Recycled Plastics Market Size, Overview, and Growth Outlook (2025–2034)

Recycled Plastics Market Poised for Rapid Expansion Amid Rising Global Sustainability Demand

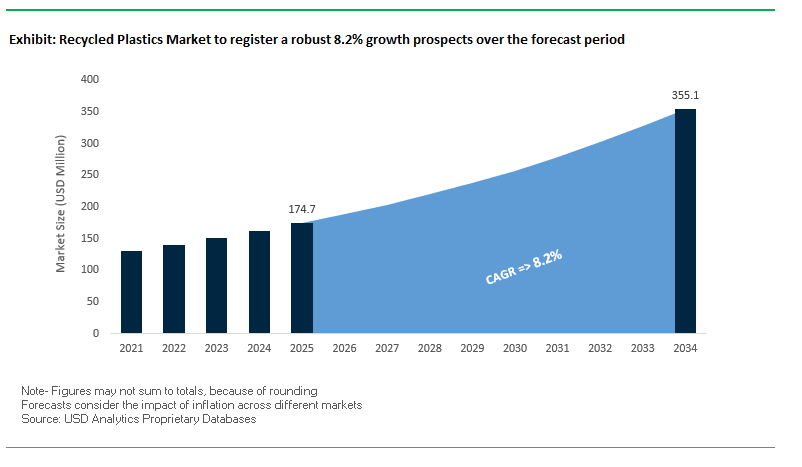

The global recycled plastics market is projected to grow from $174.7 million in 2025 to $355.1 million by 2034, registering a CAGR of 8.2%. The market growth is being driven by a structural supply-demand imbalance, technological advancements in sorting, and increased integration of post-consumer recycled (PCR) content by brands across industries. Faster growth than virgin plastics indicates a major industry shift towards sustainable material adoption, while innovations in chemical and mechanical recycling are enhancing the quality and reliability of recycled plastics.

Key Insights for industry professionals and buyers:

- Demand Outpaces Supply: Global demand for recycled plastics could exceed supply by up to 35 million tons by 2030, creating opportunities for expansion.

- Accelerated Growth Relative to Virgin Plastics: Recycled plastics production grows at 8% annually versus 2% for virgin plastics, signaling shifting industry priorities.

- Advanced Sorting Technologies: AI-enabled automated sorting reduces contamination and ensures high-quality recycled outputs.

- High PCR Integration: Leading brands, such as ExxonMobil in India, are using up to 50% PCR in products, exceeding local guidelines.

- Circular Economy Momentum: Companies are investing heavily in chemical recycling, mechanical recycling, and partnerships to improve global sustainability footprints.

- Investment-Driven Innovation: Strategic acquisitions and facility expansions are reshaping the competitive landscape.

These factors collectively highlight the strategic opportunities for market players aiming to capitalize on the growing global preference for sustainable plastic solutions.

Market Analysis: Strategic Collaborations and Facility Expansions Are Accelerating Growth in Recycled Plastics

The recycled plastics industry is witnessing strong growth due to strategic collaborations, technology-driven innovations, and expansions of production and recycling capacities. In September 2025, the Flexible Plastic Fund (FPF) published its FlexCollect report, providing a blueprint to integrate flexible plastic packaging into household recycling schemes, supported by over 400 tonnes of FPP collected during trials. Similarly, in August 2025, Mars partnered with Berry Global to transition pantry jars to 100% recycled plastic, expected to eliminate over 1,300 metric tons of virgin plastic annually.

Chemical recycling and strategic facility investments are shaping market dynamics. Loop Industries acquired a site in Gujarat, India in August 2025 to build its “Infinite Loop” manufacturing facility, targeting abundant polyester textile waste feedstock. In the same month, Indorama Ventures reported recycling over 150 billion post-consumer PET bottles since 2011, reflecting the company’s deep commitment to circular plastics. Earlier, in July 2025, Goldman Sachs Asset Management acquired Liquid Environmental Solutions, signaling increasing investment interest in circular economy ventures.

Consolidation and service integration also define recent developments. In November 2024, Waste Management acquired Stericycle for $7.7 billion, integrating regulated medical waste services into a healthcare-focused division. Market innovation continues in sustainable alternatives, as seen in March 2025, when DS Smith launched fiber-based e-commerce bags for Matas Group, offering viable alternatives to conventional plastic packaging.

Recycled Plastics Market: Trends and Opportunities Reshaping the Circular Economy

Corporate Procurement of High-Quality PCR Through Long-Term Offtake Agreements

A major trend redefining the recycled plastics market is the increasing reliance on long-term procurement agreements between brand owners and recyclers. These contracts are strategically designed to secure stable supplies of post-consumer recycled (PCR) materials, particularly high-quality resins required for food-contact and premium applications. In December 2022, Amcor entered into a five-year offtake agreement with ExxonMobil to source chemically recycled polyethylene (PE) resin, scaling up to around 220 million pounds annually. Such agreements de-risk large-scale procurement while enabling recyclers to justify capital-intensive investments in infrastructure. Importantly, pricing mechanisms within these contracts often include floors and ceilings that balance financial risks for both buyers and suppliers, as noted by the U.S. Plastics Pact. This contractual innovation is building confidence in a long-term, predictable market for recycled plastics, ensuring corporate buyers can meet ambitious recycled content goals without exposure to volatile spot pricing.

Strategic Investment in Advanced Recycling Infrastructure for Complex Plastics

Another defining trend is the wave of capital-intensive investments in advanced recycling infrastructure to process difficult plastics. Companies like Eastman Chemical have moved beyond pilot projects to establish commercial-scale facilities, with its Kingsport, Tennessee chemical recycling plant emerging as one of the largest globally. This facility can process challenging waste streams such as carpets and opaque bottles, converting them into high-quality polymers for reuse in high-value applications. The expansion of advanced recycling is closely linked to evolving regulatory frameworks. For instance, the U.S. Government Accountability Office (GAO) in 2021 highlighted that many states still classify advanced recycling facilities as waste disposal sites rather than manufacturing plants, limiting permitting and investment. However, policy reforms are accelerating as governments recognize the potential of these technologies to close the loop on plastics and reduce landfill dependency. Together, large-scale infrastructure investments and regulatory modernization are positioning advanced recycling as a cornerstone of the circular plastics economy.

Development of Non-Mechanical (Chemical) Recycling for Complex and Contaminated Feedstocks

The most transformative opportunity in the recycled plastics market is the rise of chemical recycling technologies capable of processing mixed, contaminated, and low-quality plastics that mechanical recycling cannot handle. According to a McKinsey report, chemical recycling significantly expands the recyclable universe by capturing materials such as multi-layer flexibles and heavily contaminated feedstocks, converting them into virgin-equivalent resins. Unlike mechanical recycling, which results in property degradation after multiple cycles, chemical recycling depolymerizes plastics at the molecular level. This enables the production of virgin-quality recycled resins suitable for demanding uses such as food-contact packaging and medical-grade applications. The ability to overcome “downcycling” is a game-changer, offering brands a credible pathway to achieve sustainability commitments while maintaining material performance across multiple cycles.

Integration of Digital Traceability and Mass Balance Certification

Another critical opportunity lies in digital traceability technologies and certification frameworks that build trust and compliance across the recycled plastics supply chain. The HolyGrail 2.0 initiative, facilitated by AIM—European Brands Association, has already validated the commercial-scale feasibility of digital watermarking. Industrial trials in Germany in mid-2025 achieved over 90% accuracy in differentiating food-grade from non-food-grade plastics, paving the way for cleaner, high-quality recyclate streams. Beyond sorting, traceability extends into certification. Blockchain-based pilots, such as the collaboration between Circularise and ISCC PLUS, have demonstrated how digital mass balance certification can provide an immutable audit trail for recycled content. This approach helps prevent greenwashing, ensures compliance with regional mandates, and strengthens consumer trust by offering transparent, verifiable claims. Together, digital watermarking and blockchain-based certification represent a powerful combination of technology and transparency that will drive adoption, compliance, and premium pricing in the recycled plastics market.

Competitive Landscape: Industry Leaders Are Driving Innovation and Circular Economy Adoption Across Global Recycled Plastics Markets

The competitive landscape is characterized by companies that focus on PCR content integration, advanced recycling technologies, and global expansion. Leaders are leveraging partnerships, acquisitions, and proprietary technologies to meet growing sustainability requirements while improving supply chain efficiency.

Berry Global Group, Inc.: Partnering with Global Brands to Scale PCR Adoption and Sustainable Packaging

Berry Global offers a diverse portfolio of rigid and flexible packaging with high PCR content. In August 2025, Berry partnered with Mars to convert pantry jars for brands like M&M'S to 100% recycled plastic, demonstrating leadership in FMCG packaging sustainability. The company has upgraded facilities in Heanor, UK, to process post-consumer and industrial flexible plastics, aligning with its goal to achieve 30% circular plastics across its packaging by 2030.

Indorama Ventures Public Company Limited: Transforming PET Waste into High-Quality rPET at Scale

Indorama Ventures is a leading producer of PET and recycled PET (rPET) resins. Since 2011, it has recycled over 150 billion PET bottles, showcasing a robust commitment to the circular economy. Its proprietary technology ensures low-carbon rPET production for beverages, food, and other applications. The company also promotes collection and sorting initiatives, exemplified by its “Waste Hero” program, to increase recycling efficiency globally.

SUEZ: Integrating Collection, Sorting, and Advanced Recycling to Ensure Reliable Recycled Feedstock

SUEZ specializes in environmental services and plastics recycling, converting diverse plastic waste into reusable materials. Its strength lies in an integrated approach combining collection, sorting, and advanced recycling. As co-author of the FlexCollect report in September 2025, SUEZ is actively scaling systems for hard-to-recycle plastics. Strategic partnerships and renewable energy initiatives, such as the July 2025 agreement with RATP Group, reinforce its commitment to circular and sustainable operations.

Loop Industries, Inc.: Pioneering Infinite Recycling of PET and Polyester Plastics for Global Brands

Loop Industries focuses on depolymerizing waste PET and polyester fiber into base monomers for virgin-quality resins. Its technology can process colored, contaminated, and ocean plastics without degradation. In August 2025, Loop acquired land in India for an Infinite Loop facility, exemplifying its strategy to license technology and partner with global brands for circular plastic solutions.

LyondellBasell Industries N.V.: Driving Circular Economy Adoption Through Mechanical and Chemical Recycling Innovations

LyondellBasell produces polyethylene, polypropylene, and other plastics, emphasizing mechanical and chemical recycling technologies. A founding member of the Alliance to End Plastic Waste, the company promotes circular economy initiatives worldwide. In June 2024, LyondellBasell successfully completed a commercial-scale run of Hostalen ACP 6443C, engineered for enhanced recyclability, highlighting its commitment to sustainable plastic solutions.

Recycled Plastics Market Share Insights, 2025-2034

PET leads Market Share by Polymer Type in Recycled Plastics Packaging

Polyethylene terephthalate (PET) holds the largest share at 38%, making it the champion of recycled plastics due to its established closed-loop recycling system. Food-grade rPET benefits from robust collection infrastructure, clear FDA approvals, and strong demand for bottle-to-bottle recycling, with beverage brands driving growth. High-density polyethylene (HDPE, 30%) follows as the versatile workhorse, used in opaque bottles for milk, detergents, and personal care. Its forgiving coloration and mature infrastructure make rHDPE one of the most reliable PCR streams. Polypropylene (PP, 18%) is the fastest-growing, with demand surging for trays, tubs, and closures as optical sorting and mechanical recycling technologies improve. Low-density polyethylene (LDPE, 7%), mainly recovered from bags and films, struggles with inconsistent quality and limited collection systems, relegating most PCR to non-food, thicker applications like trash bags or plastic lumber. The residual 7% from PS, PVC, and others remains problematic, with PVC actively phased out and PS constrained by low density and poor economics. PET and HDPE together account for the lion’s share because of food-contact compliance and scalable recycling economics, while PP’s rapid growth signals the next frontier in recycled polymer packaging.

Packaging dominates Market Share by End-Use in Recycled Plastics Packaging

Packaging is the undisputed leader at 65%, reflecting the direct influence of corporate sustainability targets, EPR legislation, and consumer demand for visible circular solutions. Food-grade PCR in PET and HDPE bottles commands premium value, while non-food applications like detergent, cleaning product, and cosmetic bottles drive mass demand for mixed-color PCR streams. Consumer goods (15%) are another major growth engine, with apparel, footwear, toys, and home goods integrating PCR as both a functional material and a marketing differentiator. Construction (10%) provides a critical outlet for mixed and lower-grade PCR, converting it into plastic lumber, decking, and pipes—diverting waste that might otherwise go to landfill. Automotive (7%) uses PCR for engineering-grade components such as underbody shields, liners, and trim, where durability and heat resistance are crucial. Textiles (3%), while historically the largest rPET user, largely represent downcycling, turning bottles into polyester fibers for clothing and carpets rather than maintaining circularity. Overall, packaging remains the center of gravity for PCR plastics, both in terms of volume and regulatory scrutiny, while construction and automotive ensure difficult-to-recycle streams also find durable, long-term applications.

European Union: Stringent Food Contact and Ecodesign Regulations Shaping Recycled Plastics

The European Union is at the forefront of regulating the recycled plastics market, with the introduction of Regulation (EU) 2022/1616 that establishes a legal framework for recycled plastic materials in food-contact packaging. Since July 2023, only plastics manufactured through approved or novel recycling technologies can be placed on the market, ensuring both safety and quality. This has created strong incentives for companies to invest in advanced recycling technologies, particularly those that maintain the purity required for food packaging applications.

Complementing this, the Ecodesign for Sustainable Products Regulation (ESPR), effective from mid-2024, introduced the Digital Product Passport (DPP), which requires transparency about product origin, compliance, and recyclability. The Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025, further raises the bar by setting ambitious targets for the entire packaging lifecycle, driving higher recycled content mandates. Companies are adapting to this regulatory environment by restructuring operations. For instance, Kureha Corporation exited its European heat-shrink multilayer film business to concentrate on PVDC films manufactured with in-house raw materials, boosting efficiency while ensuring compliance with EU’s sustainability directives.

United States: Federal Funding and Corporate Investments Accelerating Plastic Recycling

The United States is witnessing significant growth in the recycled plastics market, driven by regulatory backing and large-scale industry investments. The U.S. Environmental Protection Agency (EPA) is spearheading waste prevention, reuse, and recycling programs with support from the Infrastructure Investment and Jobs Act, which channels billions into building advanced recycling facilities. These developments are modernizing the nation’s recycling infrastructure and expanding access to high-quality recycled feedstocks.

According to the American Chemistry Council (ACC), more than $8.7 billion has been invested since 2017 in advanced recycling, recovery technologies, and mechanical recycling projects. A major industry trend is the adoption of mono-material packaging, which simplifies recycling streams and reduces contamination. Another driver is the premiumization of recycled plastics, with manufacturers creating high-margin cast films for premium applications such as automotive wraps and architectural graphics. These high-performance applications increasingly integrate recycled content, showcasing the versatility of next-generation recycled plastics in both consumer goods and industrial applications.

China: Domestic Recycling Infrastructure Expansion and Policy Enforcement

China has undergone a dramatic transformation in its recycled plastics market following the National Sword policy, which banned imports of most recyclable waste. This decision reshaped global recycling flows and forced China to develop robust domestic recycling infrastructure. The government’s 14th Five-Year Plan, implemented through the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE), emphasizes tighter plastic pollution control and mandates greater reuse of resources.

China is also phasing out non-biodegradable single-use plastics, with new policies under development to promote reuse systems and establish clear phase-out targets. Local companies are pioneering automation and large-scale plastic reprocessing, offering films compatible with eco-solvent, solvent, and UV printing technologies. Strategic investments, such as Kureha Corporation’s 2022 joint venture in China to produce PVDC, underline the nation’s importance as both a manufacturing hub and end market for recycled plastics. This infrastructure modernization supports the rapid growth of e-commerce packaging, automotive films, and food-grade applications in China.

India: EPR Rules and Traceability Standards Driving Market Formalization

The Indian recycled plastics market is being reshaped by the Plastic Waste Management (Amendment) Rules, 2024, which highlight Extended Producer Responsibility (EPR) for producers, importers, and brand owners. Under these rules, micro, small, and medium enterprises (MSMEs) are exempt, shifting accountability to larger manufacturers and importers. From July 2025, all plastic products in India must carry a barcode, QR code, or unique identification number to ensure traceability, enabling regulators to monitor compliance with recycling mandates.

Additionally, all recycled plastic packaging must display the percentage of recycled content and adhere to the Indian Standard IS 14534:2023. Innovation is also accelerating, with patents being granted for bioplastic derived from agricultural and dairy waste, such as ghee residue, which is biodegradable in both soil and water. These developments complement the rising demand from India’s processed food and consumer goods sectors, where recyclable and recycled plastic packaging is critical for meeting both safety standards and sustainability commitments.

Japan: Plastic Resource Circulation Strategy and Bio-PP Integration

Japan’s Plastic Resource Circulation Strategy is the key regulatory framework shaping its recycled plastics market, with an ambitious goal to make all plastic packaging reusable or recyclable by 2025. The strategy also targets doubling renewable material use by 2030, with strict waste-sorting mandates to improve material recovery efficiency. These measures reflect Japan’s broader ambition to lead in circular economy initiatives, with an emphasis on integrating recycled plastics into mainstream consumer and industrial applications.

Industry players are innovating aggressively. Companies like LyondellBasell and Shiseido are incorporating bio-polypropylene (bio-PP) into cosmetics packaging, blending renewable content with recycled plastics. Demand for premium printable films—valued for high-quality aesthetics and durability—is also rising, with recycled content increasingly incorporated to align with government mandates and consumer expectations. On an international scale, Japan’s MARINE Initiative, launched by the Ministry of Foreign Affairs (MOFA), is building global cooperation to fight marine plastic pollution, reinforcing Japan’s position as a leader in sustainable plastic management and recycled plastics innovation.

Brazil: Reverse Logistics System and Import Ban Reinforcing Domestic Recycling

Brazil’s recycled plastics market is being accelerated by the National Solid Waste Policy (PNRS), which emphasizes reuse, recycling, and responsible waste management. A key component is the reverse logistics system, which requires producers to take responsibility for post-consumer collection and recycling of packaging. This system is fostering investments in domestic recycling facilities and encouraging companies to design packaging that is easier to recover and recycle.

The introduction of Law No. 15,088 in January 2025, which bans the import of solid waste including plastics, paper, glass, and metals, is a pivotal step toward strengthening domestic waste management. By eliminating reliance on foreign recyclable inputs, the government is pushing industries to maximize the reuse of local plastic waste streams. Coupled with strong demand for sustainable packaging solutions in the food, beverage, and retail sectors, Brazil is rapidly building a more self-sufficient circular economy for recycled plastics, positioning itself as a growing leader in Latin America’s sustainability transition.

Recycled Plastics Market Report Scope

Recycled Plastics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$174.7 Million

|

|

Market Size (2034)

|

$355.1 Million

|

|

Market Growth Rate

|

8.2%

|

|

Segments

|

By Polymer Type (PET, HDPE, PP, LDPE, PVC, PS, Others), By Recycled Source (PCR Plastics, PIR Plastics), By End-Use Industry (Packaging, Automotive, Construction, Consumer Goods, Textiles), By Application (Bottles & Containers, Films & Sheets, Fibers & Filaments, Straps & Tapes)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

KW Plastics, Placon, Indorama Ventures Public Company Limited, Biffa plc, Avangard Innovative, SUEZ, SABIC, Veolia Environnement S.A., Envision Plastics, Loop Industries, Inc., PureCycle Technologies, Recyclex SA, MBA Polymers, Plastic Energy Limited, CarbonLite Holdings LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Recycled Plastics Market Segmentation

By Polymer Type

- PET

- HDPE

- PP

- LDPE

- PVC

- PS

- Others

By Recycled Source

- PCR Plastics

- PIR Plastics

By End-Use Industry

- Packaging

- Automotive

- Construction

- Consumer Goods

- Textiles

By Application

- Bottles & Containers

- Films & Sheets

- Fibers & Filaments

- Straps & Tapes

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Recycled Plastics Market

- KW Plastics

- Placon

- Indorama Ventures Public Company Limited

- Biffa plc

- Avangard Innovative

- SUEZ

- SABIC

- Veolia Environnement S.A.

- Envision Plastics

- Loop Industries, Inc.

- PureCycle Technologies

- Recyclex SA

- MBA Polymers

- Plastic Energy Limited

- CarbonLite Holdings LLC

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-step research methodology to deliver actionable insights into the recycled plastics market. Our approach integrates primary data collection from leading manufacturers, recyclers, and industry stakeholders, combined with secondary research from authoritative sources, including government reports, industry publications, and corporate filings. Market sizing and growth forecasts are calculated using a bottom-up approach, accounting for polymer types, recycled sources, end-use industries, and applications, while cross-validating with historical trends from 2015–2024. Competitive landscape analysis leverages corporate announcements, mergers, acquisitions, technological innovations, and sustainability initiatives to identify market leaders and emerging players. Regional analysis incorporates policy, regulatory frameworks, and local market dynamics in key geographies including the U.S., EU, China, India, Japan, and Brazil. USDAnalytics ensures all projections, including CAGR and market value forecasts through 2034, reflect current market realities, emerging recycling technologies, and evolving corporate sustainability commitments, enabling industry professionals to make data-driven strategic decisions with confidence.

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.