Ampoules Packaging Market Overview: Market Size, Growth, and Key Insights

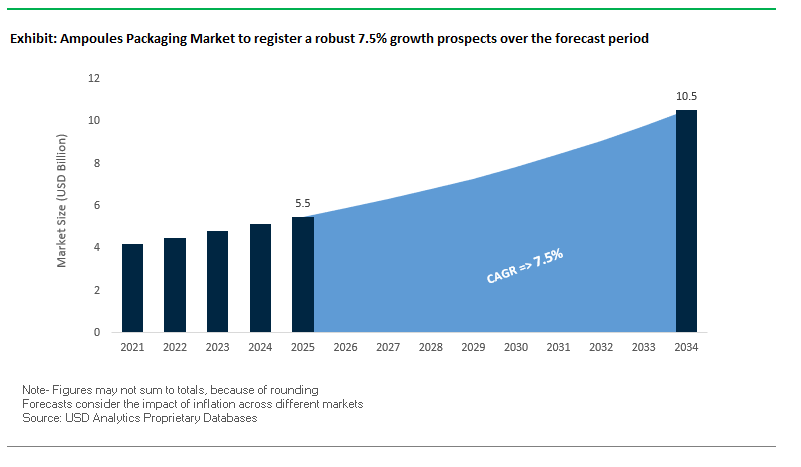

The Global Ampoules Packaging Market is projected to reach $5.5 billion in 2025 and expand to $10.5 billion by 2034, registering a robust CAGR of 7.5%. This strong growth trajectory reflects the rising demand for sterile, single-dose packaging formats in the pharmaceutical and biotechnology industries. Glass ampoules continue to dominate the market, supported by their chemical resistance, transparency, and non-reactivity, which ensure the integrity of injectable drugs and sensitive formulations.

The surge in biologic therapies and injectable drugs is further fueling demand for ampoules, as they provide secure hermetic sealing and reduce contamination risks. While glass maintains a stronghold, plastic ampoules are gaining traction in cosmetics and personal care segments due to their lightweight and shatterproof benefits. Another important driver is automation in production lines, where advanced filling and sealing technologies enhance efficiency, reduce contamination risks, and support the rapid scaling of pharmaceutical manufacturing.

Key Insights for Industry Professionals

- Glass Dominance: Glass ampoules hold the largest revenue share due to safety, integrity, and chemical resistance.

- Biologics & Injectables Drive Demand: Rising biologic therapies make ampoules critical for sterility and contamination prevention.

- Plastic Growth: Lightweight, shatterproof plastic ampoules see growing adoption in cosmetics and non-critical healthcare packaging.

- Automation Integration: Automated filling and sealing processes improve throughput, sterility, and efficiency.

Market Analysis: Recent Industry Developments

The ampoules packaging industry has seen significant developments shaped by acquisitions, joint ventures, and product innovations. In August 2025, SGD Pharma agreed to acquire Alphial S.r.l. in Italy, expanding its tubular vials and ampoules portfolio and strengthening its European presence. Earlier in May 2025, Corning partnered with SGD Pharma to launch a new glass tubing facility in India, boosting the region’s pharmaceutical packaging infrastructure.

Innovation in design remains central. Corning Incorporated introduced an advanced glass ampoule design in November 2024 with faster filling speed and compatibility for automated lines. Similarly, Aptar Pharma unveiled a tamper-evident closure for plastic ampoules in October 2024, reinforcing product safety. Sustainability is also a growing focus: Gerresheimer launched a reduced-energy glass ampoule production process in September 2024, and SCHOTT Pharma debuted pre-fillable biopharma ampoules in August 2024 with improved clarity and breakage resistance.

Strategic expansion has also been strong. Constantia Flexibles acquired a majority stake in Aluflexpack AG in February 2024, strengthening its European pharmaceutical packaging position. Meanwhile, SCHOTT AG invested BRL 50 million in its Brazilian pharmaceutical tubing facility in April 2023, expanding its footprint in Latin America. These moves underscore the industry’s focus on capacity expansion, sustainable manufacturing, and advanced packaging technologies to meet global pharmaceutical demand.

Key Trends and Emerging Opportunities Transforming the Ampoules Packaging Market

Strategic Adoption of Polymer Ampoules for Enhanced Safety and Drug Compatibility

The ampoules packaging market is witnessing a decisive shift from traditional glass to polymer materials, particularly cyclic olefin copolymer (COC) and cyclic olefin polymer (COP), driven by the need to minimize drug-container interactions and enhance patient safety. Polymer ampoules offer high chemical inertness, with minimal extractables and leachables, ensuring stability and efficacy for sensitive biologics, vaccines, ophthalmologic drugs, and mRNA therapies. Unlike glass, polymer ampoules eliminate delamination risks, preventing glass flakes from contaminating drug products a critical safety enhancement for pharmaceutical companies. Additionally, the superior mechanical integrity of polymer ampoules makes them virtually unbreakable, reducing transit breakage, protecting high-value cold-chain medications, and minimizing injury risks for healthcare professionals and patients. This trend positions polymer ampoules as a safer, more reliable solution in modern pharmaceutical packaging.

Integration of Serialization and Track-and-Trace Technologies at the Unit Level

To combat counterfeiting and comply with stringent global regulations, the industry is increasingly implementing direct-to-container serialization, including 2D Data Matrix codes, and anti-tamper features on ampoules. Regulations such as the U.S. Drug Supply Chain Security Act (DSCSA) and the EU Falsified Medicines Directive (FMD) mandate unit-level traceability for prescription drugs, necessitating advanced laser marking and vision inspection systems on production lines. The use of unique digital identifiers on each ampoule ensures authenticity verification, protecting both patient health and brand integrity. Furthermore, automated vision inspection systems enhance operational efficiency by accurately documenting expiration dates, lot codes, and GTINs, seamlessly integrating serialization into secondary and tertiary packaging processes while maintaining compliance and high production throughput.

Development of Integrated, Ready-to-Use (RTU) Polymer Ampoule Systems for Emergency and Field Medicine

There is a growing opportunity to develop pre-filled, ready-to-use polymer ampoules for emergency medications, such as naloxone, epinephrine, and antidotes, incorporating an integrated needle and plunger for intuitive administration. These all-in-one systems eliminate the need for separate syringes and vials, significantly reducing administration time and complexity in critical situations. Such designs enable first responders and non-medical personnel to deliver life-saving drugs safely and efficiently in field conditions, schools, and public spaces, expanding access to emergency treatments and enhancing patient outcomes.

Advancement of Sustainable and Recyclable Polymer Chemistry for Ampoules

Sustainability presents a key opportunity in polymer ampoules packaging. New bio-based monomers are enabling the creation of high-performance COC and COP polymers with reduced carbon footprints, offering functionality equivalent to petroleum-based counterparts. Additionally, chemical recycling pathways, including depolymerization and pyrolysis, are being explored to recover high-purity raw materials from end-of-life ampoules. These innovations pave the way for closed-loop systems, where polymer ampoules can be efficiently recycled into new products, aligning pharmaceutical packaging with circular economy principles and supporting corporate ESG goals.

Competitive Landscape: Leading Companies in Global Ampoules Packaging

The ampoules packaging market is highly competitive, with established global players leveraging R&D, acquisitions, and automation to maintain leadership. Companies are focusing on sustainable manufacturing, expansion into emerging markets, and innovations tailored for injectable therapies and biologics.

Gerresheimer AG: Pioneering Sustainable Glass Ampoule Production

Gerresheimer is a leading provider of pharmaceutical glass and plastic packaging, with a portfolio spanning ampoules, vials, and syringes. In September 2024, it introduced a sustainable glass production process, cutting energy use and carbon emissions. Its strategic focus is to provide innovative, eco-friendly packaging tailored for pharma and biotech industries, supported by deep expertise in customized solutions and a strong global presence.

SCHOTT Pharma: Innovating with Pre-Fillable Biopharma Ampoules

SCHOTT Pharma specializes in high-quality pharmaceutical glass tubing and packaging. In August 2024, it launched pre-fillable biopharma ampoules with improved clarity and reduced breakage, supported by i-Q technology for defect-free inspection. With a long history of glass innovation, SCHOTT focuses on delivering reliable, high-performance packaging solutions and continues to expand its R&D-driven global footprint.

Stevanato Group S.p.A.: Expanding Global Footprint with Ez-fill Platform

Stevanato Group offers drug containment and delivery solutions, with ampoules and vials forming a core portfolio. Its SG Ez-fill platform, a pre-sterilized, ready-to-use solution, reduces contamination risks and simplifies pharma filling operations. The company is actively investing in new facilities to expand capacity and enhance global service reach, strengthening its role as an integrated partner across the drug lifecycle.

SGD Pharma: Strengthening Market Presence with European Acquisitions

SGD Pharma is a major player in pharmaceutical glass packaging, offering bottles, vials, and ampoules. In August 2025, it acquired Alphial S.r.l., reinforcing its position in Europe, and partnered with Corning in May 2025 to build a new tubing plant in India. With a strong focus on quality, reliability, and sustainability, SGD Pharma is expanding both its manufacturing capacity and its global supply capabilities.

Ampoules Packaging Market Share Insights

Straight-Stem Formats Dominate Market Share by Ampoule Type

Straight-stem ampoules command the largest share at 45%, underscoring their role as the cost-effective backbone of the ampoules packaging industry. Their dominance is rooted in manufacturing simplicity, scalability, and universal suitability for liquid formulations, making them the preferred choice for injectables, veterinary drugs, and chemical reagents. While more advanced formats are gaining traction, the enduring relevance of straight-stem ampoules reflects the continued demand for proven hermetic sealing technologies across global pharmaceutical supply chains. Easy-open variants, including One Point Cut (OPC) and Color Break Ring (CBR), are rapidly expanding, driven by regulatory emphasis on patient safety and the reduction of glass particle contamination. Closed (Form D) and funnel-type ampoules remain niche, serving specialized pharmaceutical or industrial needs, but their role highlights the adaptability of ampoule packaging across varying technical requirements.

Pharmaceuticals Retain Overwhelming Market Share by End-Use Industry in Ampoules Packaging

The pharmaceutical sector accounts for approximately 85% of total ampoules demand, making it the undisputed driver of this industry. Ampoules are uniquely suited for high-value parenteral drugs, vaccines, and biologics that require inert, tamper-evident, and hermetically sealed packaging. With the surge in biologics, oncology treatments, and injectable therapies, the reliance on ampoules particularly advanced easy-open designs is only increasing. Beyond pharma, chemical and industrial applications represent a smaller but important niche, where ampoules are indispensable for single-use reagents and high-purity materials requiring absolute barrier protection. Personal care and cosmetics, though the smallest segment, demonstrate the growing premiumization of ampoules packaging, leveraging their single-dose precision and luxury image to differentiate skincare and cosmetic formulations in competitive markets.

United States: FDA Regulations and Innovation in Sterile Ampoules Packaging

The U.S. ampoules packaging market is heavily influenced by stringent regulations from the U.S. Food and Drug Administration (FDA), which mandate tamper-proof and sterile packaging. These evolving regulations are driving innovation in materials, sealing technologies, and automated production processes. Technological advancements, including the shift toward pre-filled ampoules and syringes, enhance patient safety, convenience, and dosing accuracy.

Corporate initiatives reflect the demand for high-quality, reliable solutions, with companies like West Pharmaceutical Services, Inc. leading innovations in injectable drug administration systems. The rising prevalence of chronic diseases, along with the rapid development of biologics and vaccines, is increasing demand for sterile ampoules. Key applications are concentrated in the pharmaceutical and healthcare sectors, where superior chemical resistance, sterility, and product integrity are critical. Significant investments are being made in infrastructure to automate filling and sealing technologies, aiming to increase production speed and precision while maintaining a sterile environment.

Germany: Precision Engineering and Regulatory Compliance Boost Ampoules Packaging

Germany’s ampoules packaging market operates under a stringent regulatory framework, including the EU Falsified Medicines Directive, which mandates serialization to combat counterfeiting. This has driven the adoption of automated labeling and vision inspection systems to ensure traceability. Germany’s global leadership in precision engineering is reflected in high-speed, high-precision filling and sealing machinery, enabling manufacturers to maintain quality standards while meeting growing demand.

Technological innovation is prominent, with Gerresheimer AG and Schott AG developing new glass formulations that improve chemical resistance and strength. Government mandates require tamper-proof and readable labeling, making automated labeling systems with data matrix printing essential. The market is strongly focused on pharmaceutical applications, particularly where chemical inertness and barrier properties are critical for drug stability. German companies are also investing heavily in sustainable ampoules production to align with EU environmental goals, combining quality, safety, and eco-friendly practices.

China: “Made in China 2025” and Dual Carbon Goals Drive Eco-Friendly Ampoules Packaging

China’s ampoules packaging industry is being reshaped by the “Made in China 2025” plan and dual carbon goals, which emphasize eco-friendly and reusable materials. Automation, AI, and the integration of “5G plus industrial internet” are improving production efficiency and flexible capacity for pharmaceutical packaging. The country’s growing biologics and vaccine sectors are fueling demand for secure, sterile, and high-quality ampoules.

Regulatory reforms, including stricter drug safety and efficacy requirements from the China Food and Drug Administration (CFDA), are shaping production standards. Investments in manufacturing infrastructure are increasing to meet the demand for sterile packaging. The expansion of e-commerce and medical logistics platforms is also driving the need for packaging that ensures product integrity during transport. Sustainable alternatives and intelligent packaging systems are gaining traction as Chinese manufacturers focus on material efficiency and compliance with environmental regulations.

India: Make in India Initiative and Automation Enhance Ampoules Production

India’s ampoules packaging market benefits from government initiatives such as “Make in India” and “Zero Effect Zero Defect,” which support quality domestic production through regulatory guidance and industrial infrastructure investments. The Central Drugs Standard Control Organization (CDSCO) enforces strict standards for sterility, safety, and durability, ensuring compliance with domestic and international pharmaceutical regulations.

Technological advancements, including automated on-demand ampoules production systems, have enhanced manufacturing speed, precision, and reliability. Rising chronic diseases like diabetes and cancer are driving demand for injectable treatments across hospitals and clinics. Indian manufacturers are increasingly producing export-oriented ampoules to comply with global standards from the FDA and European Medicines Agency, highlighting a focus on quality, safety, and scalability in the sector.

Brazil: ANVISA Regulations and Strategic Investments Fuel Pharmaceutical Ampoules Market

The Brazilian ampoules packaging market is regulated by the National Health Surveillance Agency (ANVISA), which enforces stringent quality and safety standards for pharmaceutical packaging. These regulations are a key driver for the adoption of advanced glass ampoules and reliable primary packaging solutions. Technological advancements, including robotics and AI, are enhancing production efficiency, quality control, and defect detection.

Sustainability is gaining prominence, supported by laws banning the import of plastic waste, which encourages innovative and eco-friendly packaging solutions. Strategic investments are being made as Brazil emerges as a significant player in the global pharmaceutical market. Key applications are centered on the expanding healthcare sector, where demand for vials, ampoules, and containers is rising. Global companies like Schott AG and Gerresheimer AG maintain a strong presence, providing high-quality glass ampoules to meet growing domestic and export demand.

Japan: Smart Packaging and Precision Manufacturing Redefine Ampoules Industry

Japan’s ampoules packaging market leverages advanced precision manufacturing and AI technologies to enhance design speed, production accuracy, and quality. Regulatory updates by the Ministry of Health, Labour and Welfare (MHLW) in May 2025 revised food-contact and pharmaceutical packaging requirements, ensuring higher standards for safety and compliance.

The market is embracing smart packaging, integrating sensors and digital monitoring tools to improve patient adherence and treatment efficacy. Innovations focus on high dimensional stability, resistance to deformation, and pre-filled formats suitable for an aging population and single-person households. Investment in smart packaging reflects strong corporate commitment to innovation, with a majority of pharmaceutical companies planning to expand smart packaging adoption over the next five years, combining functionality, safety, and convenience.

Ampoules Packaging Market Report Scope

Ampoules Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.5 Billion

|

|

Market Size (2034)

|

$10.5 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Material Type (Glass, Plastic), By Ampoule Type (Straight-stem, Funnel-type, Closed, Easy-Open), By End-Use Industry (Pharmaceutical, Personal Care & Cosmetics, Chemical & Industrial), By Application (Vaccines, Biologics, Injectable Drugs, Serums & Essences), By Capacity (≤2 mL, 3–5 mL, 6–10 mL, 10 mL)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Gerresheimer AG, Schott AG, Stevanato Group, SGD Pharma, Nipro Corporation, Amcor plc, West Pharmaceutical Services, Inc., Bormioli Pharma S.p.a., Corning Incorporated, Ardagh Group, PGP Glass, DWK Life Sciences, Shisecam, Vetropack Holding AG, S.P.I.P.A. s.r.l.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ampoules Packaging Market Segmentation

By Material Type

By Ampoule Type

- Straight-stem

- Funnel-type

- Closed

- Easy-Open

By End-Use Industry

- Pharmaceutical

- Personal Care & Cosmetics

- Chemical & Industrial

By Application

- Vaccines

- Biologics

- Injectable Drugs

- Serums & Essences

By Capacity

- ≤2 mL

- 3–5 mL

- 6–10 mL

- 10 mL

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Ampoules Packaging Market

- Gerresheimer AG

- Schott AG

- Stevanato Group

- SGD Pharma

- Nipro Corporation

- Amcor plc

- West Pharmaceutical Services, Inc.

- Bormioli Pharma S.p.a.

- Corning Incorporated

- Ardagh Group

- PGP Glass

- DWK Life Sciences

- Shisecam

- Vetropack Holding AG

- S.P.I.P.A. s.r.l.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and integrated research methodology to deliver actionable insights on the global Ampoules Packaging Market. Our approach combines extensive primary research, including interviews with pharmaceutical packaging engineers, quality control specialists, supply chain managers, and R&D professionals, with rigorous secondary research sourced from company reports, regulatory filings, trade journals, and industry publications. The analysis covers key dimensions such as material type (glass, plastic), ampoule formats (straight-stem, funnel-type, closed, easy-open), end-use industries (pharmaceutical, personal care & cosmetics, chemical & industrial), and applications (vaccines, biologics, injectable drugs, serums & essences). USDAnalytics also evaluates emerging trends such as polymer ampoules for enhanced drug safety, serialization and track-and-trace technologies, ready-to-use pre-filled systems for emergency medicine, and sustainable polymer chemistry innovations. Regional assessments encompass major markets including the U.S., Germany, China, India, Brazil, and Japan, integrating regulatory frameworks, automation adoption, and sustainability initiatives. Competitive benchmarking incorporates leading players like Gerresheimer AG, SCHOTT Pharma, Stevanato Group, and SGD Pharma, highlighting their strategies in innovation, capacity expansion, and sustainable manufacturing. This holistic methodology ensures a deep, professional-level understanding of the ampoules packaging ecosystem, supporting strategic decisions, operational optimization, and regulatory compliance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.