Market Overview: Rising Adoption of Sustainable and Lightweight Plastic Packaging

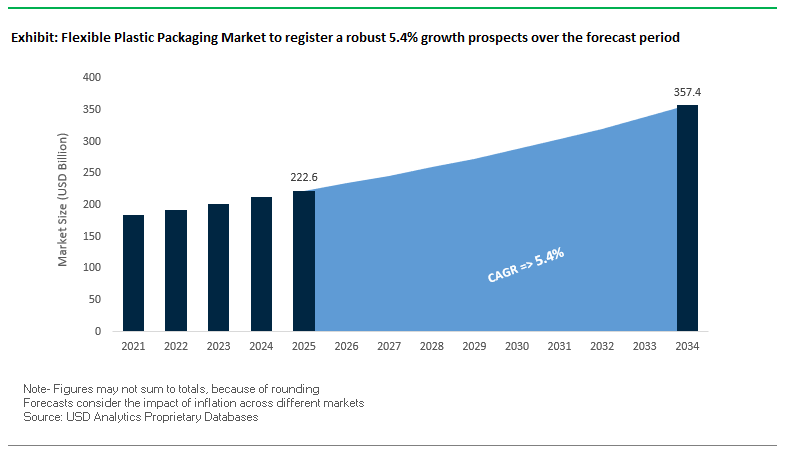

The Global Flexible Plastic Packaging Market is projected to grow from USD 222.6 billion in 2025 to USD 357.3 billion by 2034, registering a healthy CAGR of 5.4%. This industry is an essential component of the modern food, beverage, and consumer goods supply chain, valued for its ability to ensure convenience, preserve freshness, and reduce food waste. Flexible plastic packaging continues to dominate due to its versatility, lightweight structure, and cost-effectiveness, while simultaneously undergoing rapid transformation to meet global sustainability expectations.

A strong shift is underway toward recyclable, compostable, and post-consumer recycled (PCR) content-based packaging. Governments, retailers, and brand owners are all emphasizing sustainable packaging innovations to comply with circular economy targets. Another key driver is the rising demand for high-performance barrier films, which are critical in extending the shelf life of sensitive food products by protecting them from oxygen, moisture, and light exposure.

The use of lightweight flexible packaging not only reduces raw material consumption but also significantly lowers transportation and logistics costs, making it highly attractive for global brands seeking efficiency in their supply chains. Moreover, the acceleration of e-commerce and home delivery services is fueling demand for durable, impact-resistant, and lightweight flexible plastics that can handle diverse shipping conditions without compromising food safety or quality.

Key Insights for industry professionals and buyers:

- Market value to reach USD 357.3 billion by 2034, CAGR 5.4%.

- Recyclable and PCR-based packaging at the center of innovation.

- Barrier films drive shelf-life extension and food safety.

- Lightweight solutions reduce costs and carbon footprint.

- E-commerce boom fuels demand for impact-resistant flexible plastics.

Market Analysis: Recent Developments in the Flexible Plastic Packaging Industry

The Flexible Plastic Packaging Industry is undergoing a transformative phase, characterized by sustainability investments, mergers, and strategic collaborations.

In September 2025, the Flexible Plastic Fund (FPF) released its FlexCollect report in the UK, showcasing the success of its pilot program for at-home collection and recycling of flexible plastics. With an 89% satisfaction rate and nearly 90% clean recyclables, this initiative provides a scalable model for global collection systems.

In August 2025, Amcor completed a major upgrade to its Heanor, UK recycling facility, boosting its high-performance recycling infrastructure in Europe with an additional 2,800 tonnes of recyclate capacity for flexible plastic packaging. In the same month, ProAmpac announced its intent to acquire PAC Worldwide, expanding its strength in protective and e-commerce packaging—sectors that increasingly overlap with flexible plastic packaging.

Also in August 2025, the U.S. Flexible Film Initiative (USFFI) officially launched, creating a nonprofit coalition dedicated to developing a scalable recycling and recovery system for flexible plastics in the United States, signaling stronger industry alignment toward circularity.

In July 2025, two significant mergers reshaped the industry: Amcor–Berry Global combined forces to form a dominant leader in consumer packaging, while Smurfit Kappa–WestRock merged to create a giant in paper-based packaging, potentially reshaping the competitive balance with sustainable alternatives. During the same period, Huhtamaki unveiled a recyclable and compostable solution for the ice cream industry, reflecting the strong push for food-safe compostable packaging.

By May 2025, market reports confirmed that consumer demand for recyclable and compostable flexible plastic packaging was growing rapidly, particularly in Europe and North America, further accelerating R&D and infrastructure investments by key players.

Key Trends and Transformative Opportunities Driving the Flexible Plastic Packaging Market

Accelerated Adoption of Advanced Monomaterial Polyolefin Structures

The flexible plastic packaging market is witnessing a decisive transformation as manufacturers shift from multi-material laminates like PET/PE and NY/PE to advanced monomaterial structures primarily based on polyethylene (PE) or polypropylene (PP). This strategic move is driven by the growing need to create packaging that is technically recyclable in existing polyolefin streams, meeting stringent Extended Producer Responsibility (EPR) laws and corporate sustainability targets. Industry leaders such as Nestlé are piloting mono-material packaging for baby food, while Unilever is implementing PE-based pouches for personal care products. Companies like Toppan are combining mono-material barriers with compatible sealants to enhance recyclability. This trend not only creates a high-value growth avenue for suppliers who can deliver high-performance, compliant solutions but also reshapes the value chain, demanding tighter collaboration among raw material suppliers, converters, and brand owners. Investment in advanced machinery and R&D for mono-material solutions is accelerating innovation in the market.

Integration of Digital Watermarking for Smart End-of-Life Sorting

To overcome the complexity of sorting flexible packaging in Material Recovery Facilities (MRFs), the industry is increasingly adopting digital watermarking technology, exemplified by the HolyGrail 2.0 initiative. These imperceptible codes printed on packaging allow high-speed cameras to accurately identify and sort products by polymer type and food-contact status. Industrial trials in Germany achieved detection efficiency rates of 87.9% to 93.8%, validating the technology in real-world settings. Major brands, including Aldi, Arla Foods, Nestlé, and Procter & Gamble, have integrated digital watermarks, demonstrating a clear commitment to enhancing recycling performance. This technology not only enables the separation of food-grade and non-food-grade materials but also strengthens a data-driven, circular supply chain, fostering collaboration between packaging manufacturers, technology providers, and waste management companies. The adoption of digital watermarking represents a critical growth driver for manufacturers aiming to offer fully recyclable solutions.

Development of Molecular Recycling-Compatible Packaging Designs

As chemical or molecular recycling technologies scale, a significant opportunity arises to design flexible packaging optimized for advanced recycling. Such designs ensure that films, inks, and adhesives break down cleanly into base monomers without contaminating the process, enabling a circular lifecycle for complex plastics that are not suited for mechanical recycling. Companies like Eastman are investing up to $1 billion in molecular recycling facilities, capable of processing 160,000 metric tonnes of hard-to-recycle plastics annually. Major brands, including LVMH Beauty, Estée Lauder, Clarins, Procter & Gamble, L'Oréal, and Danone, have signed multi-year supply agreements, signaling strong demand for recyclable-ready packaging. This opportunity fosters collaboration among packaging manufacturers, chemical recyclers, and waste management firms, promoting an end-to-end circular supply chain.

Bio-Derived Feedstocks for Drop-In Flexible Films

Beyond recyclability, there is a growing opportunity to decarbonize flexible plastic packaging by using certified sustainable, bio-derived feedstocks such as waste cooking oil or tall oil from forestry. These feedstocks produce drop-in plastics with identical performance to fossil-based alternatives, allowing brands to reduce carbon footprints without altering existing production or recycling processes. Companies like Irplast (in partnership with SABIC) produce carbon-neutral, fully recyclable films from tall oil, while Taghleef Industries offers bioPP films from renewable resources suitable for conventional applications. Academic studies highlight ongoing research to enhance mechanical and gas barrier properties of bio-based films, making them increasingly viable for high-performance packaging. Commercializing bio-derived flexible films represents a major growth avenue, enabling manufacturers to meet sustainability goals while appealing to environmentally conscious consumers.

Competitive Landscape: Leading Players Driving Innovation and Sustainability

The Global Flexible Plastic Packaging Market is highly consolidated, with major packaging companies leveraging acquisitions, global networks, and material science innovations to strengthen their competitive advantage.

Amcor plc strengthens recycling and sustainable film development

Amcor remains a global leader in flexible plastic packaging, known for high-performance barrier films, vacuum bags, and recycle-ready pouches. In August 2025, it upgraded its UK recycling facility and expanded its healthcare packaging in Costa Rica. Its AmLite Recyclable and AmPrima® solutions highlight its strategy of making all packaging recyclable or reusable by 2025.

Huhtamaki Oyj expands compostable and recyclable flexible packaging

Huhtamaki focuses on food and beverage packaging, offering flexible films, pouches, and paper-based containers. In July 2025, it introduced a recyclable and compostable ice cream packaging solution. Its blueloop™ brand drives circular-ready designs, including mono-material PP and PE solutions.

Sealed Air Corporation pivots toward retail-focused Cryovac® solutions

Sealed Air, through its Cryovac® brand, is a leader in meat, poultry, and dairy packaging. In August 2025, it announced a turnaround strategy to shift focus toward retail packaging, addressing evolving consumer behavior. Its barrier shrink films and bags extend shelf life while reducing waste, with sustainability integration through recycled content.

ProAmpac expands with PAC Worldwide acquisition and recyclable films

ProAmpac, recognized for custom-engineered packaging solutions, announced its acquisition of PAC Worldwide in August 2025. Its ProActive Recyclable® film range provides sustainable alternatives for snacks, pet food, and frozen goods, engineered to replace hard-to-recycle laminates.

Berry Global Group advances circular polymers with Amcor merger

Berry Global is a key innovator in engineered packaging films, leveraging circular polymers, recycled content, and compostable materials. In July 2025, Berry completed its all-stock merger with Amcor, strengthening its global footprint and accelerating investments in sustainable flexible films across food, healthcare, and industrial applications.

Flexible Plastic Packaging Market Share Insights

Films & Wraps Lead Market Share by Packaging Type in Flexible Plastic Packaging

Films and wraps dominate the flexible plastic packaging market with 40% projected share in 2025, underscoring their role as the industry’s fundamental substrate and enabling material. Their versatility spans multiple applications—lamination to create pouches, single-layer wraps for baked goods and produce, shrink films for multipacks, and stretch films for pallet protection—making them indispensable across food, industrial, and consumer goods packaging. Pouches, while smaller in overall share, represent the most dynamic growth driver, fueled by stand-up pouch innovations with resealability, spouts, and high-barrier properties that support brand storytelling and lightweighting initiatives. Bags and sacks maintain volume dominance as cost-effective workhorses for retail and bulk packaging, ranging from grocery items to construction materials. Meanwhile, the “Other” category, including blister packs, inflatable void-fill, and specialized laminates, serves high-value, regulated niches. Collectively, this segmentation highlights how films & wraps secure leadership through ubiquity, while pouches capture innovation-driven growth, and bags & sacks anchor mass-volume adoption.

Food and Beverages Dominate Market Share by End-Use Industry in Flexible Plastic Packaging

The food and beverage industry commands 60% of market share in 2025, cementing its position as the single most important end-use segment for flexible plastic packaging. This dominance stems from the sector’s reliance on lightweight laminates, films, and pouches to preserve freshness, extend shelf life, and ensure safety at scale. With the rise of global processed food consumption, online grocery delivery, and single-serve packaging, flexible plastic has become irreplaceable in ensuring efficiency and regulatory compliance in food distribution chains. Cosmetics and personal care follow with a 15% share, driven by premium laminated tubes, sachets, and high-impact flexible packs that emphasize aesthetics and brand differentiation. Pharmaceuticals and healthcare demand blister packs, sterile barrier pouches, and child-resistant laminates, reflecting their compliance-driven nature. Industrial and automotive sectors rely heavily on strength and chemical resistance, utilizing heavy-duty bags and corrosion-protection films. Together, these segments demonstrate how food and beverages anchor scale and volume, while healthcare, personal care, and industrial applications drive premium, specification-led innovation.

United States Flexible Plastic Packaging Market Accelerates with Sustainable and Smart Packaging Innovations

The U.S. flexible plastic packaging market is experiencing significant transformation driven by a fragmented regulatory environment and the rise of Extended Producer Responsibility (EPR) laws across multiple states, including Maryland. These regulations shift the responsibility of recycling and waste management to manufacturers, encouraging the development of recyclable, mono-material films and minimizing multi-layer laminates. Technological advancements are central to market growth, with innovations like mono-material pouches for easier recycling and smart packaging integrated with QR codes and NFC chips, enabling supply chain traceability and enhanced consumer interaction through augmented reality experiences.

Corporate investments are expanding sustainable packaging production, with Amcor announcing a $250 million investment in its Wisconsin facility to enhance capacity for recyclable and bio-based materials. Key applications include e-commerce, direct-to-consumer (DTC) segments, and food and beverage sectors, driven by the need for durable, lightweight packaging suitable for shipping. Sustainability remains a critical market imperative, with the adoption of eco-friendly materials, bio-based films, and recyclable paperboard responding to consumer demand for environmentally responsible packaging solutions.

Germany Flexible Plastic Packaging Market Fueled by Circular Economy Practices and Regulatory Compliance

Germany’s flexible plastic packaging market operates under strict regulations, including the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates fully recyclable or reusable packaging by 2030 and limits hazardous substances like PFAS. The Packaging Act (VerpackG) promotes circular economy practices, incentivizing companies to design recyclable packaging through modulated fees, supported by strong demand for reusable containers and trays for FMCG products.

Technological innovation is driving sustainable solutions, with the development of machinery capable of processing eco-friendly materials and digital product passports or watermarks to improve recyclability and material transparency. Corporate initiatives include Amcor’s presentation of CleanStream technology at Fachpack Expo 2025, featuring mechanically recycled polypropylene (PP). Strong demand exists in retail and food service sectors, with consumers prioritizing premium pouches and high-barrier films that ensure product shelf life and align with Germany’s eco-conscious market expectations.

China Flexible Plastic Packaging Market Expands with Green Policies and Domestic Manufacturing Focus

China’s flexible plastic packaging market is strongly influenced by government initiatives under the “dual carbon” strategy and the March 2024 Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement, promoting recycling and sustainable material usage. Regulatory reforms, effective September 2023, address excessive packaging by limiting layers and void ratios, particularly impacting e-commerce goods.

Technological advancements such as automation, AI, and “5G plus industrial internet” integration enhance production efficiency and flexible packaging capacity. Domestic manufacturing is prioritized, with local companies expanding capabilities to substitute imported technologies. The rapid growth of e-commerce and food delivery sectors is a key driver, with online grocery deliveries expected to account for a significant share of new flexible packaging volumes, reinforcing China’s position as a fast-growing hub for innovative and circular packaging solutions.

India Flexible Plastic Packaging Market Strengthened by Circular Economy Initiatives and Domestic Manufacturing

India’s flexible plastic packaging market is benefiting from government initiatives supporting the circular economy, including the Food Safety and Standards (Packaging) Regulations, 2018, which ensure food-grade material safety while prohibiting recycled plastics for food contact. Technological adoption is rising, with innovations like UFlex’s Electron Beam Coating Technology eliminating print carrier layers and offering Ascelpius™ BOPET film made with up to 100% PCR content.

Corporate investments are expanding production to meet local demand, with UFlex operating over 100,000 TPA and four government-approved R&D laboratories. Key applications include food and beverage and personal care sectors, with the growth of e-commerce and sustainability trends driving demand for high-performance packaging. The “Make in India” initiative further supports domestic manufacturing, encouraging technological development and enabling local companies to efficiently meet rising national demand for sustainable flexible plastic packaging.

Japan Flexible Plastic Packaging Market Driven by High-Performance Films and Technological Collaborations

Japan’s flexible plastic packaging market leverages precision manufacturing and sustainability-driven innovations. In September 2024, Toppan Inc., in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., developed a recycled BOPP film for mass production, reflecting the country’s push toward circularity. The Plastic Resource Circulation Act (April 2022) guides the reduction of single-use plastics and encourages bio-based materials, aiming for 2 million tonnes annually by 2030.

The market emphasizes specialty and value-added films with superior barrier properties and IoT-enabled real-time tracking. Innovations such as easy-open tear notches and resealable closures cater to aging populations and single-person households. Strategic mergers and acquisitions, including Sika AG’s acquisition of Hamatite from Yokohama Rubber Co. in 2022, strengthen technological capabilities and market presence, particularly in automotive and construction sectors, positioning Japan as a leader in advanced and sustainable flexible plastic packaging solutions.

Flexible Plastic Packaging Market Report Scope

Flexible Plastic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$222.6 Billion

|

|

Market Size (2034)

|

$357.3 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material Type (PE, PP, PET, BOPP, CPP, Others), By Packaging Type (Pouches, Bags & Sacks, Films & Wraps, Other Packaging Types), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Industrial & Automotive, Other End-Use Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Berry Global Group, Inc., Sonoco Products Company, Sealed Air Corporation, DS Smith plc, ProAmpac, UFlex Ltd., Constantia Flexibles Group, Coveris Holdings SA, TC Transcontinental Packaging, Printpack Inc., Novolex Holdings, LLC, Bischof + Klein SE & Co. KG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Plastic Packaging Market Segmentation

By Material Type

- PE

- PP

- PET

- BOPP

- CPP

- Others

By Packaging Type

- Pouches

- Bags & Sacks

- Films & Wraps

- Other Packaging Types

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Industrial & Automotive

- Other End-Use Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexible Plastic Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Berry Global Group, Inc.

- Sonoco Products Company

- Sealed Air Corporation

- DS Smith plc

- ProAmpac

- UFlex Ltd.

- Constantia Flexibles Group

- Coveris Holdings SA

- TC Transcontinental Packaging

- Printpack Inc.

- Novolex Holdings, LLC

- Bischof + Klein SE & Co. KG

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-faceted research methodology to deliver a comprehensive analysis of the Global Flexible Plastic Packaging Market. The approach combined primary research, including detailed interviews with packaging manufacturers, converters, CPG brand executives, sustainability experts, and regulatory authorities, with secondary research covering company filings, patent databases, trade publications, and industry reports. Market sizing, growth projections, and trend identification were conducted across material types, packaging formats, and end-use industries, with a focus on innovations such as mono-material polyolefin structures, bio-based films, digital watermarking for recycling, molecular recycling compatibility, and lightweight solutions. Regional regulatory frameworks across the U.S., Europe, China, India, and Japan were analyzed to assess compliance, adoption rates, and impact on sustainability initiatives. Mergers, acquisitions, corporate investments, and technological advancements were also integrated into the analysis, offering actionable insights for industry professionals seeking strategic growth, operational efficiencies, and environmentally responsible packaging solutions in the flexible plastic sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.