Market Overview: Key Growth Insights in Global Compostable Packaging Industry

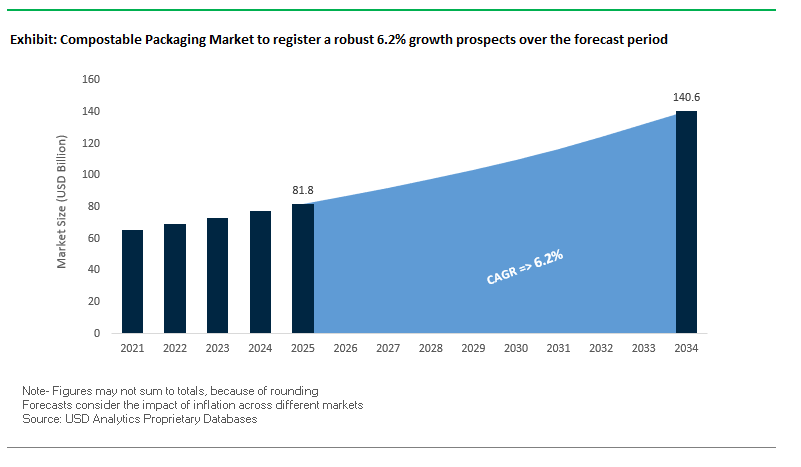

The Global Compostable Packaging Market is projected to reach USD 81.8 billion in 2025 and expand to USD 140.6 billion by 2034, growing at a steady CAGR of 6.2%. This market growth reflects the urgent global demand for sustainable alternatives to conventional plastic packaging, fueled by regulatory mandates, brand commitments to circularity, and rising consumer awareness of environmental impacts. Unlike traditional plastics, certified compostable packaging is designed to decompose safely, leaving no toxic residue or microplastics behind.

A defining feature of the industry is the increasing adoption of bio-based innovations such as Polylactic Acid (PLA), which mimics the performance of fossil-based polymers but is sourced from renewable feedstocks like corn starch. Paper and board materials are also emerging as a dominant force, leveraging existing recycling infrastructure and renewable credentials to strengthen their position in sustainable packaging. However, the industry’s success depends heavily on the expansion of composting infrastructure, as limited municipal facilities often hinder the effectiveness of compostable materials.

Key Insights for Industry Professionals:

- Market Value Growth: USD 81.8 billion in 2025 to USD 140.6 billion by 2034 (CAGR 6.2%).

- PLA and bio-based polymers are gaining dominance in high-performance compostable packaging.

- Paper-based packaging is a leading solution due to recyclability and strong brand adoption.

- Infrastructure gaps remain a key challenge, requiring municipal collaboration.

- Regulatory certifications (EN 13432, ASTM D6400, BPI) are critical adoption drivers.

Market Analysis: Recent Strategic Developments in Compostable Packaging

The compostable packaging sector is witnessing accelerated innovation and investments, underscoring the momentum toward sustainable materials. In September 2025, Mondi Group launched FunctionalBarrier Paper Ultimate, a high-barrier paper-based solution that highlights the growing trend of "paperization" across flexible packaging. In the same period, Cortec introduced its Eco Works 100 packaging film, certified industrially compostable and containing 100% USDA bio-based content, reinforcing the role of bio-derived polymers.

In July 2025, Amcor launched its Hector Child Resistant Closure (CRC) made with up to 100% PCR plastic, a move combining recyclability with sustainability. Around the same time, Futamura announced a £15 million sustainability investment at its UK site, aimed at enhancing energy efficiency and lowering emissions, reinforcing its leadership in cellulose-based compostable films. Earlier in May 2025, The Lignin Industries raised €3.9 million to scale tree-derived thermoplastics, tackling the reliance on fossil-based materials.

Innovation has also extended to consumer products. In February 2025, TIPA unveiled a home-compostable metallized high-barrier film for snack applications, solving a critical technical gap in barrier performance. In January 2025, Conserving Beauty adopted Futamura’s NatureFlex™ for its dissolvable cleansing wipes, reflecting growing adoption in personal care. Looking back, SEE (formerly Sealed Air) introduced a compostable protein tray in January 2024, certified by BPI for industrial composting an important milestone for fresh food packaging. At the strategic level, the October 2023 acquisition of Novamont by Versalis (Eni) solidified Novamont’s role as a global bioplastics leader.

Transformative Trends and Strategic Opportunities in the Compostable Packaging Market

Regulatory Mandates Driving Adoption of Compostable Packaging in Food Service

The compostable packaging market is witnessing strong regulatory momentum, particularly in the European Union, where government policies are shifting from voluntary measures to legally mandated standards for specific applications. The Packaging and Packaging Waste Regulation (PPWR, 2025) requires items such as permeable tea and coffee bags, as well as sticky produce labels, to be compostable by 2028. This legislation is creating a non-negotiable demand pull for compostable packaging solutions, compelling brand owners and manufacturers to comply. The trend is propelled by the need to prevent food-contaminated recycling streams from rendering plastics unrecyclable. In the United States, localized ordinances in cities and event venues similarly mandate compostable packaging for food service, generating targeted market demand. This regulatory-driven adoption is transforming compostable packaging from a niche product into a mandatory solution, driving R&D investment, process optimization, and market expansion.

Material Science Innovation Focused on Home-Compostable Certification

With limited industrial composting infrastructure, the end-of-life challenge for compostable packaging has catalyzed R&D into materials that meet home-compostable standards. Innovations are focused on biopolymer blends and advanced coatings that provide adequate barrier properties against moisture, oxygen, and aromas while remaining compostable in backyard bins. Organizations such as the Biodegradable Products Institute (BPI) provide certification for home-compostable films, helping consumers and municipalities trust these solutions. Research into cellulose-based films with specialized coatings demonstrates that high-performance home-compostable films are now feasible, suitable for various food applications. This trend is particularly significant for urban consumers with limited recycling access, creating a high-value opportunity to meet growing sustainability expectations.

High-Barrier Compostable Films for E-commerce Fresh Food Delivery

The surge in online grocery and meal-kit delivery has escalated flexible packaging waste, creating a critical opportunity for high-barrier compostable films. These films provide the necessary oxygen and moisture protection to maintain freshness for produce, meats, and prepared foods throughout the last-mile delivery process. Companies such as TIPA are developing home-compostable metallized high-barrier films, demonstrating that compostable packaging can meet the stringent performance requirements of perishable food products. This segment represents a high-growth avenue within the compostable packaging market, offering consumers the convenience of home composting while supporting e-commerce brands in achieving sustainability commitments. Additionally, this trend fosters collaboration between material scientists, packaging manufacturers, and online retailers, driving innovation and supply chain alignment.

Strategic Partnerships to Expand Industrial Composting Infrastructure

The lack of widespread industrial composting infrastructure presents both a challenge and an opportunity for the compostable packaging market. Industry consortia, such as the Composting Consortium managed by Closed Loop Partners, bring together major brands like PepsiCo, Kraft Heinz, and Target to invest in and pilot industrial composting solutions. This strategic approach ensures that compostable packaging has a viable end-of-life pathway, de-risking sustainability investments while supporting the circular economy. Investment opportunities span public and private capital, grants, and private equity, enabling the scaling of food-waste composting facilities in both the U.S. and Europe. By addressing this bottleneck, companies can strengthen their market positioning, improve consumer trust, and enhance global supply chain sustainability, marking a crucial growth avenue for the compostable packaging market.

Competitive Landscape: Leading Companies in Compostable Packaging Industry

The global compostable packaging industry is moderately consolidated, featuring biopolymer specialists, cellulose film producers, and diversified packaging giants advancing compostable solutions.

Novamont S.p.A. strengthens global leadership with Versalis acquisition

Novamont, renowned for its Mater-Bi bioplastics, is a leader in compostable polymers across food packaging and agriculture. In October 2023, its acquisition by Versalis (Eni) enhanced its global competitiveness. Novamont focuses on EN 13432-certified industrial compostability and continuous innovation in biochemicals, reinforcing its stronghold in European and global markets.

TIPA Corp Ltd. drives innovation in compostable snack packaging

TIPA specializes in compostable flexible films and laminates for food, fashion, and consumer goods. In February 2025, it launched a home-compostable metallized high-barrier film, overcoming a critical limitation in snack packaging sustainability. TIPA emphasizes end-of-life solutions that mimic organic waste breakdown, positioning itself as a solution provider to the global plastic waste crisis.

Futamura Chemical Co., Ltd. invests in sustainable cellulose packaging

Futamura is globally recognized for its NatureFlex™ cellulose films, widely used in food and confectionery. In July 2025, the company announced a £15 million UK investment to enhance sustainability and performance. Its focus lies in replacing conventional plastics with compostable cellulose films, leveraging deep technical expertise and strong market credibility.

NatureWorks LLC expands PLA capacity for Asia-Pacific growth

NatureWorks is a pioneer in Ingeo PLA biopolymers, serving compostable packaging, food service, and fibers. In May 2024, the company secured record financing from Krungthai Bank PCL to support its PLA expansion in Thailand, strengthening its footprint in Asia-Pacific. Its PLA products serve diverse applications, including packaging films, disposable utensils, and food service ware, all aligned with compostable standards.

Mondi Group leads in paper-based sustainable composites

Mondi is a leader in paper-based composite packaging, with strong commitments to circularity. In September 2025, it launched the FunctionalBarrier Paper Ultimate, advancing paperization in high-barrier packaging. By 2024, 87% of Mondi’s portfolio was reusable, recyclable, or compostable. As a member of the 4evergreen alliance, Mondi is driving industry-wide fiber packaging recyclability initiatives.

Novolex Holdings Inc. partners with sports venues for sustainability

Novolex, a North American leader in foodservice packaging, markets compostable solutions through its Eco-Products brand. In May 2025, Eco-Products became the official zero-waste partner of the San Francisco Giants, underscoring its push for sustainability in sports and entertainment. Novolex leverages its extensive manufacturing and distribution footprint to provide recyclable, compostable, and reusable solutions to customers ranging from small businesses to multinationals.

Compostable Packaging Market Share Insights

Bags & Pouches Retain Largest Market Share by Application in Compostable Packaging

Within the broader compostable packaging industry, bags and pouches dominate with 30% share, reflecting their role as the most visible and regulated category of single-use plastics targeted by bans and corporate sustainability programs. Their ubiquity in retail carry bags, produce bags, and lightweight flexible packaging positions them as the front line of compostable adoption. The segment benefits from relatively mature technology, with PLA/PBAT blends delivering cost-competitive solutions that balance compostability with mechanical performance. In contrast, segments such as cups & plates and trays & containers are heavily driven by the foodservice sector, where regulatory bans on EPS foam and single-use plastics accelerate adoption, though technical challenges in durability and clarity remain. Films & sheets and rigid packaging trail due to performance limitations, with rigid formats particularly constrained by high cost and weak barrier properties compared to PET. Nevertheless, rigid compostable bottles and tubs represent a high-value innovation frontier, while flexible bags and pouches will continue to lead on both volume and visibility in global regulatory discussions.

Food & Beverages Continue to Anchor Market Share by End-Use Industry in Compostable Packaging

The food and beverage sector commands 70% of global compostable packaging demand, making it the most important end-use industry by a wide margin. This dominance is due to the direct overlap between single-use plastic bans and food packaging applications, particularly in retail, restaurants, and e-commerce groceries. Compostable solutions are increasingly replacing cutlery, straws, trays, produce packaging, and single-serve sachets, with regulatory momentum accelerating adoption in both developed and emerging economies. E-commerce emerges as the second-largest and fastest-growing end-use industry, with major retailers transitioning to compostable mailers, protective cushions, and padded bags to meet ESG targets and consumer expectations. Personal care and cosmetics leverage compostable packaging more as a premium marketing attribute, aligning sustainable packaging with organic product narratives. Healthcare remains the most constrained adopter, confined to secondary and non-sterile applications due to sterility and compliance requirements. This segmentation highlights that while food and beverage remains the commercial stronghold, e-commerce is rapidly evolving as the growth engine that will diversify compostable packaging demand beyond traditional foodservice and retail channels.

United States Compostable Packaging Market Accelerated by State-Level Regulations and Material Innovation

The U.S. compostable packaging market is being strongly shaped by a patchwork of state-level regulations, driving the adoption of sustainable solutions. Maryland and Washington’s Extended Producer Responsibility (EPR) bills in May 2025 provide financial incentives for producers to use recyclable or compostable materials, while California’s SB 54, enacted in 2024, mandates a 25% reduction in plastic packaging by 2032, with all packaging required to be fully recyclable or compostable. These regulations are compelling businesses to innovate in sustainable packaging design.

Technological advancements are fueling market growth, with research from the Georgia Institute of Technology creating films from chitin and cellulose that offer superior oxygen barrier properties. Bio-based polymers like Polylactic Acid (PLA) and Polyhydroxyalkanoates (PHA) are gaining traction for both industrial and home compostable applications. Corporate investments, supported by initiatives such as the U.S. Plastics Pact, are driving the development of circular packaging solutions. Key applications include food packaging, retail, and food service sectors, with e-commerce growth and heightened hygiene awareness post-pandemic further boosting demand. Certifications from bodies like the Biodegradable Products Institute (BPI) and academic research on water-based silk fibroin coatings are adding credibility and driving adoption of high-performance compostable packaging.

Germany Compostable Packaging Market Strengthened by Circular Economy Mandates and Innovation

Germany’s compostable packaging market operates under the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates that all packaging be fully recyclable or reusable by 2030. Specific items, such as fruit stickers and tea bags, must be compostable by 2028, creating significant market opportunities. The Packaging Act (VerpackG) enforces producer responsibility across the entire lifecycle, influencing the design and production of compostable materials compatible with recycling systems.

Technological innovation in Germany is focused on ultra-modern extrusion, printing, and converting machinery for sustainable materials, ensuring quality, traceability, and compliance with regulatory demands. Collaborations between research institutions like the Fraunhofer Institute for Interfacial Engineering and Biotechnology and industry players are driving the development of advanced biodegradable packaging solutions. The market is particularly strong in food, beverage, and retail sectors, with growing demand for organic and fresh produce packaging. Corporate partnerships, including collaborations for high-performance and customized compostable solutions, are further accelerating market growth.

China Compostable Packaging Market Fueled by Green Policies and Domestic Production Expansion

China’s compostable packaging market is being driven by the government’s “dual carbon” goal, which encourages industrial sustainability and the adoption of circular materials. The March 2024 “Action Plan for Promoting Large-Scale Equipment Updates and Consumer Goods Replacement” encourages recycling and sustainable packaging, while regulatory reforms, including the national standard on “Limit of Harmful Substances of Coatings” effective June 2026, enforce safer material usage.

Technological advancements focus on automation, AI, and “5G plus industrial internet” integration, optimizing production efficiency and flexibility. Domestic production is being prioritized to substitute imported solutions, meeting the growing demand for high-quality circular packaging. Rapid growth in e-commerce, fresh food, and food delivery sectors is a key driver, alongside government efforts to curb over-packaging with a “whole-chain administration system on over-packaging.” Ongoing R&D and patent activities position China as a leader in innovative, sustainable compostable packaging solutions.

Brazil Compostable Packaging Market Expanded by Regulatory Push and Sustainable Manufacturing

Brazil’s compostable packaging market is shaped by the National Solid Waste Policy and new 2024 laws banning single-use items, with a 2030 deadline for fully compostable or recyclable packaging. Technological advancements, including robotics and AI for efficiency and quality control, are enhancing production capabilities. Biodegradable films using carboxymethyl cellulose (CMC) from sugarcane bagasse are notable innovations in this market.

Sustainability is a central focus, with companies increasingly aligning with circular economy principles. Key applications include food, beverage, and cosmetics packaging, driven by the expanding domestic food processing sector. Governmental support through decrees and ordinances is expected to enforce mandatory recycling targets of 30% this year and 50% by 2040, directly impacting production and materials. Corporate initiatives are investing in machinery and sustainable technologies to meet the growing demand for high-quality compostable packaging.

India Compostable Packaging Market Boosted by Government Programs and Strategic Partnerships

India’s compostable packaging market is bolstered by government initiatives such as “Swachh Bharat Abhiyan” and single-use plastic bans, encouraging the adoption of biodegradable alternatives. Major industry players are offering compostable films derived from cornstarch and other biopolymers, catering to both home and industrial composting needs.

Technological advancements in India include automated production systems and the development of plastic-free laminate-grade films suitable for lamination with paper and foil. Market growth is driven by the expanding e-commerce, food & beverage, and pharmaceutical sectors. Strategic partnerships like the CIRCLE Alliance, launched by Unilever, USAID, and EY in August 2024 with USD 21 million in funding, are promoting packaging circularity and reducing plastic waste. Key applications focus on ready-to-drink beverages and processed foods, reinforcing India’s role as a rapidly growing market for sustainable compostable packaging solutions.

Canada Compostable Packaging Market Strengthened by National Zero-Waste Strategy and Certification Requirements

Canada’s compostable packaging market is aligned with the government’s goal of achieving zero plastic waste by 2030. New regulations mandate labeling standards for plastic packaging, restrict the use of terms such as “compostable” or “biodegradable” without third-party certification, and prohibit the chasing-arrows symbol unless recyclability is verified.

The focus on infrastructure development complements these regulatory measures, emphasizing that labeling alone is insufficient to increase recycling and composting rates. Technological advancements are directed toward diverting compostable plastics from landfills to organic waste management systems. Corporate initiatives are increasingly aligned with government mandates, promoting product design improvements and strengthening secondary markets for recycled plastics. Targeted applications include plastic cutlery, straws, bento trays, and takeout containers, driving demand for certified compostable alternatives across Canada.

Compostable Packaging Market Report Scope

Compostable Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$81.8 Billion

|

|

Market Size (2034)

|

$140.6 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Material Type (Paper & Paperboard, Plastic, Others), By Application (Films & Sheets, Rigid Packaging, Bags & Pouches, Trays & Containers, Cups & Plates, Other), By End-Use Industry (Food & Beverages, Personal Care & Cosmetics, Healthcare, E-commerce, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Futamura Group, Novamont S.p.A., TIPA Compostable Packaging, Taghleef Industries LLC, Walki Group Oy, Billerud AB, Innovia Films, BASF SE, NatureWorks LLC, Suvjay Industries India LLP, Kingfa Sci. & Tech. Co., Ltd., Novolex, Mondi Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Compostable Packaging Market Segmentation

By Material Type

- Paper & Paperboard

- Plastic

- Others

By Application

- Films & Sheets

- Rigid Packaging

- Bags & Pouches

- Trays & Containers

- Cups & Plates

- Other

By End-Use Industry

- Food & Beverages

- Personal Care & Cosmetics

- Healthcare

- E-commerce

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Compostable Packaging Market

- Amcor plc

- Mondi Group

- Futamura Group

- Novamont S.p.A.

- TIPA Compostable Packaging

- Taghleef Industries LLC

- Walki Group Oy

- Billerud AB

- Innovia Films

- BASF SE

- NatureWorks LLC

- Suvjay Industries India LLP

- Kingfa Sci. & Tech. Co., Ltd.

- Novolex

- Mondi Group

* List Not Exhaustive

Methodology

The insights presented in this Compostable Packaging Market report have been developed by USDAnalytics using a robust, industry-focused methodology designed for professional decision-making. The research integrates primary data from in-depth interviews with key stakeholders, including biopolymer producers, packaging manufacturers, brand owners, and regulatory authorities, to understand material adoption, certification requirements, and technological advancements. Secondary research involved extensive analysis of corporate press releases, product launches, patent filings, government regulations, sustainability initiatives, and industry publications to capture market trends in PLA, PHA, cellulose, and paper-based packaging. The methodology also assessed regional policy impacts, such as EU Packaging and Packaging Waste Regulation, California SB 54, and India’s single-use plastic bans, while examining infrastructure gaps and consumer adoption patterns. Quantitative analysis of market sizing, CAGR, segmentation by material, application, and end-use, combined with qualitative evaluation of strategic investments, partnerships, and technological innovations, provides a holistic understanding of market dynamics. USDAnalytics further analyzed emerging trends in home-compostable certification, high-barrier films for e-commerce, and industrial composting partnerships, offering actionable insights into competitive strategies, growth opportunities, and regulatory drivers shaping the global compostable packaging industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.