Global Clamshell Packaging Market Overview: Sustainability, Thermoforming Efficiency, and Foodservice Demand

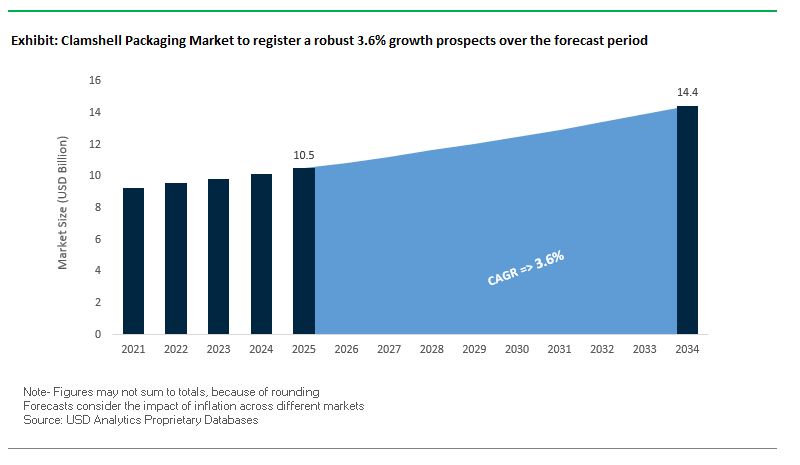

The clamshell packaging market is projected to grow from USD 10.5 billion in 2025 to USD 14.4 billion by 2034, reflecting a CAGR of 3.6%. This steady expansion is being driven by the material’s ability to balance product protection, consumer visibility, and sustainable innovation, making it an essential solution for foodservice, retail, and healthcare sectors. For industry professionals, the market is shaped by four core factors: regulatory push for recyclable content, advances in thermoforming, strong foodservice demand, and retail security/display requirements.

Clamshell packaging is no longer a commodity but a strategic enabler for circular economy goals, as most manufacturers are scaling 75%+ PCR PET integration into their products. With thermoforming enabling complex, customized designs, clamshells deliver fast production cycles and accelerate speed-to-market for new SKUs. The foodservice segment dominates consumption, particularly for fresh produce, ready meals, and grab-and-go offerings, where tamper-evidence and leak resistance are vital. Meanwhile, retail clamshells enhance on-shelf appeal by combining product visibility with security features such as built-in hanger holes and reinforced hinges.

Key Insights for packaging professionals and buyers

- PCR Content Adoption: Over 75% recycled PET integration aligns with brand ESG commitments and EU/US recyclability targets.

- Thermoforming Innovation: Advanced tooling allows customized shapes and reduced lead times, enhancing agility in retail and foodservice launches.

- Foodservice Dominance: High demand in prepared meals, produce, and grab-and-go items, where hygiene and visibility are critical.

- Security & Merchandising: Tamper-evident closures and hanger holes remain standard for retail theft reduction and visual appeal.

Market Analysis: Strategic Partnerships, Recycling Expansion, and Sustainability Wins

The past year has been transformative for the global clamshell packaging market, with sustainability and supply chain resilience taking center stage. In September 2025, Sabert Corporation Europe partnered with Flexeserve to launch the PulpUltra range, including a clamshell burger box made from 95% plant-based fibers PFAS-free and grease/moisture resistant. This reflects the sharp pivot toward plant-based and compostable packaging in foodservice. Similarly, in August 2025, Amcor expanded its recycling infrastructure in the UK and launched a new container with 50% recycled content in collaboration with Flügger, reinforcing its closed-loop strategy.

Strategic consolidations are reshaping competition. The Smurfit Kappa–WestRock merger completed in June 2025 created Smurfit WestRock, a global packaging giant influencing paper-based alternatives and shifting competitive benchmarks for plastic clamshells. Earlier, in April 2025, Sabert Corporation Europe acquired Colpac, a move that expanded its paperboard clamshell portfolio across Europe. At the same time, clamshell adoption in healthcare and medical devices is rising, with Brentwood’s February 2025 Product Development Lab investment aimed at faster R&D cycles and customer-specific designs.

Industry forums also underscored macro influences. The Mumbai Global Packaging Summit in July 2025 drew 2,200 delegates, highlighting PCR integration, trade policy, and supply chain localization. Buyers are also pressing for shorter lead times and near-shoring of thermoforming capacity, as reported in May 2025, emphasizing risk mitigation after recent global disruptions. Reports from March 2025 confirm growing demand for high-clarity recyclable PET clamshells, particularly in e-commerce, where tamper evidence + visibility are emerging as baseline requirements.

Trends and Opportunities Reshaping the Clamshell Packaging Market

Mandated Shift to Recyclable Monomaterials and Post-Consumer Recycled (PCR) Content

The clamshell packaging market is undergoing a regulatory and commercial transformation as policymakers, retailers, and brands converge on stricter sustainability mandates. The EU Packaging and Packaging Waste Regulation (PPWR), slated for full enforcement by 2030, compels manufacturers to adopt recyclable formats and integrate PCR content, or else face higher Extended Producer Responsibility (EPR) fees. Similarly, California’s plastics legislation in the U.S. and India’s Plastic Waste Management Rules (2024) require packaging producers to achieve ambitious PCR inclusion rates, further tightening the market’s compliance landscape.

Retailers are reinforcing these changes by mandating sustainable packaging from their supply chains. Walmart, Target, and other global retailers now demand packaging solutions that reduce virgin plastic dependency, incentivizing suppliers to pivot toward recyclable PET or PP clamshells. This shift is backed by supplier-side innovation, with thermoforming companies developing 100% rPET clamshells that deliver the same transparency, impact resistance, and performance as virgin plastic formats. As consumer scrutiny rises, mono-material clamshells with recycled inputs are no longer optional they are quickly becoming a baseline requirement for market participation.

Adoption of Advanced Anti-Theft and Anti-Counterfeit Features

With organized retail crime (ORC) and counterfeit goods rising globally, clamshell packaging is being re-engineered for enhanced security functionality. Innovations in irreversible locking mechanisms ensure that tampering is immediately visible, creating a clear deterrent against theft while preserving product visibility. For high-value categories such as consumer electronics and luxury accessories, manufacturers are integrating cavities into clamshells to accommodate electronic security devices, allowing retailers to protect goods without compromising merchandising.

Anti-counterfeit applications are also gaining traction, with clamshell surfaces being leveraged for holographic seals, laser etching, and serialized identifiers. These features not only protect brand integrity but also build consumer trust by providing instant authenticity verification. As retail theft costs escalate and counterfeit markets expand, secure clamshell packaging is becoming a critical differentiator for brands competing in electronics, personal care, and specialty consumer goods markets.

Development of High-Performance, Curbside-Recyclable Paper-Based Alternatives

Plastic-free packaging mandates are creating an unprecedented opportunity for paper-based clamshell alternatives. Advances in molded fiber technology are enabling trays and clamshells manufactured from bagasse, recycled paperboard, and other natural fibers to achieve durability levels comparable to plastic while offering full curbside recyclability. This makes them particularly attractive for non-food sectors such as electronics, hardware, and personal care. Hybrid designs are also emerging as a scalable compromise, featuring a recyclable paperboard base with a removable PET window for visibility. These solutions align with retailer mandates for reduced plastic while meeting consumer demand for transparent packaging. Major technology brands such as Microsoft and Sony are accelerating this transition, with sustainability commitments that prioritize eliminating plastic packaging from their supply chains. With corporate adoption driving scale, paper-based clamshell packaging stands as one of the most promising high-volume growth areas in the market.

Integration of Smart Features for Enhanced Consumer Engagement and Supply Chain Visibility

"The clamshell’s expansive, printable surface area is being transformed into a digital engagement platform. Brands are embedding QR codes that allow consumers to access product origin details, sustainability claims, and digital manuals, directly linking packaging to transparency initiatives. In retail studies, consumers reported a high willingness to scan such codes, demonstrating their effectiveness in influencing purchasing decisions.

Competitive Landscape: Key Players Driving Clamshell Packaging Innovation

The clamshell packaging market features global leaders and specialized regional players, each leveraging sustainability, innovation, and customer-centric designs to remain competitive.

Amcor Plc strengthens sustainable clamshell packaging portfolio

Amcor offers flexible and rigid clamshells for foodservice, fresh produce, and personal care, with a strong focus on AmPrima® recycle-ready structures. In August 2025, Amcor upgraded its UK recycling facility to enhance PCR supply while launching new designs that cut carbon intensity. Its vented clamshells extend produce shelf life, while eco-materials improve brand ESG scores. Amcor’s global scale and partnerships enable end-to-end integration from design to mass production.

Sonoco Products Company expands with fiber-based and thermoformed clamshells

Sonoco has a diversified portfolio across rigid paper, thermoformed plastics, and industrial packaging, with clamshells central to its food packaging division. Following its Eviosys acquisition in 2025, Sonoco expanded into metal and hybrid solutions, broadening its global reach. Its EnviroSense® platform underscores commitment to recyclability and consumer safety. Sonoco differentiates by delivering durable, shelf-appeal packaging aligned with sustainability mandates.

Placon Corporation pioneers PCR-based retail clamshell packaging

Placon is a North American specialist with flagship solutions such as the BlisterBox™ for retail. In 2025, it invested in new facilities dedicated to medical-grade clamshells, expanding its footprint in healthcare. Its sustainability focus is unmatched, integrating 75%+ PCR PET, diverting millions of bottles from landfills. Industry recognition and awards validate Placon’s innovation in high-clarity, functional packaging tailored to both retail and medical markets.

Sabert Corporation scales foodservice-focused clamshell innovations

Sabert specializes in food-to-go and deli packaging, with clamshells like the Kraft Fluted Clamshell widely used across prepared meal and grab-and-go segments. With the April 2025 Colpac acquisition, it expanded its paper-based clamshell line in Europe. Its PulpUltra launch (September 2025) reinforced its leadership in plant-based, PFAS-free clamshells. Sabert is positioned as a go-to for high-performance, presentation-ready foodservice packaging.

Hannan Products Corporation delivers integrated clamshell packaging systems

Hannan is a specialized provider known for its blister and clamshell systems, offering both packaging formats and sealing machinery such as PRO PACK and MED PACK. Its focus on cost-effective, scalable systems reduces complexity for SMEs and contract manufacturers. Recent strategy centers on instant tooling changeovers and simplified controls, making clamshell production more efficient for diverse product lines. Hannan’s system-based innovation helps reduce total packaging costs and speeds up prototyping-to-production cycles.

Clamshell Packaging Market Share Insights

PET Leads Market Share by Material in the Clamshell Packaging Industry

Polyethylene Terephthalate (PET) dominates the clamshell packaging market with a 40% share in 2025, underscoring its role as the industry’s material of choice. PET is valued for its crystal-clear visibility, strong barrier properties, and mechanical strength, making it the go-to material for electronics, consumer goods, and premium retail applications. Its recyclability and increasing availability in recycled form (rPET) strengthen its position, particularly as brands face growing pressure to reduce virgin plastic use under global sustainability mandates. PVC retains 25% of the market due to its low cost and high clarity, but its share continues to decline as regulatory and recycling challenges drive substitution toward PET and sustainable alternatives. Molded fiber and bioplastics like PLA and PHA represent the fastest-growing segments, fueled by retailer and brand commitments to plastic reduction. Molded fiber is gaining traction in fresh produce and electronics packaging for its compostability and natural aesthetics, while PLA-based bioplastics appeal to eco-conscious brands seeking marketing differentiation. Polypropylene (PP) and polystyrene (PS) play niche roles, with PP used in specific applications requiring flexibility and toughness, and PS steadily losing ground due to brittleness and negative public perception. Together, these material dynamics reflect a market in transition, balancing performance requirements with urgent sustainability demands.

Electronics Drive the Largest Market Share by Application for Clamshell Packaging

Electronics and electrical applications account for 30% of the global clamshell packaging market in 2025, making it the largest and most valuable segment. Clamshells are indispensable for protecting high-theft items such as headphones, chargers, and accessories while maintaining full product visibility a critical requirement in the consumer electronics retail environment. PET clamshells dominate this space due to their clarity, durability, and tamper-evident properties. Food and beverage packaging follows with a 25% share, where clamshells are widely used for fresh produce, bakery items, and ready-to-eat meals. This segment is also the primary driver of molded fiber adoption, as retailers shift toward compostable options for berries, salads, and prepared foods to align with sustainability regulations. Consumer goods and cosmetics rely heavily on clamshell packaging as branding tools, leveraging their visibility and structural rigidity to enhance shelf appeal and justify premium pricing. In cosmetics and personal care, clamshells support trial visibility and enhance luxury positioning through design innovations. Healthcare and pharmaceutical applications, though smaller, represent a high-value niche, where sterile kits, surgical tools, and unit-dose medicines require packaging that combines clarity, sterility maintenance, and tamper evidence. Across all applications, clamshell packaging continues to be a strategic enabler, balancing protection, visibility, and brand differentiation.

United States: Sustainability, E-Commerce, and Thermoforming Driving Clamshell Packaging Growth

The United States is leading the clamshell packaging market through innovation in sustainable materials and advanced manufacturing. A major shift is underway as companies replace traditional plastics with eco-friendly alternatives like recycled polyethylene terephthalate (rPET) and molded fiber from sugarcane bagasse. This transition reflects both corporate sustainability commitments and rising consumer demand for greener packaging solutions. At the same time, tamper-evident clamshell packaging designs are gaining traction across industries such as food, pharmaceuticals, and electronics, where product safety and consumer trust are paramount.

Technological advancement in thermoforming has made the U.S. a hub for precision-engineered clamshell packaging. Manufacturers are adopting high-speed machinery that improves customization, reduces waste, and enhances efficiency in large-scale production. Another transformative factor is the country’s booming e-commerce and meal-kit delivery sector, where durable clamshell designs protect goods during multiple handling stages while maintaining product integrity and visual appeal. These combined trends firmly position the U.S. as a global innovation leader in clamshell packaging.

China: Global Manufacturing Hub Fueling E-Commerce and Food Packaging Demand

China’s dominance in global manufacturing makes it a cornerstone of the clamshell packaging market. With its massive production capacity and cost-efficient processes, the country not only meets surging domestic demand but also serves as a key export hub for clamshells used in consumer goods, electronics, and food products worldwide. The rising popularity of convenience foods in urban centers such as ready-to-eat meals, salads, and fresh produce has accelerated demand for clamshell formats that combine visibility with freshness.

China’s thriving e-commerce ecosystem further strengthens its clamshell packaging market. Packaging durability and cost-effectiveness are essential for last-mile delivery, driving innovation in lightweight, high-strength clamshells. To keep pace with this scale, Chinese manufacturers are investing heavily in automation and robotics for thermoforming, ensuring both volume efficiency and quality control. This combination of demand-side growth and supply-side technological adoption secures China’s place as a global leader in clamshell packaging solutions.

Germany: Regulatory Compliance and Precision Materials Shaping the Market

Germany’s clamshell packaging industry is heavily shaped by European Union regulations, particularly the Packaging and Packaging Waste Regulation (PPWR), which emphasizes recyclability and the circular economy. German companies are responding by integrating higher levels of recycled content into clamshell packaging and designing solutions that align with stringent EU sustainability targets. This regulatory-driven innovation is positioning Germany as a key model for sustainable packaging compliance in Europe.

At the same time, Germany’s industrial landscape dominated by electronics and automotive manufacturing demands specialized clamshell packaging for high-value applications. Anti-static clamshells for sensitive electronics and custom-molded designs for automotive parts are particularly important. Additionally, advanced materials with enhanced barrier properties are being developed to ensure product safety without sacrificing recyclability. This balance of regulatory leadership and industry-specific innovation ensures Germany’s continued growth in premium clamshell packaging markets.

India: Sustainable Solutions and Food Delivery Services Accelerating Adoption

India’s clamshell packaging market is experiencing rapid growth, driven by government-led sustainability initiatives and an expanding food and beverage sector. The government’s strict plastic waste management regulations are encouraging manufacturers to adopt biodegradable and compostable clamshell packaging, often made from agricultural residues like sugarcane bagasse. This not only reduces environmental impact but also aligns with India’s long-term waste reduction strategies.

The booming food delivery and fast-food industries represent the largest consumer of clamshell packaging in India. With rising urbanization and lifestyle changes, demand for packaged, ready-to-eat meals has surged, making clamshells a preferred choice for convenience and hygiene. Domestic manufacturers are responding with capacity expansion and investment in modern machinery to produce diverse clamshell solutions ranging from fresh produce packaging to premium food service trays. This synergy between regulatory pressure and consumer trends is making India a fast-emerging hotspot in the global clamshell packaging industry.

Japan: Precision Manufacturing and Circular Economy Principles Defining the Market

Japan’s clamshell packaging market is characterized by high standards of precision and quality, particularly for premium applications such as electronics, cosmetics, and gourmet foods. Packaging designs emphasize both aesthetics and superior protection, reflecting the Japanese consumer’s preference for functionality combined with visual appeal. The country’s reputation for advanced manufacturing ensures consistency and innovation across clamshell packaging solutions.

Material science and technological innovation are at the forefront of Japan’s market growth. Companies are developing advanced polymers and composites that improve clarity, barrier properties, and durability while aligning with Japan’s strong circular economy framework. With one of the most efficient recycling infrastructures in the world, Japanese packaging firms are designing clamshells optimized for recyclability and easy collection, minimizing environmental footprint while meeting consumer and regulatory expectations. This focus on precision, sustainability, and innovation solidifies Japan’s role as a premium clamshell packaging market leader in Asia.

Clamshell Packaging Market Report Scope

Clamshell Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.5 Billion

|

|

Market Size (2034)

|

$14.4 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Material (Polyethylene Terephthalate, Polypropylene, Polystyrene, Polyvinyl Chloride, Molded Fiber, Bioplastics), By Application (Food & Beverage, Electronics & Electrical, Healthcare & Pharmaceuticals, Cosmetics & Personal Care, Consumer Goods, Others), By Closure Type (Snap Lock, Hinged, Slide Lock)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., Novolex, Sonoco Products Company, Sabert Corporation, Placon, DS Smith plc, Genpak, LLC, Dordan Manufacturing Company, WestRock Company, Pactiv Evergreen Inc., Lacerta Group, Fabri-Kal, Inline Plastics Corp., Nelipak Healthcare Packaging

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Clamshell Packaging Market Segmentation

By Material

- Polyethylene Terephthalate

- Polypropylene

- Polystyrene

- Polyvinyl Chloride

- Molded Fiber

- Bioplastics

By Application

- Food & Beverage

- Electronics & Electrical

- Healthcare & Pharmaceuticals

- Cosmetics & Personal Care

- Consumer Goods

- Others

By Closure Type

- Snap Lock

- Hinged

- Slide Lock

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Clamshell Packaging Market

- Amcor plc

- Berry Global Inc.

- Novolex

- Sonoco Products Company

- Sabert Corporation

- Placon

- DS Smith plc

- Genpak, LLC

- Dordan Manufacturing Company

- WestRock Company

- Pactiv Evergreen Inc.

- Lacerta Group

- Fabri-Kal

- Inline Plastics Corp.

- Nelipak Healthcare Packaging

* List Not Exhaustive

Research Coverage

This comprehensive report by USDAnalytics investigates the global clamshell packaging market, analyzing breakthroughs in sustainable materials, thermoforming efficiency, and foodservice adoption that are reshaping the sector. The report reviews market dynamics, strategic partnerships, regulatory compliance, and emerging innovations such as high-PCR PET integration, plant-based fiber alternatives, and smart anti-theft features. It highlights key drivers influencing growth, including the transition toward circular economy objectives, advanced tooling for customized clamshell formats, and the adoption of high-performance, curbside-recyclable paper-based solutions. This report is an essential resource for industry professionals seeking actionable insights into market trends, competitive strategies, and regional developments from established players like Amcor, Sonoco, Placon, Sabert, and Hannan Products, enabling informed procurement, design, and investment decisions. Analysis reviews the evolving applications across food & beverage, electronics, healthcare, cosmetics, and consumer goods, while spotlighting material shifts toward PET, molded fiber, and bioplastics. With detailed examination of sustainability mandates, e-commerce growth, and automation-driven efficiency, this report equips stakeholders to navigate the market’s regulatory, technological, and operational landscape. Historic data from 2021 to 2024 and forecast projections from 2025 to 2034 provide a robust foundation for strategic planning, while the evaluation of competitive moves, mergers, acquisitions, and innovations highlights actionable opportunities across regions.

Scope Highlights

- Segmentation: By Material (Polyethylene Terephthalate, Polypropylene, Polystyrene, Polyvinyl Chloride, Molded Fiber, Bioplastics), By Application (Food & Beverage, Electronics & Electrical, Healthcare & Pharmaceuticals, Cosmetics & Personal Care, Consumer Goods, Others), By Closure Type (Snap Lock, Hinged, Slide Lock)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic & Forecast Data: Covers 2021–2024 (historical) and 2025–2034 (forecast)

- Companies: Analysis and profiles of 15+ companies including Amcor plc, Berry Global Inc., Novolex, Sonoco Products Company, Sabert Corporation, Placon, DS Smith plc, Genpak LLC, Dordan Manufacturing Company, WestRock Company, Pactiv Evergreen Inc., Lacerta Group, Fabri-Kal, Inline Plastics Corp., Nelipak Healthcare Packaging

Methodology

The research methodology employed in this report integrates both qualitative and quantitative approaches to provide a robust and actionable assessment of the global clamshell packaging market. Data was collected from primary sources, including interviews with industry executives, packaging engineers, and procurement specialists, as well as secondary sources such as company reports, regulatory filings, trade associations, and industry journals. Market sizing and forecast modeling were conducted using bottom-up and top-down approaches, incorporating historical consumption trends, production capacity, material innovations, and regional adoption patterns. Competitive landscape analysis was performed through benchmarking of product portfolios, sustainability initiatives, and operational capabilities of key players. Cross-validation techniques ensured consistency between market projections, regulatory impacts, and emerging innovation trends, while scenario analysis addressed potential market risks related to material costs, regulatory shifts, and technological adoption. This methodical framework allows USDAnalytics to provide a highly reliable, forward-looking perspective for stakeholders seeking strategic guidance in clamshell packaging investments, product development, and sustainability planning.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.