Market Overview: Fiber Packaging Market to Reach $453.7 Billion by 2034 at 3.4% CAGR

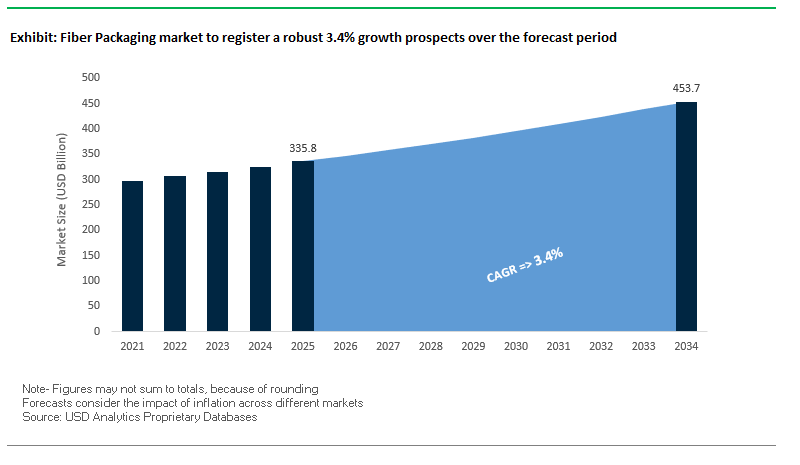

The global fiber packaging market is projected to grow from $335.8 billion in 2025 to $453.7 billion by 2034, expanding at a CAGR of 3.4%. Fiber-based packaging has become the backbone of sustainable packaging solutions, replacing plastics in multiple applications ranging from foodservice containers to e-commerce shipping boxes. For industry professionals and buyers, the market answers critical questions around sustainability compliance, performance in logistics, and the role of innovation in barrier technologies. The growing need to reduce carbon footprints and align with global ESG targets is further accelerating adoption.

Key Insights for buyers and professionals:

- E-commerce Boom: Online retail remains a key growth catalyst, with demand for lightweight, recyclable, and protective packaging rising sharply.

- Innovation in Barrier Coatings: Bio-based and PFAS-free coatings are extending fiber packaging’s reach into fresh food, frozen goods, and fast-food packaging.

- Circularity in Focus: Leading players commit to 100% recycled or sustainably sourced fiber, validating circular economy principles.

- Technology Leaps: Dry molded fiber technologies, such as PulPac’s water-free systems, cut CO2 emissions by up to 80%, reshaping production efficiency.

Market Analysis: Strategic Deals, Facility Expansions, and Sustainable Solutions

The fiber packaging industry is undergoing consolidation and innovation simultaneously, with M&A activity and technology-driven launches reshaping the competitive dynamics.

In August 2025, Mondi unveiled its Ad/Vantage Smooth Brown Paper, designed for industrial applications, showcasing its innovation in fiber-based substrates. That same month, Mondi announced plans to achieve 90% energy self-sufficiency at its Slovakian pulp and paper mill with a new biomass power plant, reinforcing its sustainability roadmap.

Major consolidation came in July 2025, when International Paper completed its $9.9 billion acquisition of DS Smith, creating a global leader with an enhanced fiber packaging footprint. In parallel, Packaging Corporation of America acquired Grief’s containerboard business for $1.8 billion, strengthening its U.S. operations. A month earlier, in June 2025, Mondi partnered with Saga Nutrition to launch a recyclable, paper-based pet food packaging solution, a sign of expanding fiber packaging applications.

Other notable moves include Ahlstrom’s April 2025 acquisition of the Stevens Point facility, boosting its specialty fiber-based material offerings for life sciences and high-performance sectors. In April 2025, International Paper also divested its Global Cellulose Fibers (GCF) business for $1.5 billion, focusing capital on core sustainable packaging segments. Meanwhile, DS Smith in March 2025 launched a new R&D and Innovation Center near Birmingham, UK, aimed at accelerating the creation of radically new circular packaging solutions.

Emerging Trends and Growth Opportunities in the Fiber Packaging Market

Accelerated Corporate Adoption of Circular Economy Principles

The fiber packaging market is experiencing a rapid transformation as corporations shift from broad sustainability pledges to concrete actions that integrate circular economy principles. Consumer pressure, investor expectations, and regulatory deadlines are compelling major brands to replace virgin plastics with fiber-based alternatives and to build out recycling infrastructure. In 2024, Unilever announced its commitment to reduce virgin plastic by over 100,000 tonnes, with fiber packaging being a core part of its material strategy. Similarly, beverage and food companies are scaling their reliance on recycled fibers to meet recyclability targets outlined under the EU Packaging and Packaging Waste Regulation (PPWR), which mandates that all packaging must be recyclable by 2030.

Industry collaborations also reflect this systemic shift. The Alliance for Beverage Cartons and the Environment (ACE) is piloting new collection and recycling models across Europe to improve carton recovery rates. Fiber packaging is thus no longer viewed solely as a “sustainable alternative,” but as a regulatory necessity and a cornerstone of corporate ESG strategies. With recycling rates becoming a competitive differentiator, fiber-based materials are emerging as a preferred solution for both consumer-facing brands and industrial supply chains.

Strategic Investment in Domestic and Diversified Production Capacity

The fiber packaging industry is also reshaping its global footprint through massive investments in domestic and regional production capacity. Geopolitical uncertainty, combined with escalating shipping costs, has driven companies to adopt nearshoring strategies to secure fiber supply and improve responsiveness to market demand. For example, in May 2024, Mondi announced a €200 million investment in its Duino mill in Italy, converting it into a high-quality recycled containerboard facility with a capacity of 420,000 tonnes per year. This project is part of the company’s €1.2 billion capital plan to strengthen its European presence.

North America is seeing a similar trend. International Paper, in June 2025, outlined its strategic plan to grow its sustainable packaging business by expanding regional production capacity, highlighting a clear pivot towards fiber-based growth. Beyond expansions, mergers and acquisitions are being pursued to secure innovative fiber technologies. These deals are designed not only to strengthen market positions but also to diversify portfolios with next-generation fiber-based barrier materials. This structural realignment underscores how fiber packaging has become both a compliance-driven requirement and a long-term growth strategy.

Development of High-Performance, Plastic-Free Barrier Coatings

A critical bottleneck for fiber packaging has long been its vulnerability to moisture, grease, and oxygen transmission, which has historically required plastic liners or PFAS-based coatings. However, a major opportunity now lies in scaling plastic-free barrier technologies that maintain fiber recyclability while extending its application to high-moisture and food-grade uses.

Companies such as Omya and Solenis are commercializing water-based and biowax-based coatings marketed under brands like EarthGuard and TopScreen that provide grease and water resistance for foodservice packaging. Academic research further validates these efforts, with cellulose nanocrystal and chitosan-enhanced coatings demonstrating superior oxygen and moisture barrier properties, while remaining compostable and repulpable. Importantly, these coatings are being engineered for compatibility with existing paper machine coaters and flexographic presses, reducing the need for costly new equipment.

The transition to bio-based coatings will enable fiber packaging to penetrate new categories traditionally dominated by plastics, including ready-to-eat meals, fast food, and frozen foods. For manufacturers, the ability to offer plastic-free, recyclable fiber packaging with functional barrier protection represents a substantial market expansion opportunity aligned with regulatory compliance and consumer demand.

Integration of Digital Technologies for Supply Chain Efficiency

Another high-value opportunity lies in embedding digital watermarks and intelligent identifiers into fiber packaging to improve both recyclability and supply chain management. Corrugated and carton packaging provide a “blank slate” for such technologies, enabling precise material sorting and enhanced transparency.

The HolyGrail 2.0 initiative has proven the industrial viability of digital watermarks, achieving over 90% detection rates in large-scale trials in Germany. This technology allows packaging to be sorted by SKU, food-grade status, or fiber quality, enabling recyclers to achieve unprecedented material purity. Beyond waste management, brands can leverage these identifiers as digital passports, enabling real-time product tracking from production lines to consumers.

For brands, this integration enhances supply chain visibility, counterfeit prevention, and consumer engagement. A consumer scanning a fiber box with a smartphone could instantly access farm-to-shelf traceability, sustainability credentials, or promotional content. This capability transforms fiber packaging from a passive container into a data-driven platform that supports circularity, compliance, and marketing differentiation.

Competitive Landscape: Global Leaders Driving Fiber Packaging Transformation

The fiber packaging market is dominated by established global leaders who are differentiating themselves through sustainable innovation, acquisitions, and end-to-end integration.

Smurfit Kappa Group Merging with WestRock to Build a Global Packaging Giant

Smurfit Kappa remains a leading producer of corrugated and containerboard solutions for food, beverage, and e-commerce. It is set to complete a landmark merger with WestRock, creating one of the largest global sustainable packaging providers. Smurfit Kappa has also trialed hydrogen-powered solutions at its plants, advancing decarbonization. With its fully integrated supply chain, the company controls sourcing from forest to final design, ensuring consistent sustainability credentials.

International Paper Expanding with DS Smith Acquisition and Strategic Investments

International Paper has solidified its position with the $9.9 billion acquisition of DS Smith in July 2025, greatly expanding its European presence. It is investing $250 million to convert a paper machine at its Riverdale mill to produce containerboard for e-commerce growth. Its decision to divest the Global Cellulose Fibers business in April 2025 allows sharper focus on high-margin packaging solutions. With containerboard and corrugated boxes as its backbone, International Paper remains a dominant global player.

Mondi plc Driving Sustainable Innovation with Barrier Papers and Energy Self-Sufficiency

Mondi has consistently led innovation with recyclable and compostable fiber packaging solutions. Its launch of FunctionalBarrier Paper Ultimate reflects strong progress toward PFAS-free, high-barrier alternatives to plastics. Mondi’s MAP2030 sustainability plan ensures every new product is “sustainable by design.” Beyond product innovation, Mondi is investing in biomass power at its Slovakian plant to achieve 90% self-sufficiency, further cementing its ESG leadership in packaging.

WestRock Company Expanding Facilities and Merging with Smurfit Kappa

WestRock offers an extensive portfolio of corrugated containers, consumer packaging, and paperboard products. Its planned merger with Smurfit Kappa will position the combined entity as a global packaging leader. In parallel, WestRock has announced a $47 million expansion at its Claremont, North Carolina plant, expected to enhance production capacity and create 50 new jobs. Its vertically integrated model ensures strong control over supply chain security and quality assurance.

DS Smith Plc Accelerating Innovation with Circular Economy Packaging

DS Smith continues to be a leader in circularity-by-design, with corrugated solutions tailored for recyclability and logistics efficiency. In March 2025, it launched a new R&D and Innovation Center in the UK, dedicated to next-generation fiber packaging solutions. Its product launches, including TailorTemp temperature-controlled packaging, highlight the company’s expansion into value-added, sustainable solutions for food, automotive, and industrial sectors. With circularity at its core, DS Smith is reinforcing its role as an innovation-driven competitor in the global market.

Fiber Packaging market Share Insights

Corrugated Boxes Dominate Market Share by Packaging Type in Fiber Packaging

In 2025, corrugated boxes command 55% of fiber packaging, the uncontested workhorse of global trade and last-mile e-commerce thanks to strength-to-weight advantages, stackability, and custom die-cutting that enable right-sizing and damage reduction. Cartons & folding boxes at 20% remain the retail-ready branding engine, offering premium print surfaces for F&B, personal care, and OTC pharma while aligning with recyclability goals. Molded fiber accelerates as the sustainable disruptor, displacing plastic clamshells and protective end-caps with compostable, recycled-pulp solutions; rapid adoption in foodservice and electronics cushioning expands its footprint. Sacks & bags anchor industrial and agri bulk flows (cement, flour, feed), prized for durability and cost per ton moved, while “other” formats paper mailers, padded envelopes scale with plastic-to-paper substitution in e-commerce. Net-net, packaging-type share reflects fiber’s circular-economy credentials and capital flowing to high-speed corrugators, digital print, and molded-fiber tooling.

Food & Beverages Lead Market Share by End-Use Industry in Fiber Packaging

Food & beverages hold 35% of fiber packaging in 2025, driven by hygiene, barrier-coating innovation (grease/moisture resistant yet recyclable), and SKU breadth from ambient groceries to frozen foods and beverage carriers. E-commerce at 30% is the modern growth catalyst, dictating investments in high-throughput box plants, on-demand right-sizing, and molded-fiber cushions for ship-in-own-container strategies. Industrial end-users provide a heavy-duty base drums, triple-wall corrugated, and large shippers prioritize performance over aesthetics while personal care & cosmetics trade up to premium cartons and molded fiber for tactile sustainability cues. Healthcare & pharmaceuticals contribute a regulated, high-value niche (child-resistant cartons, sterile barriers). This end-use mix aligns fiber with anti-plastic policies, retailer recyclability targets, and brand decarbonization roadmaps that collectively reinforce fiber’s share leadership.

United States: Driving Fiber Packaging Growth Through Automation and Sustainable Solutions

The U.S. fiber packaging market is witnessing significant expansion driven by sustainable solutions and technological advancements. Companies like Huhtamaki North America have introduced molded fiber shells for egg packaging, reflecting strong consumer demand and corporate sustainability goals to reduce plastic and foam waste. Technological innovation, particularly AI-enabled high-speed sorting systems, is enhancing the quality and efficiency of fiber packaging production by accurately processing recycled paper and cardboard.

Regulatory pressure also serves as a key growth driver. State and municipal bans on expanded polystyrene (EPS) are pushing manufacturers to innovate with cost-effective, fiber-based alternatives. The booming e-commerce sector is another major catalyst, increasing the need for durable, lightweight, and protective fiber packaging to prevent product damage during shipping. This combination of sustainability, automation, and e-commerce growth positions the U.S. as a global leader in the fiber packaging market.

Germany: Leading Europe with Circular Economy and Innovative Fiber Technologies

Germany’s fiber packaging industry is at the forefront of Europe’s circular economy initiatives, driven by strong consumer preference for recyclable and reusable paper-based products. The country’s VerpackG (Packaging Act) sets ambitious recycling targets, encouraging the development of innovative packaging solutions. Technological advancements, such as ILLIG’s Dry Fiber technology, allow the production of deep-drawn fiber-based packaging with integrated barrier properties while reducing water and energy use compared to traditional wet-molded pulp.

German manufacturers are also investing in sustainable raw materials. For instance, PAPACKS has promoted industrial hemp as a circular, scalable alternative to wood-based pulp for fiber packaging production. This strategic focus on innovation, energy efficiency, and sustainable materials enables Germany to maintain leadership in high-quality fiber packaging for food and industrial applications.

China: Massive Production Capacity and Growing Domestic Demand

China is a global powerhouse in fiber packaging, with extensive production capacity supporting both domestic and international markets. As one of the world’s largest producers and consumers of paper and paperboard, China’s market growth is fueled by rising demand from the food and beverage sector and booming e-commerce. Urbanization and a growing middle class are further driving the need for efficient, sustainable fiber packaging solutions.

Governmental regulations are shaping the industry landscape. Strict environmental policies and import restrictions on recovered paper have led to industry consolidation, with larger players like Nine Dragons and Lee & Man expanding their market share. This consolidation ensures higher efficiency, improved production standards, and the ability to meet stringent domestic and international sustainability requirements.

India: “Make in India” and Rapid Retail Expansion Boost Fiber Packaging

India’s fiber packaging market is expanding rapidly, driven by the government’s “Make in India” initiative and progressive policies allowing 100% FDI. Foreign investments, such as SIG’s aseptic carton pack facility in Ahmedabad, are injecting capital and technology into the market, with planned investments of Rs. 880 crores between 2023-2025.

Rapid urbanization and the growth of modern retail chains are fueling demand for clean, hygienic, and protective packaging. Additionally, a focus on cost-effective, locally sourced materials like paperboard and molded pulp provides an environmentally friendly alternative to traditional plastics. Indian manufacturers are increasingly leveraging sustainable raw materials and local supply chains, strengthening the country’s competitive position in the global fiber packaging market.

Brazil: Agribusiness and Technological Investments Driving Market Expansion

The Brazilian fiber packaging industry is strongly influenced by its agribusiness and forest-based sectors, providing a robust raw material base of pulp and paper. Sustainability is a key driver, with companies like Klabin introducing EkoFlex, a flexible paper-based packaging material designed to replace traditional plastic packaging in industries such as food.

Technological investments are also shaping market growth. Sonoco has expanded its footprint by acquiring full stakes in its flexible packaging joint ventures, enabling it to meet increasing demand from confectionery, dairy, and pharmaceutical markets. This combination of sustainable materials and advanced packaging technologies positions Brazil as a leading regional player in fiber packaging.

Japan: High-Performance Materials and Strategic Sustainability Alliances

Japan’s fiber packaging market is characterized by a focus on high-performance paper-based solutions and advanced materials. Innovations such as Nippon Paper Industries’ SHIELDPLUS offer barrier properties comparable to plastic films, providing environmentally friendly alternatives for food and industrial packaging.

Strategic alliances are accelerating the move toward sustainability. Partnerships like that of Nippon Paper Industries and Mitsubishi Chemical Corporation have resulted in recyclable packaging materials using biodegradable resins, while Oji Holdings is developing cellulose nanofiber (CNF) films with superior oxygen barrier properties. These advancements extend product shelf life and reduce reliance on plastics, reinforcing Japan’s leadership in technologically advanced and sustainable fiber packaging solutions.

Fiber Packaging Market Report Scope

Fiber Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$335.8 Billion

|

|

Market Size (2034)

|

$453.7 Billion

|

|

Market Growth Rate

|

3.4%

|

|

Segments

|

By Raw Material (Virgin Fiber, Recycled Fiber, Other Fibers), By Packaging Type (Corrugated Boxes, Cartons & Folding Boxes, Molded Fiber Containers & Trays, Sacks & Bags, Other Packaging), By End-Use Industry (Food & Beverages, E-commerce, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Industrial, Other End-Users), By Product (Primary Packaging, Secondary Packaging, Tertiary Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, WestRock Company, Smurfit Kappa Group plc, DS Smith Plc, Mondi Group, Huhtamaki Oyj, Graphic Packaging Holding Company, Sonoco Products Company, Klabin S.A., Stora Enso Oyj, Rengo Co., Ltd., Amcor plc, BillerudKorsnäs AB, Nine Dragons Paper (Holdings) Limited, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fiber Packaging Market Segmentation

By Raw Material

- Virgin Fiber

- Recycled Fiber

- Other Fibers

By Packaging Type

- Corrugated Boxes

- Cartons & Folding Boxes

- Molded Fiber Containers & Trays

- Sacks & Bags

- Other Packaging

By End-Use Industry

- Food & Beverages

- E-commerce

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Industrial

- Other End-Users

By Product

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Fiber Packaging Market

- International Paper Company

- WestRock Company

- Smurfit Kappa Group plc

- DS Smith Plc

- Mondi Group

- Huhtamaki Oyj

- Graphic Packaging Holding Company

- Sonoco Products Company

- Klabin S.A.

- Stora Enso Oyj

- Rengo Co., Ltd.

- Amcor plc

- BillerudKorsnäs AB

- Nine Dragons Paper (Holdings) Limited

- Greif, Inc.

*List not Exhaustive

Research Coverage

This report investigates the evolving dynamics of the global fiber packaging market, highlighting key breakthroughs in sustainable packaging solutions, barrier technologies, and circular economy integration. USDAnalytics’ analysis reviews strategic mergers, facility expansions, and technology-driven innovations that are redefining competitive landscapes for industry professionals. The report highlights recent developments, including advancements in dry molded fiber systems, bio-based barrier coatings, and smart supply chain integrations, demonstrating how fiber packaging is increasingly replacing plastics across food, e-commerce, and industrial applications. By providing detailed insights into domestic and international market trends, regulatory frameworks, and high-value applications, this report is an essential resource for manufacturers, investors, and supply chain stakeholders seeking to navigate growth opportunities, sustainability compliance, and technology adoption. Comprehensive company profiling, market share evaluation, and trend mapping ensure actionable intelligence for decision-makers aiming to capitalize on fiber packaging’s expanding footprint while aligning with global ESG and recyclability mandates.

Scope Highlights:

- Segmentation: By Raw Material (Virgin Fiber, Recycled Fiber, Other Fibers), By Packaging Type (Corrugated Boxes, Cartons & Folding Boxes, Molded Fiber Containers & Trays, Sacks & Bags, Other Packaging), By End-Use Industry (Food & Beverages, E-commerce, Personal Care & Cosmetics, Healthcare & Pharmaceuticals, Industrial, Other End-Users), By Product (Primary Packaging, Secondary Packaging, Tertiary Packaging)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Detailed analysis and profiles of 15+ companies including International Paper Company, WestRock Company, Smurfit Kappa Group plc, DS Smith Plc, Mondi Group, Huhtamaki Oyj, and others

Methodology

This fiber packaging market report is built on a robust multi-step research methodology combining primary and secondary sources to ensure data accuracy and actionable insights. The analysis integrates interviews with industry experts, corporate filings, investor presentations, and on-ground intelligence to map competitive dynamics, technological advancements, and market opportunities. Secondary research leverages trade journals, regulatory filings, and sustainability reports to identify innovation trends in barrier coatings, molded fiber technologies, and circular economy adoption. Quantitative data modeling uses historical production, shipment, and consumption figures from 2021–2024 to project the market trajectory from 2025 to 2034, incorporating factors such as regional demand, raw material availability, regulatory frameworks, and global supply chain dynamics. USDAnalytics applies rigorous validation techniques, triangulating multiple data sources to deliver high-quality, professional-grade market intelligence suitable for strategic planning, investment evaluation, and operational decision-making.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.