regulations, recyclability-driven coating design is expected to become a core competitive differentiator in the metal packaging industry.

Metal Packaging Coatings Market Share and Segmentation Insights

Rigid Metal Packaging Holds 72.3% Share Driven by Can Coating Requirements and BPA-Free Transition

The metal packaging coatings market by packaging type is led by rigid packaging, accounting for 72.3% of the global market share in 2025, primarily due to the widespread use of metal cans in food, beverage, aerosol, and paint applications. These rigid formats require both internal and external protective coatings to prevent metal corrosion, product contamination, and surface abrasion, making coatings essential to packaging performance. The segment’s dominance is further reinforced by the ongoing transition from BPA-based epoxy coatings to BPA-free alternatives, such as polyester, acrylic, and polyolefin coatings, in response to regulatory and consumer safety concerns. This reformulation trend has significantly increased innovation and demand for advanced coatings, even as overall can volumes stabilize. As a result, rigid packaging continues to be the backbone of the global metal packaging coatings market, supported by sustainability, safety compliance, and long-term durability requirements.

Corrosion and Chemical Resistance Captures 48.4% Share Due to Food Safety and Shelf-Life Requirements

In the metal packaging coatings market by functional performance, corrosion and chemical resistance dominate with a 48.4% market share in 2025, reflecting their critical role in ensuring food safety and packaging integrity. Internal can coatings must withstand exposure to acidic foods (tomatoes, fruits), salty contents (soups, vegetables), and sulfur-containing products (meat, seafood) without degrading or allowing metal leaching. This makes high-performance barrier coatings a non-negotiable requirement for manufacturers. Additionally, metal packaging is designed for long shelf life—typically 12 to 36 months, necessitating coatings that maintain adhesion, flexibility, and chemical stability over extended periods. Continuous advancements in anti-corrosion coatings, food-grade barrier technologies, and adhesion performance testing are driving innovation in this segment. Consequently, corrosion and chemical resistance remain the most critical functional drivers in the global metal packaging coatings industry.

Competitive Landscape in the Metal Packaging Coatings Market

AkzoNobel and Axalta create a global powerhouse in BPA-NI metal packaging coatings

AkzoNobel and Axalta have formed a dominant entity in the metal packaging coatings market through their 2026 all-stock merger, creating a company valued at $25 billion with combined revenues of $17 billion. The integration is expected to generate $600 million in synergies within three years, strengthening leadership in beverage and food can coatings. Their Accolade® series offers BPA-NI compliant internal and external coatings designed for seamless use in high-speed coil and sheet-fed lines. With over 40 specialized packaging labs and 4,000 R&D personnel globally, the company maintains industry-leading regulatory readiness, ensuring coatings withstand retort and pasteurization processes while meeting stringent EU and FDA standards.

PPG advances energy-efficient and specialty packaging coatings with radiation curing technologies

PPG Industries is a key innovator in metal packaging coatings, focusing on energy efficiency and specialty applications. In April 2026, the company launched the first aluminum coil-applied PVC-NI coating in the U.S., specifically designed for pet food cans to replace traditional vinyl-based systems. PPG is also investing in radiation-curable (UV/EB) coatings technology in France, enabling near-instant curing and increasing production line speeds by up to 25% while reducing energy consumption. Its iPura™ product line dominates the aerosol and aluminum tube segment, offering BPA-, phthalate-, and styrene-free coatings for clean beauty and pharmaceutical applications. Strong financial performance in 2026 is driven by growth in industrial and packaging segments.

Sherwin-Williams scales high-volume metal packaging coatings with rapid production capabilities

The Sherwin-Williams Company is strengthening its position in the metal packaging coatings market through large-scale production expansion and advanced coating technologies. In March 2026, the company increased capacity at its Bowling Green facility by 60%, enabling faster response to rising demand in beverage and food packaging sectors. Its valPure® V70 technology is the world’s first non-BPA epoxy coating for light metal packaging, with over 100 billion cans produced, demonstrating proven barrier performance and flavor neutrality. Sherwin-Williams is also focusing on automation and large-batch production to achieve lead times under five days, providing a critical advantage in a volatile supply chain environment.

Henkel leads sealant and surface treatment innovation for integrated packaging systems

Henkel Adhesive Technologies is a market leader in the chemical-to-coating interface, delivering advanced sealants and surface treatment systems for metal packaging. At METPACK 2026, the company introduced Darex WBC 4020, a water-based sealant designed for global standardization, reducing supply chain complexity. Its Darex COV series eliminates phthalate-based plasticizers, ensuring compliance with REACH and SVHC regulations. Henkel’s Bonderite E-CO system provides real-time process control during can pre-treatment, optimizing water and chemical usage while improving operational efficiency. The company also excels in low-temperature surface treatments, with lubricants functioning at 43°C, significantly lowering energy consumption and supporting sustainable manufacturing practices.

Kansai Paint strengthens APAC leadership with ultra-thin and high-speed packaging coatings

Kansai Paint is a dominant player in the Asia-Pacific metal packaging coatings market, supported by strong manufacturing presence across India and Southeast Asia. The company holds a leading position in powder and coil coatings, with eight production facilities enabling regional supply chain efficiency. Its 2026 amalgamation with Nerofix Private Limited enhances its adhesive and packaging coatings portfolio, strengthening its foothold in South Asia. Kansai’s proprietary viscosity-control technology enables ultra-thin coatings as low as 1 μm, reducing material usage and supporting lightweight packaging trends. With a strategic focus on doubling production capacity by 2030, Kansai is well-positioned to capitalize on growing demand in food and beverage export markets.

Germany Metal Packaging Coatings Market: Circular Chemistry and BPA-Free Innovation Driving European Leadership

Germany stands as the European epicenter for metal packaging coatings, driven by its leadership in sustainable food-contact materials (FCMs), circular economy initiatives, and advanced barrier coating technologies. The market is witnessing strong adoption of hybrid polyester-acrylic coating systems, enabling 100% BPA-NI (Bisphenol A Non-Intent) compliance while maintaining high sterilization resistance for aggressive food products such as acidic fruits and fermented foods. This technological advancement is critical for ensuring food safety without compromising metal recyclability.

The transformation of manufacturing infrastructure, including the conversion of Saarlouis beverage can facilities into high-tech UV-LED curing hubs, reflects Germany’s focus on energy-efficient production. Regulatory frameworks such as the revised German Packaging Act (VerpackG) are encouraging the development of coatings that support monomaterial-like recycling for steel and aluminum packaging. Investments in closed-loop solvent recovery systems are further reducing VOC emissions, while strict compliance with EU Food Contact Material (FCM) regulations ensures full traceability of coating compositions. Germany’s dominance in PVC-free organosol coatings for closures and caps highlights its strong presence in the premium organic food packaging segment.

United States Metal Packaging Coatings Market: BPA-NI Transition and Smart Coating Technologies Driving Growth

The United States is a global leader in BPA-NI metal packaging coatings, driven by stringent FDA regulations and rapid industry-wide adoption of safer chemical alternatives. Updated FDA guidelines on BPA usage have accelerated the transition toward second-generation epoxy alternatives, reshaping coating formulations across the packaging industry.

Technological innovation is a key differentiator, with the commercialization of smart coatings integrated with thermochromic indicators, enabling real-time temperature monitoring in beverage cans. Leading companies such as PPG and Sherwin-Williams are leveraging AI-driven formulation modeling to accelerate product development and improve long-term performance testing. Infrastructure investments in high-speed can coating lines and Near-Infrared (NIR) drying systems are enhancing production efficiency while reducing carbon footprints. The U.S. market also shows strong demand in aerosol packaging, where high-flexibility internal coatings are essential for handling pressure-sensitive contents in personal care products.

China Metal Packaging Coatings Market: High-Volume Manufacturing and Advanced Industrial Packaging Innovation

China dominates the metal packaging coatings market in volume, while rapidly transitioning toward high-performance, technology-driven coating solutions. Regulatory updates from the State Administration for Market Regulation (SAMR) are enforcing stricter migration limits for food-contact coatings, pushing manufacturers toward safer and more advanced formulations.

Technological advancements include the development of graphene-reinforced coatings for industrial drums, offering enhanced chemical resistance for transporting high-purity materials used in EV battery production. The expansion of waterborne coating facilities in the Greater Bay Area is strengthening export capabilities for high-quality packaging solutions. China’s booming aluminum drawn-and-ironed (DI) can market is driving demand for high-clarity external coatings that support advanced digital printing. Additionally, large-scale investments in polyester resin production are improving supply chain resilience, while strict enforcement of dual carbon targets is accelerating the shift toward low-emission technologies such as powder-based coatings.

India Metal Packaging Coatings Market: Food Processing Expansion and Regulatory Compliance Driving Demand

India is emerging as one of the fastest-growing metal packaging coatings markets, fueled by rapid expansion in food processing, beverage production, and organized retail sectors. Government initiatives such as the Production Linked Incentive (PLI) scheme are boosting domestic manufacturing, creating strong demand for compliant and high-performance coating solutions.

Regulatory enforcement by the Food Safety and Standards Authority of India (FSSAI) is making migration-safe coatings mandatory for packaged food products, ensuring consumer safety and quality standards. The transition from plastic to tinplate packaging for edible oils is significantly increasing demand for specialized internal coatings that prevent oxidation and maintain product integrity. Technological advancements such as high-speed side-seam powder coatings are supporting the rapid growth of India’s beverage can industry. Additionally, investments in integrated food parks and R&D collaborations with global coating companies are strengthening the country’s position as a key hub for sustainable and high-performance packaging solutions.

Japan Metal Packaging Coatings Market: Precision Engineering and Ultra-Thin Coating Innovations

Japan’s metal packaging coatings market is defined by its focus on ultra-thin coating technologies, precision engineering, and high-performance packaging solutions. Innovations such as CBR (Compressed Bottom Reform) technology are enabling lightweight aluminum cans supported by ultra-thin internal coatings that prevent micro-cracking during forming processes.

The country is also leading in the development of photocatalytic coatings for industrial containers, providing self-cleaning properties for outdoor storage environments. Japan’s dominance in premium coffee and beverage packaging is supported by advanced coatings that enhance functionality, including smooth opening and resealing features. Investments in digital twin coating lines are enabling real-time monitoring of coating thickness at the micron level, ensuring consistent quality and zero-defect production. Strict adherence to the Chemical Substances Control Law (CSCL) is driving the transition toward eco-friendly coating materials, reinforcing Japan’s leadership in precision coating technologies.

Brazil Metal Packaging Coatings Market: Agri-Export Demand and Sustainable Coating Innovations

Brazil is emerging as a strategic hub for metal packaging coatings, driven by its strong position in agriculture, food exports, and beverage production. The demand for biocide-free antimicrobial coatings is increasing, particularly in meat packaging, where maintaining hygiene and preventing bacterial growth are critical.

Significant investments by global players such as Crown and Ball in manufacturing infrastructure, particularly in the Manaus Free Trade Zone, are strengthening Brazil’s production capabilities. Product innovations such as heat-reflective coatings for metal containers are ensuring stability of agricultural chemicals during transport in tropical climates. Government initiatives, including the BNDES Green Credit program, are encouraging manufacturers to adopt water-based and UV-cured coating technologies. Additionally, the demand for sulfur-resistant coatings in canned protein products highlights Brazil’s focus on maintaining product quality and aesthetic appeal. Alignment with Mercosur packaging standards is further facilitating regional trade and market expansion.

Metal Packaging Coatings Market Report Scope

Metal Packaging Coatings market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2032)

|

$1.4 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Resin Type (Epoxy, Acrylic, Polyester, Polyurethane, Vinyl, Oleoresinous, Phenolic, Polyolefin), By Coating Technology (Water-borne Coatings, Solvent-borne Coatings, Powder Coatings, Radiation-Cured), By Packaging Type (Rigid Packaging, Flexible Packaging), By End-Use Industry (Food and Beverage, Personal Care and Cosmetics, Healthcare and Pharmaceutical, Industrial and Specialty, Household Products), By Substrate Material (Aluminum, Steel), By Functional Performance (Corrosion and Chemical Resistance, Flexibility and Formability, Sulfur Stain Resistance, Aesthetic and Decorative, Heat Resistance)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, BASF SE, ACTEGA, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Axalta Coating Systems Ltd., RPM International Inc., Toyo Ink SC Holdings Co., Ltd., Henkel AG and Co. KGaA, KCC Corporation, Hempel A/S, Beckers Group, Siegwerk Druckfarben AG and Co. KGaA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Packaging Coatings Market Segmentation

By Resin Type

- Epoxy

- Acrylic

- Polyester

- Polyurethane

- Vinyl

- Oleoresinous

- Phenolic

- Polyolefin

By Coating Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Powder Coatings

- Radiation-Cured

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By End-Use Industry

- Food and Beverage

- Personal Care and Cosmetics

- Healthcare and Pharmaceutical

- Industrial and Specialty

- Household Products

By Substrate Material

By Functional Performance

- Corrosion and Chemical Resistance

- Flexibility and Formability

- Sulfur Stain Resistance

- Aesthetic and Decorative

- Heat Resistance

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Metal Packaging Coatings Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- BASF SE

- ACTEGA

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Axalta Coating Systems Ltd.

- RPM International Inc.

- Toyo Ink SC Holdings Co., Ltd.

- Henkel AG & Co. KGaA

- KCC Corporation

- Hempel A/S

- Beckers Group

- Siegwerk Druckfarben AG & Co. KGaA

*- List not Exhaustive