Market Overview: Egg Packaging Market to Reach $8.6 Billion by 2034 with 4.5% CAGR

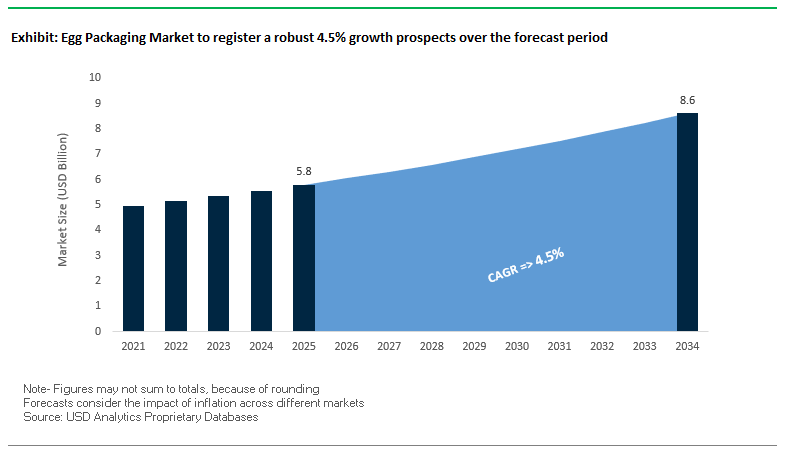

The global egg packaging market is projected to expand from $5.8 billion in 2025 to $8.6 billion by 2034, reflecting a steady CAGR of 4.5%. Egg packaging plays a critical role in ensuring food safety, product protection, and supply chain efficiency, while also serving as a medium for brand presentation and sustainability commitments. For industry professionals, the sector’s growth trajectory is being shaped by the dominance of molded fiber solutions, heightened consumer sustainability expectations, and the integration of logistics-driven design innovation.

Key Insights for Industry Stakeholders:

- Molded fiber dominance: Pulp-based cartons remain the leading material due to compostability, strength, and cost-effectiveness, with molded fiber accounting for the largest market share.

- Logistical optimization: Packaging designs are increasingly engineered for stackability, denesting efficiency, and dimensional stability, cutting losses during transit and maximizing truckload utilization.

- Shift to recycled content: Global producers are introducing 100% recycled molded fiber cartons in line with consumer demand and regulatory pressure for circular packaging.

- Transparency demand: PET and hybrid cartons with windows or full visibility are gaining traction, as consumers prioritize visual inspection of eggs before purchase.

Market Analysis: Strategic Acquisitions, Certifications, and Portfolio Restructuring (2024–2025)

The egg packaging industry is experiencing strong consolidation, sustainability certification milestones, and portfolio realignments that redefine competition across North America, Europe, and Asia.

In August 2025, Huhtamaki completed the acquisition of Zellwin Farms Company, a U.S. molded fiber specialist, strengthening its position in the North American egg packaging market. That same month, Huhtamaki celebrated 100 days of integration at its newly acquired Florida facility, underscoring its focus on operational efficiency, safety, and innovation in molded fiber production.

April 2025 saw Pactiv Evergreen’s acquisition by Novolex, creating a consolidated powerhouse in food and beverage packaging. This merger expands capabilities in sustainable molded fiber cartons while ensuring cost-efficient solutions for diverse customers. Earlier, in January 2025, Pactiv Evergreen earned the FSC®-Recycled certification for its egg packaging portfolio and showcased these certified products at the IPPE event in Atlanta, highlighting their 100% recycled content value proposition.

Strategic restructuring also continues to reshape competition. In December 2024, Sonoco sold its Thermoformed and Flexibles business to TOPPAN Holdings for $1.8 billion, focusing its investments on molded fiber and paper-based packaging. In the same month, Novolex and Pactiv Evergreen announced their $6.7 billion merger, further consolidating leadership in food and specialty packaging.

Other industry moves include Mauser Packaging Solutions’ April 2024 acquisition of Consolidated Container Company, a step that expands rigid packaging capabilities and may indirectly influence plastic-based egg packaging segments. Together, these developments demonstrate a market driven by acquisition-led growth, certification-led trust-building, and efficiency-led innovation.

Trends and Opportunities Reshaping the Egg Packaging Market

Accelerated Adoption of Molded Pulp Alternatives to Plastic and PS

The egg packaging market is undergoing a fundamental material transition as producers, retailers, and regulators push to eliminate single-use plastics and polystyrene (PS) clamshells. The European Union’s Single-Use Plastics Directive (SUPD) and Packaging and Packaging Waste Regulation (PPWR) have set strict mandates for recyclability, forcing rapid adoption of molded fiber cartons that are both compostable and recyclable. In the U.S., twelve states have already banned expanded polystyrene, which is further accelerating demand for sustainable alternatives. Companies like Huhtamaki are responding by launching 100% recycled molded fiber egg cartons, which provide a durable yet eco-friendly solution for large-scale egg producers. At the consumer level, demand for renewable and biodegradable packaging is growing sharply, as studies highlight strong preferences for plastic-free, plant-based materials. This consumer-led and regulation-driven momentum is positioning molded pulp as the new standard in egg packaging globally.

Integration of Smart and Traceability Features to Enhance Food Safety

Food safety and consumer trust are now strategic priorities in the egg packaging industry, leading to the rapid adoption of digital traceability features. In the European Union, Class A eggs already carry unique producer codes that identify the production method, origin country, and farm registration, providing transparency throughout the supply chain. This practice is spreading worldwide, with packaging increasingly incorporating QR codes, lot numbers, and even blockchain technology to enable consumers and regulators to trace eggs back to their source within seconds. Such systems prove critical in food safety incidents such as the 2018 U.S. recall of over 200 million eggs due to Salmonella contamination where rapid traceability can prevent widespread public health risks. A study on mobile QR-based systems confirmed that consumer access to digital traceability data significantly increases trust and confidence in food products. Egg packaging is therefore evolving from a passive container into a safety and transparency enabler, reshaping brand-consumer relationships.

Development of High-Performance, Water-Resistant Molded Fiber

One of the most promising opportunities in the egg packaging market lies in the development of water-resistant molded pulp cartons that maintain compostability while addressing the inherent weakness of fiber: moisture absorption. Refrigerated storage environments often expose cartons to condensation, which can compromise structural strength. To overcome this, researchers and suppliers are pioneering advanced bio-based coatings and additives. Academic findings show that applying wax or starch-based coatings can reduce moisture absorption by up to 35%, while polyamide-epichlorohydrin and cationic starch additives have demonstrated improved wet strength and durability. Additionally, optimizing fiber composition, particularly with long-chain softwood fibers, has been shown to enhance moisture resistance over hardwood-based pulp. Patent activity is accelerating, with new paraffin and rosin-based additives offering commercially viable, compostable moisture-barrier solutions. This innovation is creating a path toward fully functional, plastic-free egg cartons capable of competing with traditional PS and plastic clamshells in high-humidity environments.

Packaging Optimization for Automated and Robotic Distribution Systems

With supply chains becoming increasingly automated, there is a major opportunity to redesign egg packaging for compatibility with robotic and automated warehouse systems. Packaging used in robotic palletizing must meet exact dimensional tolerances and offer enhanced rigidity and surface properties for reliable robotic gripping. Robotics giant KUKA has introduced systems capable of palletizing up to 108,000 eggs per hour, showcasing how automation can dramatically improve efficiency in distribution centers. Precision handling is critical, as robots are being deployed to pick and place multiple carton formats without manual intervention. This shift means egg packaging must not only be protective and sustainable but also engineered for machine compatibility. Consistency and quality of cartons are essential, as automated palletizers depend on uniform packaging performance to reach speeds of 300 cases per hour. As robotic systems proliferate in food distribution, egg packaging engineered for automation is poised to become a strategic differentiator for producers and suppliers.

Competitive Landscape: Key Players Reshaping the Global Egg Packaging Industry

The global egg packaging sector is dominated by a mix of specialized molded fiber leaders, diversified packaging giants, and integrated machinery providers. Each player leverages sustainability, regional expansion, and product innovation to build market advantage.

Huhtamaki Oyj Strengthening North American Molded Fiber Leadership

Huhtamaki is a global leader in molded fiber egg cartons and filler flats, emphasizing renewable and recyclable solutions. In August 2025, the company acquired Zellwin Farms and integrated its Florida facility within 100 days, expanding its North American production footprint. With operations in 36 countries, Huhtamaki combines local delivery with global reach, ensuring secure supply for multinational egg producers while pursuing profitable, acquisition-led growth in the sustainable molded fiber segment.

Pactiv Evergreen Inc. FSC-Certified Molded Fiber and Foam Packaging

Pactiv Evergreen offers molded fiber and foam cartons, catering to both sustainability-focused and cost-sensitive buyers. In January 2025, it earned the FSC®-Recycled certification, affirming its use of 100% recycled content. Its $6.7 billion merger with Novolex in December 2024 consolidates its leadership in food packaging, enhancing material diversity and strengthening its market presence across North America. By balancing fiber and foam portfolios, Pactiv Evergreen addresses a wide spectrum of customer demands.

Tekni-Plex Material Science-Driven Diversification in Egg Packaging

Tekni-Plex leverages material science expertise to provide egg packaging solutions in molded fiber, rPET, and foam. Its cartons are engineered for denesting efficiency and compatibility with high-speed filling lines, making them ideal for large-scale producers. With eight manufacturing sites across the U.S. and Mexico, Tekni-Plex offers regional sourcing flexibility and tailored solutions to support sustainability targets, reinforcing its reputation as a versatile packaging partner.

Sonoco Products Company Portfolio Realignment to Focus on Paper-Based Packaging

Sonoco remains a significant player in molded pulp egg packaging, with a strong foundation in industrial paper and consumer packaging. Its December 2024 divestiture of its Thermoformed and Flexibles business for $1.8 billion streamlines its portfolio and allows greater focus on paper-based packaging solutions. Leveraging its integrated mill network, Sonoco ensures consistent lead times and lightweight carton designs that reduce logistics costs and emissions, supporting customer sustainability initiatives.

SANOVO TECHNOLOGY GROUP Integrated Machinery for Egg Packaging Efficiency

SANOVO, while not a direct carton manufacturer, plays a pivotal role with its egg handling and packaging machinery. Its solutions cover grading, robotic automation, and packing equipment, enabling producers to maximize efficiency and maintain biosecurity standards. SANOVO’s collaboration-driven model allows the co-development of customized solutions, including the launch of HIL-Medium and HIL-Large trays in India, tailored for local markets. This integration of machinery with packaging processes makes SANOVO a vital enabler of large-scale egg packaging operations.

Egg Packaging Market Share Insights

Egg Cartons and Trays Dominate Market Share by Product Type in Egg Packaging

In 2025, egg cartons hold 60% of the egg packaging market, making them the dominant product type, followed by trays with 30%, while boxes and other specialized formats contribute a smaller share. Egg cartons remain the retail standard, favored for consumer convenience, stackability, and branding opportunities in the competitive supermarket aisle. The shift from polystyrene to molded pulp reflects rising sustainability pressures, as retailers and consumers increasingly demand recyclable and compostable options. Trays, by contrast, underpin the industrial and foodservice supply chain, enabling cost-effective bulk handling for bakeries, restaurants, and processors. Although egg boxes and niche packaging formats are gaining traction in online grocery and specialty segments, their volumes remain limited compared to mainstream cartons and trays. This segmentation highlights the dual nature of the egg packaging market cartons serving consumer-facing retail visibility, and trays sustaining the high-volume B2B distribution backbone.

Retail Leads Market Share by End-Use Industry in Egg Packaging

By end-use, retail represents 55% of the egg packaging market in 2025, reinforcing its role as the largest and most brand-driven segment. Supermarket sales dictate packaging design, with cartons acting as key marketing vehicles to showcase sustainability claims, organic certifications, and free-range positioning. Foodservice and food processing, accounting for 40%, are heavily reliant on durable trays and bulk packaging optimized for logistics rather than aesthetics, reflecting the scale of commercial egg use in industrial baking and catering. Institutional users such as schools, hospitals, and correctional facilities also consume large volumes, with growing emphasis on cost efficiency and recycled-content mandates in line with public procurement policies. While smaller niches exist in farmers’ markets and specialty channels, the overall market share remains concentrated in the dual pillars of retail branding and bulk foodservice supply, together shaping demand for both sustainable materials and operational efficiency.

United States: Sustainable Molded Fiber and Smart Packaging Transform Egg Industry

The U.S. egg packaging market is undergoing a significant transformation, driven by consumer demand for sustainable and eco-friendly solutions. There is a clear shift from traditional plastic and foam cartons toward molded fiber and recycled paperboard packaging. Leading companies like Huhtamaki North America are rolling out new molded fiber shells tailored for U.S. egg producers. Innovation is also focused on incorporating post-consumer recycled (PCR) content, as seen in Tekni-Plex’s updated Dolco ProPlus carton, which includes 25% PCR foam polystyrene, supporting the principles of the circular economy.

In addition, the integration of smart packaging technologies is enhancing supply chain visibility. RFID tags and QR codes on cartons allow for real-time traceability, improving food safety compliance and enabling consumers to access detailed product information. The rise of e-commerce and retail-focused packaging is further driving demand for durable, protective cartons designed to prevent egg breakage during shipping, highlighting the intersection of sustainability, technology, and logistics efficiency in the U.S. market.

Germany: Circular Economy and Automation Leading Egg Packaging Innovation

Germany’s egg packaging market is a frontrunner in Europe’s circular economy, emphasizing recyclable and reusable materials. Corrugated cardboard and other paper-based solutions dominate, with innovations aimed at improving functionality and sustainability. Companies like Eggbox GmbH have introduced 100% recyclable corrugated cardboard cartons using natural starch glue and mineral oil-free inks, catering to both environmental and regulatory standards.

The market also emphasizes automation and robotics to streamline operations. German companies, including AKON Robotics, provide automated palletizing and depalletizing solutions for egg trays, increasing production efficiency while reducing labor costs. This combination of sustainable packaging, high-tech automation, and regulatory compliance ensures Germany remains a leader in innovative and eco-friendly egg packaging solutions.

China: High-Volume Production and Regulatory Compliance Drive Market Growth

China’s egg packaging market is a global production powerhouse, catering to both its massive domestic consumption and international export demand. The country’s focus on high-quality and protective packaging is driven by the need to prevent egg breakage during transport. Local producers are investing in robust carton designs to ensure durability and product integrity across extensive distribution networks.

Governmental regulations on food safety are modernizing labeling and packaging standards, including stricter allergen disclosure and clear expiry date formats. These regulatory developments are pushing the market toward transparent, compliant, and reliable egg packaging, enhancing both domestic and export competitiveness.

India: Urbanization and Policy Support Fuel Growth in Egg Packaging

India’s egg packaging market is growing rapidly due to urbanization, a rising middle class, and modern retail expansion. There is strong demand for hygienic, well-packaged eggs, supporting both retail and processed egg product sectors. The Production Linked Incentive Scheme for the Food Processing Industry (PLISFPI) further encourages investment in packaging infrastructure, enabling higher efficiency and quality.

The market is increasingly focused on cost-effective and locally sourced materials like paperboard and molded pulp, which provide affordable, sustainable, and environmentally friendly solutions. These developments are positioning India as a rapidly emerging market for innovative and eco-conscious egg packaging.

Brazil: Innovative Designs and Alternative Raw Materials Reduce Egg Breakage

Brazil’s egg packaging market is addressing the critical challenge of egg breakage during long-distance transport. Huhtamaki Brazil has developed an innovative tray design that reduces breakage by 50%, demonstrating a strong commitment to logistics efficiency and product safety.

R&D efforts are also exploring alternative raw materials beyond recycled paper, including sugarcane, coconut shells, and bamboo, creating humidity-resistant and stronger fiber trays. These innovations combine sustainability with performance, positioning Brazil as a regional leader in advanced and eco-friendly egg packaging solutions.

Japan: Precision Automation and Raw Egg Safety Define the Market

Japan’s egg packaging industry is characterized by high-precision automation, ensuring superior quality control and product safety. Advanced systems clean, inspect, and sort eggs for size, cracks, and blood spots before gently placing them into cartons via high-speed robotic machines, minimizing breakage.

Given the cultural practice of consuming raw eggs, the market prioritizes rigorous safety standards. Packaging and inspection technologies detect even minor imperfections, maintaining consumer safety. The integration of automation, quality assurance, and hygienic packaging makes Japan a global leader in high-quality and safe egg packaging solutions.

Egg Packaging Market Report Scope

Egg Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.8 Billion

|

|

Market Size (2034)

|

$8.6 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Material Type (Paper, Plastic, Other Materials), By Product Type (Egg Cartons, Egg Trays, Egg Boxes, Other Packaging), By End-Use Industry (Retail, Foodservice & Food Processing, Institutional, Other End-Users), By Pack Size (6 Eggs, 12 Eggs, 18 Eggs, 30 Eggs, Bulk Packs)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamaki Oyj, International Paper Company, Pactiv Evergreen Inc., Hartmann A/S, Sonoco Products Company, Tekni-Plex, Inc., DS Smith Plc, MyPak Packaging, Rengo Co., Ltd., Sealed Air Corporation, BillerudKorsnäs AB, Dispak, Visy Industries, Cascades, Inc., Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Egg Packaging Market Segmentation

By Material Type

- Paper

- Plastic

- Other Materials

By Product Type

- Egg Cartons

- Egg Trays

- Egg Boxes

- Other Packaging

By End-Use Industry

- Retail

- Foodservice & Food Processing

- Institutional

- Other End-Users

By Pack Size

- 6 Eggs

- 12 Eggs

- 18 Eggs

- 30 Eggs

- Bulk Packs

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Egg Packaging Market

- Huhtamaki Oyj

- International Paper Company

- Pactiv Evergreen Inc.

- Hartmann A/S

- Sonoco Products Company

- Tekni-Plex, Inc.

- DS Smith Plc

- MyPak Packaging

- Rengo Co., Ltd.

- Sealed Air Corporation

- BillerudKorsnäs AB

- Dispak

- Visy Industries

- Cascades, Inc.

- Greif, Inc.

*List not Exhaustive

Research Coverage

This report investigates the global egg packaging market, analyzing key innovations, material transitions, and supply chain strategies that are redefining food safety, sustainability, and operational efficiency. USDAnalytics’ analysis reviews breakthroughs in molded fiber technology, water-resistant coatings, smart traceability solutions, and automation-compatible packaging designs, highlighting their role in enhancing egg protection, brand visibility, and consumer trust. This report is an essential resource for packaging engineers, supply chain managers, and sustainability executives seeking actionable insights into regulatory compliance, circular economy adoption, and logistics optimization. It also examines strategic mergers, acquisitions, and certification achievements that influence competitive dynamics, while evaluating high-performance designs tailored for retail, foodservice, and institutional distribution. By assessing historical trends from 2021 to 2024 and providing forecasts through 2034, this study delivers a comprehensive understanding of market expansion, material adoption, and regional growth opportunities, enabling stakeholders to anticipate evolving consumer expectations and regulatory pressures. Furthermore, the research highlights portfolio innovations, automation readiness, and eco-friendly packaging solutions across leading companies, ensuring professionals can navigate the market’s shift from polystyrene and plastics to recyclable, compostable, and technologically advanced formats.

Scope Highlights:

- Segmentation: By Material Type (Paper, Plastic, Other Materials); By Product Type (Egg Cartons, Egg Trays, Egg Boxes, Other Packaging); By End-Use Industry (Retail, Foodservice & Food Processing, Institutional, Other End-Users); By Pack Size (6 Eggs, 12 Eggs, 18 Eggs, 30 Eggs, Bulk Packs)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies Covered: In-depth analysis and profiles of 15+ companies, including Huhtamaki Oyj, International Paper Company, Pactiv Evergreen Inc., Hartmann A/S, Sonoco Products Company, Tekni-Plex, Inc., DS Smith Plc, MyPak Packaging, Rengo Co., Ltd., Sealed Air Corporation, BillerudKorsnäs AB, Dispak, Visy Industries, Cascades, Inc., and Greif, Inc.

Methodology

This research employs a combination of primary and secondary approaches to deliver accurate, actionable insights into the egg packaging market. Primary research involves interviews with packaging engineers, R&D specialists, supply chain executives, and sustainability managers across leading companies to validate trends, material adoption, and automation requirements. Secondary research integrates company reports, regulatory filings, patent databases, trade publications, and scientific studies to track innovations in molded fiber, water-resistant coatings, recycled content, and digital traceability. Market sizing and forecasts are calculated using a blend of bottom-up and top-down methods, accounting for production capacity, regulatory mandates, consumer trends, and sustainability adoption. Competitive benchmarking examines mergers, acquisitions, certifications, and technology deployment, while regional analysis considers economic drivers, policy frameworks, and consumption patterns. USDAnalytics cross-validates data to ensure reliability, providing professionals with a thorough understanding of current market conditions and future opportunities.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.