Pharmaceutical Packaging Market Overview: Biologics, RTU Formats, and Connected Packs Accelerate Growth

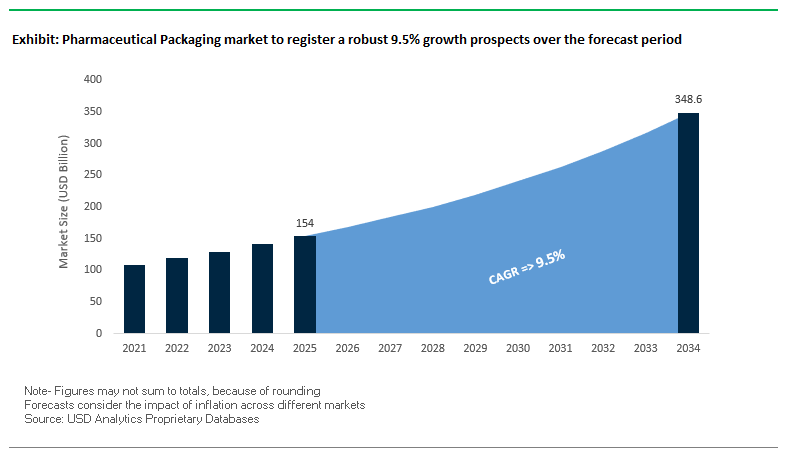

The global pharmaceutical packaging market is set to expand from USD 154.0 billion in 2025 to USD 348.5 billion by 2034, at a robust CAGR of 9.5%. For industry buyers and technical leaders, packaging has become a strategic lever for patient safety, drug stability, and regulatory compliance, especially as pipelines tilt toward biologics and specialty therapies. Beyond containment, next-gen primary packaging (vials, prefilled syringes, cartridges) and secondary/tertiary systems are being redesigned for cold-chain integrity, child resistance, senior usability, circular materials, and digital traceability. The question is no longer which pack—but which validated, data-rich, and sustainable system de-risks filing, speeds scale-up, and ensures supply resilience.

Key Insights for Industry Stakeholders

- Biologics reshape primary packaging: Sensitive biologics are pushing adoption of high-barrier glass, prefilled syringes, and containment solutions with tight extractables/leachables controls.

- Safety by design: >75% of new controlled-substance Rx launches use child-resistant and senior-friendly formats to mitigate misuse and improve adherence.

- Connected/traceable packs: Over 40% of pharma companies invest in NFC/QR-enabled packs for authentication, adherence support, and supply-chain visibility.

- Ready-to-Use surge: RTU/RTF vials and cartridges (pre-washed/sterilized) are scaling to cut contamination risk and accelerate fill-finish readiness.

Market Analysis: 2024–2025 Moves in M&A, RTU Alliances, and Sustainable Systems

Consolidation and platform plays defined late-2024 through 2025 as suppliers raced to build global capacity, RTU ecosystems, and circular materials. In September 2024, a U.S. initiative from Cabinet Health launched the first national pill-bottle recycling program, signaling policy and consumer pressure to curb pharma packaging waste. November 2024 saw Gerresheimer, SCHOTT Pharma, and Stevanato Group deepen collaboration to normalize RTU vials/cartridges, reducing line changeovers and contamination risk across biologics fill-finish.

Sustainability milestones intensified. January 2025, Aptar Pharma introduced a high-performance nasal spray in recyclable packaging, aligning device performance with circularity. At Pharmapack (February 2025), survey insights spotlighted progress and hurdles on greener materials adoption. March 2025, AptarGroup detailed ESG advances in its 2024 sustainability report, reinforcing a shift to responsible sourcing and packaging circularity. The year’s largest strategic combination arrived in April 2025, when Amcor and Berry Global announced a definitive merger to form a consumer and healthcare packaging leader with complementary films, devices, and healthcare portfolios—poised to influence spec decisions in pharma and med-health adjacencies.

Balance sheet moves and capacity expansions supported growth pipelines. May 2025, Gerresheimer repaid part of the Bormioli Pharma acquisition bridge financing (EUR 200M), increasing flexibility for selective capex and deals. August 2025, SGD Pharma agreed to acquire Alphial to expand tubular glass in Europe, while earlier alliances and capex (e.g., JV with Corning in India) neared readiness—evidence of regional redundancy strategies for critical glass tubing. Across this window, RTU/RTF formats, automation-ready inspection, and digitally enabled packs emerged as differentiators for speed-to-market, compliance, and patient experience.

Transformative Trends and Emerging Opportunities in the Pharmaceutical Packaging Market

Strategic Adoption of Connected Packaging and Serialization for Enhanced Traceability

The pharmaceutical packaging market is entering a new era of digital integration, where packaging is no longer just a protective layer but an intelligent node in the global healthcare supply chain. Major pharmaceutical companies are making multi-million-dollar investments in cloud-based serialization platforms that enable every drug package to carry a unique, traceable identity. In 2024, one leading global manufacturer announced a strategic program to implement connected serialization across its operations, ensuring real-time verification and authentication of medicines worldwide. Beyond compliance, this development strengthens patient safety and addresses the World Health Organization’s alarming statistic that 10% of medical products in low- and middle-income countries are substandard or falsified. Technologies such as Near-Field Communication (NFC) tags and IoT-enabled sensors embedded in packaging are being piloted to monitor cold chain conditions, ensuring biologics and vaccines remain within safe temperature ranges during transit. This integration of traceability and data-driven insights represents a paradigm shift from packaging as a static entity to packaging as a smart, responsive component of pharmaceutical logistics.

Accelerated Investment in Sustainable Material Science and Recyclable Monomaterial Structures

Sustainability is becoming an equally powerful force in reshaping pharmaceutical packaging, as companies align with ambitious carbon reduction and waste elimination targets. Industry leaders such as Novartis have pledged to make 100% of their packaging reusable, recyclable, or compostable by 2030. These commitments are fueling rapid innovation in eco-friendly materials that meet the sector’s demanding regulatory and safety standards. For example, in February 2024, Sanofi Consumer Healthcare joined the Blister Pack Collective to co-develop recyclable, fiber-based blister packs, a radical shift from the traditionally non-recyclable aluminum-plastic laminates. The pharmaceutical industry is also exploring breakthroughs from adjacent markets, such as Amcor’s development of a recyclable retort pouch for wet pet food, which demonstrates that high-barrier, mono-material solutions can withstand sterilization processes. Applying this innovation to pharma opens the door to recyclable pouches for medical devices, antibiotics, and temperature-sensitive drugs. This transition from incremental sustainability to disruptive material science innovation reflects how the pharmaceutical packaging industry is balancing environmental responsibility with uncompromising performance requirements.

Development of Packaging for the Booming GLP-1 and Biologics Drug Classes

The meteoric rise of biologics and GLP-1 receptor agonists is creating a premium market for specialized packaging solutions. With patients increasingly managing chronic conditions such as diabetes and obesity through long-acting injectable drugs, demand is surging for pre-filled syringes and auto-injectors that simplify self-administration. Packaging companies are re-engineering designs to handle larger volumes, higher-viscosity formulations, and precision dosing, while ensuring safety and compliance. Cold chain logistics are also emerging as a critical opportunity. GLP-1 drugs and biologics are highly temperature-sensitive, requiring advanced insulated packaging systems validated for global distribution. Beyond logistics, patient-centricity is shaping design. Auto-injectors with intuitive two-step mechanisms, automated needle retraction, and clear visual cues are being developed to minimize user error and improve adherence. This convergence of medical device packaging, logistics, and user-focused engineering underscores how biologics and GLP-1 therapies are expanding the role of packaging from product protection to an enabler of patient outcomes.

Leveraging Regulatory Push for Patient-Centric and Accessible Design

Regulators are increasingly mandating packaging designs that prioritize patient accessibility, usability, and safety, opening up opportunities for innovation in inclusive pharmaceutical packaging. In the UK, the Human Medicines Regulations 2012 require Braille labeling on all prescription packaging, setting a precedent for patient-first design. Similar mandates across Europe and North America emphasize readability, error prevention, and universal accessibility. Guidance from the UK’s MHRA on the use of Tallman lettering is a prime example of how regulatory frameworks are pushing packaging toward error-proofing to reduce potentially life-threatening mix-ups. In response, companies are rolling out accessible features such as large, high-contrast fonts, ergonomic caps requiring minimal force, and peel-back blister foils that are easier for patients with limited dexterity. These adaptations are not only regulatory necessities but also commercial differentiators in markets where patient trust and adherence are paramount. As the global population ages and self-administration becomes more common, patient-centric packaging solutions represent one of the most strategically important growth opportunities for the industry.

Competitive Landscape: High-Value Containment, RTU Platforms, and Device Innovation

The pharmaceutical packaging competitive field is anchored by global glass leaders, device specialists, and flexible/rigid converters scaling RTU, high-barrier, and sustainable solutions. Vendors differentiate on regulatory support, analytical testing, material science, and validated supply chains across North America, Europe, and Asia.

Amcor plc advances sustainable healthcare and flexible platforms

Amcor delivers a broad pharmaceutical portfolio spanning high-barrier flexible films, rigid containers, cartons, and patient-centric blisters. In April 2025, it entered a definitive merger agreement with Berry Global, creating a packaging powerhouse to serve consumer and healthcare end-markets at scale. Strategically, Amcor pushes AmPrima™ recycle-ready solutions and has an MoU with NOVA Chemicals to expand recycled PE usage. Its Integrated Solutions Program pairs packaging with analytical testing and regulatory expertise, while Costa Rica network expansion (2024) bolsters Americas supply.

Gerresheimer AG scales high-value solutions for biologics

Gerresheimer leads in glass and polymer primary packaging—vials, ampoules, syringes, cartridges—with strong traction in biologics containment via its Gx Biological Solutions and RTF syringes. In May 2025, it partially repaid bridge financing for Bormioli Pharma, preserving financial headroom for growth. Its November 2024 alliance with SCHOTT Pharma and Stevanato accelerates RTU standardization. Gerresheimer is also investing in proprietary devices and contract manufacturing, expanding capacities across China, India, and Brazil.

AptarGroup, Inc. elevates patient-centric drug delivery and circularity

Aptar is synonymous with dispensing and delivery systems—nasal, ophthalmic, injectable, oral—engineered for adherence and usability. Its strategy centers on patient-centric design (e.g., preservative-free multi-dose platforms) and smart packaging with digital tracking. In January 2025, Aptar Pharma launched a new recyclable nasal spray device, coupling device performance with recyclability. Backed by a global R&D and prototyping/testing network, Aptar helps customers navigate human factors, validation, and regulatory pathways.

West Pharmaceutical Services, Inc. secures injectable integrity and speed-to-market

West specializes in elastomer and polymer components for injectables—stoppers, seals, plungers, and syringe components—critical for chemical compatibility and container closure integrity. Its Integrated Solutions de-risk programs from component selection to analytical testing. The AccelTRA® platform supplies ready-to-file components for generics, shortening timelines. West’s portfolio is central to prefilled syringes, vials, and cartridges in vaccines and complex biologics.

SCHOTT AG raises the bar in pharmaceutical glass performance

SCHOTT manufactures FIOLAX® pharmaceutical glass tubing and finished vials/ampoules/cartridges with superior hydrolytic resistance for sensitive drugs. The EVERIC® vial family targets delamination control and can include hydrophobic coatings to protect formulations. adaptiQ® RTU platforms optimize fill-finish efficiency and sterility assurance, while perfeXion® 100% optical inspection ensures tight dimensional and cosmetic specs—vital for automated lines and CCI. SCHOTT’s focus is quality-by-design from tubing to finished container.

SGD Pharma expands tubular capacity and global resilience

SGD Pharma supplies molded and tubular glass vials for injectable, oral, and topical meds, with Sterinity delivering depyrogenated sterile empty vials. In August 2025, it agreed to acquire Alphial, boosting tubular capacity in Europe to support rising biologics demand. Its 2023 JV with Corning in India—now nearing operational readiness—adds regional redundancy for critical glass tubing. Strategically, SGD focuses on patient safety, quality, and resilient supply chains across global pharma hubs.

Pharmaceutical Packaging market Share Insights

Market Share by Product Type in Pharmaceutical Packaging

Primary packaging dominates the pharmaceutical packaging market with a 52% share in 2025, reflecting its critical role in ensuring drug stability, safety, and efficacy. This segment covers blister packs, vials, bottles, and prefilled syringes, all of which must comply with strict regulations on sterility and barrier performance. Regulatory frameworks in regions such as the US FDA, EMA, and WHO emphasize material compatibility to prevent leachables and extractables, driving continuous investment in high-quality glass, plastics, and aluminum laminates. The rise of biologics and sterile injectables has further increased the value of this segment, as prefilled syringes and auto-injectors require complex engineering to maintain precision and stability. Secondary packaging holds a 33% share, driven by its central role in compliance and communication. Beyond protection, secondary packaging (cartons, labels, inserts) is increasingly embedded with serialization, tamper-evident seals, QR codes, and RFID tags to meet global anti-counterfeiting mandates such as the EU Falsified Medicines Directive and the US Drug Supply Chain Security Act. These requirements have elevated secondary packaging from a branding tool to a critical safety component. Meanwhile, tertiary packaging accounts for 15%, reflecting its indispensable function in logistics and supply chain resilience. Shipping boxes, pallets, and insulated crates are becoming smarter with IoT-enabled sensors for temperature and humidity tracking—particularly vital for biologics, vaccines, and other cold-chain dependent drugs. While tertiary packaging’s value is smaller relative to primary and secondary, its importance has surged with the globalization of pharmaceutical distribution and the rise of advanced therapies requiring stringent handling.

Market Share by Drug Delivery Mode in Pharmaceutical Packaging

Oral drug delivery remains the largest segment with a 45% share in 2025, underscoring the dominance of tablets and capsules in global medicine consumption. High patient compliance, cost-effective production, and streamlined distribution make oral drugs the backbone of pharmaceutical demand. Packaging formats like blister packs and HDPE bottles are standardized, scalable, and easy to dispense, aligning perfectly with mass-market small-molecule drugs. However, the parenteral and injectable segment—holding 28% of the market—is the fastest-growing by value. The surge of biologics, biosimilars, vaccines, and oncology therapies has accelerated demand for prefilled syringes, auto-injectors, and sterile vials, which require advanced manufacturing precision and stringent quality assurance. This segment also benefits from rising adoption of self-administration devices, particularly in chronic disease management. Topical drug delivery packaging continues to hold a steady share, serving dermatology, pain management, and hormone therapy markets. Innovation here centers on precise dosage and patient convenience, with pump dispensers, unit-dose tubes, and transdermal patches gaining traction. Inhalation, nasal, and ocular drug delivery packaging, though smaller in volume, represents highly specialized, high-value niches. Devices like pMDIs, DPIs, nasal sprays, and sterile eyedroppers integrate packaging with drug delivery, making them complex and cost-intensive. Their growth is tied to expanding respiratory, allergy, and ophthalmology markets. Collectively, these dynamics underscore how packaging is not merely a protective layer but an integral part of the drug delivery ecosystem, with each mode shaping demand for specialized materials, engineering, and compliance-driven innovation.

United States: Smart Pharmaceutical Packaging and Sustainability Leading the Market

The United States pharmaceutical packaging market is advancing rapidly with the adoption of smart and connected packaging solutions, including RFID tags, QR-enabled sensors, and real-time temperature monitoring systems. These innovations are particularly vital for cold chain logistics of biologics, specialty drugs, and vaccines, ensuring safety and compliance throughout the distribution process. Another defining trend is the shift towards sustainable materials, exemplified by Bayer’s introduction of PET blister packs for Aleve, in partnership with Liveo Research, which reduces carbon footprint by 38% and eliminates PVC. This focus on eco-friendly solutions is resonating strongly with regulatory goals and consumer preferences.

Additionally, compliance with the Drug Supply Chain Security Act (DSCSA) is driving robust investments in serialization, holographic labels, and tamper-evident packaging, making the U.S. a hub for anti-counterfeiting technologies. The rise of personalized medicine and home healthcare is fueling demand for patient-centric formats like pre-filled syringes and customized blister packs, while AI-driven automation is transforming production lines with greater accuracy, scalability, and efficiency. Together, these trends solidify the U.S. as a global leader in pharmaceutical packaging innovation.

China: Regulatory Reforms and Rapid Expansion of Packaging Manufacturing

China’s pharmaceutical packaging industry is being reshaped by stringent regulatory reforms led by the National Medical Products Administration (NMPA). Revised GMP standards and inclusion of 46 new packaging material requirements in the upcoming Chinese Pharmacopoeia 2025 Edition highlight the government’s commitment to drug quality and safety. This is pushing manufacturers to adopt advanced technologies and align with global best practices in materials and traceability.

China is also undergoing massive manufacturing expansion to meet surging demand for generics, biologics, and vaccines. Investments in modern packaging plants reflect the country’s dual strategy of enhancing self-reliance and competing globally. Sustainability is another priority, with regulatory pushes to curb excessive packaging and encourage biodegradable or recyclable materials. Local manufacturers are upgrading processes with smart technologies to improve supply chain transparency, ensuring compliance and competitiveness both domestically and internationally.

Germany and France: Sustainability, Circular Economy, and Patient Safety Driving Growth

Germany and France are at the forefront of the European pharmaceutical packaging market, shaped by the EU pharmaceutical package legislation that emphasizes environmental risk assessments, supply security, and patient access. Both countries benefit from well-established recycling infrastructures, allowing for high-level integration of circular economy principles, particularly in recyclable plastics and paper-based solutions.

In addition, the regulatory environment mandates continuous innovation in child-resistant and tamper-evident designs, ensuring maximum patient safety and consumer trust. Companies in Germany and France are also investing in advanced manufacturing processes, including high-quality borosilicate glass vials and ampoules that are critical for sensitive biologics and injectable therapies. This strong combination of sustainability, functionality, and patient safety positions both markets as key innovation hubs within Europe.

Japan: Smart Packaging Leadership in an Aging Society

Japan’s pharmaceutical packaging sector is highly influenced by its rapidly aging population and prevalence of chronic diseases, creating demand for packaging that is user-friendly, accessible, and tailored to elderly patients. Easy-to-open closures, clear labeling, and ergonomic formats are increasingly prioritized to improve adherence and usability.

At the same time, Japan is a global leader in smart packaging adoption, with NFC-enabled packaging, RFID technology, and blockchain-enabled tracking systems already integrated into multiple pharmaceutical supply chains. These solutions enhance patient compliance while strengthening anti-counterfeiting and supply chain transparency. Coupled with Japan’s strong commitment to sustainable and biodegradable packaging materials, the market is setting global benchmarks in innovation, patient care, and eco-conscious design.

India: Growing Generics Market Driving Packaging Innovation

India, as the world’s largest supplier of generic drugs and vaccines, is experiencing rapid growth in pharmaceutical packaging. The demand is being shaped by the need for high-volume, cost-effective, yet safe and compliant solutions. At the same time, regulatory initiatives like the National Mission on Sustainable Packaging are encouraging domestic manufacturers to explore bio-based plastics, biodegradable films, and eco-friendly alternatives.

With increasing consumer awareness, the country is also witnessing greater adoption of tamper-evident and child-resistant packaging, especially for OTC drugs and exports to regulated markets. Indian pharmaceutical packaging manufacturers are investing heavily in technological upgrades such as automated filling and sealing systems to meet international standards and improve global competitiveness. The dual focus on affordability and innovation ensures India’s pharmaceutical packaging sector remains pivotal in the global supply chain.

Brazil: Catering to Elderly Consumers and Expanding E-Commerce Channels

Brazil’s pharmaceutical packaging market is evolving with a strong emphasis on user-friendly designs for an aging population. Packaging with larger fonts, ergonomic closures, and simplified dosing solutions are being developed to enhance medication adherence among elderly patients.

The rapid expansion of e-commerce in pharmaceuticals is also reshaping packaging needs, with a focus on tamper-evident seals and protective features that preserve product integrity during transit. Sustainability remains a critical priority, with rising adoption of lightweight and eco-friendly materials like recycled PET (rPET) and bio-based plastics. As pharmaceutical distribution channels diversify, Brazil is increasingly investing in packaging solutions that balance patient safety, durability, and environmental responsibility.

Pharmaceutical Packaging Market Report Scope

Pharmaceutical Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$154 Billion

|

|

Market Size (2034)

|

$348.5 Billion

|

|

Market Growth Rate

|

9.5%

|

|

Segments

|

By Product Type (Primary Packaging, Secondary Packaging, Tertiary Packaging), By Material (Plastics & Polymers, Glass, Paper & Paperboard, Metals, Others), By Drug Delivery Mode (Oral Drug Delivery, Parenteral/Injectable Drug Delivery, Topical Drug Delivery, Inhalation Drug Delivery, Nasal Drug Delivery, Ocular Drug Delivery, Other Drugs Delivery)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Gerresheimer AG, West Pharmaceutical Services, Inc., Berry Global Inc., AptarGroup, Inc., Tekni-Plex, Inc., Schott AG, Huhtamaki Oyj, DWK Life Sciences LLC, Comar, LLC, Bormioli Pharma S.p.A., SGD Pharma, AR Packaging, Constantia Flexibles Group GmbH, EPL Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pharmaceutical Packaging Market Segmentation

By Product Type

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

By Material

- Plastics & Polymers

- Glass

- Paper & Paperboard

- Metals

- Others

By Drug Delivery Mode

- Oral Drug Delivery

- Parenteral/Injectable Drug Delivery

- Topical Drug Delivery

- Inhalation Drug Delivery

- Nasal Drug Delivery

- Ocular Drug Delivery

- Other Drugs Delivery

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Pharmaceutical Packaging Market

- Amcor plc

- Gerresheimer AG

- West Pharmaceutical Services, Inc.

- Berry Global Inc.

- AptarGroup, Inc.

- Tekni-Plex, Inc.

- Schott AG

- Huhtamaki Oyj

- DWK Life Sciences LLC

- Comar, LLC

- Bormioli Pharma S.p.A.

- SGD Pharma

- AR Packaging

- Constantia Flexibles Group GmbH

- EPL Limited

* List Not Exhaustive

Research Coverage

This report investigates the pharmaceutical packaging market with a concentrated emphasis on biologics containment, RTU/RTF platforms, connected packs, and sustainability breakthroughs; it synthesizes industry milestones, commercial pilots, and technology validation so stakeholders can assess speed-to-market, regulatory risk, and patient-centric performance. The analysis reviews cross-sector case studies, serialization and cold-chain integrations, and materials science advances—highlighting practical trade-offs between extractables/leachables control, circularity, and usability—and this report is an essential resource for packaging engineers, regulatory leads, C-suite strategists, and investors seeking evidence-based advice. USDAnalytics applies scenario mapping and investment lenses to identify priority product classes, regional vulnerability points, and vendor strategies that materially affect supply resilience and filing timelines, offering targeted recommendations to align packaging choices with clinical, commercial, and ESG objectives.

Scope Highlights

Segmentation: By Product Type (Primary Packaging, Secondary Packaging, Tertiary Packaging); By Material (Plastics & Polymers, Glass, Paper & Paperboard, Metals, Others); By Drug Delivery Mode (Oral Drug Delivery, Parenteral/Injectable Drug Delivery, Topical Drug Delivery, Inhalation Drug Delivery, Nasal Drug Delivery, Ocular Drug Delivery, Other Delivery Modes).

Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

Timeframe: Historical series covering 2021–2024 with forward forecasts from 2025–2034.

Companies: Includes analysis and executive-level profiles of 15+ strategic players across glass, device, and flexible/rigid converter categories.

Methodology

The study uses a hybrid research design combining primary interviews with packaging R&D and quality leads, procurement managers, contract manufacturers, cold-chain logisticians, and regulatory experts, plus exhaustive secondary research of annual reports, regulatory guidances, patent filings, trade literature, and validated shipment/production data; market sizing was generated through both bottom-up (plant capacity, SKU-level consumption) and top-down (end-market demand) techniques, with cross-validation via company CAPEX announcements and observed plant startups. Technology adoption curves were modelled from pilot deployments and licensing activity; scenario and sensitivity analyses quantify impacts from raw-material price swings, serialization mandates, and accelerated biologics/GLP-1 demand. All findings were stress-tested against supply-disruption scenarios and regulatory permutations to produce investment-grade, actionable forecasts and prioritized strategic recommendations.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.