Plastic-Based Egg Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Plastic-Based Egg Packaging Market Set to Grow to $6.7 Billion by 2034 Driven by Durability and Sustainability

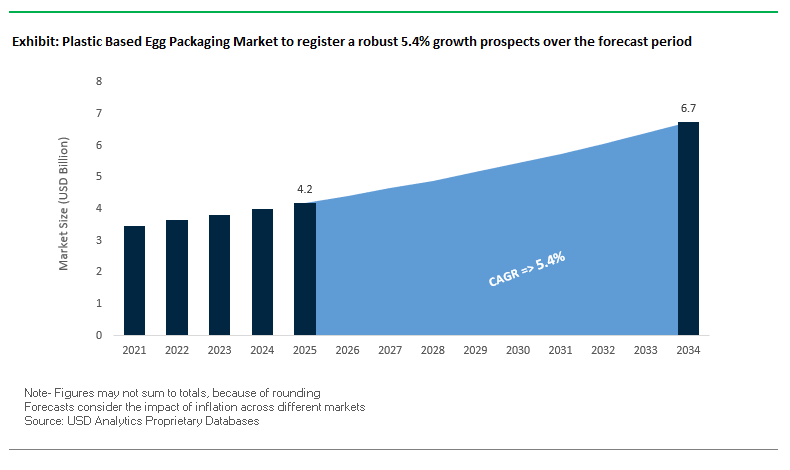

The global plastic-based egg packaging market is projected to grow from $4.2 billion in 2025 to $6.7 billion by 2034, representing a CAGR of 5.4%. The market growth is underpinned by retail sector demand, consumer preferences for transparency, and innovations in sustainable materials. Plastic egg cartons, particularly clamshells, provide superior shock absorption, moisture barrier properties, and durability, ensuring eggs reach consumers intact.

Key Insights for industry professionals and buyers:

- Durability and Protection Drive Adoption: Plastic clamshells are widely used due to their shock absorption and moisture resistance, critical for transport and retail display.

- Shift Towards Recycled Content: Use of post-consumer recycled PET (rPET) supports circular economy initiatives and reduces environmental impact.

- Consumer Preference for Transparency: Clear PET packaging enables visual inspection, building trust and influencing purchasing decisions.

- Standardization Supports Retail Efficiency: Supermarkets favor stackable, standardized designs, boosting supply chain efficiency and shelf appeal.

- Sustainability Trends Influence Product Design: Manufacturers are increasingly incorporating eco-friendly materials and innovative packaging designs to align with consumer and regulatory expectations.

Market Analysis: Plastic-Based Egg Packaging Industry Experiences Sustainability-Driven Innovation and Competitive Pressures

The plastic-based egg packaging market has seen a surge in sustainability-focused developments, industry collaborations, and competitive innovations. In September 2025, The Times of India highlighted the growing trend of biodegradable and plant-based alternatives, influencing strategic priorities for plastic-based egg packaging manufacturers. In August 2025, Mondi ramped up production of FunctionalBarrier Paper Ultimate, a high-barrier paper-based alternative for eggs and other food products, providing an indirect competitive pressure to traditional plastics.

Corporate mergers and global expansion are shaping the market dynamics. In July 2025, Smurfit Kappa and WestRock merged to form Smurfit WestRock, creating a global paper-based packaging leader and intensifying competition for conventional plastic egg packaging solutions. Simultaneously, Fortis X launched Africa’s first biodegradable sugarcane-based packaging in July 2025, and Graphic Packaging International introduced its PaperSeal® Pressed MAP Tray in June 2025, reducing plastic use by up to 85% in food applications.

Sustainability and technological innovation continue to be central to market evolution. Nfinite Nanotechnology partnered with Amcor in April 2025 to enhance oxygen barrier performance in recyclable and compostable packaging. Leading brands, including Pete & Gerry’s Organic Eggs in February 2025, adopted 100% recycled PET cartons as environmentally preferable alternatives. In January 2025, La Foundary developed mushroom mycelium-based sustainable packaging, potentially applicable for eggs, indicating the sector’s openness to novel eco-friendly materials.

Emerging Trends and Strategic Opportunities in the Plastic-Based Egg Packaging Market

Accelerated Material Transition to Recycled PET (rPET) and Polypropylene (PP)

The plastic-based egg packaging market is undergoing a decisive shift toward recycled PET (rPET) and polypropylene (PP), driven by regulatory mandates, corporate sustainability pledges, and technological investments in recycling. India’s Plastic Waste Management Rules amendment, effective April 1, 2025, requires 30% recycled content in rigid plastic packaging, directly influencing egg cartons that fall under this category. To support this mandate, multiple companies have secured certification to produce food-grade rPET resin for safe use in food-contact packaging, ensuring reliability of supply. Corporate sustainability strategies are reinforcing this trend. Ovotherm, for instance, produces egg cartons from 100% rPET, achieving full recyclability and lowering carbon emissions by 40% compared to pulp alternatives, according to third-party life-cycle assessments. Simultaneously, Plastics Europe is spearheading investments in chemical recycling, with funding expected to rise from €2.6 billion in 2025 to €8 billion in 2030, focusing on polyolefins like PP. These investments are crucial for generating food-grade recycled PP, unlocking scalability for egg packaging manufacturers. Collectively, these developments reflect a global pivot toward recycled and recyclable plastic-based formats, positioning rPET and PP as the dominant materials of the future.

Integration of Enhanced Functional and Smart Features

Beyond sustainability, plastic egg packaging is evolving into a functional and intelligent solution for reducing food waste and improving consumer transparency. Modified Atmosphere Packaging (MAP) has been proven to extend the shelf life of eggs significantly. A study published in ResearchGate demonstrated that eggs stored in a 100% carbon dioxide atmosphere preserved albumen quality, measured by the Haugh unit, far better than eggs stored under normal air conditions. By mitigating spoilage, MAP offers a direct response to one of the industry’s most pressing challenges. At the same time, digital technologies are being embedded into egg cartons to enhance traceability and consumer trust. QR codes and NFC tags now provide customers with instant access to information on farm practices, animal welfare standards, and freshness indicators. Intelligent packaging technologies such as time–temperature indicators and biosensors further allow real-time monitoring of product quality throughout the cold chain. By merging smart features with packaging, manufacturers are creating a dual value proposition: extended shelf life for retailers and actionable transparency for consumers.

Development of Monomaterial and Easily Recyclable Designs

A major opportunity for the plastic-based egg packaging market lies in the redesign of traditional cartons into monomaterial formats that simplify recycling and improve consumer compliance. Historically, multi-material designs—such as polystyrene (PS) bases with PET labels—have created barriers to recyclability due to material incompatibility. The next wave of innovation involves developing egg cartons made entirely from PET, including integrated labeling, ensuring seamless compatibility with existing PET recycling streams. A complementary opportunity exists with polypropylene: a 2025 study by Closed Loop Partners highlighted that high quantities of food-grade PP are already captured by material recovery facilities through AI-powered sorting. By producing monomaterial PP cartons labeled clearly as “PP – Recyclable,” manufacturers can encourage consumer participation and optimize recovery rates. Simplified recycling systems, reinforced by clear consumer instructions, will not only increase recycling volumes but also improve brand reputation in markets where regulatory pressure and consumer awareness are at an all-time high.

Advanced Recycling and Closed-Loop System Partnerships

The establishment of closed-loop partnerships represents another transformative opportunity for the plastic-based egg packaging industry. Collaboration between food producers, waste management companies, and advanced recyclers can enable discarded cartons to be collected, processed, and chemically recycled into high-quality, food-grade resins. These resins can then be reintegrated into new egg cartons, creating a truly circular model that reduces reliance on virgin plastics. For instance, SABIC’s joint venture with Plastic Energy has already demonstrated the viability of such systems, producing TACOIL—a pyrolysis oil derived from post-consumer waste—as a direct substitute for virgin feedstock. Plastics Europe’s €8 billion commitment to chemical recycling capacity expansion by 2030 further underscores the scalability of this model. By embracing chemical recycling, the egg packaging industry can overcome limitations of traditional mechanical processes, ensuring that even contaminated or mixed plastic waste streams can be recovered. This transition not only supports compliance with food-contact safety standards but also enables the industry to meet EU and global 2030 recyclability targets while advancing corporate ESG goals.

Competitive Landscape: Global Plastic-Based Egg Packaging Market is Dominated by Companies Innovating in Sustainability and High-Performance Solutions

The plastic-based egg packaging market is led by companies investing in sustainability, product protection, and innovative packaging formats, providing both conventional and eco-conscious options.

Huhtamaki Oyj: Leading the Industry with Integrated Plastic and Sustainable Egg Packaging Solutions

Huhtamaki offers high-quality plastic and molded fiber egg cartons with advanced denesting and closing features for streamlined egg packing. The company aims to make all packaging recyclable or reusable by 2030. Its focus on product integrity, efficiency, and sustainability positions it as a leading choice for retailers seeking durable, environmentally responsible packaging solutions.

Sonoco Products Company: Delivering High-Strength and Moisture-Resistant Plastic Egg Cartons

Sonoco provides rigid plastic egg cartons and trays for premium and multi-egg formats. The company invests in lightweight, high-barrier designs that extend shelf life while reducing material usage. Sonoco’s strategy emphasizes value-added, sustainable packaging solutions that enhance brand appeal and meet growing consumer demand for eco-friendly options.

Pactiv Evergreen Inc.: Driving Sustainable Packaging Innovation with Biodegradable Egg Cartons

Pactiv Evergreen focuses on biodegradable and high-barrier egg packaging solutions. Recent initiatives include the launch of biodegradable egg cartons, reducing plastic usage. The company is committed to providing innovative, convenient, and sustainable food packaging, helping customers achieve operational efficiency and sustainability goals.

Sealed Air Corporation: Protecting Product Integrity Through Superior Cushioning Plastic Egg Trays

Sealed Air specializes in plastic-based egg trays made from PET or EPS, offering enhanced cushioning and moisture barrier properties. The company’s solutions are designed to reduce product damage and waste, supporting sustainability initiatives and ensuring eggs remain intact from production to retail.

International Paper Company: Expanding Sustainable Egg Packaging Through Fiber-Based and Premium Solutions

International Paper provides molded fiber and paperboard egg cartons, integrating stackable designs and premium printing to appeal to environmentally conscious consumers. The company focuses on renewable, recyclable, and sustainable packaging, strengthening its competitive position against conventional plastic-based egg cartons.

Plastic Based Egg Packaging Market Share Insights, 2025-2034

Cartons Dominate Market Share by Packaging Type in the Plastic-Based Egg Packaging Industry

Cartons hold a commanding 55% share of the plastic-based egg packaging industry, solidifying their position as the global retail standard. Plastic cartons, commonly PET or PS, deliver the best balance between protection, branding, and visibility, outperforming pulp alternatives in durability and consumer appeal. Their resealable design, compatibility with automated packing lines, and ability to showcase freshness make them the format of choice for supermarkets worldwide. Plastic trays capture a significant secondary share, primarily serving food service and institutional customers, where durability, stackability, and transport efficiency outweigh retail branding needs. Clamshell packaging plays a premium role, used by free-range and organic egg producers to differentiate products with 360-degree visibility and premium presentation. Bulk packaging, though a smaller segment, is indispensable in upstream supply chains, particularly for transport from farms to grading stations, where efficiency and reusability drive adoption. The segmentation clearly shows how cartons drive consumer-facing retail dominance, while trays and bulk systems underpin food service and supply chain logistics.

Chicken Eggs Overwhelmingly Drive Market Share by Application in the Plastic-Based Egg Packaging Industry

The packaging industry for eggs is overwhelmingly defined by chicken eggs, which account for 92% of demand, reflecting global production and consumption dominance. Plastic packaging solutions for chicken eggs are optimized for standardized sizes, ensuring efficiency across automated filling, transportation, and retail distribution. Duck eggs maintain a small but regionally significant niche, particularly in Asia, where their larger size requires custom cavities and specialized materials to ensure safe transport. Quail eggs represent a premium delicacy segment, commanding specialized miniature cartons and trays designed for fragile handling and upscale presentation, often positioning the packaging as a luxury element of the product. Other bird eggs, including turkey, goose, and ostrich, represent a negligible portion of the market, typically relying on custom or hand-packed solutions due to their low commercial volume. The overwhelming dominance of chicken eggs demonstrates how the egg packaging market is structurally aligned with global poultry production, with specialized packaging niches emerging only in regional or premium value chains.

United States Plastic Based Egg Packaging Market Shaped by FDA Rules and State-Level Bans

The United States plastic-based egg packaging market is evolving under the dual influence of federal food safety standards and state-driven sustainability laws. The Food and Drug Administration (FDA) and the USDA enforce strict requirements for food-contact packaging, mandating contamination-free materials in plastic egg cartons to maintain supply chain integrity. These regulations have made compliance and material safety a central driver of packaging innovation. A notable development is Tekni-Plex’s 25% PCR foam polystyrene egg carton, designed to cut environmental impact while adhering to federal standards.

Sustainability remains a key pressure point. State-level policies such as Washington’s ESHB 1293 and California’s 2024 single-use carryout bag ban, effective January 2026, will restrict certain plastic food packaging, creating regulatory headwinds for conventional plastic egg cartons. At the same time, the rise of e-commerce grocery delivery is driving demand for durable, protective, and tamper-proof packaging capable of withstanding shipping. The U.S. market is thus pivoting toward recycled-content plastic cartons and bio-based alternatives, while also emphasizing clear recyclability labeling and certification, to meet consumer expectations for transparency and eco-friendly solutions.

European Union Plastic Based Egg Packaging Market Driven by PPWR and Recycling Targets

The European Union plastic based egg packaging market is primarily influenced by the Packaging and Packaging Waste Regulation (PPWR), effective from February 2025, which establishes stricter recyclability benchmarks. From August 2026, food packaging containing PFAS above threshold levels will be banned, directly impacting plastic egg cartons that historically relied on fluorinated coatings for grease and moisture resistance. By 2030, only packaging achieving at least 70% recyclability will qualify as recyclable, forcing companies to adopt mono-material and design-for-recycling strategies.

In addition, harmonized recycling labels, mandatory by 2028, will transform consumer communication on egg carton sustainability. While many stakeholders, including the Alliance for Sustainable Packaging, are calling for a temporary “pause” in PPWR due to cost implications, leading manufacturers are accelerating innovations. Companies are already developing clear-label, single-polymer PET cartons that comply with EU recycling streams. With these combined policies, Europe is at the forefront of transitioning egg packaging toward high recyclability, reduced PFAS exposure, and standardized consumer labeling.

China Plastic Based Egg Packaging Market Transitioning to Green Packaging Standards

The China plastic based egg packaging market is shaped by a blend of eco-regulation and circular economy initiatives. The June 2025 packaging regulation directly targets delivery-related waste by promoting recycled materials and restricting excessive wrapping. Enforcement by the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) emphasizes strict reductions in non-compliant plastics, while pushing manufacturers toward biodegradable and recyclable options.

Local innovation is strong, with companies like Jingxing Packaging Materials Co. adopting closed-loop systems that recycle scrap materials into new packaging. Over 100 companies have received “green product” certification, highlighting the country’s momentum toward eco-compliance. Further shaping the market is China’s “positive list” system for food-contact materials, alongside the GB 4806.15-2024 adhesives standard, which set stricter criteria for plastic food packaging. Together, these measures are positioning China as a fast-growing market for sustainable, compliant plastic egg cartons that align with both regulatory and consumer expectations.

India Plastic Based Egg Packaging Market Supported by EPR and Bioplastic Innovation

The India plastic based egg packaging market is driven by the Plastic Waste Management Rules (2016, amended 2022), which emphasize Extended Producer Responsibility (EPR). This framework compels manufacturers and brand owners to collect, recycle, and manage waste from plastic egg cartons, ensuring accountability throughout the lifecycle. At the same time, the Swachh Bharat Abhiyan (Clean India Mission) is driving broader consumer awareness on waste segregation and clean packaging use.

Innovation and investment are gaining momentum. Startups like Dharaksha Ecosolutions, which produces packaging from agricultural waste, reflect the shift toward biodegradable and plant-based alternatives. Meanwhile, the FSSAI is consulting stakeholders on food-grade sustainable packaging, encouraging the use of compostable plastics in the food sector. With government support for domestic R&D and manufacturing, India is rapidly emerging as a hub for eco-friendly plastic alternatives in egg packaging, supported by its circular economy agenda.

United Kingdom Plastic Based Egg Packaging Market Influenced by Plastic Packaging Tax and Recycling Goals

The United Kingdom plastic based egg packaging market is driven by the Plastic Packaging Tax (PPT), introduced in April 2022, which applies to all plastic packaging with less than 30% recycled content. By the 2024–2025 fiscal year, HMRC data revealed 51% compliance, indicating strong market adoption of recycled-content materials. This economic incentive has pushed carton manufacturers toward PCR-based plastics and single-material designs that are easier to recycle.

Research is also underway into mono-material and high-barrier recyclable packaging to reduce reliance on complex laminates. Although the UK has exited EU frameworks such as the Falsified Medicines Directive (FMD), it continues to prioritize anti-counterfeiting measures and traceability technologies across all packaging categories, including food-contact plastics. Combined with growing consumer demand for sustainable grocery packaging, the UK market is accelerating its transition toward circular, recyclable egg packaging solutions.

Japan Plastic Based Egg Packaging Market Evolving with Positive List Regulations and Circular Economy Goals

The Japan plastic based egg packaging market is advancing under newly implemented positive list regulations for food-contact materials, ensuring that only approved synthetic materials are used in plastic cartons. This policy is shaping material selection and innovation, with companies exploring eco-friendly, high-performance polymers that meet stringent safety standards.

Japan’s strong push for a circular economy and waste reduction is driving both government and industry-backed initiatives for sustainable plastic alternatives. The expansion of e-commerce and home delivery services is adding further demand for robust, protective, and recyclable egg packaging solutions. With consumer interest rising in eco-friendly grocery packaging, Japanese manufacturers are developing next-generation recyclable and compostable plastic cartons that balance food safety, durability, and sustainability.

Plastic Based Egg Packaging Market Report Scope

Plastic Based Egg Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.2 Billion

|

|

Market Size (2034)

|

$6.7 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (PET, PS, PE, PVC, PLA & other Bio-based plastics, Recycled Content Plastics, Others), By Packaging Type (Cartons, Trays, Clamshells, Bulk Packaging), By End-Use (Retail, Food Service, Institutional, E-commerce), By Application (Chicken Eggs, Duck Eggs, Quail Eggs, Other Bird Eggs)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Huhtamaki Oyj, Pactiv Evergreen Inc., Smurfit Kappa Group plc, DS Smith Plc, Mondi plc, WestRock Company, Sonoco Products Company, Alffan Plastic Co. Ltd., Tekni-Plex, Inc., Genpak LLC, Winpak Ltd., CKF Inc., Placon Corporation, The PFM Group, FPC International Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Based Egg Packaging Market Segmentation

By Material

- PET

- PS

- PE

- PVC

- PLA & other Bio-based plastics

- Recycled Content Plastics

- Others

By Packaging Type

- Cartons

- Trays

- Clamshells

- Bulk Packaging

By End-Use

- Retail

- Food Service

- Institutional

- E-commerce

By Application

- Chicken Eggs

- Duck Eggs

- Quail Eggs

- Other Bird Eggs

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Based Egg Packaging Market

- Huhtamaki Oyj

- Pactiv Evergreen Inc.

- Smurfit Kappa Group plc

- DS Smith Plc

- Mondi plc

- WestRock Company

- Sonoco Products Company

- Alffan Plastic Co. Ltd.

- Tekni-Plex, Inc.

- Genpak LLC

- Winpak Ltd.

- CKF Inc.

- Placon Corporation

- The PFM Group

- FPC International Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and multi-faceted research methodology to deliver actionable insights into the Plastic-Based Egg Packaging Market. Our approach integrates primary research through interviews with key stakeholders, including packaging manufacturers, retailers, foodservice operators, and sustainability experts, alongside secondary research from regulatory filings, industry reports, corporate disclosures, and patent databases. Market sizing, CAGR analysis, and growth projections are conducted using both top-down and bottom-up modeling, segmented by material (PET, PS, PE, PVC, PLA, recycled content), packaging type (cartons, trays, clamshells, bulk), end-use (retail, food service, institutional, e-commerce), and egg type (chicken, duck, quail, others). We assess emerging trends such as recycled PET adoption, monomaterial designs, smart and functional packaging, and chemical recycling initiatives, alongside regional regulatory frameworks including the EU PPWR, UK Plastic Packaging Tax, India’s EPR rules, China’s green packaging mandates, and U.S. FDA and state-level sustainability legislation. Competitive benchmarking evaluates mergers, collaborations, and sustainability-driven innovations by leading companies such as Huhtamaki, Pactiv Evergreen, Sonoco, and Sealed Air, providing professionals with a detailed understanding of market dynamics, growth drivers, sustainability initiatives, and strategic opportunities shaping the global plastic-based egg packaging industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.