Recyclable Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Global Recyclable Packaging Market to Reach $389.8 Billion by 2034 Driven by Rising Eco-Conscious Consumer Demand

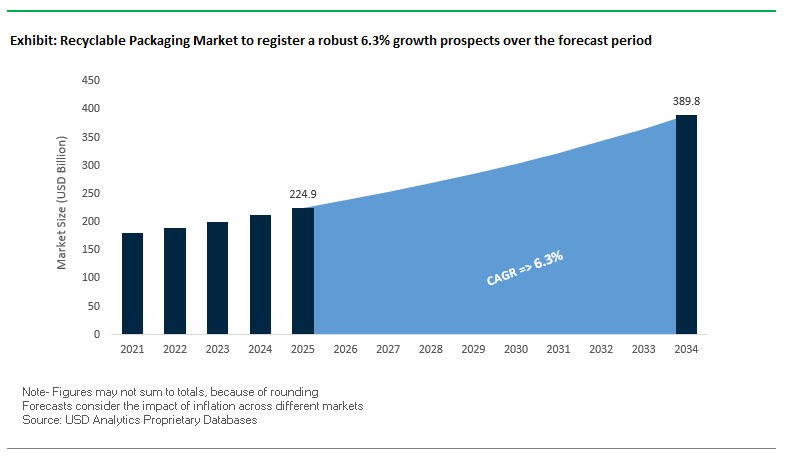

The global recyclable packaging market is projected to grow from $224.9 billion in 2025 to $389.8 billion by 2034, with a CAGR of 6.3%. Increasing consumer awareness of environmental impact and regulatory pressure are driving brands to adopt sustainable packaging solutions. Paper-based materials dominate the sector, supported by widespread recyclability and versatility across industries, from food and beverages to e-commerce. Incorporating post-consumer recycled (PCR) content is increasingly a strategic priority to achieve circular economy goals and reduce reliance on virgin materials.

Key Insights for industry professionals and buyers:

- Consumer Preference for Eco-Friendly Packaging: Nearly 80% of consumers consider a brand's environmental impact before purchasing.

- Paper-Based Packaging as Market Leader: Corrugated and folding cartons remain preferred for recyclability and versatility.

- Post-Consumer Recycled Content Enhances Sustainability: Helps “close the loop” and meet corporate circular economy targets.

- Technological Innovation for Efficiency: Digital printing and automation improve production speed and customization while enhancing recyclability.

- Diverse Applications Across Industries: Recyclable packaging solutions are essential for institutional food service, retail, and logistics sectors.

Market Analysis: Strategic Investments and Innovations Accelerate Growth in Recyclable Packaging Industry

The recyclable packaging market is experiencing significant expansion through technological innovations, strategic investments, and regulatory-driven initiatives. In August 2025, Amcor upgraded its UK recycling facility to enhance plastic waste processing capabilities, signaling the company’s commitment to a circular economy. In the same month, International Paper announced the sale of its Global Cellulose Fibers business for $1.5 billion while investing $250 million to convert a Riverdale mill paper machine for containerboard production, emphasizing a focus on core sustainable packaging. Novolex appointed a new Chief Procurement Officer in August 2025 to optimize its supply chain for sustainable operations.

Recent innovations reflect the industry’s push for practical, eco-conscious solutions. In May 2025, Eco-Products, a Novolex brand, partnered with DNO Produce to launch molded fiber-based cafeteria packaging with plant-based films. In April 2025, Amcor collaborated with Nfinite Nanotechnology to validate nanocoating technology for enhancing oxygen barrier performance in recyclable and compostable packaging. In March 2025, Cascades Inc. introduced produce baskets made from up to 100% recycled fibers, offering growers sustainable alternatives to hard-to-recycle packaging.

Mergers and regulatory developments are also shaping market dynamics. In September 2024, Smurfit Kappa Group and WestRock signed a definitive agreement to create a global sustainable packaging leader, expanding both product diversity and geographic presence. Additionally, innovations like 3M’s Print Wrap Film IJ280 in November 2024 demonstrate cross-industry application of high-performance, sustainable materials.

Recyclable Packaging Market: Key Trends and Future Opportunities

Mandated Shift to Mono-Material Packaging Designs

A central trend shaping the recyclable packaging market is the strong regulatory push towards mono-material packaging formats, particularly within the European Union. The EU Single-Use Plastics Directive (SUPD) establishes clear targets for PET beverage bottles—requiring at least 25% recycled content by 2025 and 30% by 2030. By embedding these requirements into national legislation, EU regulators are pushing brand owners and converters to design packaging that maximizes recyclability while improving the overall quality of recycled material reintroduced into the supply chain. Mono-material packaging is emerging as the most efficient solution to achieve these targets, as it reduces the complexity of recycling streams. Corporate players are aligning rapidly: Unilever, for example, has transitioned to polyethylene (PE)-based mono-material pouches for personal care products, while Nestlé’s 2019 “Negative List” of materials flagged PVDC coatings as incompatible with circular economy goals. The combination of regulation, brand commitments, and consumer expectations is accelerating the transition to mono-material packaging in categories ranging from food and beverage to personal care and household products.

Strategic Investment in Advanced Recycling Infrastructure for Flexible Plastics

Another defining trend in the recyclable packaging market is the rise of consortium-driven investments in advanced recycling technologies, particularly for flexible plastics. Historically, flexibles have posed significant recycling challenges due to their lightweight, multilayer structures. In response, leading consumer goods companies and chemical producers are partnering under umbrella initiatives such as the Alliance to End Plastic Waste, which has pledged over $1 billion toward infrastructure and technology development. These investments are particularly focused on scaling chemical recycling methods capable of converting mixed or hard-to-recycle plastics into high-quality feedstocks. A critical enabler of these efforts is certification under systems like ISCC PLUS, which ensures traceability of recycled and bio-based materials through mass balance accounting. By enabling food-contact approval of chemically recycled content, certifications are unlocking new opportunities for brands to meet regulatory and voluntary recycled content commitments in sensitive applications such as food and beverage packaging, where quality and safety are paramount.

Digital Watermarking for Hyper-Accurate Sorting and High-Quality Recyclate

One of the most groundbreaking opportunities in the recyclable packaging market is the industrial-scale deployment of digital watermarking. The HolyGrail 2.0 Initiative, led by AIM European Brands Association, has validated the technical and commercial feasibility of this approach. In trials conducted at a German materials recovery facility, announced in April 2025, digitally watermarked rigid plastic packaging achieved detection accuracy rates between 87.9% and 93.8%. This level of precision enables SKU-level sorting, distinguishing between food-grade and non-food-grade materials with unprecedented accuracy. For recyclers, this technology represents a step change, as it unlocks the ability to produce high-quality recyclate streams suitable for stringent food-contact applications. By creating new, hyper-accurate sorting streams, digital watermarking helps bridge one of the most persistent gaps in the circular economy scaling food-grade recycled plastics. Furthermore, the technology supports compliance with the EU Packaging and Packaging Waste Regulation (PPWR), which demands greater quality and traceability in recycled packaging materials.

Development of High-Barrier, Recyclable Paper-Based Alternatives

Another key opportunity lies in the evolution of paper-based packaging formats engineered with advanced coatings that mimic the performance of plastics. Packaging leaders like Mondi have been at the forefront, unveiling innovations such as the “FunctionalBarrier Paper Ultimate” in September 2025. This solution offers oxygen transmission rate (OTR) and water vapor transmission rate (WVTR) levels comparable to conventional plastic films, making it viable for demanding applications such as instant coffee sachets, frozen foods, and dry mixes. Beyond sustainability, a major advantage of these innovations is operational: they are compatible with existing form-fill-seal (FFS) machinery, enabling brand owners to adopt paper-based solutions without incurring major capital expenditures. This “drop-in” characteristic accelerates industry-wide adoption by minimizing transition costs while meeting regulatory and consumer expectations for plastic reduction. As paper-based solutions expand into high-barrier categories, they present a scalable and recyclable alternative, reinforcing paper’s role in next-generation packaging ecosystems.

Competitive Landscape: Leading Recyclable Packaging Companies Are Prioritizing Circular Economy and Technological Innovation

The competitive landscape of recyclable packaging is defined by companies that integrate sustainable materials, circular economy practices, and technological innovation into their portfolios. Market leaders focus on expanding global footprints, investing in R&D, and enhancing recycling capabilities to meet rising demand for eco-friendly solutions.

International Paper Company: Streamlining Operations to Focus on Sustainable Packaging Leadership

International Paper is a global leader in fiber-based packaging, pulp, and paper products. In August 2025, the company sold its Global Cellulose Fibers business for $1.5 billion and invested $250 million in its Riverdale mill to produce containerboard. Its core strengths lie in forest stewardship, recycling, and water conservation, making it a trusted provider of recyclable and renewable packaging solutions across agriculture and e-commerce sectors.

Smurfit Kappa Group: Creating a Global Sustainable Packaging Leader Through Strategic Merger

Smurfit Kappa specializes in paper-based packaging solutions, including corrugated and folding cartons. The September 2024 merger with WestRock positions the company as a global sustainable packaging leader with extensive geographic coverage. Smurfit Kappa’s multi-million-pound R&D investments optimize fiber performance and recyclability, while its circular business model ensures full control over design, manufacturing, and recycling processes.

Amcor plc: Expanding Recycling Capabilities and Driving Innovation in Sustainable Packaging

Amcor develops a wide range of rigid and flexible recyclable packaging solutions. In August 2025, the company expanded its UK recycling facility to strengthen circular economy initiatives. Amcor’s EcoGuard™ brand highlights recyclable and reusable features, and its April 2025 collaboration with Nfinite Nanotechnology demonstrates its commitment to barrier performance and sustainable innovation.

DS Smith Plc: Championing Closed-Loop Recycling to Reinforce Sustainable Packaging Solutions

DS Smith provides recyclable retail, shelf-ready, and transit packaging. Its circular model collects, recycles, and reintegrates paper and corrugated materials, reducing waste and promoting sustainability. R&D investments focus on fully recyclable translucent packaging alternatives for plastic windows in ready meal packs. Expansion in North America, including new headquarters in Atlanta, strengthens its global footprint.

Novolex: Leveraging Diverse Materials and PCR Content to Support Circular Economy Growth

Novolex manufactures paper, plastic, and sustainable packaging for food, retail, and industrial markets. Its Eco-Products brand won a national award in April 2025 for reusable containers, emphasizing commitment to sustainability. The company offers molded fiber bases, plant-based films, and products with at least 10% post-consumer recycled (PCR) content, supported by two plastic film recycling facilities to ensure a circular approach.

Recyclable Packaging Market Share Insights, 2025-2034

Boxes & Cartons Lead Market Share by Packaging Type in the Recyclable Packaging Industry

Boxes and cartons account for the largest share of the recyclable packaging industry at 35%, supported by their mono-material composition, efficient recycling infrastructure, and consumer preference for fiber-based packaging. Innovation in water-based barrier coatings and functional recyclable alternatives to polyethylene has accelerated their role as the industry’s benchmark for circularity. Bottles and jars follow at 30%, leveraging mature PET and HDPE recycling streams, though the focus is shifting towards mono-material PET constructions that eliminate non-recyclable labels and barriers. Bags and pouches, holding 15%, represent the most active frontier of R&D, as converters race to replace multi-material laminates with recyclable all-PE or all-PP formats. Films and wraps, with 10% share, face the greatest infrastructure challenges, as collection and contamination issues hinder recycling rates despite design advances. Tubes and vials (10%) are transitioning toward recyclable HDPE and aluminum solutions, addressing growing pressure in personal care and pharmaceuticals. This segmentation shows that cartons and bottles anchor volume, while pouches, films, and tubes lead innovation toward true recyclability.

Food & Beverages Dominate Market Share by End-Use in the Recyclable Packaging Industry

The food and beverage sector leads with 40% share of recyclable packaging demand, reflecting both its sheer consumption volume and intense regulatory and consumer pressure to eliminate non-recyclable packaging formats. The key challenge lies in balancing barrier performance with recyclability, as producers seek mono-material and paper-based solutions that maintain shelf life without increasing food waste. Consumer goods represent 25%, where recyclable packaging has become a core brand differentiator, with companies adopting recycled content and refillable systems as part of sustainability strategies. E-commerce, at 15%, is reshaping secondary packaging, shifting from mixed-material mailers to recyclable paper-based formats to meet consumer expectations for waste-free delivery. Personal care and cosmetics contribute 12%, where recyclable packaging supports luxury positioning and eco-conscious branding. Healthcare and pharmaceuticals, with 8%, remain cautious adopters due to strict regulatory validation needs, focusing primarily on recyclable secondary packaging. This breakdown highlights how food and consumer-facing industries drive momentum, while regulatory sensitivity tempers adoption in healthcare.

European Union: PPWR and Circular Economy Regulations Reshaping Packaging Standards

The European Union is at the forefront of transforming the recyclable packaging market with the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. This landmark regulation governs the entire life cycle of packaging and introduces sweeping rules for recyclability and reuse. By January 2030, all packaging must achieve a minimum 70% recyclability (Grade C), while by 2038, stricter thresholds of Grade B (80%) or Grade A (95%) will apply. One of the most impactful changes is the ban on single-use plastic packaging for fresh fruits and vegetables under 1.5 kg, effective 2030, which is expected to accelerate the adoption of fiber-based trays, compostable films, and reusable packaging systems.

The EU is also restricting the use of PFAS in food contact packaging materials from August 2026, requiring companies to shift toward PFAS-free coatings and adhesives. By 2028, a harmonized recycling label will become mandatory, standardizing communication for consumers across all member states. Additionally, new rules targeting “empty space” in e-commerce packaging, limiting it to no more than 50% by 2030, are reshaping design strategies for logistics and retail. These strict measures are compelling producers to invest in eco-innovations, mono-material solutions, and closed-loop systems, positioning the EU as the global benchmark for sustainable recyclable packaging.

United States: EPA Initiatives and Infrastructure Investments Driving Recycling Innovations

In the United States, the recyclable packaging market is being steered by the U.S. Environmental Protection Agency (EPA) and industry collaborations like the U.S. Plastics Pact, which are pushing toward a circular economy for plastics. Innovations focus on improved sorting systems, chemical recycling advancements, and mono-material film development, which simplify recycling and reduce contamination in material recovery facilities. Demand is rising for mono-material polyethylene (PE) and polypropylene (PP) structures, which offer both recyclability and barrier properties for food and consumer packaging.

The federal Infrastructure Investment and Jobs Act is catalyzing growth by funding advanced recycling facilities and local manufacturing upgrades, which enhance material recovery rates across states. Beyond plastics, there is strong momentum for paper-based trays, molded fiber bags, and recyclable cartons, responding to consumer and corporate sustainability goals. Another notable trend is the premiumization of recyclable packaging, where manufacturers focus on high-margin cast films and luxury recyclable wraps for automotive, electronics, and architectural applications. These developments underline the U.S. commitment to merging sustainability with performance and branding in recyclable packaging.

China: Policy-Driven Recycling Systems and Domestic Demand Expansion

China’s recyclable packaging market is being accelerated by multiple government-led initiatives, including the “14th Five-Year Plan”, which emphasizes the establishment of a robust waste recycling system. The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are jointly driving stricter controls on plastic pollution, encouraging the adoption of eco-friendly substrates and recyclable packaging materials.

New national standards for edible agricultural products regulate interspace ratios, packaging layers, and cost limits, ensuring packaging is not excessive or wasteful. These rules directly impact fresh produce and food packaging, prompting a shift toward lightweight recyclable materials. Additionally, China’s Dual Circulation strategy prioritizes domestic consumption, fueling growth in e-commerce packaging and thereby raising demand for recyclable solutions. Government-backed tax incentives for green technologies and remanufacturing industries are further supporting innovation in recyclable mono-material films and bio-based polymers, strengthening China’s position as both a high-demand and high-production hub for recyclable packaging.

India: EPR Regulations and Bioplastic Innovation Strengthening Recyclable Packaging

India’s recyclable packaging market is evolving under the Plastic Waste Management (Amendment) Rules, 2024, which strengthen Extended Producer Responsibility (EPR) obligations for producers, importers, and brand owners. While MSMEs are exempt from EPR, larger suppliers and raw material manufacturers must ensure proper recycling and waste management, effectively driving systemic responsibility across the supply chain. Another key requirement mandates that all recycled plastic packaging must display the percentage of recycled content and comply with the Indian Standard IS 14534:2023, creating transparency and accountability.

Innovation is a critical driver in India, with patents emerging for bioplastics derived from agricultural and dairy waste—including ghee residue-based materials that are biodegradable in water and soil. Meanwhile, rising processed food and packaged dairy consumption is accelerating demand for recyclable films and trays. Collaborative efforts such as the India Plastics Pact, spearheaded by the Confederation of Indian Industry (CII) and WWF India, set a clear pathway toward 100% reusable or recyclable plastic packaging by 2030. Combined with government incentives and private investments, India is positioning itself as a fast-growing recyclable packaging hub, balancing affordability with sustainability innovation.

Japan: Bio-PP Adoption and Paper-Based Barrier Materials Leading Innovation

Japan is demonstrating leadership in next-generation recyclable materials, particularly through the adoption of bio-polypropylene (bio-PP). Supported by government targets to introduce 2 million tons of bio-PP products annually by 2030, companies such as LyondellBasell and Shiseido are integrating bio-based solutions into cosmetics and food packaging. At the same time, paper-based barrier materials are gaining traction—Nippon Paper Industries’ SHIELDPLUS, a high-barrier paper resistant to oxygen and odor transmission, represents a key innovation in sustainable packaging.

The country’s circular economy initiatives emphasize materials that are easily recycled or composted, reinforcing innovation in mono-material structures and chemical-free coatings. Oversight by the Japan Vinyl Industry Association (JVIA) ensures safety and quality in vinyl and plastic-based products, balancing compliance with innovation. With a culture that prioritizes premium aesthetics and eco-conscious consumption, Japan is driving recyclable packaging solutions that are both functional and design-oriented, supporting its role as a global model for sustainable packaging technologies.

Brazil: National Solid Waste Policy and Reverse Logistics Systems Accelerating Adoption

Brazil’s recyclable packaging market is guided by the National Solid Waste Policy (PNRS), which sets comprehensive rules for waste reduction, recycling, reuse, and disposal. A cornerstone of this policy is the implementation of reverse logistics systems, which place responsibility for post-consumer collection and recycling on producers and distributors. This regulatory pressure is accelerating investment in circular supply chains and eco-friendly packaging materials.

The country’s focus on curbing solid waste generation aligns with the adoption of recyclable trays, films, and containers—particularly in food packaging. Technologies like Modified Atmosphere Packaging (MAP) and vacuum-sealed recyclable films are being deployed to extend shelf life and reduce food waste, reflecting the link between sustainability and product quality. With strong government initiatives and increasing consumer awareness, Brazil is building a market framework that emphasizes responsibility, innovation, and compliance, positioning itself as a key Latin American hub for recyclable packaging solutions.

Recyclable Packaging Market Report Scope

Recyclable Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$224.9 Billion

|

|

Market Size (2034)

|

$389.8 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Material (Plastics, Paper & Paperboard, Glass, Metal, Bioplastics), By Packaging Type (Bottles & Jars, Boxes & Cartons, Bags & Pouches, Films & Wraps, Tubes & Vials), By End-Use Industry (Food & Beverages, Consumer Goods, Healthcare & Pharmaceuticals, E-commerce, Personal Care & Cosmetics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, DS Smith Plc, Smurfit Kappa Group Plc, Graphic Packaging Holding Company, Sonoco Products Company, Huhtamaki Oyj, International Paper Co., WestRock Company, ProAmpac, Berry Global, Inc., Greif, Inc., Silgan Holdings Inc., Pactiv Evergreen Inc., PAPACKS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Recyclable Packaging Market Segmentation

By Material

- Plastics

- Paper & Paperboard

- Glass

- Metal

- Bioplastics

By Packaging Type

- Bottles & Jars

- Boxes & Cartons

- Bags & Pouches

- Films & Wraps

- Tubes & Vials

By End-Use Industry

- Food & Beverages

- Consumer Goods

- Healthcare & Pharmaceuticals

- E-commerce

- Personal Care & Cosmetics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Recyclable Packaging Market

- Amcor plc

- Mondi Group

- DS Smith Plc

- Smurfit Kappa Group Plc

- Graphic Packaging Holding Company

- Sonoco Products Company

- Huhtamaki Oyj

- International Paper Co.

- WestRock Company

- ProAmpac

- Berry Global, Inc.

- Greif, Inc.

- Silgan Holdings Inc.

- Pactiv Evergreen Inc.

- PAPACKS

* List Not Exhaustive

Methodology

The research methodology for the Recyclable Packaging Market combines rigorous primary and secondary research approaches to deliver precise, actionable insights for industry professionals. Primary research involved in-depth interviews with packaging engineers, sustainability experts, supply chain managers, and senior executives from leading brands and converters across North America, Europe, and Asia-Pacific. Secondary research encompassed detailed analysis of company annual reports, regulatory frameworks, patents, sustainability disclosures, technical journals, and industry publications, with a focus on mono-material designs, paper-based packaging innovations, and advanced recycling technologies. Advanced data triangulation was applied to validate market sizing, CAGR projections, and regional trends, integrating factors such as government regulations, consumer preferences, raw material costs, and technological advancements in digital watermarking, barrier coatings, and PCR integration. Forecasts were built using both top-down and bottom-up approaches, while regional insights were contextualized against local policy mandates, circular economy initiatives, and e-commerce growth dynamics. This multi-layered methodology by USDAnalytics ensures that the report provides accurate, fact-based, and strategic intelligence aligned with the evolving global recyclable packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.